Sample Category Title

Fed’s Kugler encouraged by renewed progress on inflation

In a speech, Fed Governor Adriana Kugler acknowledged that while inflation remains too high, she is "encouraged" by the overall progress and outlook. Kugler expressed "cautious optimism" based on recent economic and inflation data, suggesting that Fed is on track towards its 2% inflation target.

She noted that progress may have stalled in the first quarter of the year, but subsequent information on economic activity, the labor market, and inflation indicates "renewed progress."

Kugler indicated that, "If the economy evolves as I am expecting, it will likely become appropriate to begin easing policy sometime later this year."

Fed’s Logan: Neutral rate may be higher post-pandemic, inflation risks persist

In a moderated Q&A session overnight, Dallas Fed President Lorie Logan stated, "From a monetary policy perspective, we're in a good position, we're in a flexible position to watch the data and be patient." She highlighted the need for "several months" of favorable data to gain confidence that inflation is on track to the 2% target.

Despite signs that the economy is balancing better, Logan expressed concerns about persistent upside risks to inflation. She also suggested that the neutral rate setting may now be higher than pre-pandemic levels.

"We've just been surprised by how well the economy has performed at these higher levels of rates," she noted. Logan attributed this to structural changes in the economy, implying that the neutral rate might be higher than it was in the decade before the pandemic.

Fed’s Musalem calls for sustained favorable conditions before rate cuts

In his debut speech, St. Louis Federal Reserve President Alberto Musalem emphasized the need for sustained favorable conditions before considering a reduction in interest rate. He stated that he needs to see a period of favorable inflation, moderating demand, and expanding supply, which could take "months, and more likely quarters" to materialize.

He also did not rule out additional rate hikes if inflation remains significantly above 2% or if it reaccelerates, although he noted this was not his base case scenario.

Musalem also expressed uncertainty about whether the current monetary policy stance is sufficiently restrictive, pointing out that financial conditions "feel accommodative for some parts of the economy while restrictive for others."

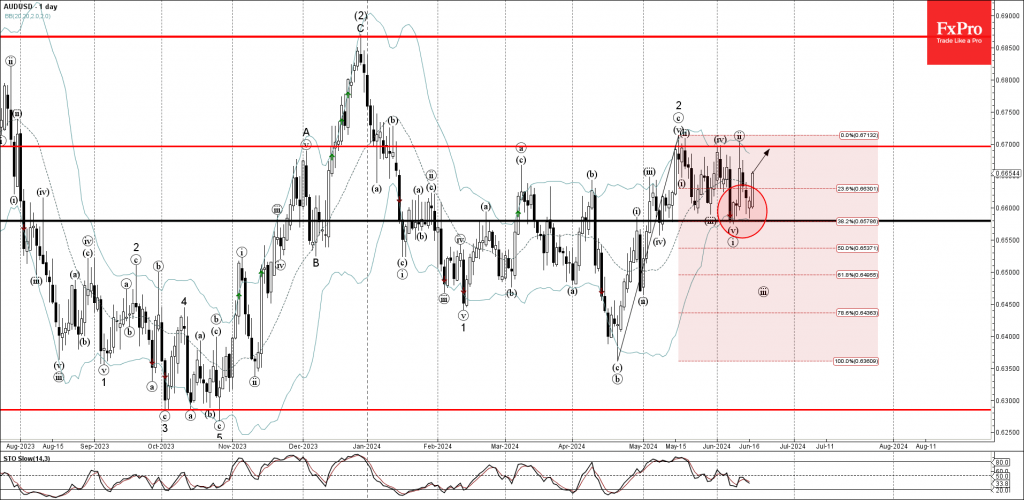

AUDUSD Wave Analysis

- AUDUSD reversed from key support level 0.6580

- Likely to rise to resistance level 0.6700

AUDUSD currency pair recently reversed up from the key support level 0.6580 (which has been reversing the price from the start of May) coinciding with the lower daily Bollinger Band.

