Sample Category Title

Bad News is Bad News

September began on an ugly note, to say the least. The US equities tumbled after the latest ISM data showed a fifth month of contraction in the US manufacturing, and at accelerated pace. The latter revived the recession worries ahead of this week’s critical US jobs data, and sent the S&P500 more than 2% down. This was the worst selloff since August 5, when a weak jobs data from the US had boosted the recession worries, the expectation of a 50bp cut from the Federal Reserve (Fed) and resulted in an almost 10% selloff of the S&P500. The technology stocks led losses, yesterday. Nasdaq 100 dived more than 3%, as Nvidia tumbled nearly 10% as part of the broader macroeconomic worries and suspected AI fatigue, and another 2.42% in the afterhours trading on news that the DoJ sent subpoenas to the company because it suspects that Nvidia violated antitrust laws, made switching harder to other chipmakers and penalized companies that didn’t use Nvidia’s AI chips exclusively. In Asia, TSM tumbled 5%, and SK Hynix fell more than 8%.

Now we know that the antitrust allegations are part of the daily life of all Big Tech companies. They come and go without doing too much harm to these Big Tech’s growth potentials as many of them are natural monopolies and others naturally benefit from their dominant market positions. But the news come at a time when Nvidia is vulnerable. Just a week ago, the company released blowout results. They exceeded their own sales forecast by $2bn for the fifth consecutive quarter, gave a strong – and a stronger-than-expected – forecast for the current quarter, announced a big stock buyback and addressed issues regarding the delay of the Blackwell chip saying that there is nothing to be worried about. But yet, the stock price fell as investors focused on potential problems – like what if the Big Tech cut their AI spending. But hey, the Big AI spenders like Meta and Google said that they will continue to spend big – and overspend if necessary – to make their AI investments worth. What I am trying to say here is that, except the DoJ news, recent news from Nvidia could’ve been interpreted in a positive way, but they have not. To me, this is a sign of fatigue.

And it’s in the middle of this bad mood that Broadcom is preparing to announce good results this week thanks to a rebound in networking equipment sales like Cisco and conversion from perpetual licenses to subscription model for VMware, acquired last year. Unfortunately, good results may not lead to a positive market reaction... The stock already tanked more than 6% yesterday, and no one can guarantee that good looking results would reverse the selloff...

... because the broad macroeconomic environment is not necessarily supportive of risk appetite right now.

Bad news is bad news for everyone

The slowing US growth and soft data boost the recession worries and rate cut expectations. The rate cut expectations favour a sector rotation from highly valued Big Tech toward the non-tech pockets of the market. BUT the expectation of jumbo rate cut is bad for all stocks, regardless of their technology exposure. Yesterday, Nasdaq certainly recorded the biggest loss but the Dow Jones fell 1.5% from an ATH and the Russell 2000 dropped 3%. Bad news is bad news for everyone.

In bonds, the US 2-year yield fell to 3.85% as expectations of a jumbo cut rose on yesterday’s data, the probability of a 50bp cut from the Fed in September rose above 40%, the 10-year yield retreated to 3.82% and the 30-year yield fell to 4.10%. All eyes are on the US jobs data – which has the potential to either make things worse or throw a floor under the recent risk selloff. Today, the job openings data is expected to show fewer job openings. On Thursday and Friday, the ADP and the official jobs data are expected to show a rebound in hiring and wages. And good news will be good news when the US reveals its latest jobs figures this week.

FX and Energy

Crude oil tumbled more than 5% yesterday and is testing the $70pb support to the downside. Rising recession worries, the expectation of waning global demand, prospects of fewer production restrictions from OPEC, combined with the falling tensions in Libya that could allow half a million barrels return to the market, are weighing on oil prices this morning. I believe that sufficiently strong jobs data between now and Friday could bring the dipbuyers to the market, yet if the jobs data looks ugly, we could see US crude settle below the $70pb for a while.

