Sample Category Title

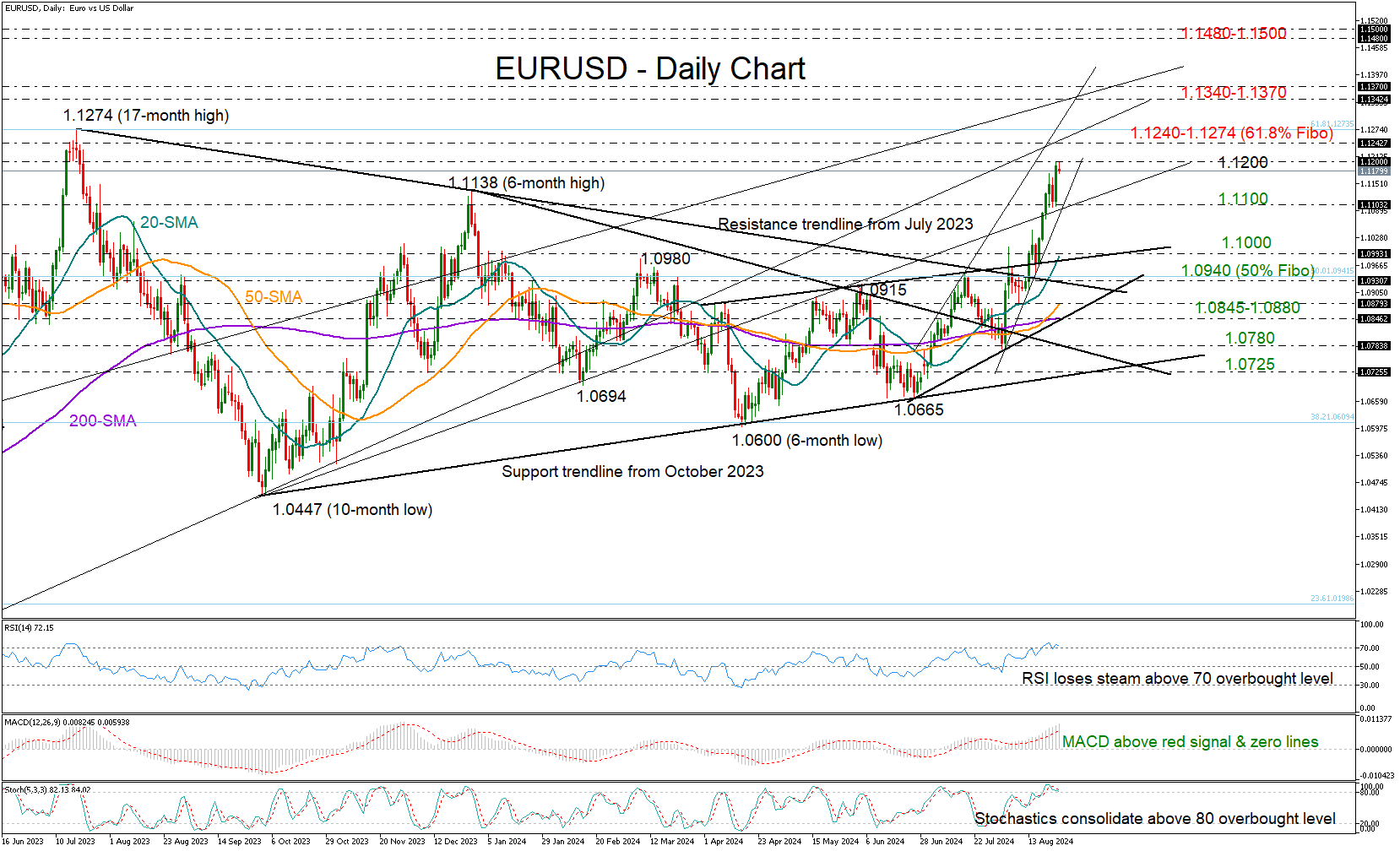

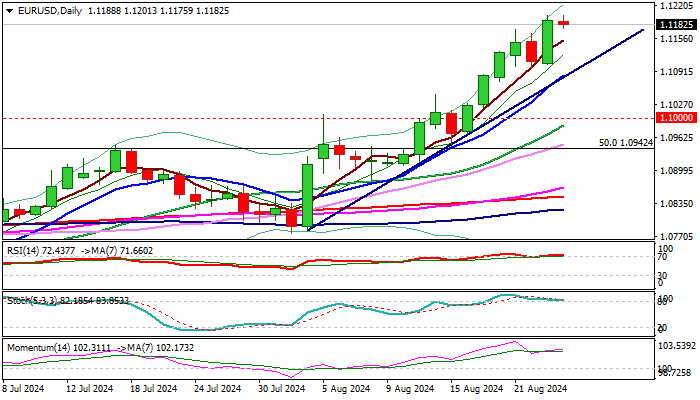

EURUSD Eyes 2023 Top After Quick Rally

- EURUSD returns to positive trend after Powell confirms dovish policy adjustment

- Technical signals reflect weakening positive bias; next resistance could be at 1.1240-1.1274

EURUSD has had a great August so far, rising sharply from 1.0776 to nearly 1.1200 to mark its best monthly performance since November 2022.

