Sample Category Title

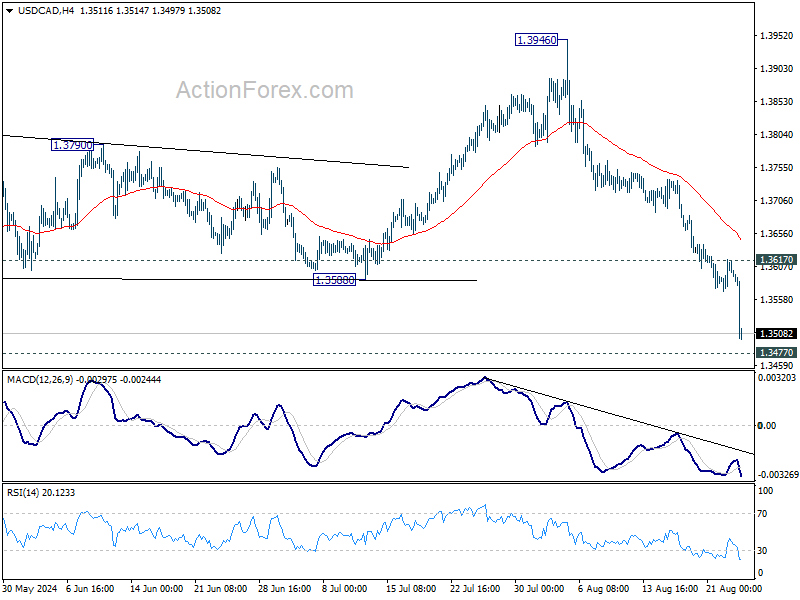

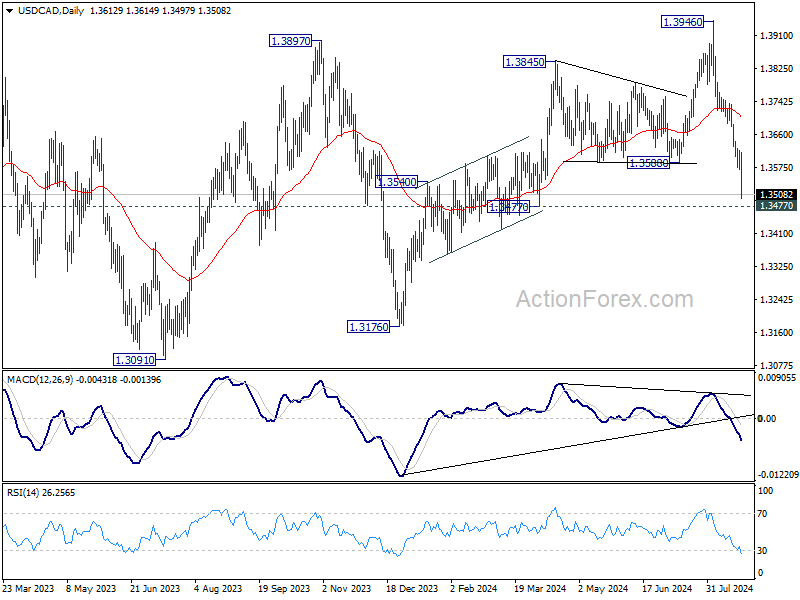

USD/CAD Weekly Outlook

USD/CAD's steep decline and strong break of 1.3588 support argues that while rise from 1.3176 has completed already. Fall from 1.3946 is seen as another falling leg inside medium term range pattern. Initial bias stays on the downside this week for 1.3477 support. Firm break there will target 1.3091/3176 support zone. On the upside, above 1.3617 resistance will turn intraday bias neutral first.

In the bigger picture, current development suggests that corrective pattern from 1.3976 (2022 high) is extending with another falling leg. While deeper decline could be seen, strong support should emerge above 1.2947 resistance turned support to bring rebound. Rise from 1.2005 (2021 low) is still in favor to resume at a later stage.

In the longer term picture, price actions from 1.4689 (2016 high) are seen as a consolidation pattern, which might have completed at 1.2005. That is, up trend from 0.9506 (2007 low) is expected to resume at a later stage. This will remain the favored case as long as 1.2947 resistance turned support holds.

