Sample Category Title

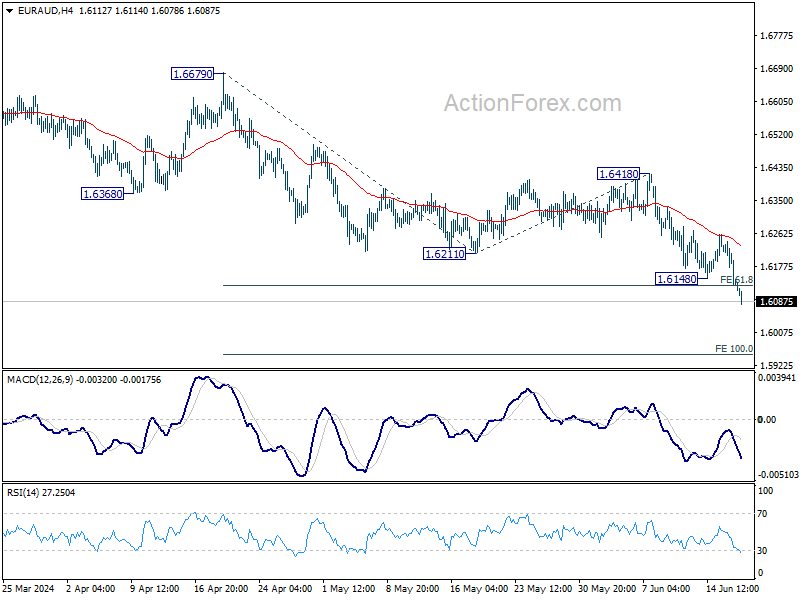

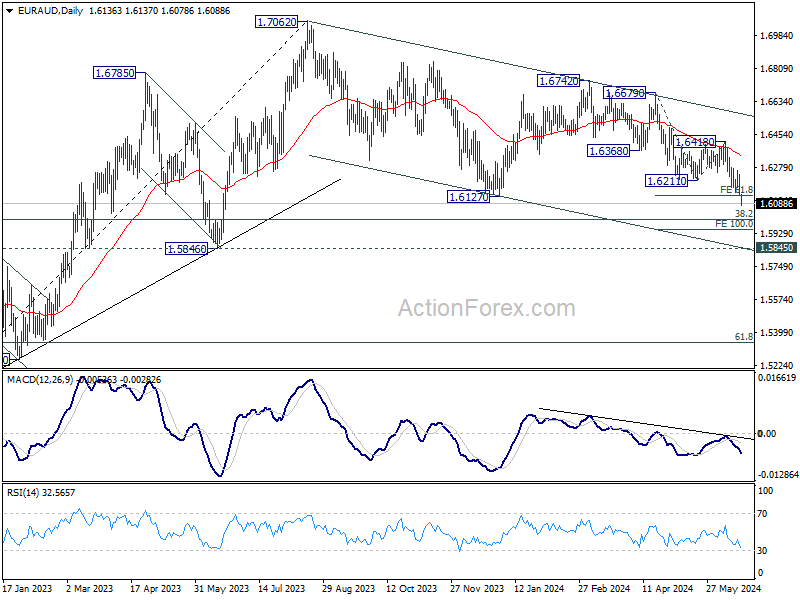

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6093; (P) 1.6172; (R1) 1.6212; More...

EUR/AUD's down trend resumed by breaking through 1.6148 temporary low and intraday bias is back on the downside. Next target is 100% projection of 1.6679 to 1.6211 from 1.6418 at 1.5950. On the upside, above 1.6148 minor resistance will turn intraday bias neutral and bring consolidations again, before staging another decline.

In the bigger picture, fall from 1.7062 medium term top is seen as a correction to the up trend from 1.4281 (2022 low). In case of deeper fall, strong support is expected around 1.5846 and 38.2% retracement of 1.4281 to 1.7062 at 1.6000 to bring rebound. Break of 1.7062 is in favor as a later stage.

