Sample Category Title

Commodity Currencies on the Rise: Market Focus Shifts to US and Canadian Data

Commodity-linked currencies continue to strengthen, while the US dollar remains under pressure amid easing geopolitical tensions and a shift in investor preference towards riskier assets. Reports of a temporary ceasefire between the US and Iran have helped stabilise sentiment and reduced demand for safe-haven assets, supporting currencies sensitive to the global economic cycle, including the Australian and Canadian dollars.

Another factor weighing on the dollar is expectations around Federal Reserve monetary policy, which remain highly sensitive to incoming macroeconomic data. Lower US Treasury yields and ongoing uncertainty بشأن inflation dynamics are reinforcing cautious market positioning. Against this backdrop, attention is turning to upcoming US data releases, including inflation, consumer sentiment, and business activity indicators, which may reshape interest rate expectations.

AUD/USD

AUD/USD continues its upward move after breaking out of the 0.6840–0.6960 range. The next upside targets are the yearly highs in the 0.7160–0.7180 area. The bullish scenario would be invalidated if the pair falls and holds below 0.7020.

Key events for AUD/USD:

- Today at 15:30 (GMT+3): US Core CPI

- Today at 17:00 (GMT+3): University of Michigan inflation expectations

- Today at 17:00 (GMT+3): University of Michigan consumer sentiment

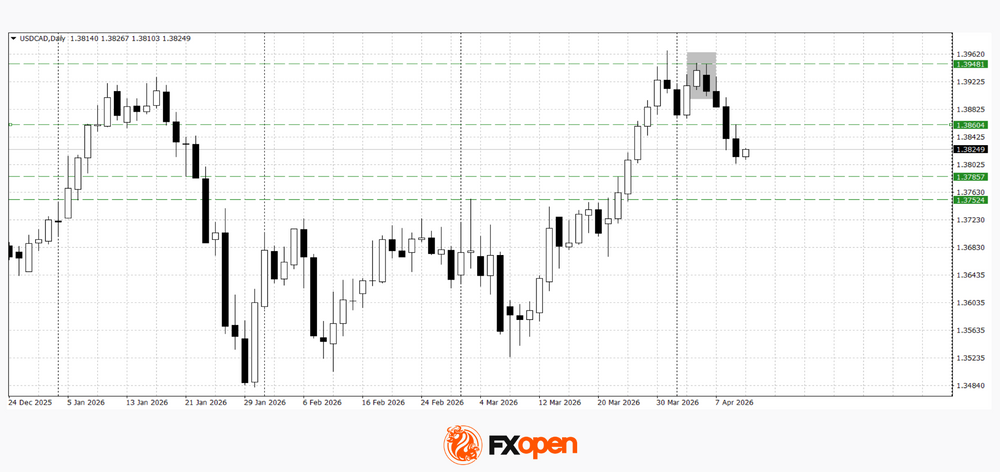

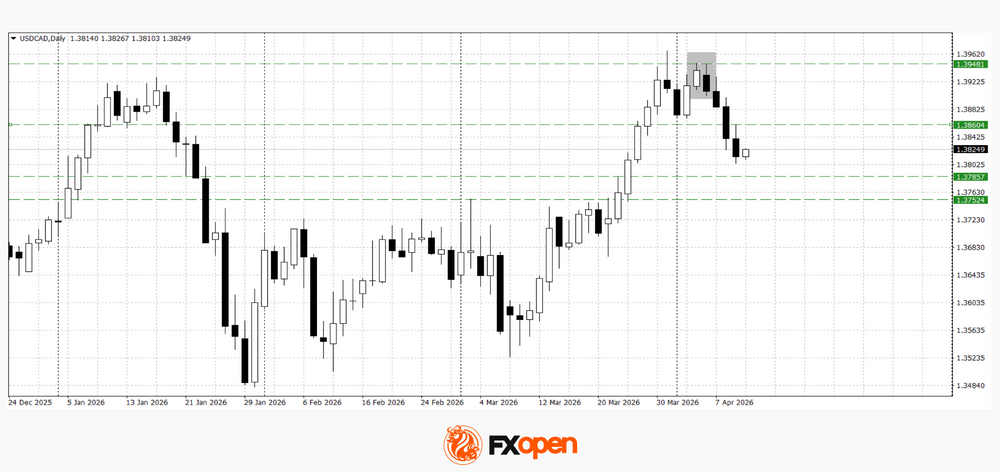

USD/CAD

USD/CAD is trending lower, continuing the move driven by Canadian dollar strength. The downside breakout reflects a shift in favour of commodity currencies, supported by both the broader macro backdrop and expectations ahead of key Canadian data, including the employment report.

Technical analysis suggests a potential decline towards the 1.3750–1.3780 range, as several reversal patterns have formed on the daily timeframe. The bearish outlook would be invalidated if the pair rises and holds above 1.3860.