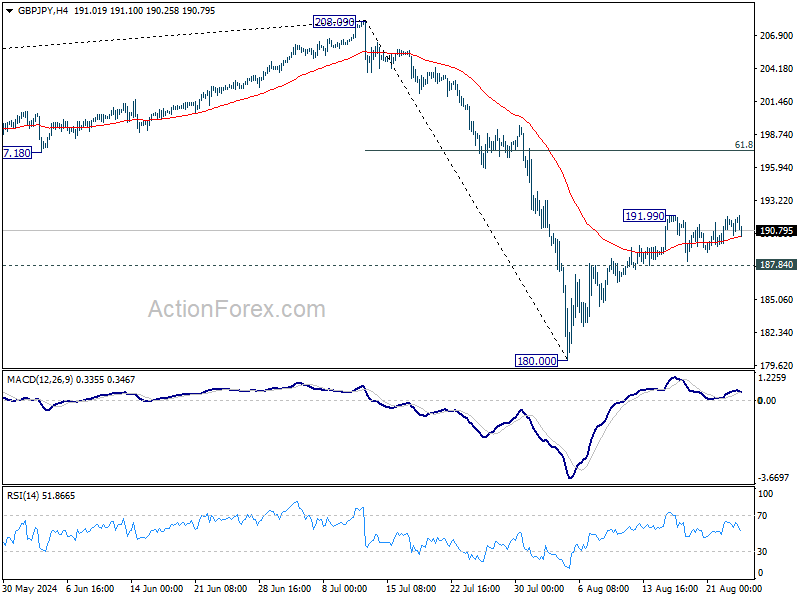

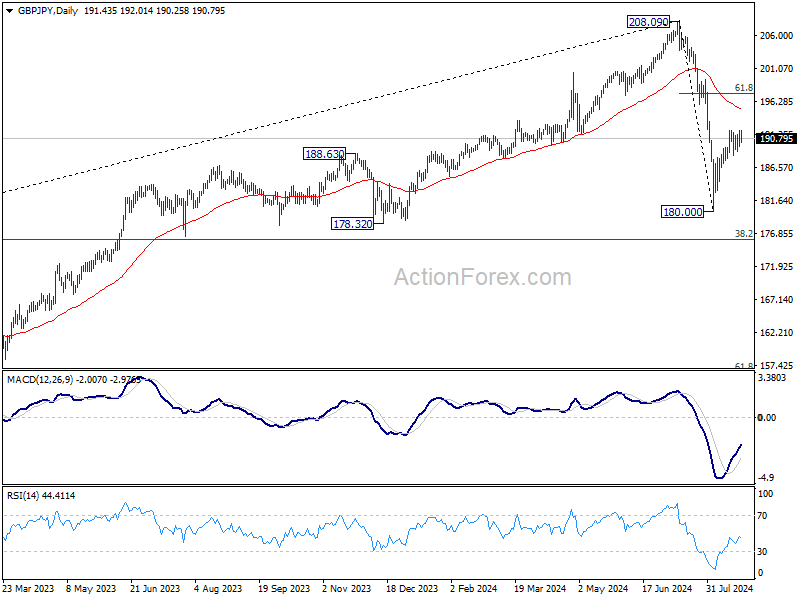

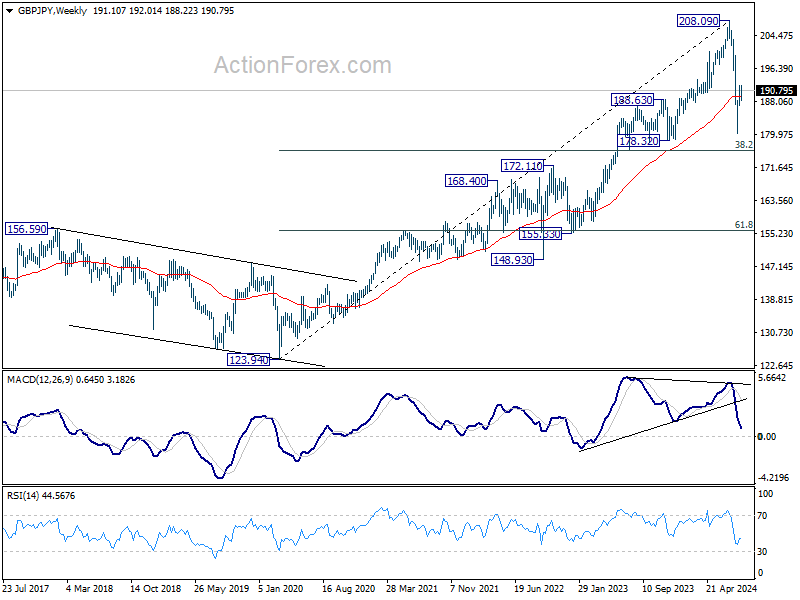

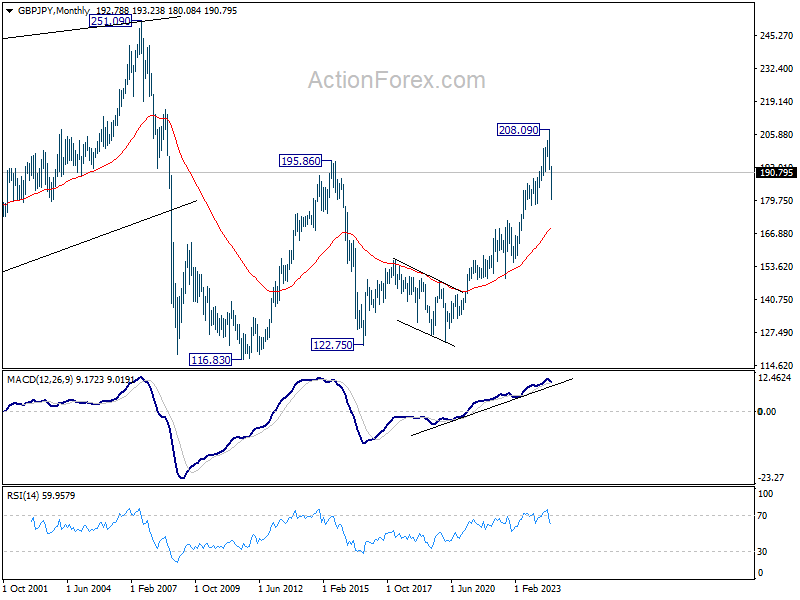

GBP/JPY Weekly Outlook

GBP/JPY stayed in sideway trading below 191.99 last week and outlook is unchanged. Initial bias remains neutral this week first. On the upside, above 191.99 will target 61.8% retracement of 208.09 to 180.00 at 197.35, as the second leg of the corrective pattern from 208.09. On the downside, however, firm break of 187.84 support will argue that rebound from 180.00 has completed, and turn bias back to the downside for retesting 180.00 instead.

In the bigger picture, price actions from 208.09 are seen as a correction to whole rally from 123.94 (2020 low). Current development suggests that the first leg has completed and the range of medium term consolidation should be set between 38.2% retracement of 123.94 to 208.09 at 175.94 and 208.09.

In the longer term picture, considering bearish divergence condition in W MACD, 208.09 is at least a medium term top. It's still early to conclude that the up trend from 122.75 (2016 low) has completed. But it's at least in a medium term corrective phase, with risk of correction to 55 M EMA (now at 169.35).

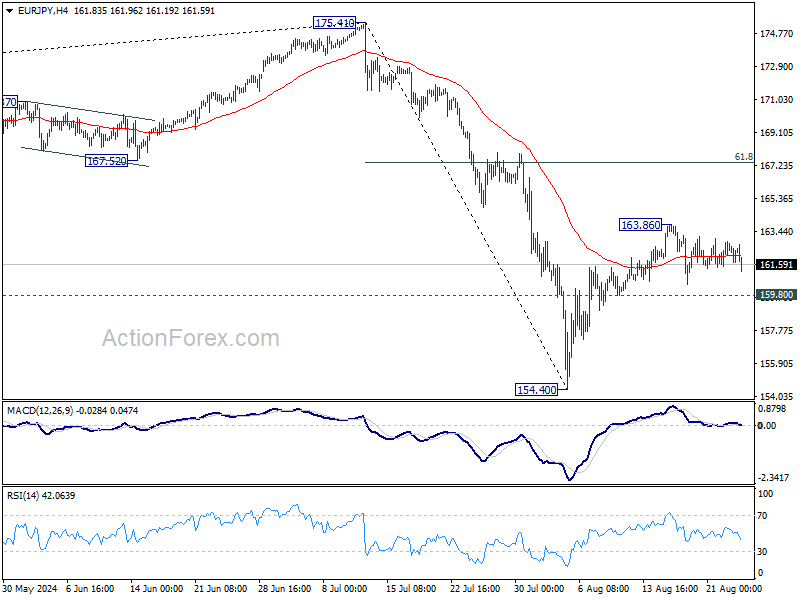

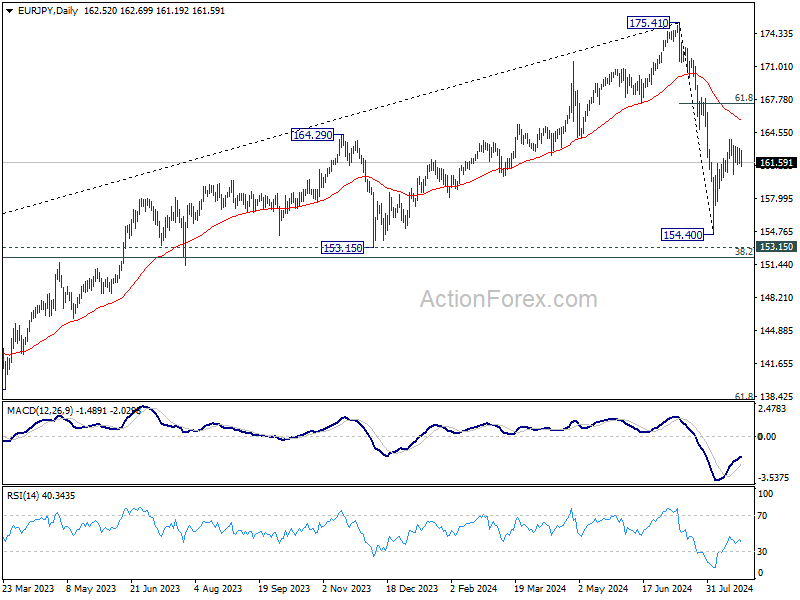

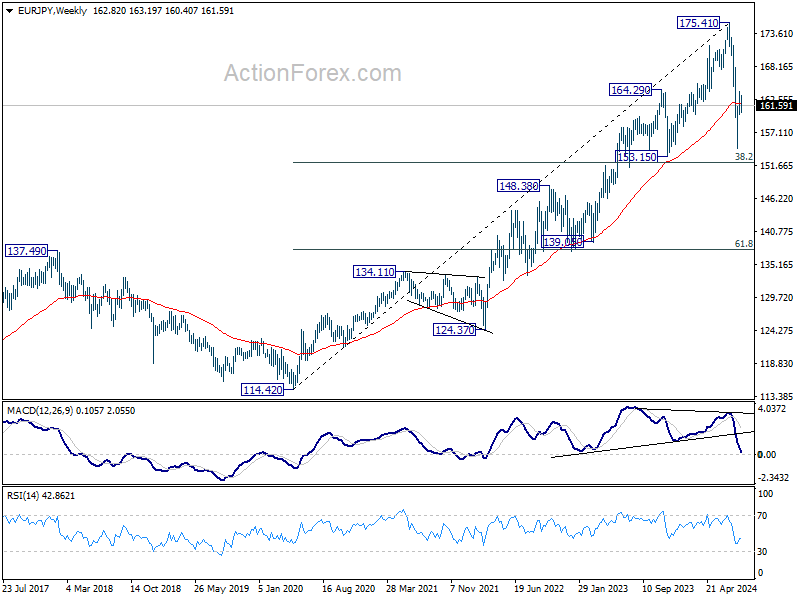

EUR/JPY Weekly Outlook

EUR/JPY stayed in sideway trading below 163.86 last week and outlook is unchanged. Initial bias stays neutral this week first. On the upside, break of 163.86 will target 61.8% retracement of 175.41 to 154.40 at 167.38, as the second leg of the corrective pattern from 175.41. On the downside, however, firm break of 159.80 support will suggest that the rebound from 154.40 has completed, and turn bias back to the downside for 154.40 instead.

In the bigger picture, price actions from 175.41 are seen as correction to rally from 114.42 (2020 low). Current development suggests that the first leg has completed. The range of consolidation should be seen between 38.2% retracement of 114.42 to 175.41 at 152.11 and 175.41 high.

In the long term picture, considering bearish divergence condition in W MACD, 175.41 is at least a medium term top. It's still early to conclude that up trend from 94.11 (2012 low) has completed. But a medium term corrective phase is in progress with risk of deeper fall back to 55 M EMA (now at 145.56).