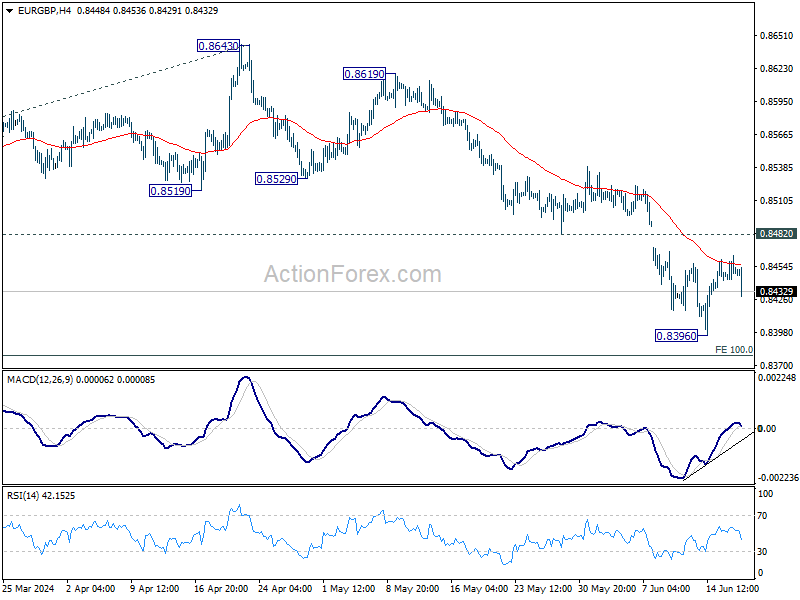

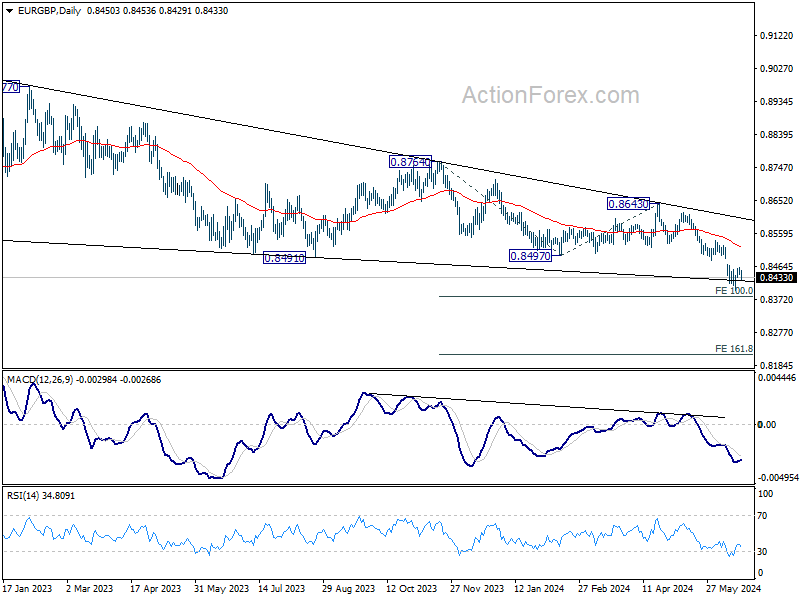

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8442; (P) 0.8453; (R1) 0.8463; More...

Intraday bias in EUR/GBP remains neutral first as consolidations continue above 0.8396. Outlook will remain bearish as long as 0.8482 support turned resistance holds. Below 0.8396 will resume larger down trend to 0.8376 projection level next.

In the bigger picture, down trend from 0.9267 (2022 high) is in progress. Next target is 100% projection of 0.8764 to 0.8497 from 0.8643 at 0.8376. Sustained break there will target 161.8% projection at 0.8211 next. For now, outlook will remain bearish as long as 0.8643 resistance holds, even in case of stronger rebound.