Key events for USD/CAD:

- Today at 15:30 (GMT+3): Canada unemployment rate

- Today at 15:30 (GMT+3): average hourly wages (permanent employees)

- Today at 22:30 (GMT+3): CFTC net speculative positions in crude oil

The strength in commodity currencies is being driven by a combination of easing geopolitical risks, a weaker US dollar, and rising demand for risk assets. Breakouts in AUD/USD and USD/CAD reinforce the likelihood of trend continuation; however, upcoming US and Canadian data remain a key source of uncertainty. Depending on the outcome, the current momentum may either extend or shift into a phase of consolidation.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips (additional fees may apply). Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

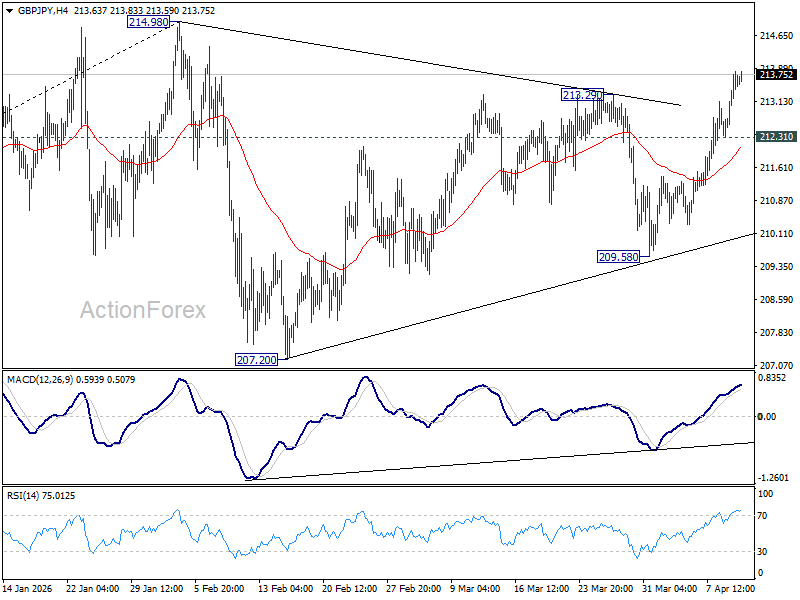

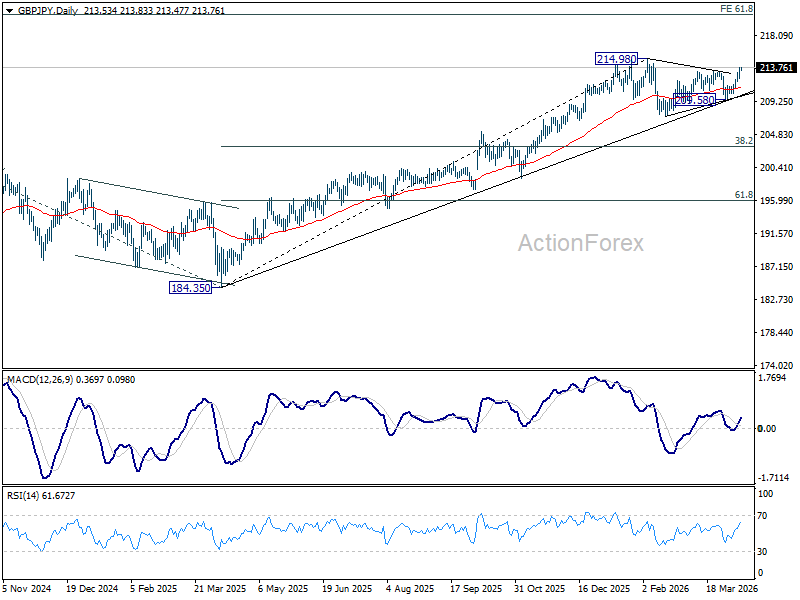

GBP/JPY Daily Outlook

Daily Pivots: (S1) 212.69; (P) 213.27; (R1) 214.22; More...

Intraday bias in GBP/JPY remains on the upside for retesting 214.98 high. Decisive break there will confirm larger up trend resumption. On the downside, below 212.31 minor support will turn bias neutral first. But risk will now remain on the upside as long as 209.58 support holds, in case of retreat.

In the bigger picture, up trend from 123.94 (2020 low) is still in progress. Firm break of 214.98 will target 61.8% projection of 148.93 (2022 low) to 208.09 (2024 high) from 184.35 at 220.90. This will remain the favored case as long as 55 W EMA (now at 204.08) holds, even in case of another deep pullback.