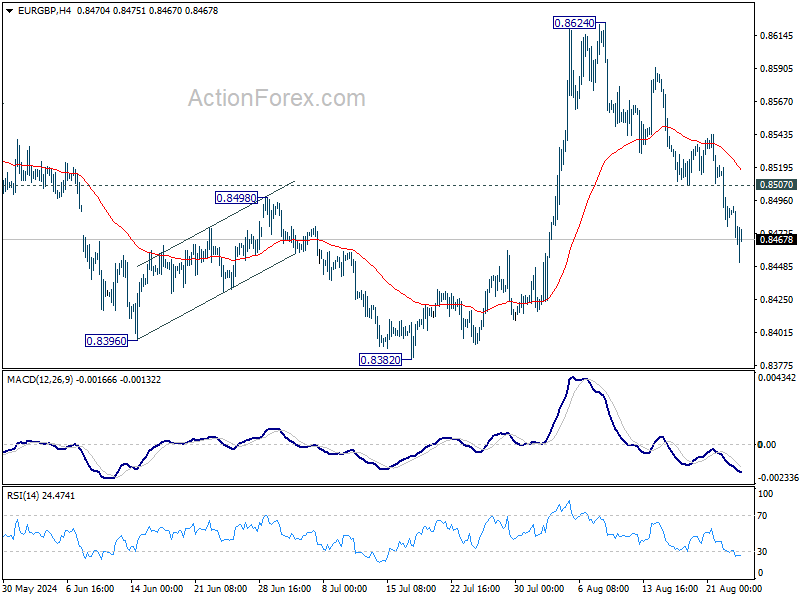

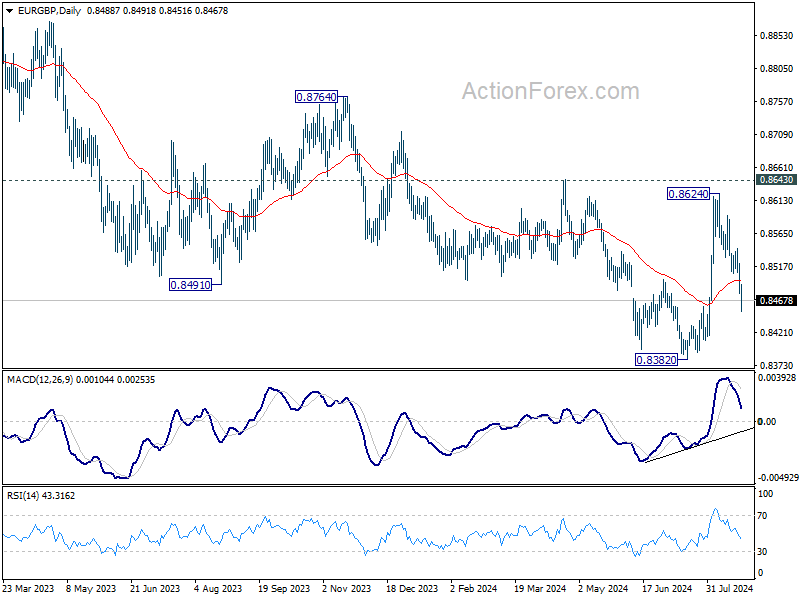

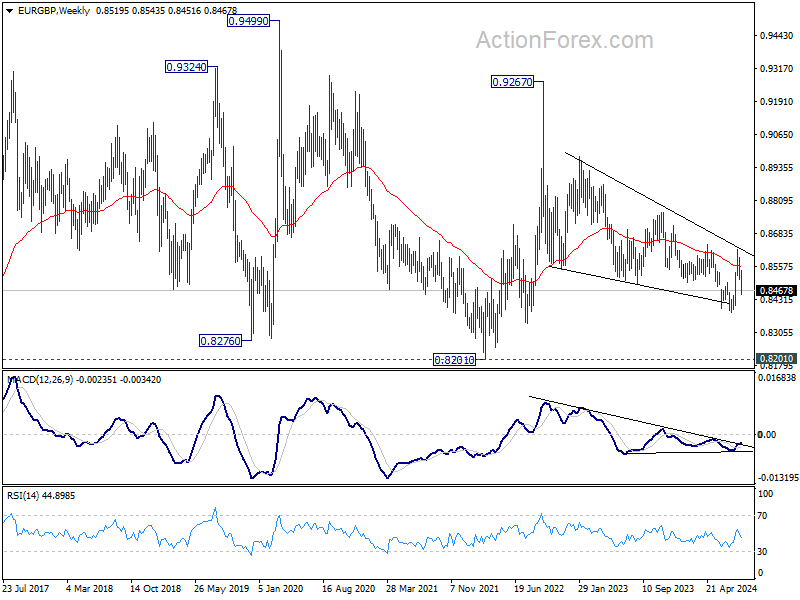

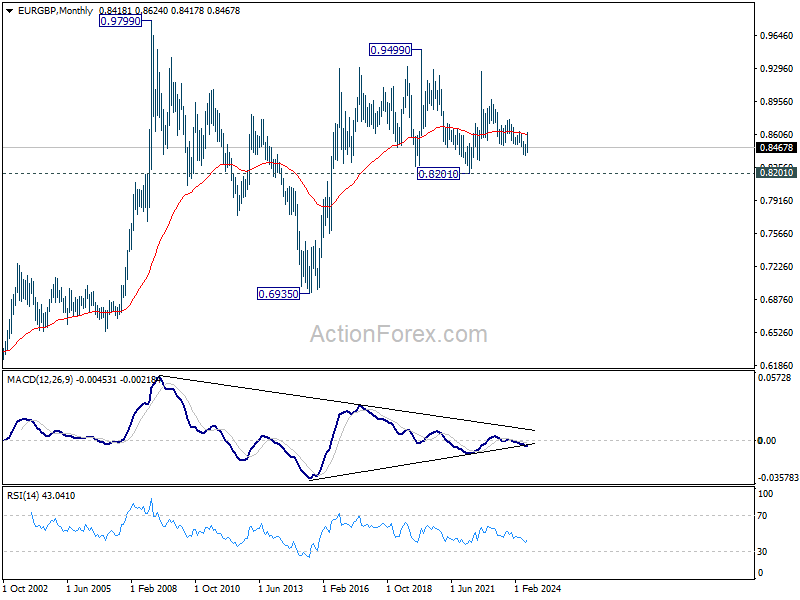

EUR/GBP Weekly Outlook

EUR/GBP's steep decline last week suggest that rebound from 0.8382 has completed 0.8624 already, after rejection by 0.8643 resistance. Initial bias stays on the downside this week for retesting 0.8382 low. Decisive break there will resume larger down trend. On the upside, above 0.8507 support turned resistance will turn intraday bias neutral first.

In the bigger picture, while the rebound from 0.8382 is strong, there is no confirmation of trend reversal yet. As long as 0.8643 resistance holds, down trend from 0.9267 could still resume through 0.8382 at a later stage towards 0.8201 (2022 low). However, firm break of 0.8643 will indicate that such down trend has completed, and turn outlook bullish for 0.8764 resistance next.

In the long term picture, price action from 0.9499 (2020 high) is seen as part of the long term range pattern from 0.9799 (2008 high). Range trading should continue between 0.8201 and 0.9499, until there is clear signal of imminent breakout.