The pair violated a bearish engulfing candlestick pattern after refusing to close below 1.1100 on Friday, increasing optimism that the rally might have more room to run. Nevertheless, it is crucial to be cautious as the RSI and stochastic oscillator display weakness in the overbought zone, indicating that selling interest persists.

The 1.1240-1.1274 area, which includes the 61.8% Fibonacci retracement of the 2021-2022 downtrend and the trendline from the 2022 trough, could keep the bulls busy in the short term. A move higher could hit a wall somewhere between 1.1340 and 1.1370, with the latter being a tough obstacle during November 2021-February 2022. If the battle there is won, it could trigger substantial buying up to the 2022 double top region of 1.1480.

Looking to the downside, a close below 1.1100 might lead the price towards the 20-day simple moving average (SMA) seen near 1.1000. A move lower could shift all the attention to the 50% Fibonacci of 1.0940 and the broken resistance trendline from July 2023. Then, the 50- and 200-day SMAs at 1.0880 and 1.0845 respectively could block an extension to 1.0780. If this does not occur, selling pressure could stretch towards the 1.0725 region.

All in all, EURUSD exited its 2024 sideways trajectory and might aim for new higher highs, though for a meaningful rally, it might need to cross above the 2023 barrier of 1.1240-1.1274.

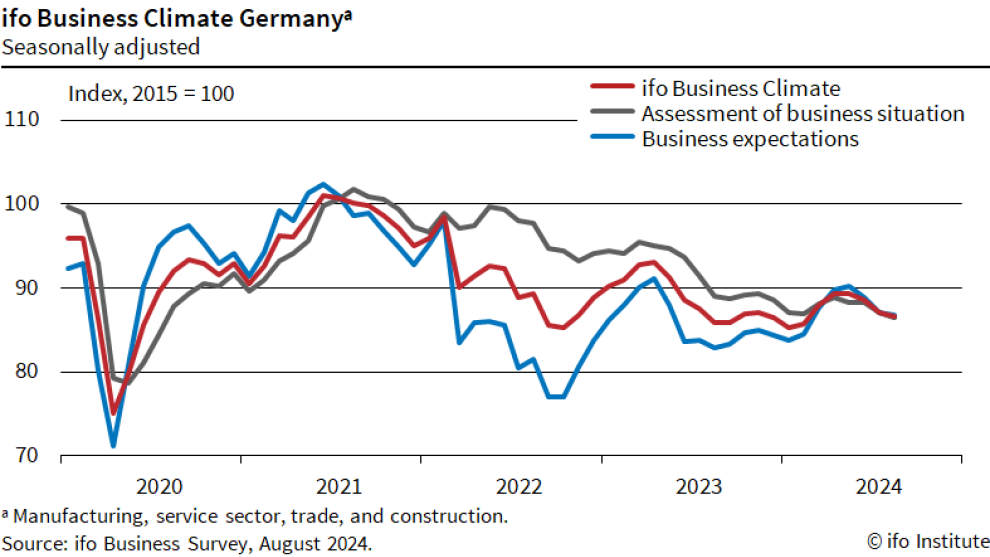

German Ifo business climate falls to 86.6, Ifo warns of worsening economic crisis

In August, Germany’s Ifo Business Climate Index dropped from 87.0 to 86.6, slightly surpassing expectations of 86.5 but still signaling growing economic concerns. Current Assessment Index also dipped from 87.1 to 86.5, aligning with forecasts, while Expectations Index marginally beat predictions at 86.8, although still reflecting a decline from 87.0

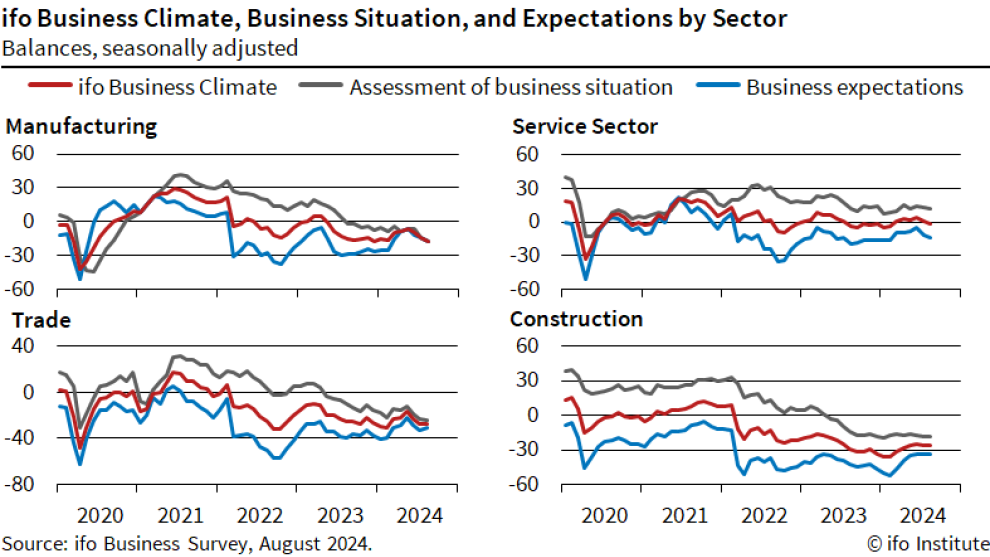

Sector-wise, manufacturing sector saw a significant decline from -14.2 to -17.8. Services sector turned negative, falling from 0.8 to -1.3. Trade sector showed a minor improvement from -27.9 to -27.4, while construction remained stagnant at -26.4.