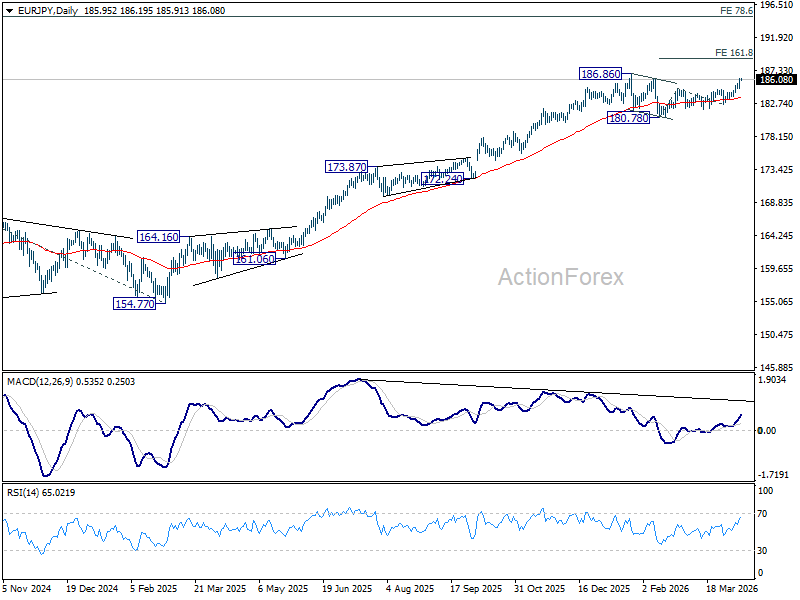

EUR/JPY Daily Outlook

Daily Pivots: (S1) 185.15; (P) 185.71; (R1) 186.54; More...

Intraday bias in EUR/JPY remains on the upside for retesting 186.86 high. Firm break there will resume larger up trend. Next near term target is 161.8% projection of 180.78 to 184.75 from 182.56 at 188.98. On the downside, below 184.77 minor support will delay the bullish case and turn intraday bias neutral first.

In the bigger picture, consolidations from 186.86 might still extend. But as long as 55 W EMA (now at 176.56) holds, the larger up trend from 114.42 (2020 low) remains intact. Firm break of 186.86 will pave the way to 78.6% projection of 124.37 (2022 low) to 175.41 (2025 high) from 154.77 at 194.88 next.