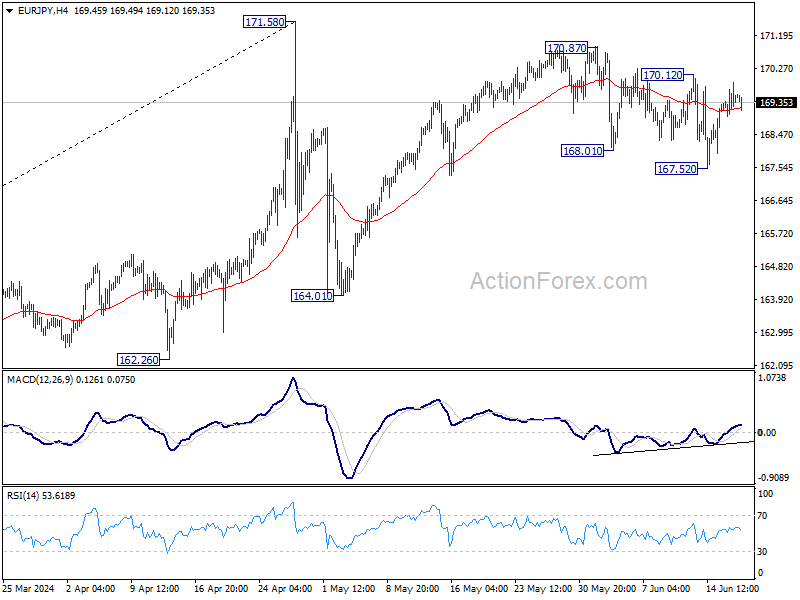

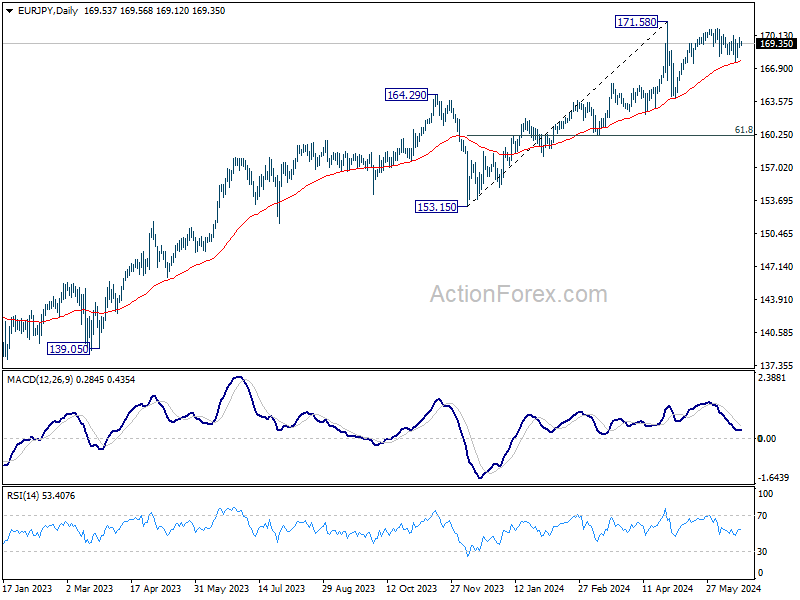

EUR/JPY Daily Outlook

Daily Pivots: (S1) 169.04; (P) 169.47; (R1) 169.98; More...

Intraday bias in EUR/JPY stays neutral first. On the upside break of 170.12 resistance will argue that pull back from 170.87 has completed at167.52, after drawing support from 55 D EMA. Intraday bias will be back on the upside for 170.87 and then 171.58 high.

In the bigger picture, as long as 55 W EMA (now at 159.83) holds, price actions from 171.58 medium term top are seen as as correcting the rise from 153.15 only. That is, larger up trend remains in favor to continue as a later stage. However, sustained break of 55 W EMA will argue that larger scale correction is underway and target 153.15 support.

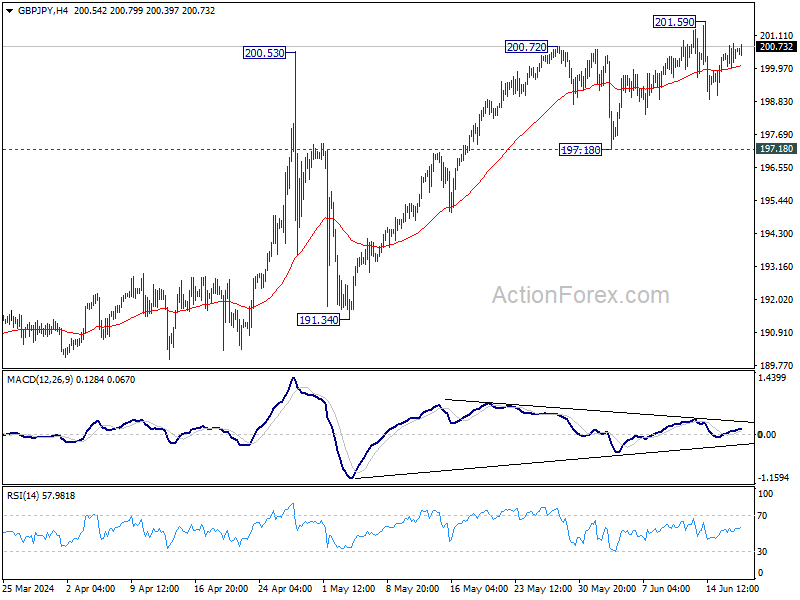

GBP/JPY Daily Outlook

Daily Pivots: (S1) 200.14; (P) 200.49; (R1) 200.97; More...

GBP/JPY is extending the consolidations below 201.59 and intraday bias stays neutral. Further rally is expected as long as 197.18 support holds. However, considering bearish divergence condition in 4H MACD, firm break of 197.18 will confirm short term topping, and turn bias back to the downside for 191.34 support instead.

In the bigger picture, as long as 188.63 resistance turned support holds, long term up trend is expected to continue. Next target is 100% projection of 155.33 to 188.63 from 178.32 at 211.62.