Ifo President Clemens Fuest issued a stark warning, stating, "The German economy is increasingly falling into crisis."

EUR/USD Outlook: Looks for Test of 2023 High After Limited Correction

EURUSD cracked 1.1200 barrier after Friday’s 0.75% rally (the biggest daily gain since Aug 2) and hit new 2024 high early Monday.

Bulls remain firmly in play after strong advance in past two weeks and on track for the biggest monthly gain since November 2022, as weakening dollar on strong Fed rate cut signals, continues to underpin the single currency

Next target at 1.1275 (2023 high / Fibo 61.8% of larger 1.2349/0.9535 downtrend) is coming in focus, with firm break here to generate strong signal of bullish continuation of an uptrend from 0.9535 (Sep 2022 low) which was paused for a multi-month consolidation.

Meanwhile, bulls are likely to take a breather as the action was repeatedly capped by falling and thickening monthly cloud, with overbought daily studies adding to signals of limited correction which should offer better buying opportunities.

Higher base at 1.1100 zone (Aug 21/22/23 low) reinforced by bull trendline and rising 10DMA marks solid support, where dips should find firm ground.

Res: 1.1201; 1.1221; 1.1239; 1.1275.

Sup: 1.1152; 1.1100; 1.1084; 1.1039.

For Now, We Don’t Fight the Broader USD Downtrend

Markets

At its keynote Jackson Hole speech on Friday, Fed Chair Powell explicitly reconfirmed the change in the Fed’s assessment on the balance between fighting inflation and preserving maximum employment it already signaled at the July policy meeting. ‘The upside risks to inflation have diminished. And the downside risks to employment have increased.’ The Fed’s confidence that inflation is on a sustainable path to 2.0% is growing. The labor market has cooled considerably from its formerly overheated state. Even as the rise in unemployment mainly comes from a rise in labour supply rather from layoffs, the Fed doesn’t seek or welcome a further cooling of the labour market. With respect to the potential pace of easing Powell stated that while keeping a data-dependent approach. ‘The current level of our policy rate gives us ample room to respond to any risks we may face, including the risk of unwelcome further weakening in labor market conditions.’ With this kind of remarks, Powell left all options open but didn’t formally challenge the market view that the Fed might move to 50 bps steps in a not that distant future. US yields on Friday closed between 8.8 bps (2-y) and 3.5 bps (30-y) lower. Markets now see more than 100 bps of cumulative rate cuts before the end of this year, with the low of the cycle seen near 3.0% (end 2025/early 2026). Despite Friday’s decline, US bond yields didn’t break recent (intraday) lows and are holding above the lows from the early August risk-off move. Still, the picture for the 2-y yield remains fragile. German yields declined between 2.5 bps (5-y) and 0.5 bps (30-y). The direction of travel for the dollar remains clear: south. DXY closed at a 100.72 (from 101.46). EUR/USD tested the 1.12 big figure (close 1.1192). Equity investors embraced the prospect of further, Fed-led easing of (global) financial conditions. US indices gained op to 1.47% (Nasdaq). The S&P 500 (+1.15%) closed less than 1.0% below its all-time peak. The Eurostoxx 50 added 0.5%.

Today’s calendar is modestly interesting with US durable goods orders and German Ifo confidence. US activity data are gaining importance as the Fed is putting less weight on inflation, but the durables’ series is very volatile. Even so, we look out whether the decline in US yields might slow as quite some easing is already discounted. German Ifo confidence is expected to confirm weakness in other recent data evidence. For German/EMU bond markets, inflation to be published on Thursday (Germany) and Friday (EMU), probably are more important. For now, we don’t fight the broader USD downtrend as long markets maintain the view that the Fed can move to 50 bps steps in a not that distant future. Key USD support kicks in at DXY 99.58 and EUR/USD 1.1276 (2023 top).

News & Views

Bank of England governor Bailey said that policy settings will need to remain restrictive for sufficiently long until the risks to inflation remaining sustainably around the 2% target in the medium term have dissipated further. “The course will therefore be a steady one.” The UK central bank chief is nevertheless becoming more confident that things are heading in the right direction. Second round inflation effects appear to be smaller than the BoE expected. They are revising down their assessment on how persistent these pressures would be, though don’t take it for granted yet. Bailey gave no guidance for the outcome of the next, September, policy meeting. UK money markets attach a 25% chance to back-to-back rate cuts with the more likely scenario being that the BoE only implements a next 25 bps rate cut in November, when the new quarterly Monetary Policy Report will be released. Sterling continues outperforming both EUR and USD with cable (GBP/USD), breaching 1.32 for the first time since Q1 2022.