In the FX, the falling US yields didn’t pull the dollar index lower yesterday, as the greenback benefited from risk-off inflows. As such, the EURUSD extended losses to 1.1026 as Cable tipped a toe below 1.31. Both are better bid this morning. A soft set of economic data from the US could bring the USD bears back to the market, but if the market shifts to the panic mode, the dollar selloff could remain limited.

All Eyes on JOLTs Labour Market Data

In focus today

In the US, markets will pay close attention to the JOLTs labour market data for July. The Fed has highlighted the number of job vacancies as a key measure of labour market tightness, with the latest data signalling cooling labour demand but still low levels of actual layoffs.

In Sweden, the Prospera inflation survey will be published at 8:00 CET followed by the services PMI at 8:30. We expect the survey result will show expectations roughly in line with the 2% target for the CPIF index, with risk skewed to the downside, increasing the pressure on Riksbank to cut more aggressively. For the PMI, we project an almost unchanged level compared to 53.8 in July.

The Polish central bank will kick off the slew of September central bank meetings. We and markets project an unchanged rate decision at 5.75%.

Overseas, Bank of Canada will also announce their key policy rate, where we expect a rate cut of 25bp, bringing its policy rate to 4.25% - in line with markets.

Overnight, we get Japanese July wage data, which will reflect the strength of the spring pay increases. The details in the wage data will be key for the inflation outlook and important for the Bank of Japan's decision making in H2.

Economic and market news

What happened yesterday

In the US, the ISM manufacturing PMI for August printed slightly weaker than expected at 47.2 (cons: 47.5). The details were even less optimistic, with the order-inventory balance plunging into contraction (in line with PMIs released earlier) which tends to be a negative leading signal for manufacturing production. Price and employment indices climbed higher, but it should be noted that the realized employment growth in the manufacturing sector has remained weak, and goods prices have continued to record deflation over the past few months.

In Switzerland, a batch of data was released. Headline inflation for August was lower than expected at 1.1% (cons: 1.2%) while core remained steady at 1.1% (cons: 1.1%), implying that Q3 inflation is set to print markedly lower than the SNB's latest forecast at 1.5%. Additionally, monthly momentum crept lower in both headline and core. GDP for Q2 came in at 0.5% q/q (adjusted for sporting events), aligning with expectations.

On the commodities front, oil prices tumbled some 4%, nearing their lowest level since early 2024. Several factors contributed to the downtick, including souring global risk sentiment, a stronger USD and concerns regarding the planned OPEC+ output raises next month. Additionally, Bloomberg reported that a deal is close to resolving the dispute halting Libyan oil activities, with exports and production being curtailed early this week amid an ongoing rift between rival political factions over control of the central bank and oil revenue.

Equities: Global equities declined by 1.5% yesterday in a full-blown, classic risk-off session, marked by significant cyclical underperformance driven by sectors such as tech, growth, and momentum. In contrast, minimum volatility stocks experienced one of their best days this year in relative terms, with true defensive industries ending higher in the US. Yields were lower across the curve, predominantly driven by the long end. The VIX saw a 5-point jump as equities consistently drifted lower throughout the session, closing near day lows. We term this classic risk-off due to the correlations observed across various asset classes, including the negative bond/equity correlation, driven by concerns over growth and demand rather than inflation. Yesterday market action revealed more about investors' positioning and sentiment than the impact of a soft ISM number. In the US yesterday, Dow -1.5%, S&P 500 -2.1%, Nasdaq -3.3%, Russell 2000 -3.1%. Asian markets were sharply lower this morning, with cyclical leaders Japan, Taiwan, and South Korea all down more than 3%.

FI: Declining oil prices, affecting both the linkers and the nominal bonds, sent yields markedly lower from the early afternoon, with 10y German bunds ending 7bp lower at 2.27%. Markets added 5bp to ECB pricing by end 2025. Yesterday, ECB's Simkus said that an October rate cut was quite unlikely. Markets are pricing 8bp for that meeting. The 2086 Austrian bond auction resulted in an outperformance relative to European peers in the long end. Today focus turns to the US JOLTS report as well as Villeroy is set to be on the wires (13:00 CET).