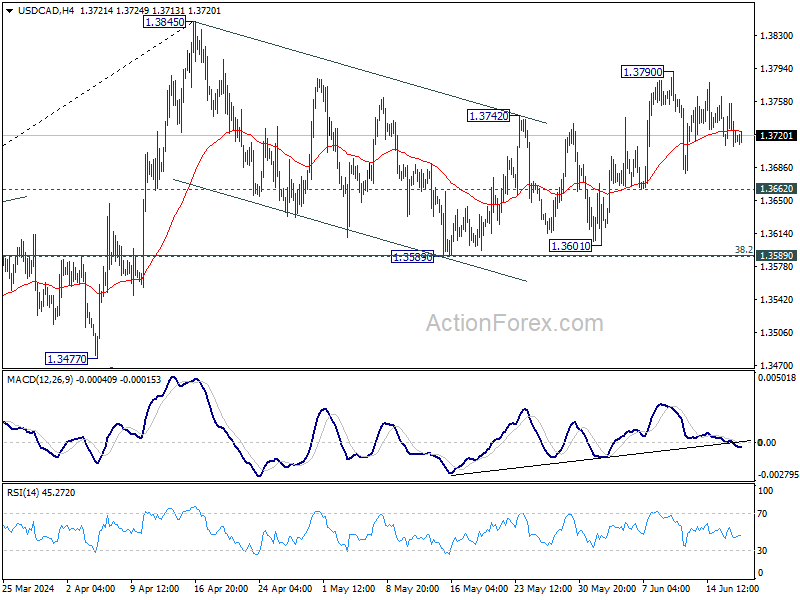

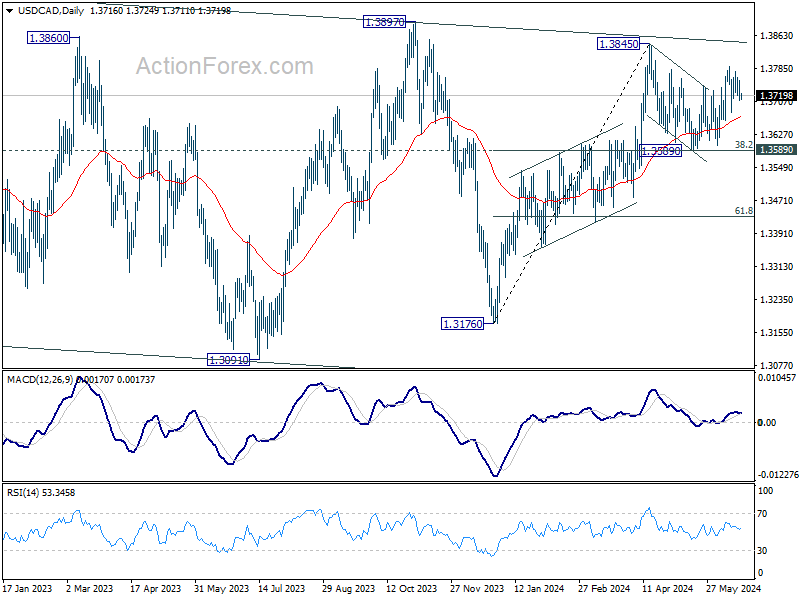

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3699; (P) 1.3728; (R1) 1.3747; More...

No change in USD/CAD's outlook as range trading continues. Intraday bias remains neutral for the moment. Corrective fall from 1.3845 should have completed already. Further rally is expected as long as 1.3662 support holds. Break of 1.3790 will target a retest on 1.3845 first. Nevertheless, break of 1.3662 will turn bias to the downside to extend the corrective pattern from 1.3845 with another falling leg.

In the bigger picture, price actions from 1.3976 (2022 high) are viewed as a corrective pattern. In case of another fall, strong support should emerge above 1.2947 resistance turned support to bring rebound. Firm break of 1.3976 will confirm up resumption of whole up trend from 1.2005 (2021 low). Next target is 61.8% projection of 1.2401 to 1.3976 from 1.3176 at 1.4149.