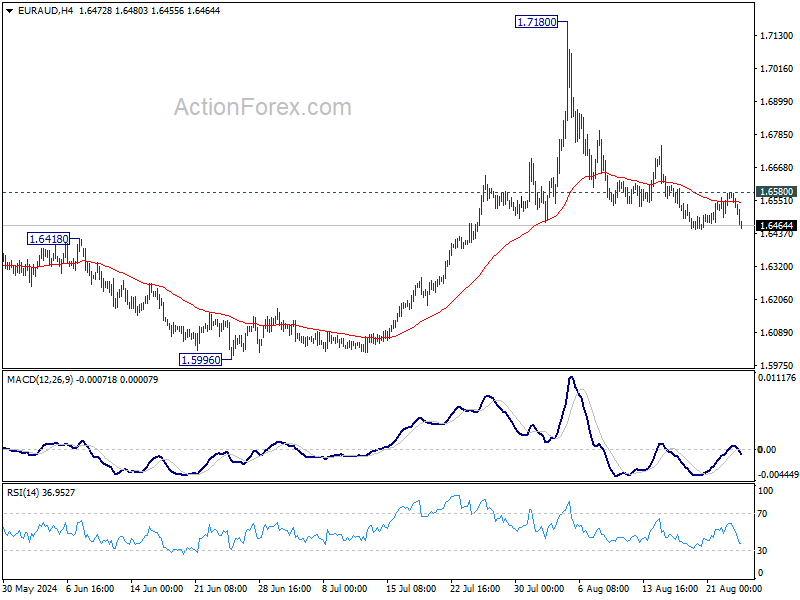

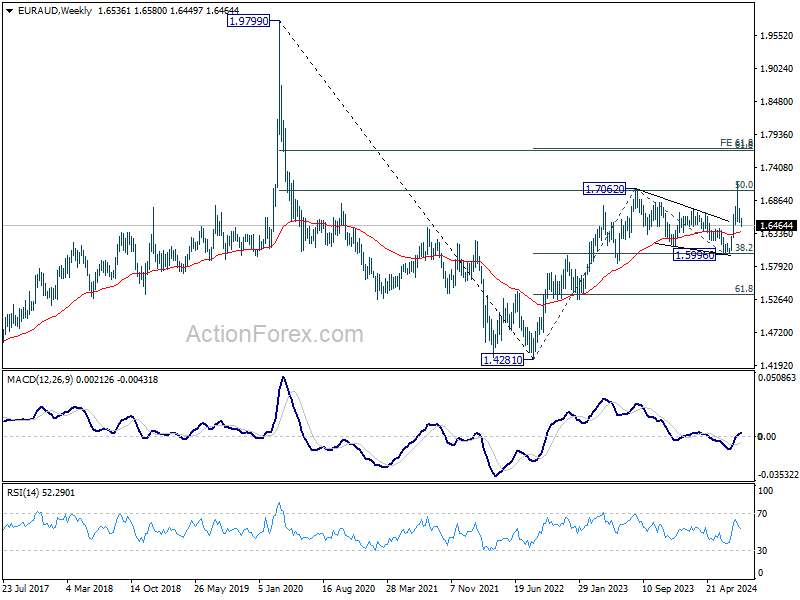

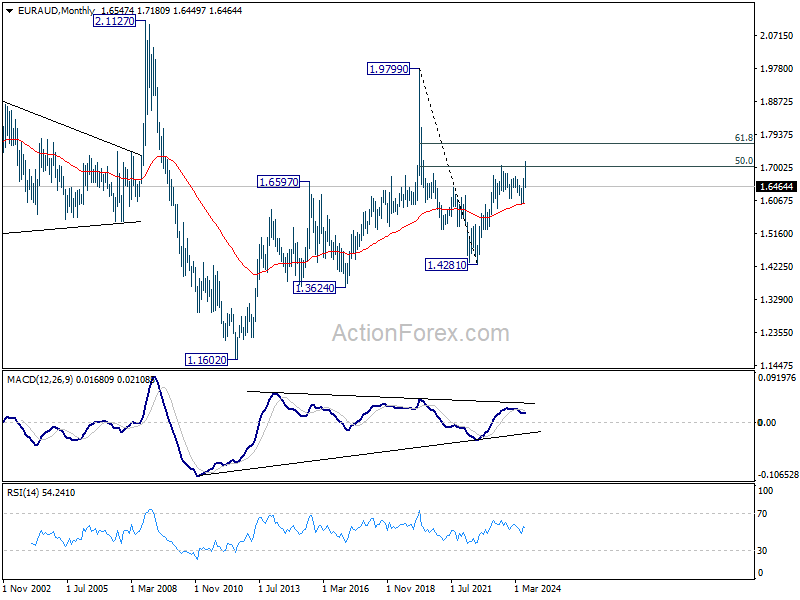

EUR/AUD Weekly Outlook

EUR/AUD gyrated lower last week despite weak downside momentum. On the downside, sustained trading below 55 D EMA (now at 1.6432) will argue that rise from 1.5996 has completed. Deeper fall would then be seen back to this support. Nevertheless, strong rebound from current levels, followed by break of 1.6580 resistance, will argue that pullback from 1.7180 has completed already. Intraday bias will then be back on the upside for stronger rebound.

In the bigger picture, corrective fall from 1.7062 medium term top should have completed at 1.5996. Larger up trend from 1.4281 (2022 low) is resuming. Next target is 61.8% projection of 1.4281 to 1.7062 from 1.5996 at 1.7715. However, sustained break of 55 D EMA will dampen this bullish view and extend medium term range trading.

In the longer term picture, price actions from 1.9799 (2020 high) are seen as a long term decline at the same scale as the rise from 1.1602 (2012 low). Rebound from 1.4281 is seen as the second leg. As long as 55 M EMA (now at 1.6006) holds, this second leg could still extend higher. However, sustained trading below 55 M EMA will open up the bearish case for extending the decline through 1.4281 low.

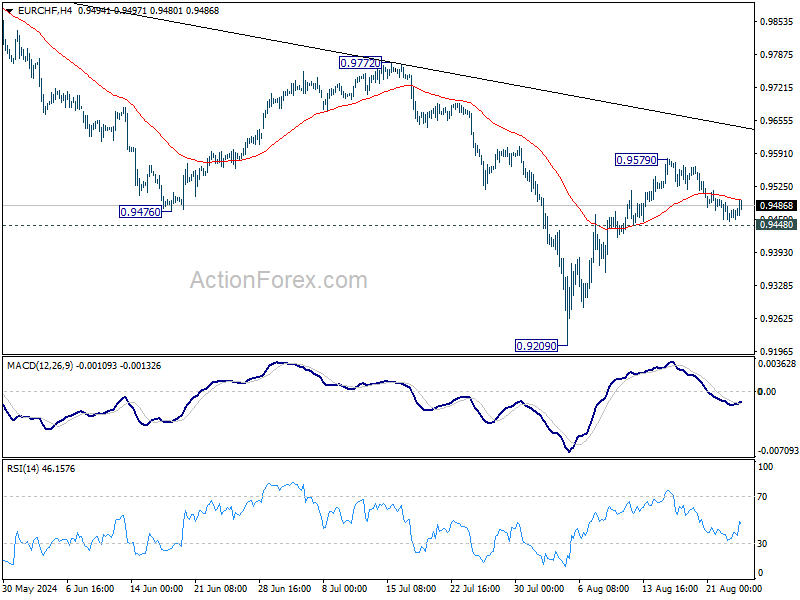

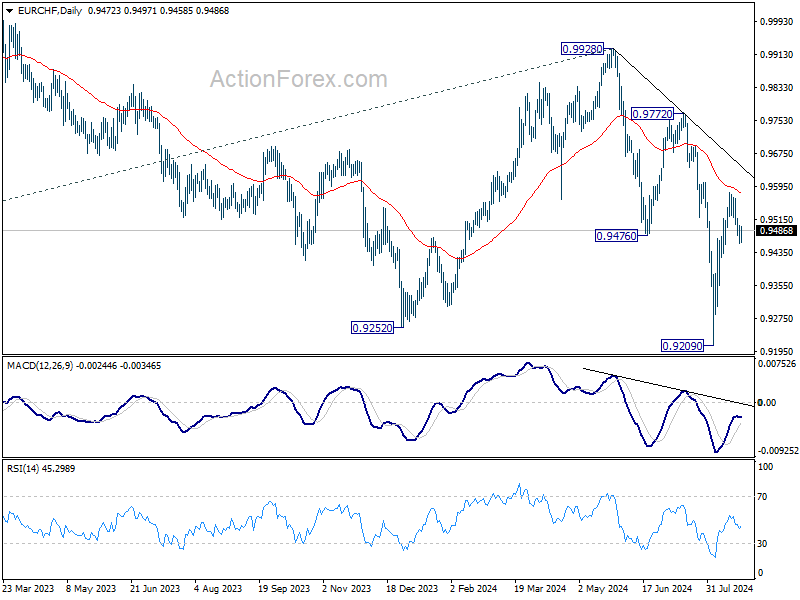

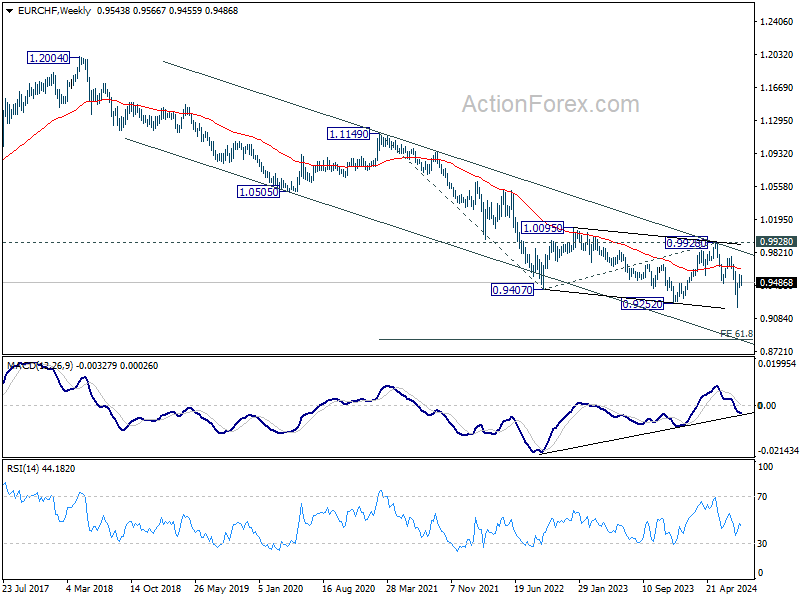

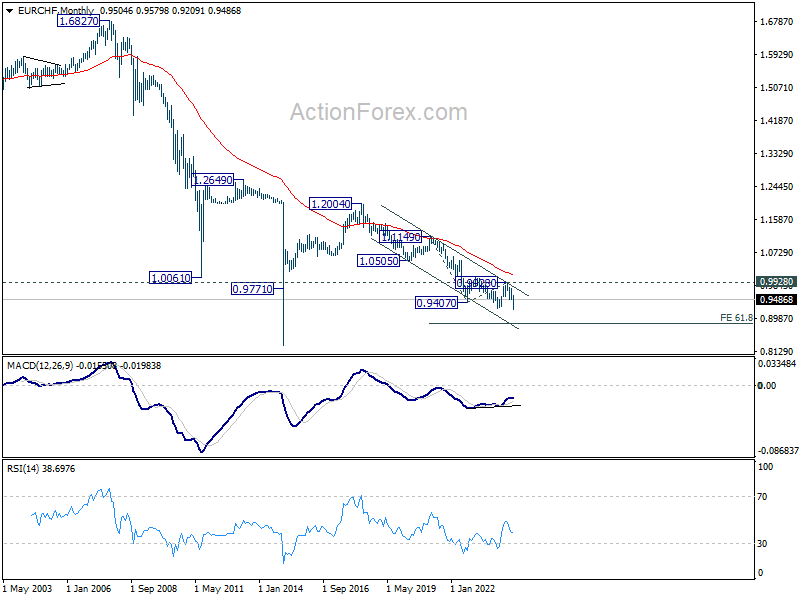

EUR/CHF Weekly Outlook

EUR/CHF's retreat from 0.9579 extended lower last week but recovered slightly ahead of 0.9448 support. Initial bias remains neutral this week first, and further rally is in favor. On the upside, sustained break of 55 D EMA (now at 0.9576) will pave the way back to 0.9972/0.9928 resistance zone. However, decisive break of 0.9448 will suggest rejection by 55 D EMA, and turn bias back to the downside for 0.9209 low.