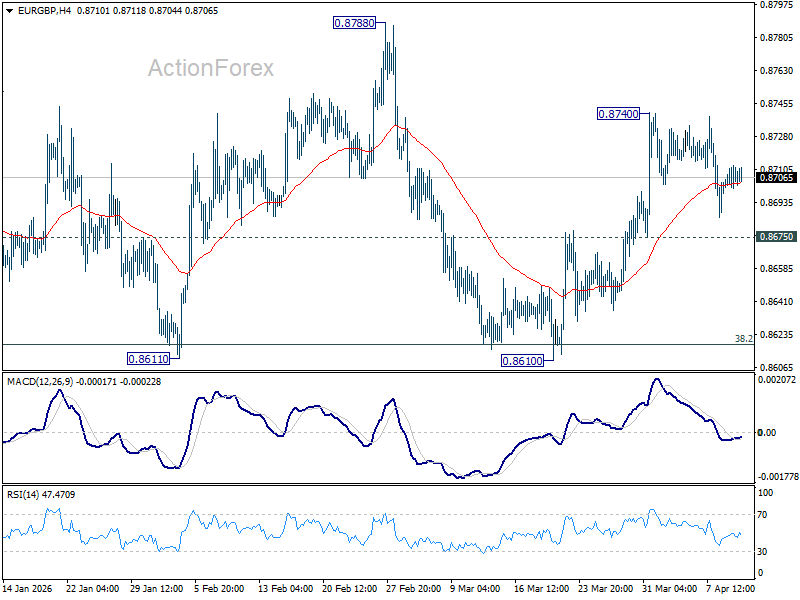

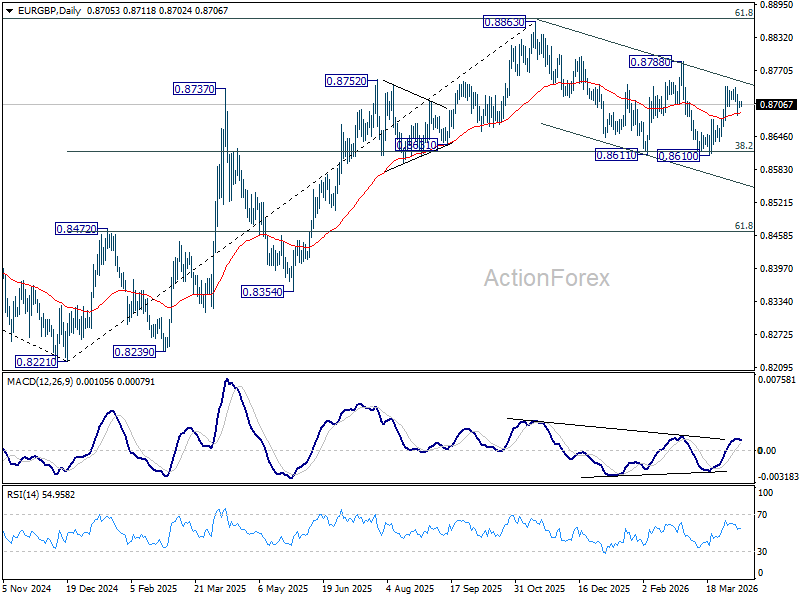

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8699; (P) 0.8708; (R1) 0.8717; More…

EUR/GBP is still extending consolidations below 0.8740 and intraday bias stays neutral. On the upside, above 0.8740 will resume the rebound from 0.8610 short term bottom to 0.8788 resistance next. However, break of 0.8675 will bring retest of 0.8610 low instead.

In the bigger picture, strong support was seen again from 38.2% retracement of 0.8821 to 0.8863 at 0.8618. Break of 0.8788 resistance will argue that larger rise from 0.8221 might be resume to resume through 0.8863. Nevertheless, sustained trading below 0.8618 should confirm reversal, and bring deeper fall to 61.8% retracement at 0.8466 at least.

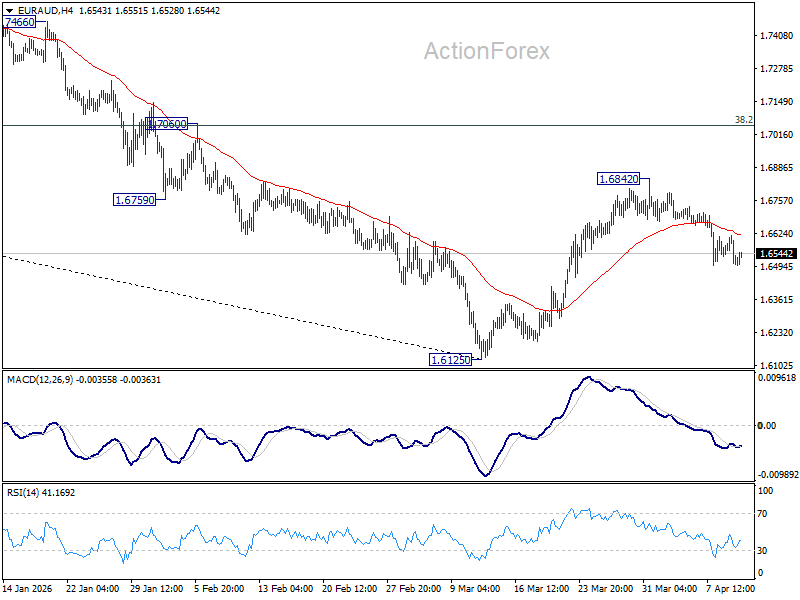

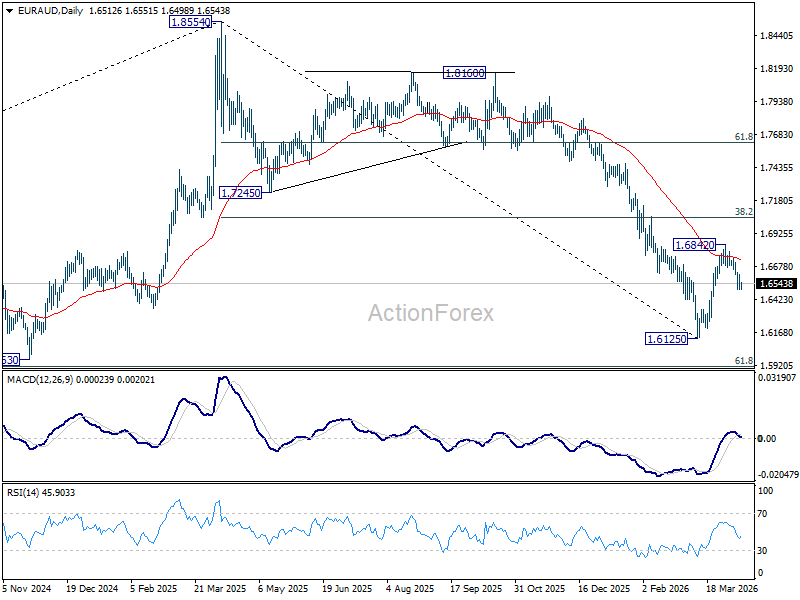

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6477; (P) 1.6548; (R1) 1.6590; More...