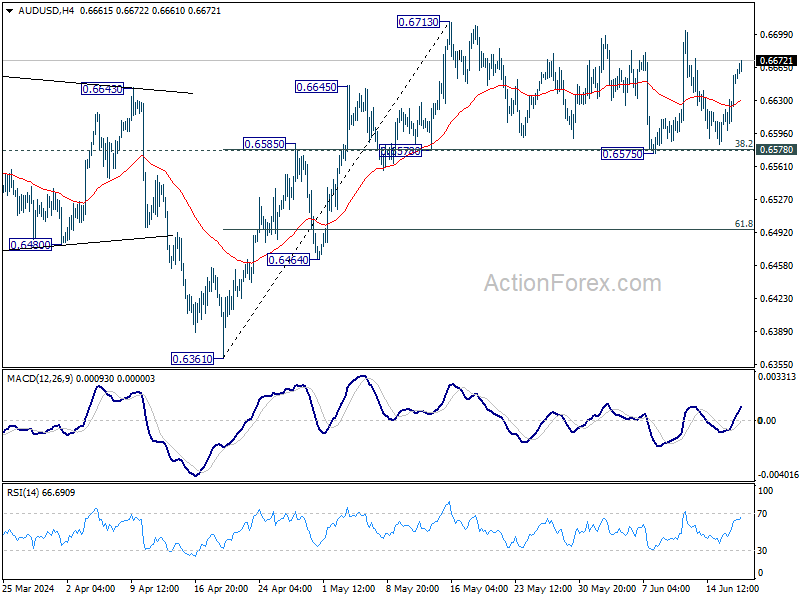

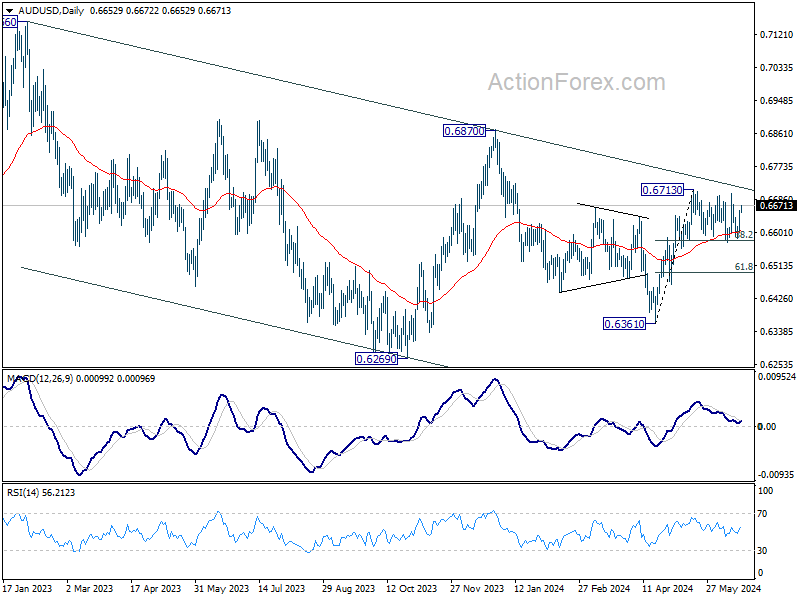

AUD/USD Daily Report

Daily Pivots: (S1) 0.6619; (P) 0.6639; (R1) 0.6676; More...

Range trading continues in AUD/USD and intraday bias remains neutral. Further rally remains in favor with 0.6578 cluster support (38.2% retracement of 0.6361 to 0.6713 at 0.6579) intact. On the upside, firm break of 0.6713 will resume whole rise from 0.6361 to 0.6870 resistance next. However, sustained break of 0.6578 will dampen this bullish view, and bring deeper fall to 61.8% retracement at 0.6495.

In the bigger picture, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern to the down trend from 0.8006 (2021 high). Fall from 0.7156 (2023 high) is seen as the second leg, which could have completed at 0.6269 already. Rise from there is seen as the third leg which is now trying to resume through 0.6870 resistance.

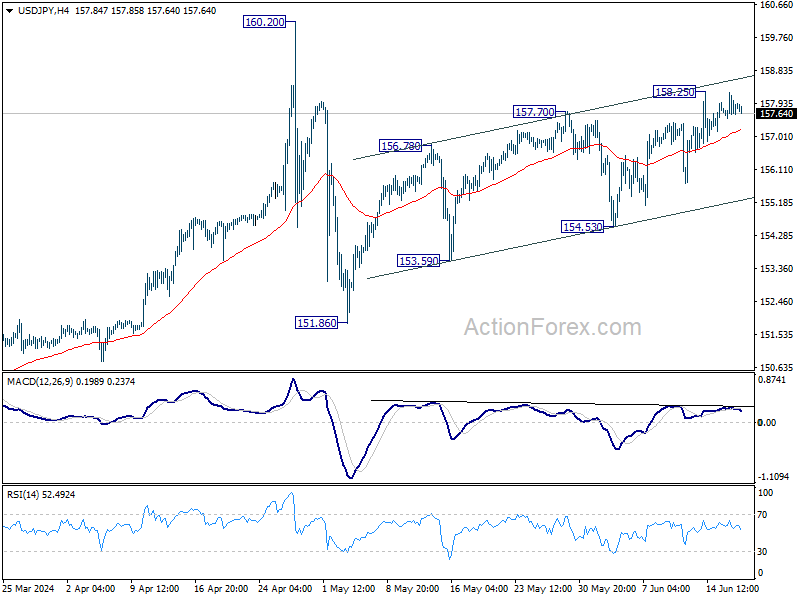

USD/JPY Daily Outlook

Daily Pivots: (S1) 157.50; (P) 157.87; (R1) 158.21; More...