Brazil central bank governor Campos Neto warned at the Kansas City Fed’s Jackson Hole conference that the country’s tight labour market is challenging the central bank’s bid to rein in inflation. Consumer prices have been picking up across Latin America with Brazilian inflation hitting the 4.5% Y/Y ceiling of the tolerance range (3% +- 1.5 ppt) in July. With economic activity picking up, Campos Neto warned that the central bank’s data dependency could result in an higher policy rate if needed. The Brazilian central bank raised its policy rate from 2% in 2021 to a 13.75% peak by mid-2022. They started a gradual easing cycle in mid-2023, but paused it in June at a 10.50% policy rate. arlier this month, influential board member Galipolo who is rumoured to succeed Campos Neto when his term ends in December, indicated that a rate hike is on the table at the next (September) policy meeting.

Graphs

GE 10y yield

The ECB cut policy rates by 25 bps in June. Stubborn inflation (core, services) make follow-up moves less evident. Markets nevertheless price in two to three more cuts for 2024 as disappointing US and unconvincing EMU activity data rolled in, dragging the long end of the curve down. The move accelerated during the early August market meltdown.

US 10y yield

The Fed in its July meeting paved the way for a first cut in September. It turned attentive to risks to the both sides of its dual mandate as the economy is moving to a better in to balance. Markets tend to err in favour of a 50 bps lift-off. The pivot weakened the technical picture in US yields with another batch of weak eco data pushing the 10-yr sub 4%. Powell at Jackson Hole didn’t challenge markets’ positioning.

EUR/USD

EUR/USD moved above the 1.09 resistance area as the dollar lost interest rate support at stealth pace. US recession risks and bets on fast and large (50 bps) rate cuts trumped traditional safe haven flows into USD. EUR/USD 1 1.1276 (2023 top) serves as next technical reference.

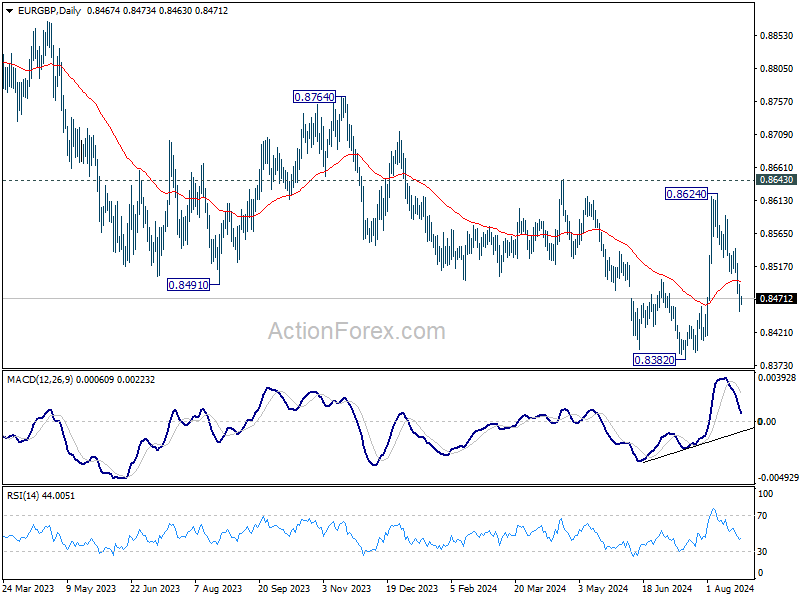

EUR/GBP

The BoE delivered a hawkish cut in August. Policy restrictiveness will be further unwound gradually on a pace determined by a broad range of data. The strategy similar to the ECB’s balances out EUR/GBP in a monetary perspective. Risk-off proved a more important driver of GBP recently, triggering a brief return from 0.84 towards 0.86.

Powell Gives the All-Clear

‘The time has come for policy to adjust, and the direction of the travel is clear’ said Federal Reserve (Fed) Chair Jerome Powell at his Jackson Hole speech on Friday. He didn’t give any guidance regarding the size of the coming rate cut despite speculation of at least one jumbo rate cut before the end of the year. Instead, he kept the door open for large cut bets. ‘The pace of rate cuts will depend on the incoming data, the evolving outlook and the balance of risks’ he said. And Chicago Fed’s Governor Goolsbee said that it’s time to pay more attention to the employment side, making it clear for everyone that – as the inflation side seems to be under control – the developments in the employment leg will determine the size of the cuts. And the employment data of late has been weak – no alarmingly weak just yet but weak enough - to keep the doves in charge of the market after Powell’s dovish speech last Friday. The US yields and the US dollar index further dived. The yields and the dollar are now waiting impatiently next week’s jobs data update – as the jobs data gains importance after a long focus on inflation. But before that, we will be watching the US GDP update this Thursday and the core PCE index – the Fed’s favourite gauge of inflation on Friday. The US GDP is expected to have rebounded to 2.8% in Q3, from 1.4% printed a quarter earlier. But Atlanta Fed’s GDP Now index suggests that the Q3 growth may be slower than that – around 2%. Sufficient weak growth and inflation figures should keep the Fed doves in the playground before next week’s jobs data.

The expectation of a 50bp cut has been rising slowly but surely. And the risk assets are surfing on that vibe in the absence of a major stress. The S&P500 and Nasdaq extended gains by more than 1% and the Russell 2000 index jumped more than 3% on Friday. I remain convinced that a 25bp cut is the right dose of dovishness to help keep appetite intact in the stock markets.