Intraday bias in EUR/AUD stays on the upside at this point. Corrective rebound from 1.6125 could have completed at 1.6842 after rejection by 55 D EMA (now at 1.6733). Deeper fall should be seen to retest 1.6125. Firm break there will resume larger down trend. On the upside, though, break of 1.6842 will resume the rebound to 38.2% retracement of 1.8554 to 1.6125 at 1.7053.

In the bigger picture, fall from 1.8554 medium term top is seen as reversing the whole up trend from 1.4281 (2022 low). Deeper decline should be seen to 61.8% retracement of 1.4281 to 1.8554 at 1.5913, which is slightly below 1.5963 structural support. Decisive break there will pave the way back to 1.4281. For now, risk will stay on the downside as long as 55 W EMA (now at 1.7207) holds, even in case of strong rebound.

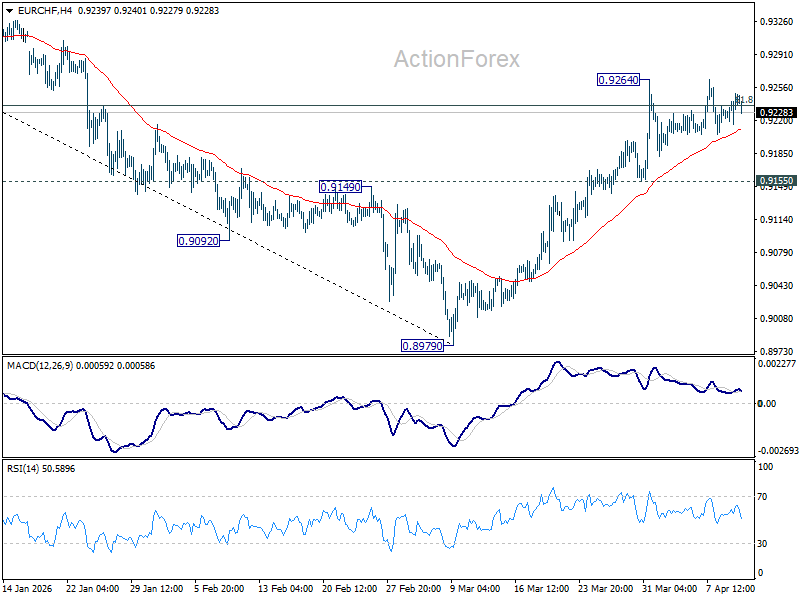

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9227; (P) 0.9240; (R1) 0.9262; More....

Intraday bias in EUR/CHF stays neutral and more consolidations could be seen below 0.9264. On the upside, sustained trading above 61.8% retracement of 0.9394 to 0.8979 at 0.9235 will pave the way to 0.9394 key resistance next. However, break of 0.9155 support will turn bias back to the downside for 0.8979 low.

In the bigger picture, as long as 55 W EMA (now at 0.9281) holds, the larger down trend from 0.9928 (2024 high) is still expected to continue through 0.8979 at a later stage. However, sustained break of 55 W EMA should confirm medium term bottoming, and bring stronger rise through 0.9394 resistance, even as a corrective move.

US Inflation Data Provides First ‘Hard’ Evidence on Economic Fall-out from the Conflict

Markets

Markets yesterday were looking for a new short-term equilibrium/new starting point as a next phase in the Middle East conflict had started. Earlier this week markets were pushed back and forth by consecutive U-turns as the war between the US and Iran unfolded. The ceasefire announced Wednesday morning avoided an outright escalation and triggered an impressive relieve short-squeeze. However, markets soon realized that reaching a sustained military & political solution faces multiple high hurdles. With Iran only allowing minimal, highly selective and strictly controlled passage through the Strait of Hormuz any relieve to supply disruptions (and price pressure) is probably hard to imagine. Israel agreeing to hold talks with Lebanon intraday eased overall market ‘hesitation’ to some extent. After Wednesday’s sharp decline, Brent oil yesterday rebounded to the $97 p/b area. This also triggered a partial reversal of Wednesday’s easing on interest rate markets. German yields rose between 2.8 bps (2-y) and 5.9 bps (30-y) with similar moves visible in the UK as markets try get further insight in the ECB’s and the BoE’s reaction function. Moves in US yields again were more modest with yields easing between 2.6 bps (5-y) and -0.2 bps (30-y). With policy still slightly above neutral, the US central bank still has some more room to maneuver with the March inflation data to be published today a first post-war reality check. A $22 bln US 30-y Treasury Bond sale tailed slightly and only met mediocre investor interest even as the yield (4.876%) was the highest monthly result since July. Equities took a breather after Wednesday’s aggressive squeeze higher (EuroStoxx 50 -0.29%; S&P 500 +0.62%). The dollar stayed on the backfoot. DXY closed at 98.8 from an open near 99.15. EUR/USD closed near 1.17. The yen still underperforms (USD/JPY close just below 159).