No change in USD/JPY's outlook and intraday bias stays neutral. Further rally would be in favor as long as 154.53 support holds. Break of 158.25 will resume the choppy rise from 151.86 towards 160.20 high. But upside should be limited there, at least on first attempt.

In the bigger picture, price actions from 160.20 medium term top are seen as a corrective pattern to rise from 150.25 only. Another rally is still expected at a later stage through 160.02 to resume the larger up trend. However, decisive break of 150.87 will argue that larger correction is possibly underway, and target 146.47 support next.

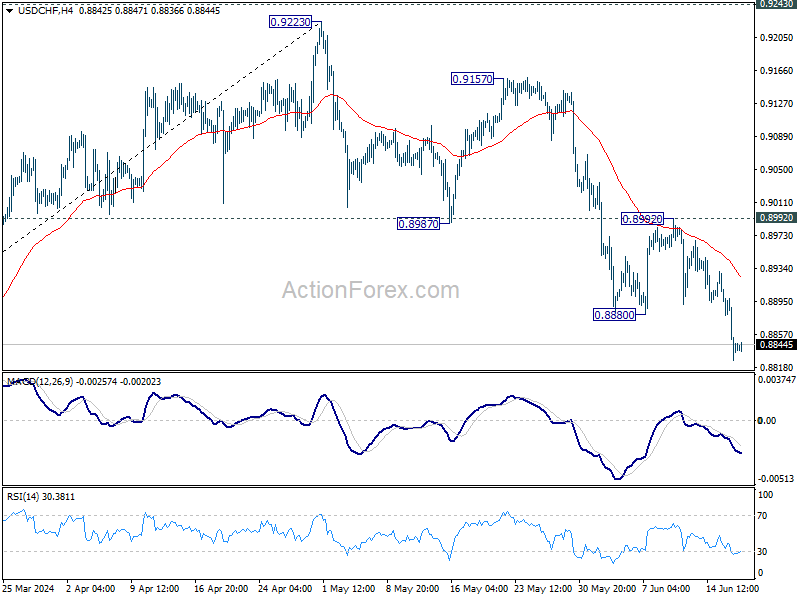

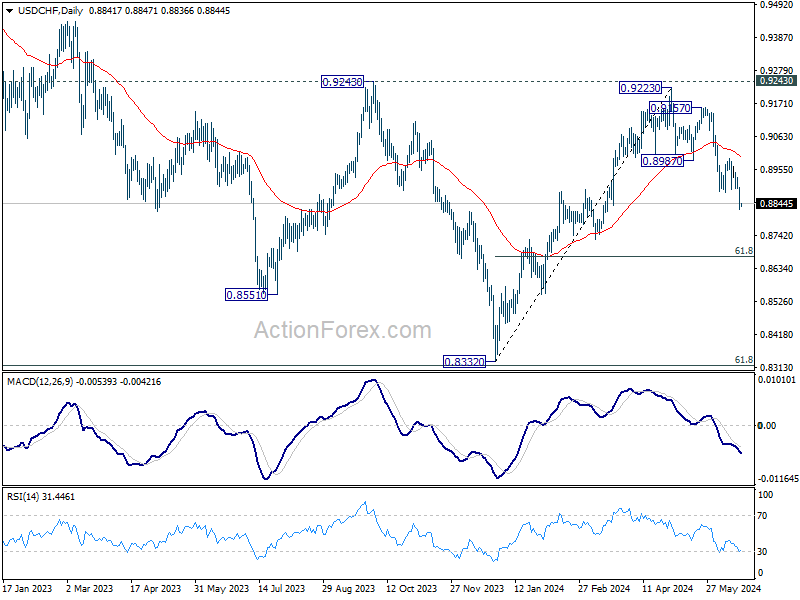

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8809; (P) 0.8860; (R1) 0.8892; More….

Intraday bias in USD/CHF stays on the downside for the moment. Rise from 0.8332 could have completed at 0.9223, ahead of 0.9243 key resistance. Further decline would be seen to 61.8% retracement of 0.8332 to 0.9223 at 0.8672 next. For now, risk will stay on the downside as long as 0.8992 resistance holds, in case of recovery.

In the bigger picture, price actions from 0.8332 medium term bottom are seen as developing into a corrective pattern to the down trend from 1.0146 (2022 high). Rejection by 0.9243 resistance affirms this case, and maintains medium term bearishness. While more range trading could be seen between 0.8332/0.9243 first, downside break out is mildly in favor at a later stage.