FX: Risk-off sentiment pushed the USD, JPY and CHF higher during yesterday's session with a lower-than-expected Swiss CPI failing to prove a substantial headwind for the CHF. NOK and SEK were among the worst performers with EUR/NOK breaching the 11.80 mark. Oil prices plunged yesterday with risk sentiment, a stronger dollar and concerns over whether OPEC+ will proceed with planned output hike next month caused headwinds.

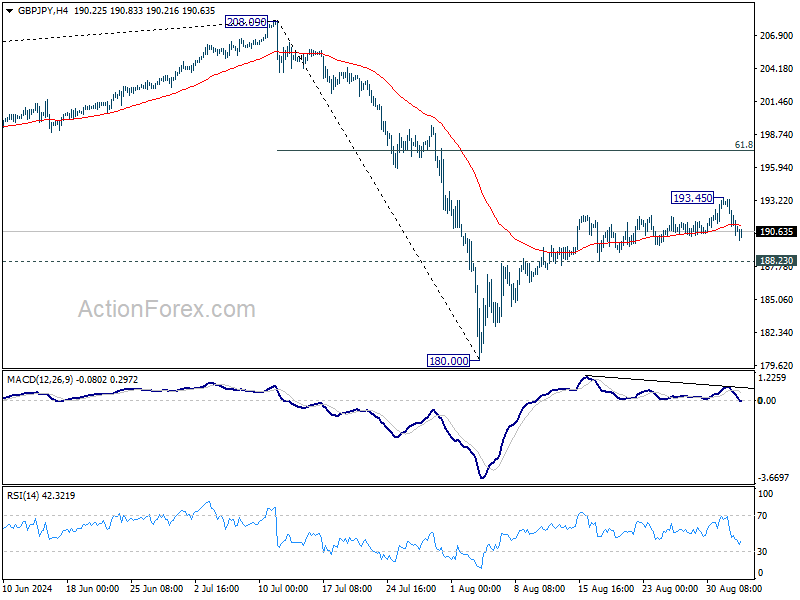

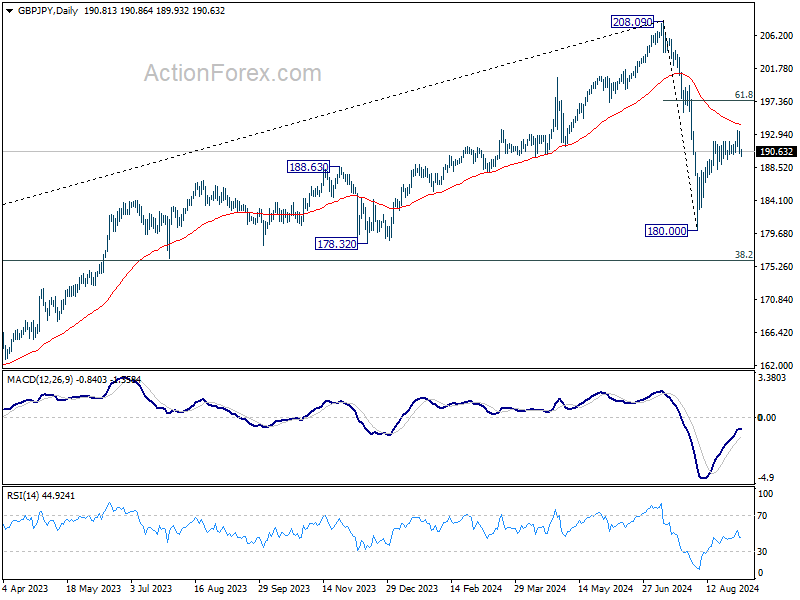

GBP/JPY Daily Outlook

Daily Pivots: (S1) 189.61; (P) 191.49; (R1) 192.66; More...