Asian equities this morning mostly hold a constructive bias looking forward to the US-Iran negotiations scheduled to take place in Islamabad staring tomorrow. Oil at the same time shows no clear bias (Brent $96.75). The dollar also shows no clear direction (DXY 98.9, EUR/USD 1.169, the yen still underperforms (159.3)). Aside from headlines on developments/negotiations regarding the conflict in the Middle East, US inflation data to be published today provides a first ‘hard’ evidence on the economic fall-out from the conflict. We expect US headline inflation to jump to 3.3% Y/Y (from 2.4%). The rise in core inflation for now is expected to be ‘limited‘ to 2.6% Y/Y (from 2.5%). It will be interesting to see the reaction of US markets especially in case of a higher than expected outcome. Inflation expectations measures from the U. of Michigan consumer confidence survey also deserve more than average attention.

News & Views

The Bank of Korea left its policy rate unchanged at 2.5%. The central bank kept a balanced assessment on the impact of the war in the Middle East which poses both downside growth and upside inflation risks. CPI inflation for the year is expected to considerably exceed the February forecast of 2.2%, while core inflation is also likely to be somewhat higher than the previous forecast of 2.1%. If the current shocks (energy, other commodities, supply chain disruptions) are prolonged, leading to a broadening of inflationary pressures and heightened inflation expectations, a monetary policy response is required. Departing BoK governor Rhee compared the current situation with the aftermath of the Russian invasion in Ukraine. While the economy is currently in a moderate recovery instead of facing pent-up demand, it is more vulnerable to rising inflation (expectations) because of the weaker currency and the potential for faster pass-through in prices. South Korean money markets currently discount two to three rate hikes by the BoK for this year.

The OECD’s new chief economist, Scarpetta, warned that governments that cut fuel taxes after the start of the Iran war must swiftly phase out those costly subsidies. Scarpetta said that such initiatives helped fuel inflation, store up fiscal problems and blunt incentives to cut dependence on fossil fuels. Any measures should be targeted at low-income households and energy-intensive businesses. Earlier this week, also the EC warned against turning the current energy crunch into a fiscal crisis.

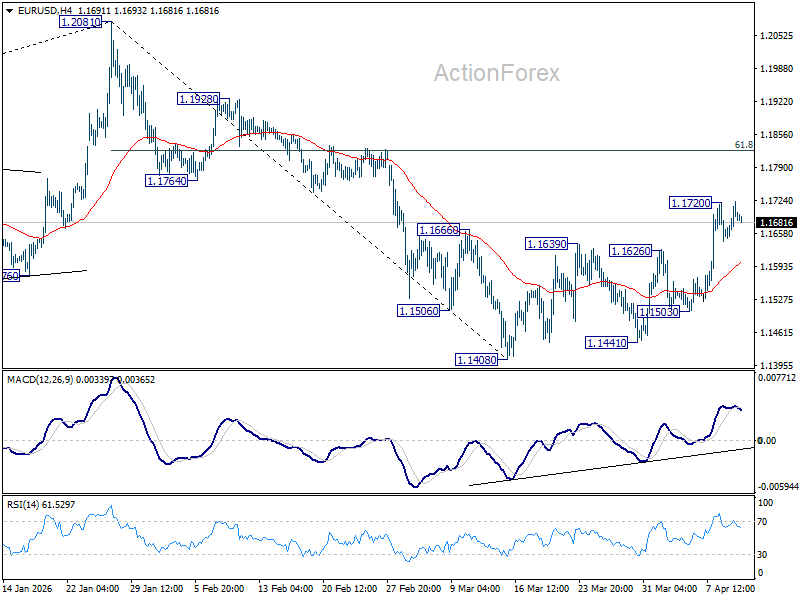

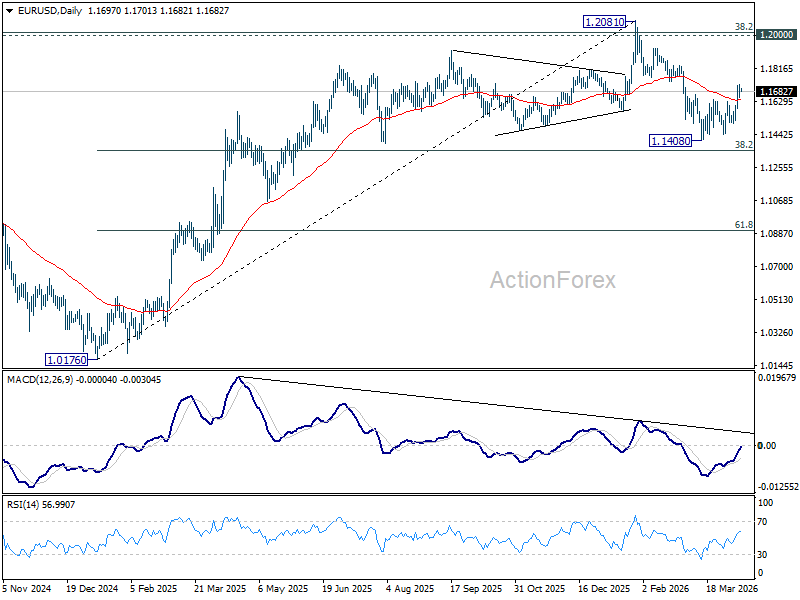

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1658; (P) 1.1692; (R1) 1.1733; More….