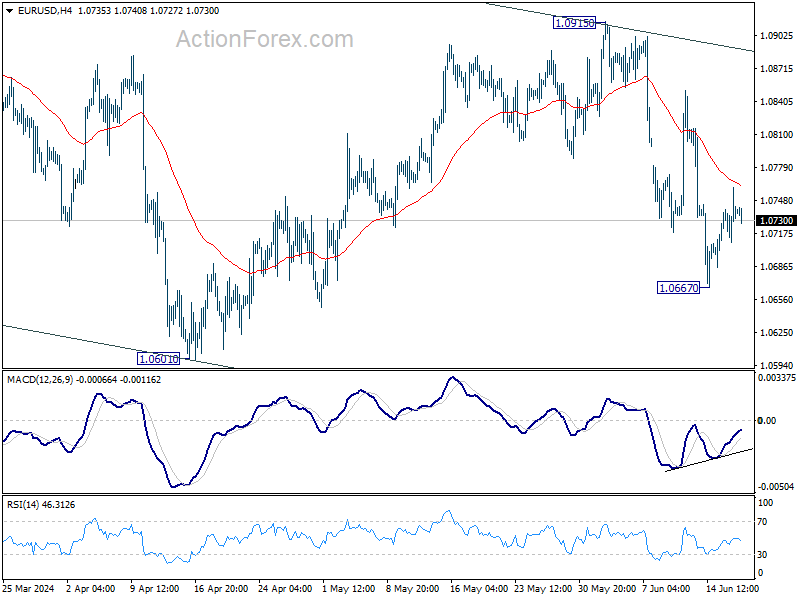

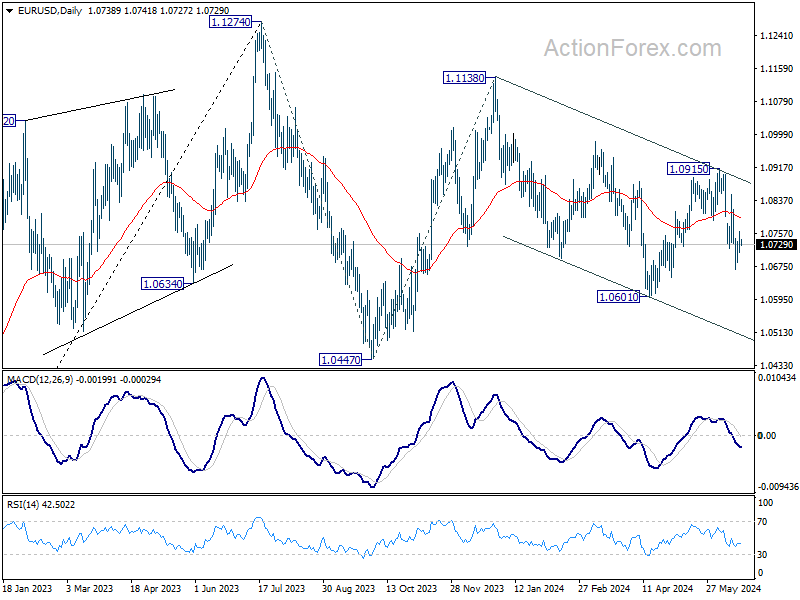

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0713; (P) 1.0737; (R1) 1.0765; More....

Intraday bias in EUR/USD remains neutral and outlook is unchanged. More consolidations could be seen but further fall is expected as long as 55 4H EMA (now at 1.0763) holds. Fall from 1.0915 is seen as another leg in the larger corrective pattern. Below 1.0677 will target 1.0601 low first. Firm break there will target channel support at 1.0500 next.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern that's still in progress. Break of 1.0601 will target 1.0447 support and possibly further to 100% projection of 1.1274 to 1.0447 from 1.1138 at 1.0311. For now, this will remain the favored case as long as 1.0915 resistance holds, in case of rebound.

BoE Still Has Work to Do to Bring Inflation Back Under Control

Markets

Market focus shifted back to the US yesterday. After last week’s softer than expected price data, US retail sales for the second consecutive month suggested that consumer demand might be slowing. It could point to a better supply-demand balance that might help inflation to slow further. May headline sales only rose a meagre 0.1% M/M coming on the back of a (downwardly) revised 0.2% decline in April. Control group sales, seen as a proxy for private consumption in GDP calculations, rebounded 0.4% (vs 0.5% consensus), but this wasn’t enough to reverse last months -0.5% decline. After a limited rebound on Monday, US yields again ceded between 6 bps (5-y) and 5 bps (30-y). US yields across the curve are again closing in on the lows touched end last week (2-y 4.71%, 10-y 4.22%, 30-y 4.35%). Money markets discount two 25 bps rate cuts by the end of the year. A long line up of Fed governors (with individual nuances) reiterated they need more than one month of better inflation data to be confident to start an easing cycle. European/German bond yields early in the session tried to regain some ground after the recent safe have decline, but this was also reversed after the US data. German yields eased between 0.9 bps (5-y) and 2.3 bps (30-y). Some (temporary) calm also returned to intra-EMU bond markets The French 10-y yield spread (vs Germany) narrowed 2 bps (to 77 bps). A similar easing was seen for the likes of Greece (-4 bps), Italy (-3 bps), Spain and Portugal (-2 bps). European equities also tried to move away from last week’s lows (EuroStoxx 50 + 0.72%). The S&P 500 and the Nasdaq again finished at (marginally higher) closing record levels. The dollar after the US retail sales data reversed earlier intraday gains, but in the end any losses were limited (DXY close 105.26, EUR/USD 1.0740). USD/JPY even closed slightly stronger at 157.86.