The support level 0.6580 was further strengthened by the 38.2% Fibonacci correction of the previous upward impulse from April.

Given the strength of the support level 0.6580 and the strong USD sales, AUDUSD currency pair can be expected to rise further to the next resistance level 0.6700, which stopped the previous waves 2, iv and ii.

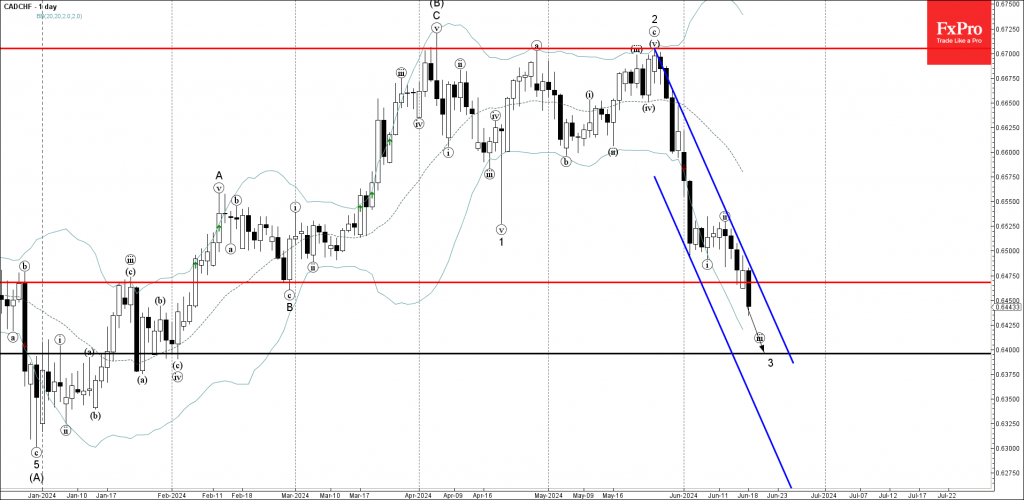

CADCHF Wave Analysis

- CADCHF broke key support level 0.6465

- Likely to fall to support level 0.6400

CADCHF currency pair under the bearish pressure after breaking the key support level 0.6465 (which started the impulse wave C in February).

The breakout of the support level 0.6465 accelerated the active impulse waves 3 and iii, which belong to the higher impulse wave (C) from August.

CADCHF currency pair can be expected to fall further to the next support level 0.6400, low of wave iv, and the target for the completion of the active impulse wave 3.

NZD: Market Breakdown Ahead of GDP Release

The NZDUSD pair rose nearly a quarter of a percent to the 0.6110s after the US Dollar weakened following disappointing US Retail Sales data for April and May. The lower-than-expected retail sales growth in May and downward revisions for April indicate a slowdown in US consumer spending, leading to revised market expectations of future US interest rate cuts. The probability of the Federal Reserve cutting rates by 0.25% in September increased from 55% to 60%, with a 68% chance of a total 0.25%-0.50% cut by then. Meanwhile, the New Zealand Dollar remains broadly weaker due to a slump in the country's services sector and consecutive quarters of negative GDP growth, suggesting a recession and increasing the likelihood of a rate cut by the Reserve Bank of New Zealand in November. Despite recent Fed officials' hawkish comments, the NZD's performance is weighed down by domestic economic challenges and rate cut expectations.