Intraday bias in EUR/USD stays neutral at this point. Further rise is expected as long as 55 4H EMA (now at 1.1596) holds. Fall from 1.2081 could have completed as a correction at 1.1408. Above 1.1720 will resume the rise from 1.1408 to 1.8% retracement of 1.2081 to 1.1408 at 1.1824. However, sustained break of 55 4H EMA will suggest that the rebound has completed, and bring retest of 1.1408 low instead.

In the bigger picture, the strong support from 38.2% retracement of 1.0176 to 1.2081 at 1.1353 suggests that the pullback from 1.2081 is more likely a corrective move. Strong support was also found in 55 W EMA (now at 1.1505). Focus is back on 1.2 key cluster resistance level. Decisive break there will carry long term bullish implications. Nevertheless, break of 1.1408 support will revive the case of medium term bearish trend reversal.

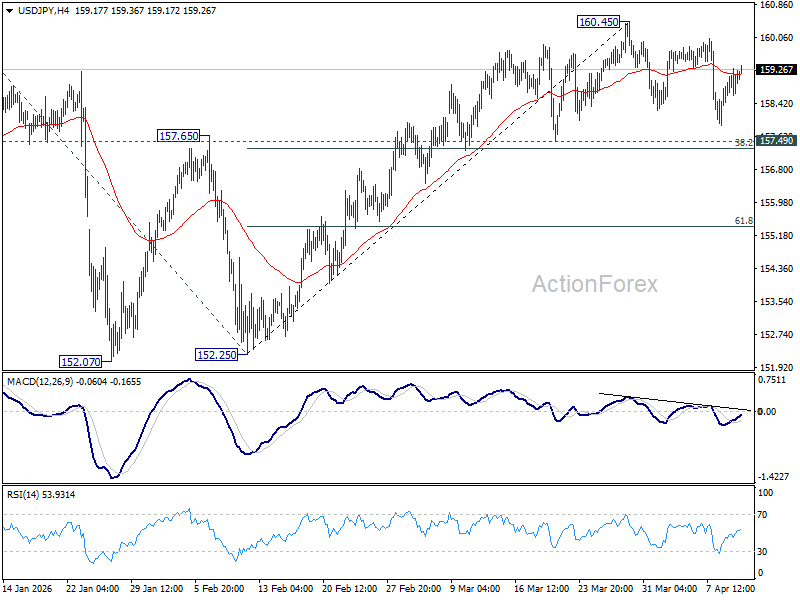

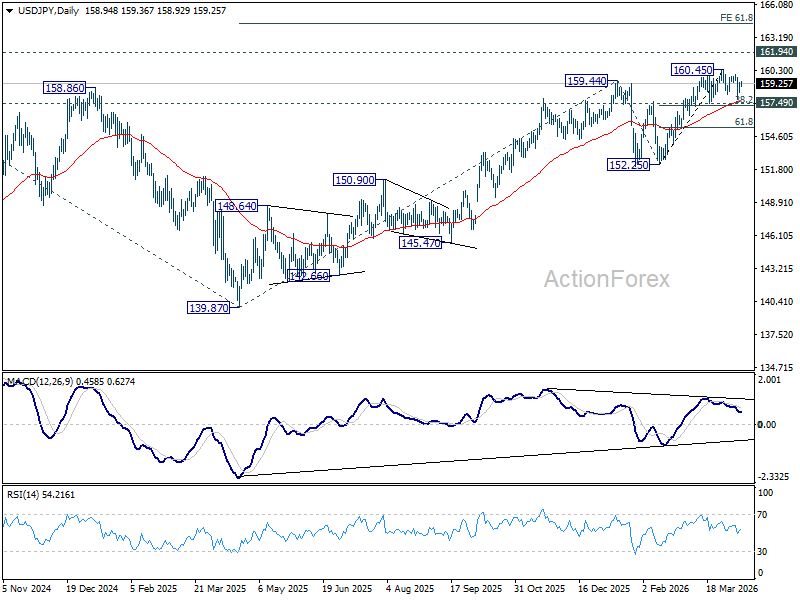

USD/JPY Daily Outlook

Daily Pivots: (S1) 158.54; (P) 158.92; (R1) 159.38; More...