In the FX, the US dollar’s further dive pushed the EURUSD to 1.12 on Friday, but the pair sees resistance at this level in Asia this morning, and I still believe that the euro’s recent surge is overdone against the US dollar and a correction would be healthy at the current levels. This week, the Eurozone countries will be releasing their preliminary CPI numbers for August and the expectations are weak. EZ headline inflation may have eased from 2.6% to 2.2%, while core inflation is still seen a bit sticky slightly below the 3% mark. But inflation in Europe seems to be in check as well – a situation that should allow the European Central Bank (ECB) to continue cutting the rates. European economies need the rate cuts more than the US does, but the ECB is expected to cut by 50bp before the year ends vs 100bp cut expected for the Fed. Hence there is a growing room for a dovish adjustment for the ECB expectations.

Finally, crude oil gained on Friday along with risk assets, and bulls are joining in this morning on news that Israel has declared a 48-hour state of emergency after launching a pre-emptive strike on Hezbollah sites in Southern Lebanon, in anticipation of a response to last month’s assassination of its military chief.

Nvidia reports on Wednesday

Nvidia earnings are due after the Wednesday’s closing bell, and the expectations remain sky-high. The company has pointed at $28bn sales in Q2 when it released earnings last quarter - double the amount it made a year earlier, and the market consensus is around $28.7bn. Although the worries regarding the Big Tech’s big AI spending have been mounting as the AI investments haven’t yet improved the company profits just yet (except at Meta), the big AI spenders like Meta and Google who account for 40% of Nvidia’s revenue said that they’d rather overspend in AI than underspend to make sure not to miss the decisive AI turn. Hence, Nvidia could announce another blowout quarter. But Nvidia cannot afford any missteps at current valuations. Everything from the numbers to guidance should be perfect the keep the rally going. And this is where, the rising competition and impatient investors – who could force the big spenders to spend less on AI – become growing challenges.

Fed Chair Powell Ready to Loosen Monetary Policy

In focus today

We will have a quiet start to the week on the data front. The most important release today is the German Ifo index. Consensus expectations is for a small decline, which in that case would be the fifth consecutive month that would have happened. This would be in line with the PMI index, which declined in August, as we saw last week.

The Riksbank minutes from the August meeting will be released at 9.30 CET. The meeting itself proved rather uneventful for markets, with a fully expected rate cut from 3.50% to 3.25% and signals of more to come. We will look to see whether any participants discussed the possibility of larger 50bp cuts and what the prerequisites would be for such a move.

Overnight on Tuesday, China will release industrial profits for July. They increased 3.6% y/y in June, but PMI data suggests the economy lost momentum in July and we could see profit growth slip into negative again.

The highlight of the week will be the batch of inflation data due on Friday, when we will get flash inflation from the euro area, PCE inflation from the US and Tokyo inflation from Japan.

Economic and market news

What happened overnight

In China, the People's Bank of China (PBoC) kept its one-year medium-term lending facility rate unchanged at 2.30% as widely expected, as it was lowered last month. We expect the PBoC to lower the rate further over the next couple of months as the economy needs more stimulus and the recent yuan appreciation provides more policy space to lower rates.

What happened over the weekend

In Middle East, tensions rose once again after a missile exchange between Israel and Hezbollah on Sunday. Hezbollah said its bombardment was a retaliation for Israel's killing of one of its most senior commanders last month in Beirut. The timing of Hezbollah's attack was surprising considering that Gaza ceasefire negotiations are ongoing. Iran, whose leaders have vowed a revenge for the assassination of Hamas leader, Ismail Haniyeh on its territory in early August, has earlier said they would delay their response and allow time for peace talks. The next question is if the recent developments jeopardize the talks and change the calculus of Iran.

What happened on Friday

In the US, Fed chair Powell gave a clear signal that he is ready to start cutting interest rates already in September. He said that upside risk to inflation has diminished, while downward risk to the labour market has increased. Yields on 2Y and 10Y US-treasuries dropped around 8 and 5 bp, respectively during Friday's session. USD weakened with EUR/USD up around 0.6% on Friday, briefly rising above the 1.12 mark. USD/JPY is now around the lowest point in 2024 and testing the level from 5 August, which was the lowest in 2024.

We changed our ECB call, meaning that now we expect ECB to cut policy rates at the upcoming ECB meeting on 12 September, in line with consensus and market pricing. The reason for the change is not due to baseline projection of the euro area inflation path, but the weak growth development and the labour market through the summer have changed the probability distribution in our view around the inflation path towards the policy-relevant horizon, see Reading the Markets EUR - The new issuance season has begun. We pencil in a September 24 rate cut from the ECB, 23 August.

Market movements

Equities: Global equities were higher on Friday and showed gains last week. Like this week, the past week was loaded with significant events in the latter half, including PMI data and Powell's speech at Jackson Hole on Friday. Although Powell did not introduce any new economic policies, he confidently declared that the economy has achieved a soft landing, signalling a time for policy adjustment. Investors embraced this message of a soft landing, driving shares higher, particularly in cyclical sectors and notably in small caps. Should this soft-landing scenario persist for an extended period, we believe there is substantial potential for continued outperformance in small-cap stocks. In the US, the indices showed the following movements: Dow +1.1%, S&P 500 +1.2%, Nasdaq +1.5%, Russell 2000 +3.2%. Asian markets are presenting a mixed picture this morning, with Japanese stocks notably underperforming. Both US and European futures are trending lower today.