In the bigger picture, medium term corrective pattern from 0.9407 (2022 low) might have completed with three waves to 0.9928. Decisive break of 0.9252 (2023 low) will confirm long term down trend resumption. Next target will be 61.8% projection of 1.1149 to 0.9407 from 0.9928 at 0.8851. For now, outlook will stay bearish as long as 0.9928 resistance holds, even in case of strong rebound.

In the long term picture, fall from 1.2004 (2018 high) is part of the multi-decade down trend. Firm break of 0.9928 resistance is needed to be the first sign of long term bottoming. Otherwise, outlook will remain bearish.

Summary 8/26 – 8/30

Monday, Aug 26, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 08:00 | EUR | Germany IFO Business Climate Aug | 86.5 | 87 |

| 08:00 | EUR | Germany IFO Current Assessment Aug | 86.5 | 87.1 |

| 08:00 | EUR | Germany IFO Expectations Aug | 86.5 | 86.9 |

| 12:30 | USD | Durable Goods Orders Jul | 4.00% | -6.70% |

| 12:30 | USD | Durable Goods Orders ex Transport Jul | 0.00% | 0.40% |

| 23:50 | JPY | Corporate Service Price Index Y/Y Jul | 2.90% | 3.00% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 08:00 | EUR | Germany IFO Business Climate Aug | |

| Forecast: 86.5 | Previous: 87 | ||

| 08:00 | EUR | Germany IFO Current Assessment Aug | |

| Forecast: 86.5 | Previous: 87.1 | ||

| 08:00 | EUR | Germany IFO Expectations Aug | |

| Forecast: 86.5 | Previous: 86.9 | ||

| 12:30 | USD | Durable Goods Orders Jul | |

| Forecast: 4.00% | Previous: -6.70% | ||

| 12:30 | USD | Durable Goods Orders ex Transport Jul | |

| Forecast: 0.00% | Previous: 0.40% | ||

| 23:50 | JPY | Corporate Service Price Index Y/Y Jul | |

| Forecast: 2.90% | Previous: 3.00% | ||

Tuesday, Aug 27, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 06:00 | EUR | Germany GDP Q/Q Q2 F | -0.10% | -0.10% |

| 13:00 | USD | S&P/CS Composite-20 HPI Y/Y Jun | 7.10% | 6.80% |

| 13:00 | USD | Housing Price Index M/M Jun | 0.20% | 0.00% |

| 14:00 | USD | Consumer Confidence Aug | 100.2 | 100.3 |

| GMT | Ccy | Events | |

|---|---|---|---|

| 06:00 | EUR | Germany GDP Q/Q Q2 F | |

| Forecast: -0.10% | Previous: -0.10% | ||

| 13:00 | USD | S&P/CS Composite-20 HPI Y/Y Jun | |

| Forecast: 7.10% | Previous: 6.80% | ||

| 13:00 | USD | Housing Price Index M/M Jun | |

| Forecast: 0.20% | Previous: 0.00% | ||

| 14:00 | USD | Consumer Confidence Aug | |

| Forecast: 100.2 | Previous: 100.3 | ||

Wednesday, Aug 28, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 01:30 | AUD | Construction Work Done Q2 | 0.70% | -2.90% |

| 01:30 | AUD | Monthly CPI Y/Y Jul | 3.40% | 3.80% |

| 06:00 | EUR | Germany GfK Consumer Confidence Sep | -18.4 | |

| 08:00 | CHF | UBS Economic Expectations Aug | 9.4 | |

| 08:00 | EUR | Eurozone M3 Money Supply Y/Y Jul | 2.80% | 2.20% |

| 14:30 | USD | Crude Oil Inventories | -4.6M |

| GMT | Ccy | Events | |

|---|---|---|---|

| 01:30 | AUD | Construction Work Done Q2 | |

| Forecast: 0.70% | Previous: -2.90% | ||

| 01:30 | AUD | Monthly CPI Y/Y Jul | |

| Forecast: 3.40% | Previous: 3.80% | ||

| 06:00 | EUR | Germany GfK Consumer Confidence Sep | |

| Forecast: | Previous: -18.4 | ||

| 08:00 | CHF | UBS Economic Expectations Aug | |

| Forecast: | Previous: 9.4 | ||

| 08:00 | EUR | Eurozone M3 Money Supply Y/Y Jul | |

| Forecast: 2.80% | Previous: 2.20% | ||

| 14:30 | USD | Crude Oil Inventories | |

| Forecast: | Previous: -4.6M | ||

Thursday, Aug 29, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 01:00 | NZD | ANZ Business Confidence Aug | 27.1 | |

| 01:30 | AUD | Private Capital Expenditure Q2 | 1.10% | 1.00% |

| 05:00 | JPY | Consumer Confidence Index Aug | 37.1 | 36.7 |

| 09:00 | EUR | Eurozone Economic Sentiment Indicator Aug | 95.9 | 95.8 |

| 09:00 | EUR | Eurozone Industrial Confidence Aug | -10.6 | -10.5 |

| 09:00 | EUR | Eurozone Services Sentiment Aug | 5.1 | 4.8 |

| 09:00 | EUR | Eurozone Consumer Confidence Aug F | -13.4 | -13.4 |

| 12:00 | EUR | Germany CPI M/M Aug P | 0.00% | 0.30% |

| 12:00 | EUR | Germany CPI Y/Y Aug P | 2.10% | 2.30% |

| 12:30 | CAD | Current Account (CAD) Q2 | -5.4B | |

| 12:30 | USD | Initial Jobless Claims (Aug 23) | 234K | 232K |

| 12:30 | USD | GDP Annualized Q2 P | 2.80% | 2.80% |

| 12:30 | USD | GDP Price Index Q2 P | 2.30% | 2.30% |

| 12:30 | USD | Goods Trade Balance (USD) Jul P | -97.1B | -96.6B |

| 12:30 | USD | Wholesale Inventories Jul P | 0.20% | 0.20% |

| 14:00 | USD | Pending Home Sales M/M Jul | 4.80% | |

| 14:30 | USD | Natural Gas Storage | 35B | |

| 22:45 | NZD | Building Permits M/M Jul | -13.80% | |

| 23:30 | JPY | Tokyo CPI Y/Y Aug | 2.20% | |

| 23:30 | JPY | Tokyo CPI core Y/Y Aug | 2.20% | 2.20% |

| 23:30 | JPY | Tokyo CPI core-core Y/Y Aug | 1.50% | |

| 23:30 | JPY | Unemployment Rate Jul | 2.50% | 2.50% |

| 23:50 | JPY | Industrial Production M/M Jul P | 3.30% | -4.20% |

| 23:50 | JPY | Retail Trade Y/Y Jul | 2.90% | 3.70% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 01:00 | NZD | ANZ Business Confidence Aug | |