USD/JPY is still extending consolidations below 160.45 and intraday bias stays neutral. Further rise is expected as long as 157.49 cluster support (38.2% retracement of 152.25 to 160.45 at 157.31) holds. Firm break of 160.45 will resume the rise from 152.25 to retest 161.94 high. However, firm break of 157.31/49 will bring deeper fall back to 61.8% retracement at 155.38 next.

In the bigger picture, outlook is unchanged that corrective pattern from 161.94 (2024 high) should have completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94. This will remain the favored case as long as 55 W EMA (now at 152.97) holds. Firm break of 161.94 will pave the way to 61.8% projection of 102.58 to 161.94 from 139.87 at 176.75.

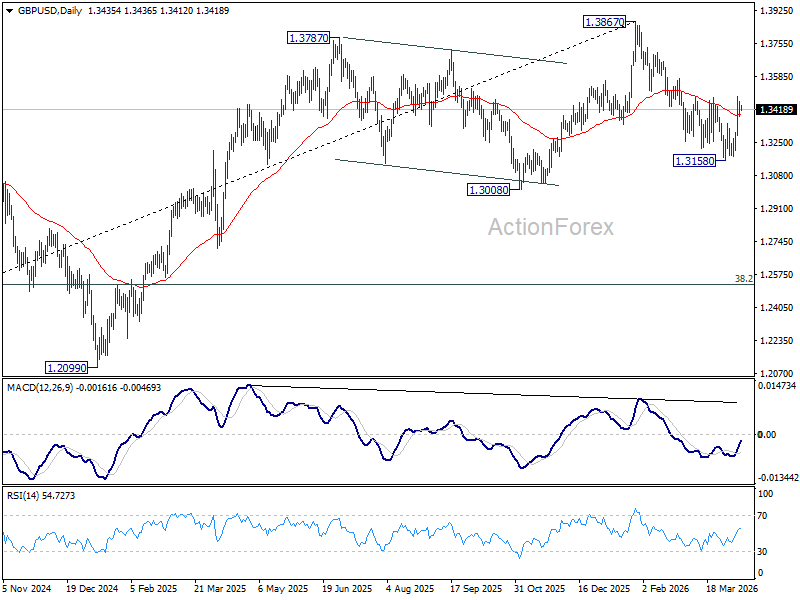

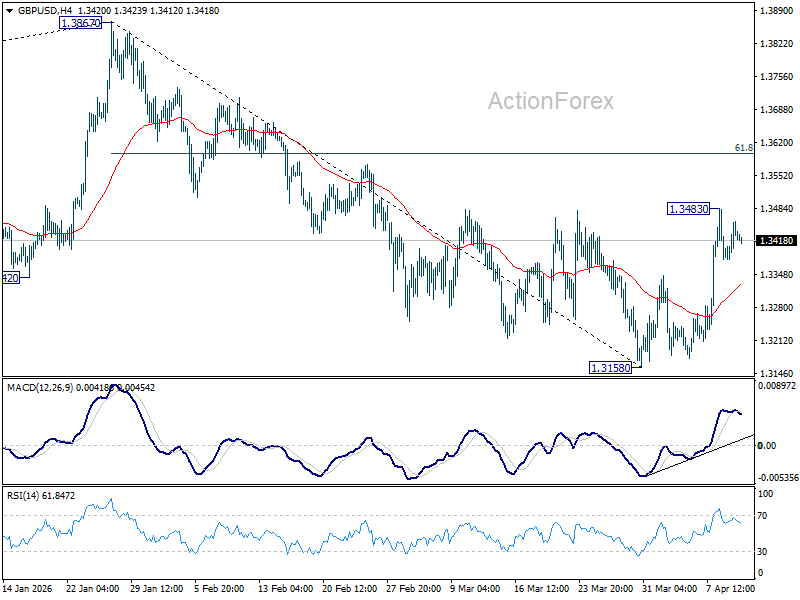

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3392; (P) 1.3425; (R1) 1.3470; More...

Consolidations continue below 1.3483 temporary top and intraday bias in GBP/USD remains neutral. Fall from 1.3867 could have completed as a correction at 1.3158 already. Above 1.3483 will target 61.8% retracement of 1.3867 to 1.3158 at 1.3596. Firm break there will bring retest of 1.3867 high. Nevertheless, sustained break of 55 4H EMA (now at 1.3328) will dampen this bullish view and bring retest of 1.3158 instead.

In the bigger picture, current development suggests that price actions from 1.3867 are merely a corrective pattern within the broader up trend from 1.0351 (2022 low). With 1.3008 support intact, medium term bullishness is maintained and break of 1.3867 is back in favor for a later stage, towards 1.4248 key resistance (2021 high).