FI: Global yields ended a smidgen lower on Friday, after a choppy session, especially in the afternoon around Powell's speech in Jackson hole. While Powell did not give guidance on the size of the upcoming rate cut(s), his key message was that 'The time has come for policy to adjust. The direction of travel is clear, and the timing and pace of rate cuts will depend on incoming data, the evolving outlook, and the balance of risks' 2y treasuries dropped 8bp on the speech to trade at 3.92%, while the 10y ended about 5bp lower at 3.80%.

FX: The end to last week saw the USD sell-off on Powel'’s rate-cut preparedness which brought EUR/USD back close to the 1.12 mark. Also risk-sensitive currencies in the likes of ZAR, AUD, NZD and NOK all rallied as we headed into the weekend. Noteworthy, SEK was relatively immune to the big moves in broader cross asset markets. Overnight it has been relatively quiet although the opening has seen some of the safe havens like CHF gain modestly.

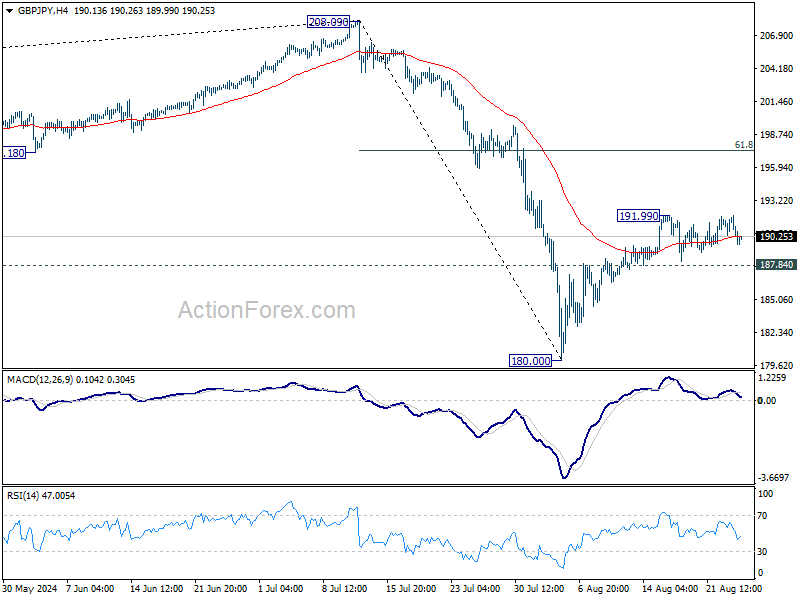

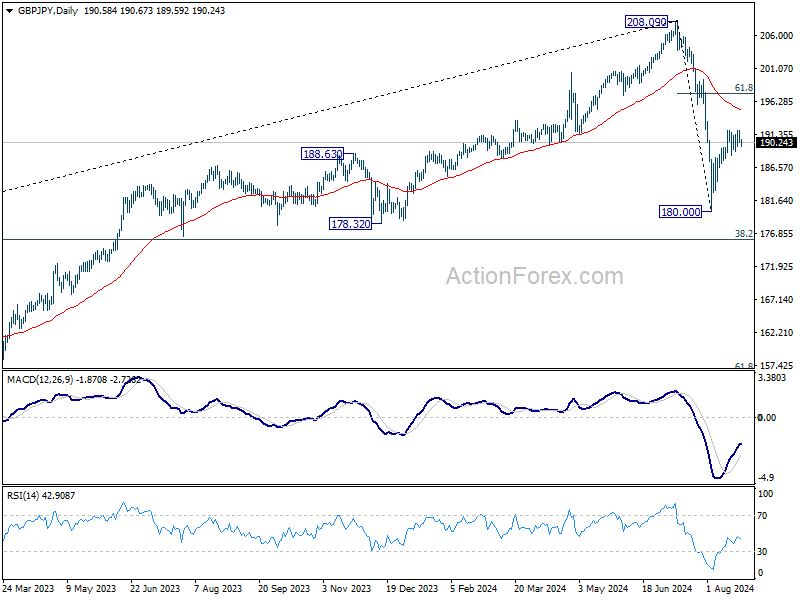

GBP/JPY Daily Outlook

Daily Pivots: (S1) 190.01; (P) 191.02; (R1) 191.77; More...

Intraday bias in GBP/JPY remains neutral for the moment, as range trading continues below 191.99. On the upside, above 191.99 will target 61.8% retracement of 208.09 to 180.00 at 197.35, as the second leg of the corrective pattern from 208.09. On the downside, however, firm break of 187.84 support will argue that rebound from 180.00 has completed, and turn bias back to the downside for retesting 180.00 instead.

In the bigger picture, price actions from 208.09 are seen as a correction to whole rally from 123.94 (2020 low). Current development suggests that the first leg has completed and the range of medium term consolidation should be set between 38.2% retracement of 123.94 to 208.09 at 175.94 and 208.09.