Intraday bias in GBP/JPY is turned neutral first with current retreat. On the upside, above 193.45 will resume the rebound from 180.00 to 61.8% retracement of 208.09 to 180.00 at 197.35. However, firm break of 188.23 support will argue that rebound from 180.00 has completed, and turn bias back to the downside for retesting 180.00 instead.

In the bigger picture, price actions from 208.09 are seen as a correction to whole rally from 123.94 (2020 low). Current development suggests that the first leg has completed and the range of medium term consolidation should be set between 38.2% retracement of 123.94 to 208.09 at 175.94 and 208.09.

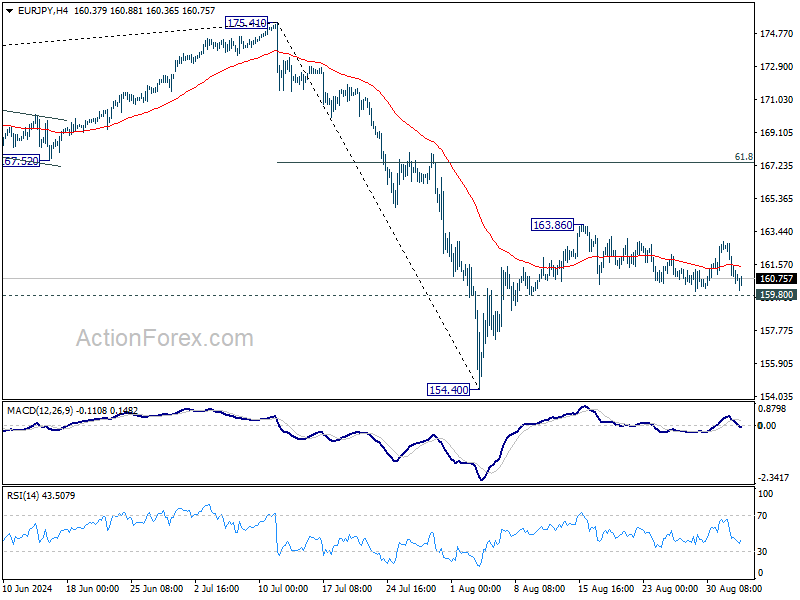

EUR/JPY Daily Outlook

Daily Pivots: (S1) 159.83; (P) 161.31; (R1) 162.13; More....

EUR/JPY is still bounded in range of 159.80/163.86 and intraday bias remains neutral. On the upside, break of 163.86 will target 61.8% retracement of 175.41 to 154.40 at 167.38, as the second leg of the corrective pattern from 175.41. On the downside, however, firm break of 159.80 support will suggest that the rebound from 154.40 has completed, and turn bias back to the downside for 154.40 instead.

In the bigger picture, price actions from 175.41 are seen as correction to rally from 114.42 (2020 low). Current development suggests that the first leg has completed. The range of consolidation should be seen between 38.2% retracement of 114.42 to 175.41 at 152.11 and 175.41 high.

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8406; (P) 0.8420; (R1) 0.8435; More...

EUR/GBP is staying in consolidation from 0.8399 and intraday bias remains neutral. Stronger recovery cannot be ruled out but further decline is expected as long as 0.8466 minor resistance holds. Below 0.8399 will resume the fall from 0.8624 and target 0.8382 support. Firm break there will resume larger down trend.

In the bigger picture, as long as 0.8624 resistance holds, down trend from 0.9267 is expected to continue. Firm break of 0.8382 will target 0.8201 (2022 low). However, decisive break of 0.8624 will indicate that such down trend has completed, and turn outlook bullish for 0.8764 resistance next.