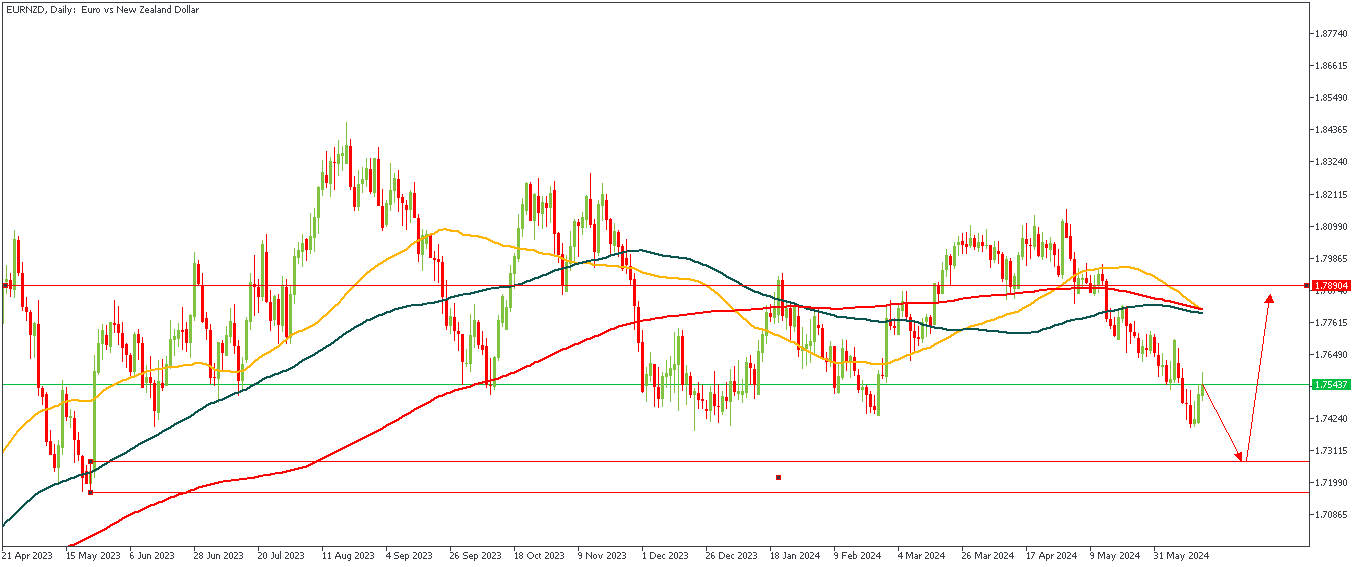

EURNZD – D1 Timeframe

The rectangular zone on the daily timeframe chart of EURNZD above depicts a drop-base-rally demand zone that was formed right after a sweep of liquidity from the previous low; making it a pretty strong area of price action to consider. Also, the zone fits into the 88% region of the Fibonacci retracement tool, thus confirming my bullish sentiment.

Analyst’s Expectations:

- Direction: Bullish

- Target: 1.78904

- Invalidation: 1.71636

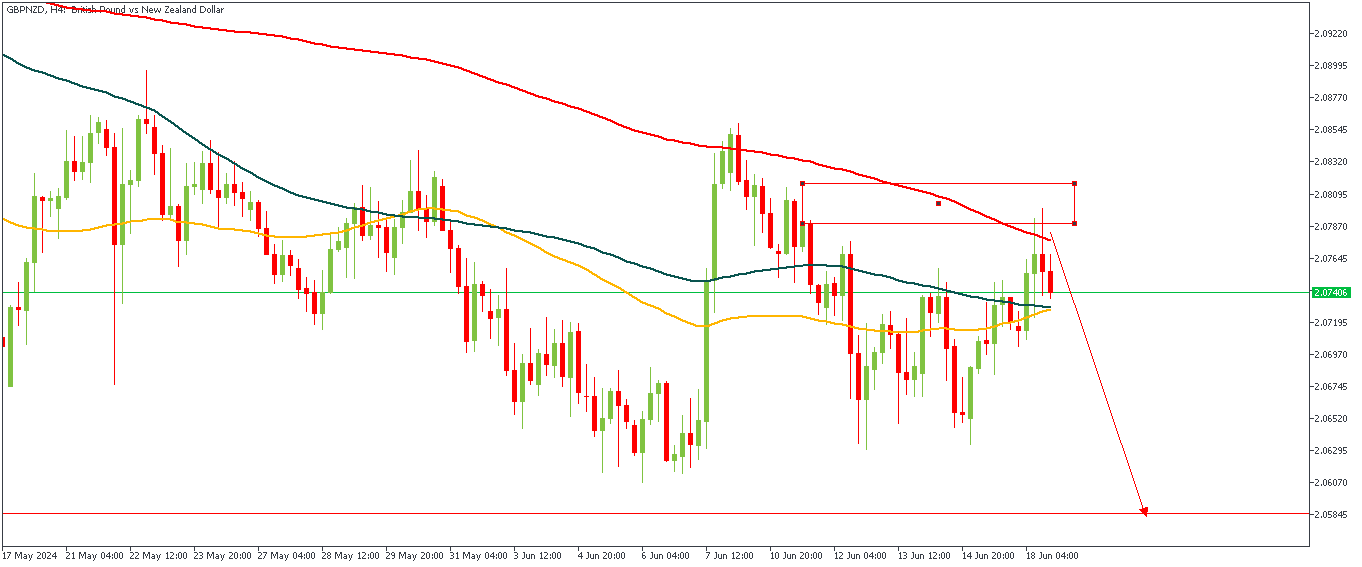

GBPNZD – H4 Timeframe

GBPNZD on the 4-hour timeframe presents a clean argument in favor of the bearish sentiment. Here, we see price trade into a supply zone that is nested on top of the 200-day moving average and get rejected immediately after. This gives an indication that the current move could play out as a bearish impulse; hence, my sentiment on GBPNZD is bearish.

Analyst’s Expectations:

- Direction: Bearish

- Target: 2.05870

- Invalidation: 2.08167

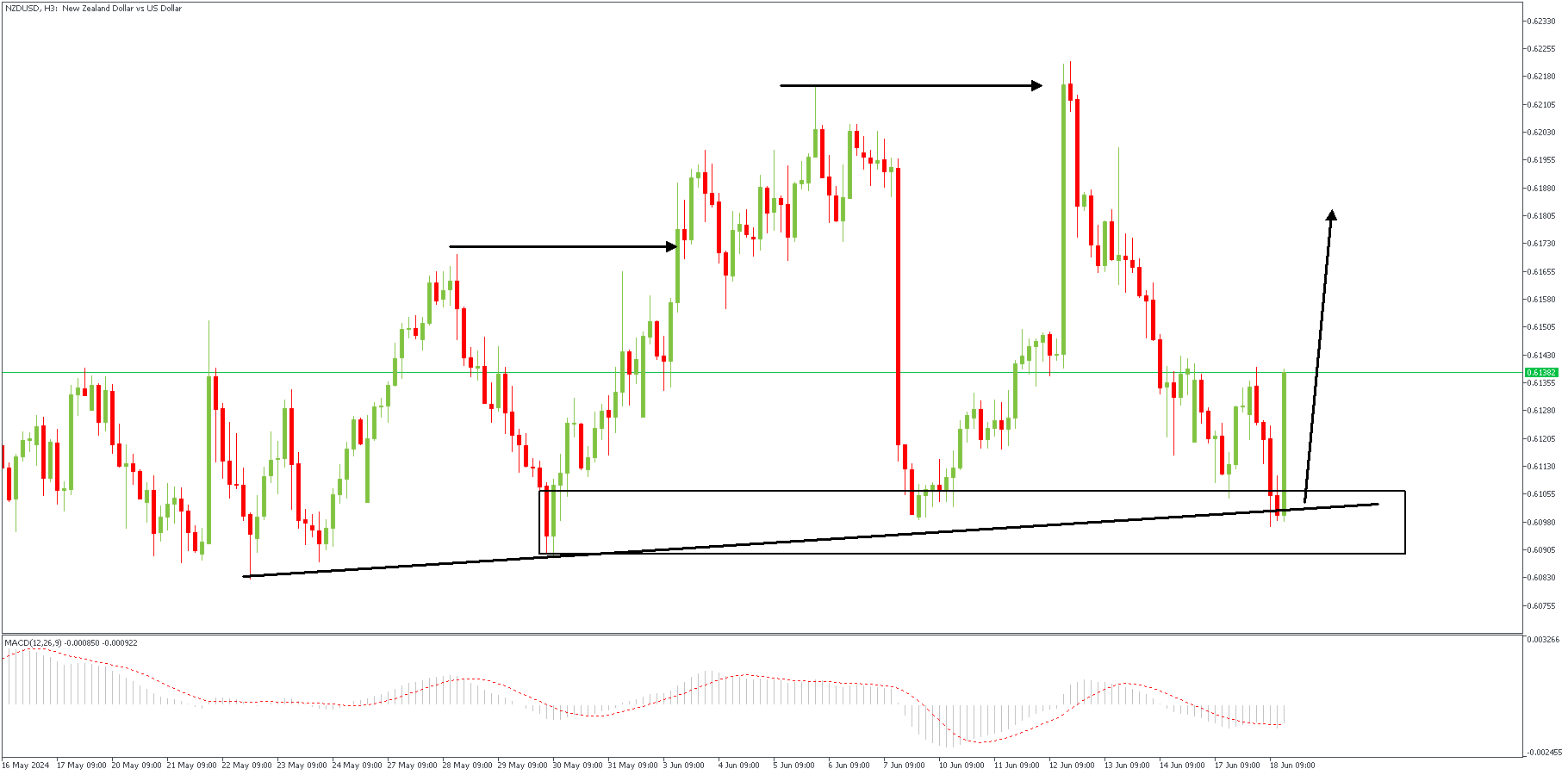

NZDUSD – H3 Timeframe

NZDUSD on the 3-hour timeframe has just bounced off the drop-base-rally demand zone. The trendline support provides an additional confluence as it overlaps the demand zone. The final piece that brings it all together is the MACD indicator’s signal of a bullish onset as seen on the indicator window of the attached chart. These factors point me clearly in favor of a bullish move for NZDUSD.

Analyst’s Expectations:

- Direction: Bullish

- Target: 0.60430

- Invalidation: 0.61565

Fed’s Barkin optimistic on inflation, emphasizes “sustainment” and “broadening”

Richmond Fed President Thomas Barkin expressed optimism about the inflation outlook in an interview with MNI Webcast. Barkin noted that we are "on the back side of inflation," indicating that inflationary pressures are easing.

He highlighted that the next several months will be critical in gaining more insights and that Fed is well-positioned from a policy standpoint to react and ease montary policy.

Barkin emphasized two key themes: "sustainment" and "broadening."

Sustainment refers to maintaining a downward trend in both headline and core inflation, ensuring that it continues on a path towards 2% target. Broadening implies that this trend should be consistent across a wide range of goods and services in the inflation basket.

Fed’s Williams foresees gradual rate cuts amid continued disinflation

New York Fed President John Williams shared optimistic views on the US economy in an interview with FOX Business today. Williams highlighted encouraging signs that supply and demand are rebalancing, contributing to a "disinflationary process continuing." He anticipates that inflation will keep decreasing throughout the second half of this year and into the next.

Williams expects interest rates to "come down gradually over the next couple of years" as inflation moves back towards the Fed's 2% target and the economy follows a strong, sustainable path.

However, he refrained from specifying the timing of the first rate cut, stating, "I'm not going to make a prediction" about the exact path of policy.

Williams emphasized that future decisions will be data-dependent, noting, "I think that things are moving in the right direction" for eventual policy easing.

SNB Expected to Cut, But Risk of Disappointment

- Expectations of a June cut by the SNB have been gaining traction

- But inflation picture isn't entirely favourable; weak franc doesn’t help

- A lot of uncertainty awaits the SNB’s decision due Thursday at 07:30 GMT

Will the SNB cut rates again?