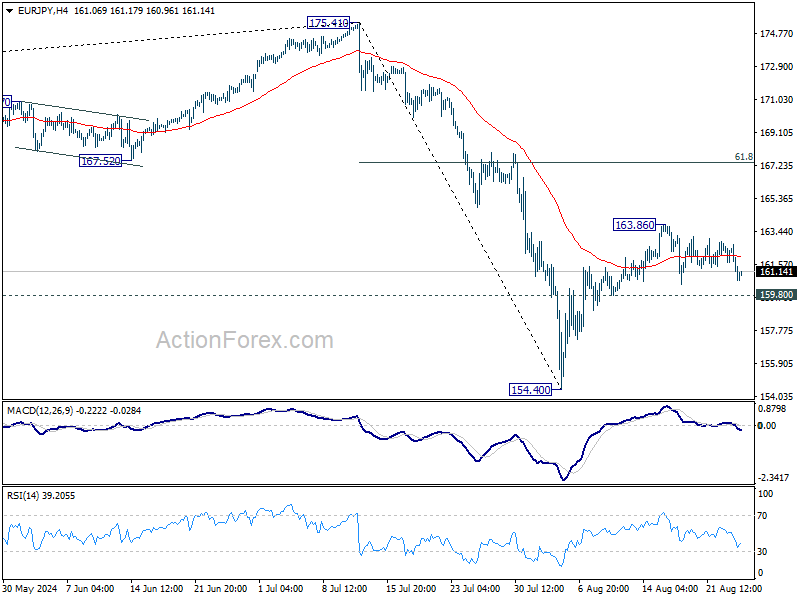

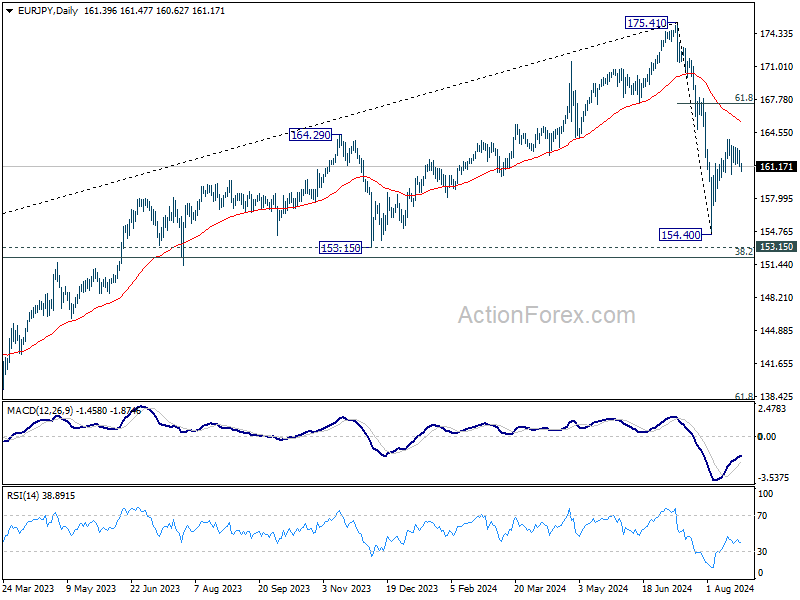

EUR/JPY Daily Outlook

Daily Pivots: (S1) 160.94; (P) 161.83; (R1) 162.44; More....

Intraday bias in EUR/JPY remains neutral as range trading continues below 163.86. On the upside, break of 163.86 will target 61.8% retracement of 175.41 to 154.40 at 167.38, as the second leg of the corrective pattern from 175.41. On the downside, however, firm break of 159.80 support will suggest that the rebound from 154.40 has completed, and turn bias back to the downside for 154.40 instead.

In the bigger picture, price actions from 175.41 are seen as correction to rally from 114.42 (2020 low). Current development suggests that the first leg has completed. The range of consolidation should be seen between 38.2% retracement of 114.42 to 175.41 at 152.11 and 175.41 high.

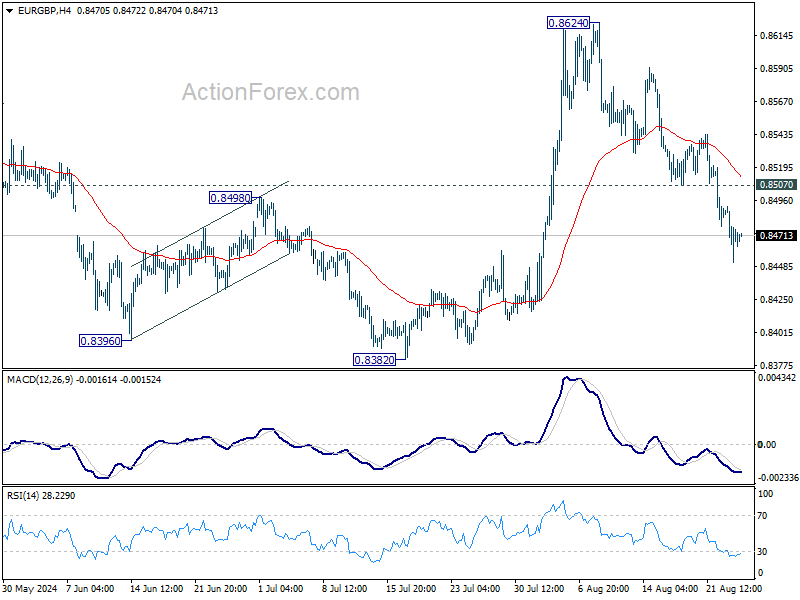

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8450; (P) 0.8472; (R1) 0.8491; More....