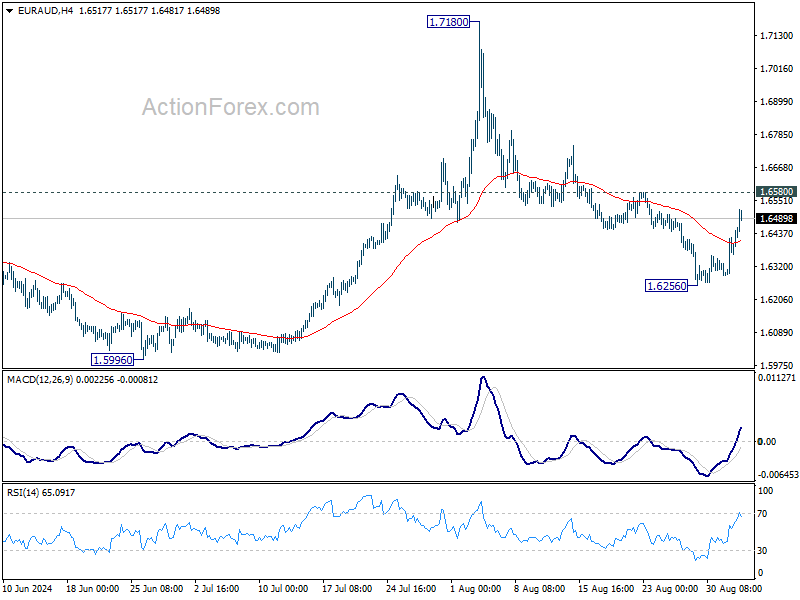

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6346; (P) 1.6403; (R1) 1.6510; More...

While EUR/AUD's rebound from 1.6256 extended, upside is capped below 1.6580 resistance so far. Intraday bias remains neutral and fall from 1.7180 is still in favor to continue. On the downside, break of 1.6256 support will target 1.5996 key support level next. However, decisive break of 1.6580 will turn bias back to the upside for stronger rebound.

In the bigger picture, outlook is mixed up by the deeper than expected fall from 1.7180. Yet as long as 1.5996 support holds, up trend from 1.4281 (2022 low) is still expected to resume at a later stage. Firm break of 1.7180 will pave the way to 61.8% projection of 1.4281 to 1.7062 from 1.5996 at 1.7715.