| Forecast: | Previous: 27.1 | ||

| 01:30 | AUD | Private Capital Expenditure Q2 | |

| Forecast: 1.10% | Previous: 1.00% | ||

| 05:00 | JPY | Consumer Confidence Index Aug | |

| Forecast: 37.1 | Previous: 36.7 | ||

| 09:00 | EUR | Eurozone Economic Sentiment Indicator Aug | |

| Forecast: 95.9 | Previous: 95.8 | ||

| 09:00 | EUR | Eurozone Industrial Confidence Aug | |

| Forecast: -10.6 | Previous: -10.5 | ||

| 09:00 | EUR | Eurozone Services Sentiment Aug | |

| Forecast: 5.1 | Previous: 4.8 | ||

| 09:00 | EUR | Eurozone Consumer Confidence Aug F | |

| Forecast: -13.4 | Previous: -13.4 | ||

| 12:00 | EUR | Germany CPI M/M Aug P | |

| Forecast: 0.00% | Previous: 0.30% | ||

| 12:00 | EUR | Germany CPI Y/Y Aug P | |

| Forecast: 2.10% | Previous: 2.30% | ||

| 12:30 | CAD | Current Account (CAD) Q2 | |

| Forecast: | Previous: -5.4B | ||

| 12:30 | USD | Initial Jobless Claims (Aug 23) | |

| Forecast: 234K | Previous: 232K | ||

| 12:30 | USD | GDP Annualized Q2 P | |

| Forecast: 2.80% | Previous: 2.80% | ||

| 12:30 | USD | GDP Price Index Q2 P | |

| Forecast: 2.30% | Previous: 2.30% | ||

| 12:30 | USD | Goods Trade Balance (USD) Jul P | |

| Forecast: -97.1B | Previous: -96.6B | ||

| 12:30 | USD | Wholesale Inventories Jul P | |

| Forecast: 0.20% | Previous: 0.20% | ||

| 14:00 | USD | Pending Home Sales M/M Jul | |

| Forecast: | Previous: 4.80% | ||

| 14:30 | USD | Natural Gas Storage | |

| Forecast: | Previous: 35B | ||

| 22:45 | NZD | Building Permits M/M Jul | |

| Forecast: | Previous: -13.80% | ||

| 23:30 | JPY | Tokyo CPI Y/Y Aug | |

| Forecast: | Previous: 2.20% | ||

| 23:30 | JPY | Tokyo CPI core Y/Y Aug | |

| Forecast: 2.20% | Previous: 2.20% | ||

| 23:30 | JPY | Tokyo CPI core-core Y/Y Aug | |

| Forecast: | Previous: 1.50% | ||

| 23:30 | JPY | Unemployment Rate Jul | |

| Forecast: 2.50% | Previous: 2.50% | ||

| 23:50 | JPY | Industrial Production M/M Jul P | |

| Forecast: 3.30% | Previous: -4.20% | ||

| 23:50 | JPY | Retail Trade Y/Y Jul | |

| Forecast: 2.90% | Previous: 3.70% | ||

Friday, Aug 30, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 01:30 | AUD | Retail Sales M/M Jul | 0.20% | 0.50% |

| 01:30 | AUD | Private Sector Credit M/M Jul | 0.40% | 0.60% |

| 05:00 | JPY | Housing Starts Y/Y Jul | -1.10% | -6.70% |

| 06:00 | EUR | Germany Import Price Index M/M Jul | 0.00% | 0.40% |

| 06:00 | EUR | Germany Retail Sales M/M Jul | 0.00% | -1.20% |

| 06:45 | EUR | France Consumer Spending M/M Jul | 0.60% | -0.50% |

| 06:45 | EUR | France GDP Q/Q Q2 | 0.30% | 0.30% |

| 07:00 | CHF | KOF Leading Indicator Aug | 100.6 | 101.00 |

| 07:55 | EUR | Germany Unemployment Change Aug | 61K | 18K |

| 07:55 | EUR | Germany Unemployment Rate Aug | 6% | 6% |

| 08:30 | GBP | Mortgage Approvals Jul | 61K | 60K |

| 08:30 | GBP | M4 Money Supply M/M Jul | 0.50% | 0.50% |

| 09:00 | EUR | CPI Y/Y Aug P | 2.20% | 2.60% |

| 09:00 | EUR | CPI Core Y/Y Aug P | 2.80% | 2.90% |

| 09:00 | EUR | Eurozone Unemployment Rate Jul | 6.50% | 6.50% |

| 12:30 | CAD | GDP M/M Jun | 0.10% | 0.20% |

| 12:30 | USD | Personal Income M/M Jul | 0.20% | 0.20% |

| 12:30 | USD | Personal Spending Jul | 0.50% | 0.30% |

| 12:30 | USD | PCE Price Index M/M Jul | 0.20% | 0.10% |

| 12:30 | USD | PCE Price Index Y/Y Jul | 2.50% | |

| 12:30 | USD | Core PCE Price Index M/M Jul | 0.20% | 0.20% |

| 12:30 | USD | Core PCE Price Index Y/Y Jul | 2.60% | |

| 13:45 | USD | Chicago PMI Aug | 44.6 | 45.3 |

| 14:00 | USD | Michigan Consumer Sentiment Index Aug F | 67.8 | 67.8 |

| GMT | Ccy | Events | |

|---|---|---|---|

| 01:30 | AUD | Retail Sales M/M Jul | |

| Forecast: 0.20% | Previous: 0.50% | ||

| 01:30 | AUD | Private Sector Credit M/M Jul | |

| Forecast: 0.40% | Previous: 0.60% | ||

| 05:00 | JPY | Housing Starts Y/Y Jul | |

| Forecast: -1.10% | Previous: -6.70% | ||

| 06:00 | EUR | Germany Import Price Index M/M Jul | |

| Forecast: 0.00% | Previous: 0.40% | ||

| 06:00 | EUR | Germany Retail Sales M/M Jul | |

| Forecast: 0.00% | Previous: -1.20% | ||

| 06:45 | EUR | France Consumer Spending M/M Jul | |

| Forecast: 0.60% | Previous: -0.50% | ||

| 06:45 | EUR | France GDP Q/Q Q2 | |

| Forecast: 0.30% | Previous: 0.30% | ||

| 07:00 | CHF | KOF Leading Indicator Aug | |

| Forecast: 100.6 | Previous: 101.00 | ||

| 07:55 | EUR | Germany Unemployment Change Aug | |

| Forecast: 61K | Previous: 18K | ||

| 07:55 | EUR | Germany Unemployment Rate Aug | |

| Forecast: 6% | Previous: 6% | ||

| 08:30 | GBP | Mortgage Approvals Jul | |

| Forecast: 61K | Previous: 60K | ||

| 08:30 | GBP | M4 Money Supply M/M Jul | |

| Forecast: 0.50% | Previous: 0.50% | ||

| 09:00 | EUR | CPI Y/Y Aug P | |

| Forecast: 2.20% | Previous: 2.60% | ||

| 09:00 | EUR | CPI Core Y/Y Aug P | |

| Forecast: 2.80% | Previous: 2.90% | ||

| 09:00 | EUR | Eurozone Unemployment Rate Jul | |

| Forecast: 6.50% | Previous: 6.50% | ||

| 12:30 | CAD | GDP M/M Jun | |

| Forecast: 0.10% | Previous: 0.20% | ||

| 12:30 | USD | Personal Income M/M Jul | |

| Forecast: 0.20% | Previous: 0.20% | ||

| 12:30 | USD | Personal Spending Jul | |

| Forecast: 0.50% | Previous: 0.30% | ||

| 12:30 | USD | PCE Price Index M/M Jul | |

| Forecast: 0.20% | Previous: 0.10% | ||

| 12:30 | USD | PCE Price Index Y/Y Jul | |

| Forecast: | Previous: 2.50% | ||

| 12:30 | USD | Core PCE Price Index M/M Jul | |

| Forecast: 0.20% | Previous: 0.20% | ||

| 12:30 | USD | Core PCE Price Index Y/Y Jul | |

| Forecast: | Previous: 2.60% | ||

| 13:45 | USD | Chicago PMI Aug | |

| Forecast: 44.6 | Previous: 45.3 | ||

| 14:00 | USD | Michigan Consumer Sentiment Index Aug F | |

| Forecast: 67.8 | Previous: 67.8 | ||

Markets Weekly Outlook – Powell Delivers with Nvidia Earnings, PCE Data Next

- Fed Chair Powell signals policy adjustments are needed, emphasizing concerns about labor market weakness.

- The impact of Powell’s remarks on the FX space saw GBP/USD and EUR/USD reach new highs.

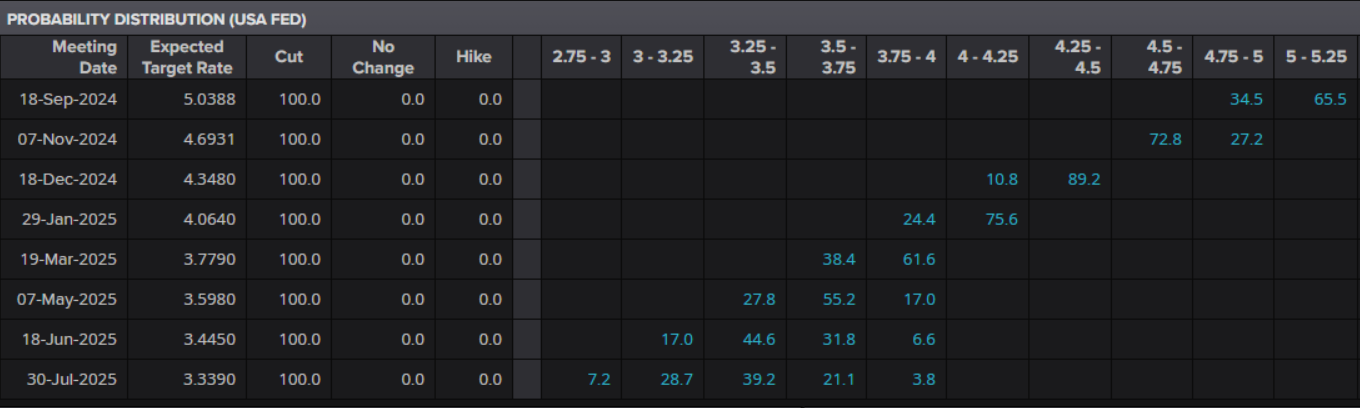

- Markets are pricing in a 34.5% chance of a 50 bps cut and 65.5% of a 25 bps cut at the Federal Reserve’s September meeting.