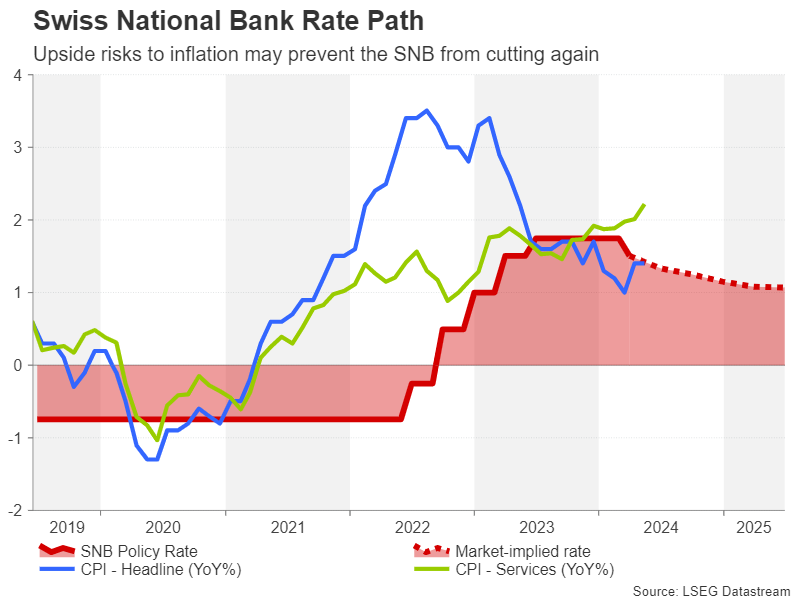

The Swiss National Bank (SNB) got the ball rolling with interest rate cuts back in March, becoming the first major central bank to start its easing cycle. Inflation in Switzerland only peaked at 3.5% y/y and has been within the Bank’s 0-2% target for the past year. Investors might therefore be right to think that further easing is on the cards at the June meeting.

However, inflation may not be quite as subdued as the headline CPI figures suggest. Services inflation remains on an uptrend, reaching 2.2% y/y in May - the highest since 2001. But even headline CPI has started to creep up again, rising to 1.4% y/y in April and holding steady in May. Moreover, the Swiss franc has been on the slide this year, adding to price pressures via higher import costs.

SNB President Thomas Jordan, who is due to step down from his post in September, recently said he sees small upside risks to inflation, with the weaker Swiss franc being the likely source. Those comments at the end of May caught investors off guard, triggering a sizeable reversal in the franc against both the US dollar and the euro (although possible SNB intervention in the foreign exchange market may also have been a factor for the rebound).

Are expectations of a cut justified?

Yet, most investors have been ratcheting up their bets of a follow-up 25-basis-point cut in June since Jordan’s remarks and market pricing currently points to around a 68% probability of such an action. Quite possibly, the rally in the franc is seen as lessening the upside risks to inflation and that’s why rate cut expectations have been moving in tandem with franc appreciation.

However, the Swiss currency is still more than 5% down against the dollar in the year-to-date and more than 2% lower versus the euro. When also considering the acceleration in services inflation and the stronger-than-expected GDP growth in the first quarter, there is little urgency for SNB policymakers to cut again so soon.

Swissie could be in for a bumpy ride

All this has set the stage for some heightened volatility on Thursday as a ‘surprise’ decision to stand pat would wrong foot many investors, while a rate cut would also come as unexpected to some traders. For the franc, the June decision will likely be critical for its near-term outlook as the chances of further gains depend on it.

Dollar/franc is in danger of breaching the key support barrier of the 200-day moving average (MA) in the 0.8890 area. If the SNB disappoints the dovish expectations and keeps rates unchanged at 1.50%, this could drag the pair down to the 50% Fibonacci retracement of the late December-early May uptrend at 0.8777 before testing the 61.8% Fibo of 0.8672.

But if the Bank does deliver a cut and hints at more to follow, dollar/franc could rebound towards the June peak of 0.8993 before aiming for the 50-day MA at 0.9061.

All in all, the SNB’s decision of whether to ease policy again in June is likely to be much more of a close call than the market pricing suggests and there will be a surprise element whatever the outcome.