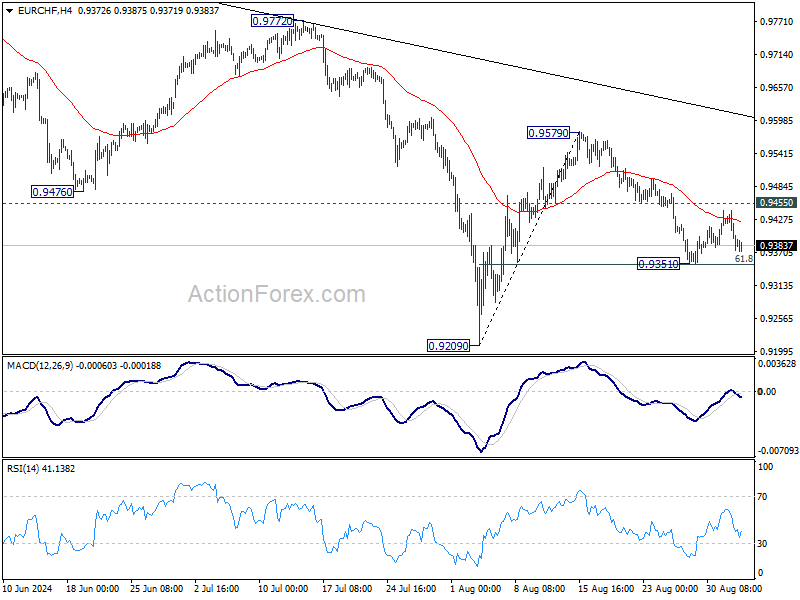

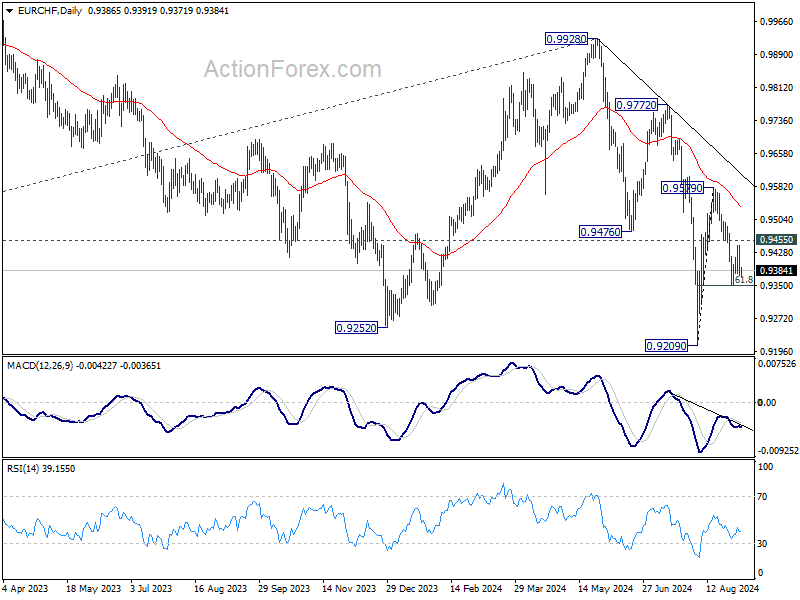

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9361; (P) 0.9403; (R1) 0.9430; More....

No change in EUR/CHF's outlook and intraday bias stays neutral first. As noted before, rebound from 0.9209 could have completed at 0.9579 already. Deeper fall is expected as long as 0.9455 minor resistance holds. Break of 0.9351 will target 0.9209 low next. However, break of 0.9497 will turn bias back to the upside for 0.9579 resistance instead.

In the bigger picture, medium term corrective pattern from 0.9407 (2022 low) might have completed with three waves to 0.9928. Decisive break of 0.9252 (2023 low) will confirm long term down trend resumption. Next target will be 61.8% projection of 1.1149 to 0.9407 from 0.9928 at 0.8851. For now, outlook will stay bearish as long as 0.9928 resistance holds, even in case of strong rebound.

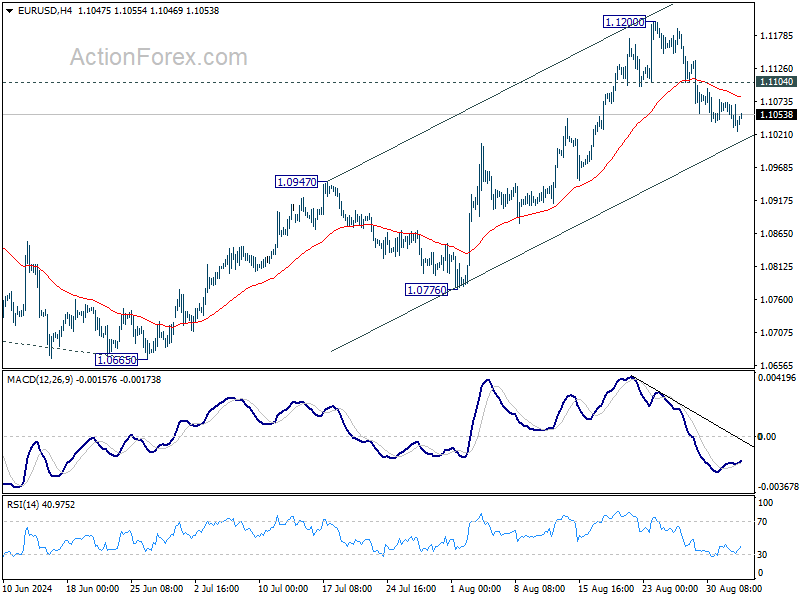

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1018; (P) 1.1051; (R1) 1.1075; More....