- US PCE and EU Inflation data are highlights.

Week in Review: Time for Policy to Adjust

As the week draws to a close, Fed Chair Jerome Powell certainly delivered with his remarks at the Jackson Hole Symposium.

Heading into the Powell speech my biggest fear was that markets had priced in a lot for September already and the response to Powell’s remarks may be muted. The Fed Chair however delivered, noting that it is ‘time for policy to adjust’ while reiterating his concern around further labor market weakness.

Markets are pricing in a 34.5% chance of a 50 bps cut and 65.5% of a 25 bps cut at the Federal Reserve’s September meeting. Between now and then the biggest focus will be placed on the jobs data out on September 6th. This comes after the largest downward revision on jobs data by the Bureau of Labor Statistics since the global financial crisis.

Any significant downside miss by the September jobs print and expectation for a 50 bps cut will ramp up. In Fed Chair Powell’s own words “Fed does not welcome further weakening of the labor market”.

Source: LSEG

After a brief pullback on Thursday, the DXY slid to fresh lows on Friday following Powell’s remarks. The impact of this on the FX space saw GBP/USD print fresh highs above 1.3200 and EUR/USD finally revisit the 1.1200 handle.

Oil is on course for back to back gains but is likely to finish the week in the red. Ongoing demand concerns and stalling airline fares continue to weigh on oil prices. The anticipation of rate cuts may add a bit of optimism but we will have to wait and see if that bleeds over into next week.

US Indices enjoyed a strong week overall with the three major indexes on course for a weekly gain despite some up and down moves on Friday. Much like Gold, US Indices did not manage to hold onto its gains following the Powell remarks. Is this a sign that much of the potential 25 bps rate cut for September has already been priced in?

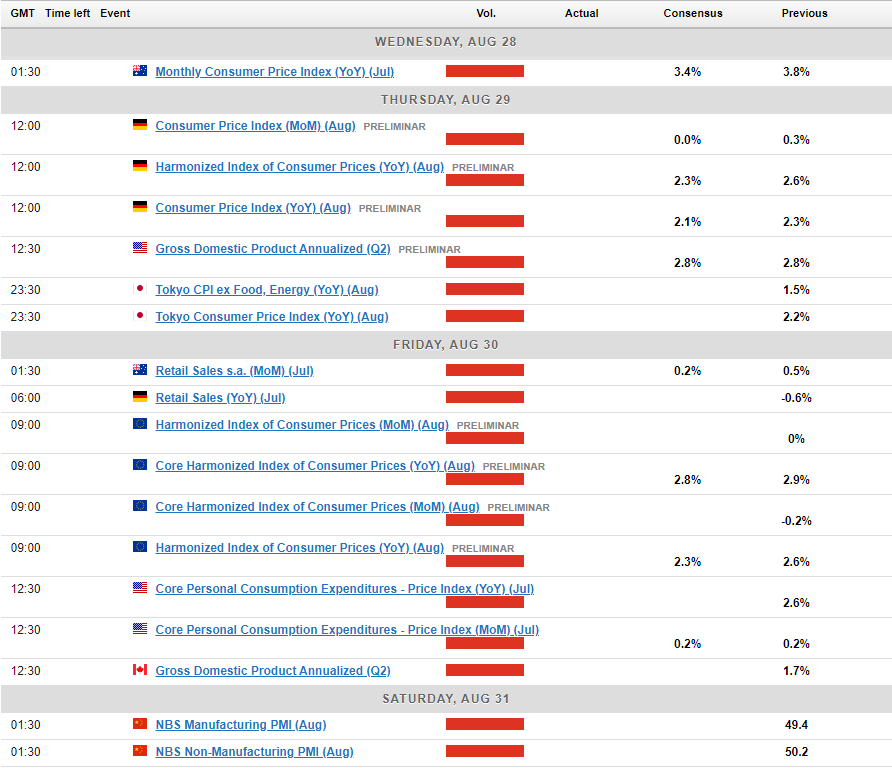

The Week Ahead: Lots of Data but Fed Rate Cut Set in Stone

Asia Pacific Markets

In Asia, the upcoming week is a busy one on the economic data front. Inflation, GDP and Production data take center stage with upbeat data prints expected.

Japan leads the way with a host of data releases as market participants continue to watch closely. In Tokyo, consumer inflation is anticipated to decline from 2.2% year-on-year in July to 1.9% in August, primarily due to the government’s temporary energy subsidy program. Despite this, the service sector is expected to see an acceleration in price increases, fueled by robust wage growth.

Industrial production is likely to bounce back with a 3.0% month-on-month rise, reversing the 4.2% drop in June, as auto manufacturing gradually recovers and semiconductor-related output improves, as indicated by recent export data. Meanwhile, labor market conditions are projected to remain tight due to persistent labor shortages, reflecting ongoing challenges in workforce availability. The data should support the hawkish stance taken by BoJ Governor Ueda in his Friday testimony before the Japanese parliament where he promised more rate hikes ahead.

China delivers no major data releases except for the Lending facility rate and industrial profits data.

Australia has a busy week ahead with the RBA hoping the data will make their jobs and decision making process easier. There is a host of data out of Australia but the biggest ones will likely be the inflation report and retail sales data. The recent RBA decision to keep rates on hold was met with some skepticism but there is hope that inflation remained steady over the period. The combination of seasonal influences, a slowdown in food price inflation, and decreasing gasoline prices is expected to result in a nearly flat month-on-month change.

Europe + UK + US

In Europe and the US, it’s another data-heavy week. The UK has a bank holiday on Monday to start the week but the US and other parts of Europe remain open.

Most of the high impact data releases from Europe and the US are due later in the week. The key highlights will be EU inflation data and of course from the US we have the Fed’s preferred inflation gauge, the PCE price index.

Usually the PCE would have a major impact on rate cut expectations however heading into next week’s release and jobs data is likely to hold a bigger sway. Unless we have a massive miss from the US and a significant rise in the PCE number any response to the data is likely to be muted.

The EU inflation figures are crucial, especially after sources from the ECB suggested rising backing for a 25 basis point cut at the next Central Bank meeting. If inflation decreases slightly or aligns with expectations, this could put some pressure on the Euro, as traders are likely to increase their bets on a rate cut.

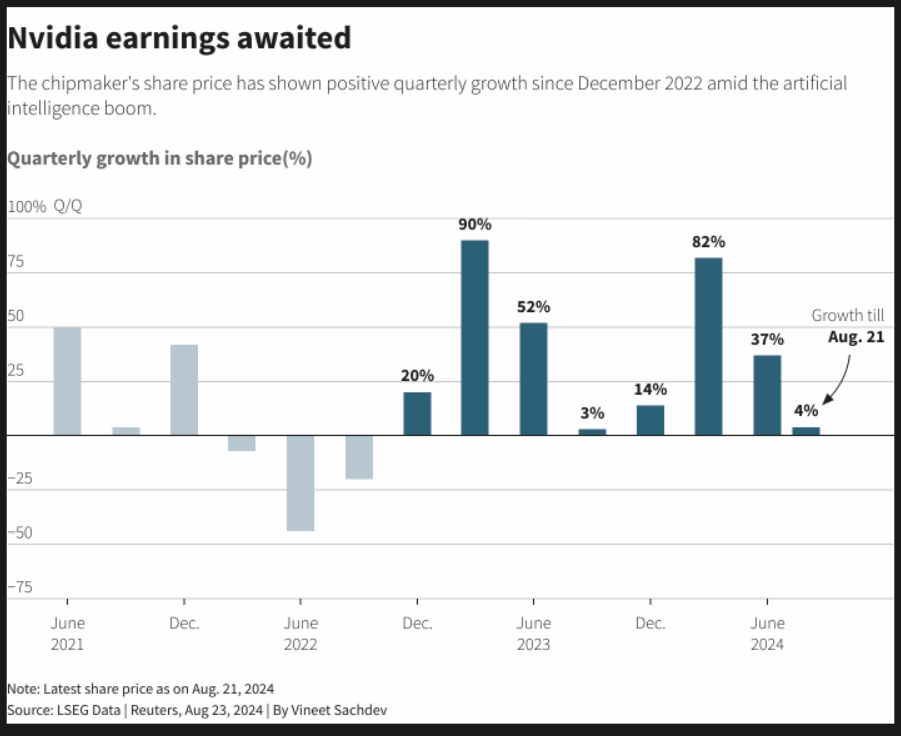

Lastly on the earnings front we have the much anticipated Nvidia earnings release next week. Nvidia shares remain up around 150% this year as markets will be looking to gauge the investor enthusiasm around AI. There has been growing chatter comparing the rise of Nvidia to the early 2000s dotcom bubble and the selloff following lackluster data by Alphabet and Tesla led to a steep selloff. Will AI mania get another vote of confidence and propel US indices to fresh highs?