US markets are closed today for the Junetheenth holiday and there are few data in EMU. Except for important news from the political scene in France, trading in European markets probably will be technical in nature. The EU commission is expected to open an excessive debt procedure against seven member states, including France. This comes as no surprise but won’t help to restore calm on intra-EMU (bonds) markets.

UK May CPI data were close to expectations this morning. Headline CPI eased to 0.3% M/M bringing the Y/Y measure exactly at the 2% BoE target. Core inflation also, as expected, eased to 3.5% from 3.9%. Still the decline in services inflation (5.7% from 5.9%) was less than hoped for. Even as the inflation target for the headline figure has been reached, underlying data suggested that the BoE still has work to do to bring inflation back under control in a sustainable way. This suggests balanced communication at tomorrow’s BoE policy meeting. In a first reaction, sterling tentatively gains a few ticks (EUR/GBP 0.8446).

News & Views

The US’ Congressional Budget Office jacked up its deficit forecast for the running fiscal year (through September) by about 27% to a whopping $1.92tn, or 6.7% of GDP. Doing so the nonpartisan budget watchdog no longer expects the deficit to shrink compared to last FY ($1.69tn, 6.3% of GDP). The new estimate is some $400 bn higher than February’s and reflects additional spending for Ukraine, the Biden administration student-loan relief plans as well as an increase in estimated Medicaid spending. In the updated 10 year outlook, the CBO is projecting deficits equal or in excess of 5.5%. “Since at least 1930, deficits have not remained that large for more than five years in a row.”, the CBO said in an umpteenth warning to the unsustainable fiscal situation. The new economic forecasts assume faster growth (2%) and inflation (2.7% vs 2.1% in the February forecast), leading the CBO to be more cautious on Fed rate cuts. They now expect a first move to happen in 2025Q1 vs mid-2024 previously.

Japan’s Ministry of Finance is considering a shift towards issuing bonds with shorter maturities, Bloomberg reported this morning based on draft proposal. It would mean a major policy shift from the past where the ministry tended to extend the maturity of debt, locking in the extremely low (and negative) rates for as long as possible. The proposal comes after the BoJ recently abandoned its yield curve programme, raised its policy rate out of negative territory and is planning to cut bond purchases from the current JPY 6tn per month. Yields across the spectrum have risen, especially at the long end of the curve as a result.

Graphs

GE 10y yield

The ECB cut its key policy rates by 25 bps at the June policy meeting. A more bumpy inflation path in H2 2024, the EMU economy gradually regaining traction and the Fed’s higher for longer US strategy make follow-up moves difficult. Markets are coming to terms with that. For the time being, though, the political narrative dominates. After hitting a new YtD top at 2.7%, the German 10-yr yield corrected lower on safe haven bids.

US 10y yield

The Fed is seeking more evidence than just one slower-than-expected (May) CPI is providing. Upgraded inflation forecasts and a higher neutral rate complicate the exact timing of a first cut further. June dots suggest one move in 2024 followed by four more next year. Markets are positioned more aggressively, turning the recent low in yields into a technical support zone. The US 10-y yield is testing the downside of the 4.2/4.7% trading range.

EUR/USD

EUR/USD is trapped in the 1.06-1.09 range. The desynchronized rate cut cycle with the ECB exceptionally taking the lead, strong US May payrolls and a swing to the right in European elections pulled the pair away from 1.09 resistance. The Fed meeting balanced the weaker than expected US CPI outcome. Euro fragility makes a return to the 1.06 downside more likely than not.

EUR/GBP

Debate at the Bank of England is focused at the timing of rate cuts. Slower than expected April disinflation and a surprise general election on July 4 suggest that a June cut in line with the ECB looks improbable. Sterling gained momentum with money markets now discounting a Fed-like scenario. EUR/GBP tested the 2023 & 2024 lows near 0.85. Euro weakness eventually pulled the trick after French president Macron called snap elections following a weak showing in EU elections.