No change in EUR/USD's outlook for now. While retreat from 1.1200 might extend lower, rally from 1.0665 is in favor to continue as long as 1.0947 resistance turned support holds. Above 1.1104 minor resistance will bring retest of 1.1200 first. Break there will target 1.1274 high next. However, firm break of 1.0947 will indicate reversal and turn bias back to the downside.

In the bigger picture, prior break of 1.1138 resistance indicates that corrective pattern from 1.1274 has completed at 1.0665 already. Decisive break of 1.1274 (2023 high) will confirm whole up trend from 0.9534 (2022 low). Next target will be 61.8% projection of 0.9534 to 1.1274 from 1.0665 at 1.1740. This will now be the favored case as long as 1.0947 resistance turned support holds.

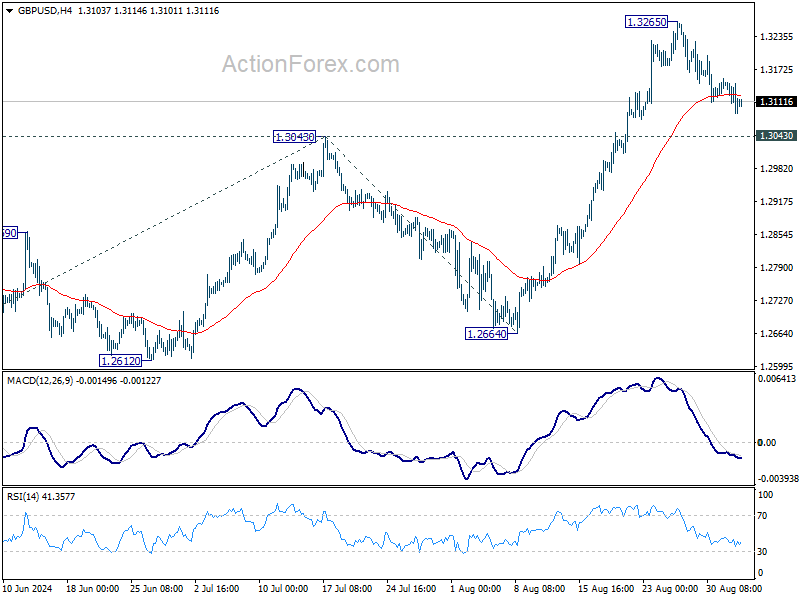

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3084; (P) 1.3119; (R1) 1.3150; More...

Outlook in GBP/USD remains unchanged as consolidation from 1.3265 is still extending. Intraday bias remains neutral for the moment. While deeper retreat cannot be ruled out, downside should be contained well above 1.3043 resistance turned support to bring rebound. On the upside, above 1.3265 will resume larger up trend to 100% projection of 1.2298 to 1.3043 from 1.2664 at 1.3409. However, firm break of 1.3043 will indicate short term topping and turn bias back to the downside for deeper pullback.

In the bigger picture, up trend from 1.0351 (2022 low) is resuming. Next target is 38.2% projection of 1.0351 to 1.3141 from 1.2298 at 1.3364. For now, outlook will stay bullish as long as 1.2664 support holds, even in case of deep pullback.

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8474; (P) 0.8506; (R1) 0.8534; More…

No change in USD/CHF's outlook and intraday bias stays neutral for now. Further decline is expected as long as 0.8540 resistance holds. Break of 0.8339 will resume the fall from 0.9223 and target 0.8332 low. However, considering bullish convergence condition in 4H MACD, firm break of 0.8540 will confirm short term bottoming, and turn bias back to the upside for 0.8747 resistance instead.

In the bigger picture, price actions from 0.8332 (2023 low) are currently seen as a medium term corrective pattern, with fall from 0.9223 as the second leg. Strong support could be seen from 0.8332 to bring rebound. Yet, overall outlook will continue to stay bearish as long as 0.9243 resistance holds. Firm break of 0.8332, however, will resume larger down trend from 1.0146 (2022 high).