Source: LSEG

Chart of the Week

This week’s highlighted chart is Brent Crude Oil following a mixed week. Brent is now trading at a delicate level heading into the new week with a host of headwinds to consider as well.

The late surge off a key support level on Thursday and Friday has made the outlook heading into next week intriguing. We had two massive bullish days which brings a retest of the descending trendline to the fore as the new week begins.

Demand concerns continue to plague oil prices and may hamper a deeper recovery next week. Immediate resistance rests at 80.00 psychological level with the descending trendline just resting above.

On the downside 77.25 support is key before the 75.00 mark is reached.

Brent Crude Oil Daily Chart – August 23, 2024

Source:TradingView.Com (click to enlarge)

Key Levels to Consider:

Support:

- 77.25

- 75.00

- 73.00

Resistance:

- 80.00

- 81.58

- 82.54 (200-day MA)

The Weekly Bottom Line: Fed Chair Powell Endorses September Rate Cut

U.S. Highlights

- Minutes from the July 30-31 FOMC meeting as well as Chair Powell’s speech at Jackson Hole showed a clear commitment that the FOMC will start cutting rates in September.

- The Fed is likely to start slow, cutting by 25 basis points next month. But any signs of a more abrupt cooling in the labor market will result in a more aggressive pace of rate cuts.

- Adding to evidence of a cooler labor market, annual benchmark revisions showed non-farm employment ended Q1 with less momentum than previously thought.

Canadian Highlights

- Headline inflation continued to decelerate in July, coming in at a palatable 2.5% year-on-year - the lowest reading since early 2021.

- The CNR/CPKC work stoppage made news this week, and the government has sent the parties to final arbitration, which hopefully sees operations return in the coming days.

- Retail sales came in weak for June, reminding us that consumers’ spending power remains limited in the face of high rent and high interest rates.

U.S. – Fed Chair Powell Endorses September Rate Cut

It was a quiet week on the economic data calendar, but there was plenty of Fed communication for market participants to digest. The headliner was Fed Chair Powell’s speech at the annual Jackson Hole Symposium, where the Chairman signaled a clear desire for the FOMC to begin reducing its policy rate at its next meeting in September. The news hardly came as a surprise, particularly coming after the release of the July 30-31 FOMC minutes, which indicated that the “vast majority of participants” supported cutting rates at the next meeting. Though equity markets see-sawed through most of the week, a clear commitment from Powell that the Fed will soon start loosening its policy stance helped to fuel a late-week rally, with the S&P 500 looking to end the week up 1.3%. Bond yields across the curve were lower by 10-15 basis-points (bps) on the week, with the 10-year Treasury sitting at 3.8% at the time of writing.

Two years ago, Chair Powell delivered a very somber message during his speech at Jackson Hole, stating the Federal Reserve will do “whatever it takes to restore price stability” even if that meant “inflicting some economic pain”. At the time, inflation was sitting at a multi-decade high while the labor market had tightened to a degree not seen in recent history. It had become obvious that policymakers had fallen well behind the curve and were scrambling to play catch-up. While many feared that the FOMC’s swift actions of quickly raising the policy rate (Chart 1) risked overtightening and potentially tipping the economy into a recession, the downturn never materialized.

During his speech Friday morning, Chair Powell acknowledged the progress the Fed has made over the past two years, specifically noting that the upside risks to inflation have diminished while the downside risks to employment have increased. While Powell offered nothing in terms of the speed of adjustment, other policymakers speaking this week highlighted the importance of a “gradual” and “methodical” approach to loosening policy, which supports a 25 basis point cut in September. However, Powell also emphasized that the FOMC “does not seek or welcome any further cooling in the labor market”, which suggests the next several employment reports will be critical in determining the future path of the policy rate.

Fears of a further cooling in the labor market aren’t completely unfounded. Earlier this week, the BLS released its preliminary annual benchmark revisions for non-farm employment, which showed that payrolls were 818 thousand less over the twelve-month period ending in March 2024 - the largest downward adjustment since 2009. This implies that job gains likely averaged closer to 174 thousand per-month over the reference period, as opposed to the 242 thousand currently reported (Chart 2).

Even after incorporating the revisions, there’s nothing yet to suggest that the labor market has overcorrected. This is why we feel that the FOMC is likely to opt for a more gradual approach in the beginning. However, it is clear that policymakers have become hypervigilant of the labor market and any further signs of cooling is likely to bring a more aggressive path for rate cuts.

Canada – The Door is Wide Open for More Rate Cuts

Fed Chair Powell’s Jackson Hole speech might have been the headliner for financial markets this week, but Canadian economic data were an exciting opening act. Canadian Consumer Price Index (CPI) inflation confirmed that the Bank of Canada (BoC) can keep up its rate cutting pace. At the same time, retail sales showed that consumer spending remains constrained in the face of still high interest rates. The CNR/CPKC labour dispute is heading for binding arbitration, which will hopefully limit the downside risk to near-term economic growth. All this combined to anchor expectations that the BoC will cut its overnight rate by 25 basis points at its announcement in two weeks.

Headline inflation continued to decelerate in July, coming in at a palatable 2.5% year-on-year (y/y). That is the lowest reading since early 2021 and marks the seventh month in a row that inflation has fallen within the BoC’s 1% to 3% range (Chart 1). Even more convincing is that inflation excluding the impact of mortgage interest costs has been below the 2% target rate for nearly all of 2024. Outside of structural factors facing Canada’s housing sector, inflation is back to normal.

Looking forward, inflation’s underlying details point to continued improvement over the remainder of the summer. The base-effects - the impact of last summer’s price increases dropping out of the annual inflation figures – that pushed July’s inflation rate lower, will support a continuation of the recent disinflationary trend. Furthermore, core inflation rates have continued to ease (2.6% y/y for the average of the BoC’s core rates), which points to improved underlying inflationary dynamics. The only caveat is that there has been a noticeable upturn in the three-month annualized pace of inflation, having gone from 1.4% in March to 2.7% in July. This increase has raised our eyebrows, but rather than signaling a re-emergence of future inflation, it points to inflation settling around the mid-2% level in 2025.

Also making headlines was the announcement of the CNR/CPKC work stoppage. On Thursday, nine thousand workers were locked out, halting rail traffic for goods, ranging from fertilizer to hazardous chemicals. Approximately $1 billion a day is transported over rail lines, while thousands of transit users saw their main commuting method unavailable. As of Friday, the government has sent the dispute to final arbitration, which should result in (but doesn’t guarantee) operations going back to normal in the coming days.

Retail sales, on the other hand, reminded us that consumers are under pressure. There was a noticeable drop-off in spending in June, which has been a trend for consumers facing tough spending choices in the face of rising rents and higher mortgage payments. All this combines to make a convincing case for the BoC to keep cutting its policy rate. With the door to rate cuts wide open, we expect the central bank will proceed with cuts at each of its next three remaining decisions over 2024 (Chart 2).

Weekly Economic & Financial Commentary: The Time Has Come for Policy to Adjust

Summary

United States: Homes Out of Range

- Chair Powell delivered a distinctively dovish speech this week at Jackson Hole. Elsewhere, a slew of housing data revealed that, although green shoots are sprouting, affordability issues continue to constrain the housing market. Meanwhile, another decline in the Leading Economic Index was a reminder that recession risks lie ahead.

- Next week: Durable Goods (Mon.), Personal Income & Spending (Fri.)

International: Adjusting Our Foreign Central Bank & U.S. Dollar Outlook

- We published our August International Economic Outlook report this week and made some notable adjustments to our forecasts. More specifically, with the Fed likely on track to cut interest rates in September, we believe select foreign central banks can also either cut more aggressively or initiate easing cycles. In addition, as we see the Fed front-loading its easing, we have also adjusted our U.S. dollar outlook to see a stable-to-stronger greenback over the second half of 2025.

- Next week: Canada GDP (Fri.), Eurozone CPI (Fri.), India GDP (Fri.)

Interest Rate Watch: Powell: "The Time Has Come for Policy to Adjust"

- In a widely anticipated speech in Jackson Hole, Wyo., today, the Fed Chair signaled that the FOMC will be cutting rates at its next meeting on Sept. 18. The question is 25 bps or 50 bps?

Credit Market Insights: What Is Driving the Growth in Bankruptcy Filings?

- The rate of businesses filing for bankruptcy has picked up significantly in 2024 and is currently at its highest level since the global financial crisis. What is driving this growth in business bankruptcy, and is it something we should be alarmed about?

Topic of the Week: What a Downward Revision of 818K Jobs Means for the Labor Market

- The preliminary estimate for the 2024 benchmark revision to nonfarm payrolls (NFP) announced this week indicates the level of employment in March 2024 will be revised downward by 818K come the official annual benchmark in early 2025. The announcement was in line with expectations (including ours) for a large negative revision; so, what have we learned from the preliminary benchmark and the data that informed it?