EUR/GBP's fall from 0.8624 is in progress and intraday bias stays on the downside. for retesting 0.8382 low. Decisive break there will resume larger down trend. On the upside, above 0.8507 support turned resistance will turn intraday bias neutral first.8507 support turned resistance will turn intraday bias neutral first.

In the bigger picture, while the rebound from 0.8382 is strong, there is no confirmation of trend reversal yet. As long as 0.8643 resistance holds, down trend from 0.9267 could still resume through 0.8382 at a later stage towards 0.8201 (2022 low). However, firm break of 0.8643 will indicate that such down trend has completed, and turn outlook bullish for 0.8764 resistance next.

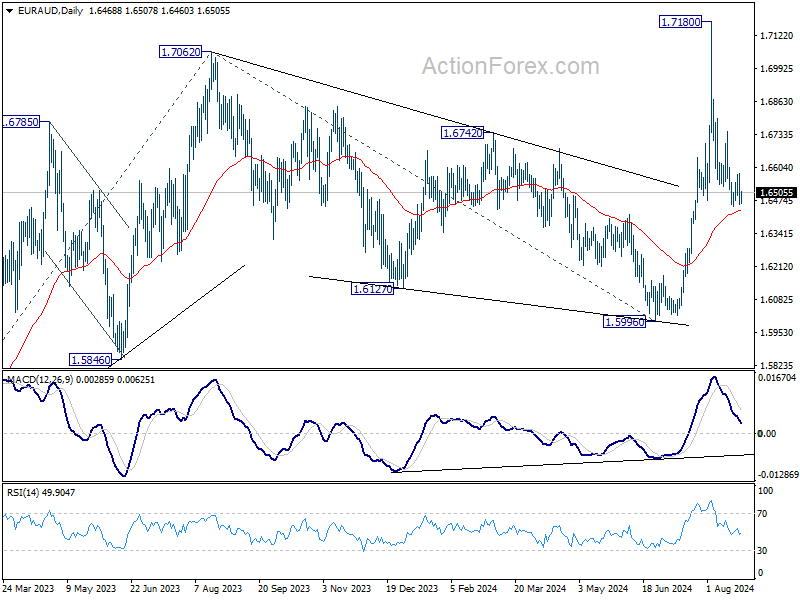

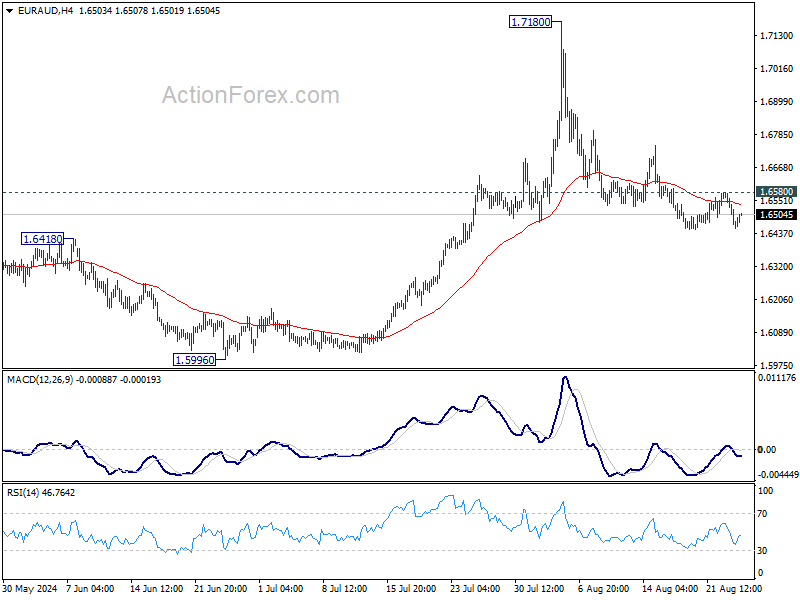

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6424; (P) 1.6503; (R1) 1.6549; More...

Intraday bias in EUR/AUD stays neutral first. On the downside, sustained trading below 55 D EMA (now at 1.6432) will argue that rise from 1.5996 has completed at 1.7180 Deeper fall would then be seen back to this support. Nevertheless, strong rebound from current levels, followed by break of 1.6580 resistance, will argue that pullback from 1.7180 has completed already. Intraday bias will then be back on the upside for stronger rebound.

In the bigger picture, corrective fall from 1.7062 medium term top should have completed at 1.5996. Larger up trend from 1.4281 (2022 low) is resuming. Next target is 61.8% projection of 1.4281 to 1.7062 from 1.5996 at 1.7715. However, sustained break of 55 D EMA will dampen this bullish view and extend medium term range trading.