Sample Category Title

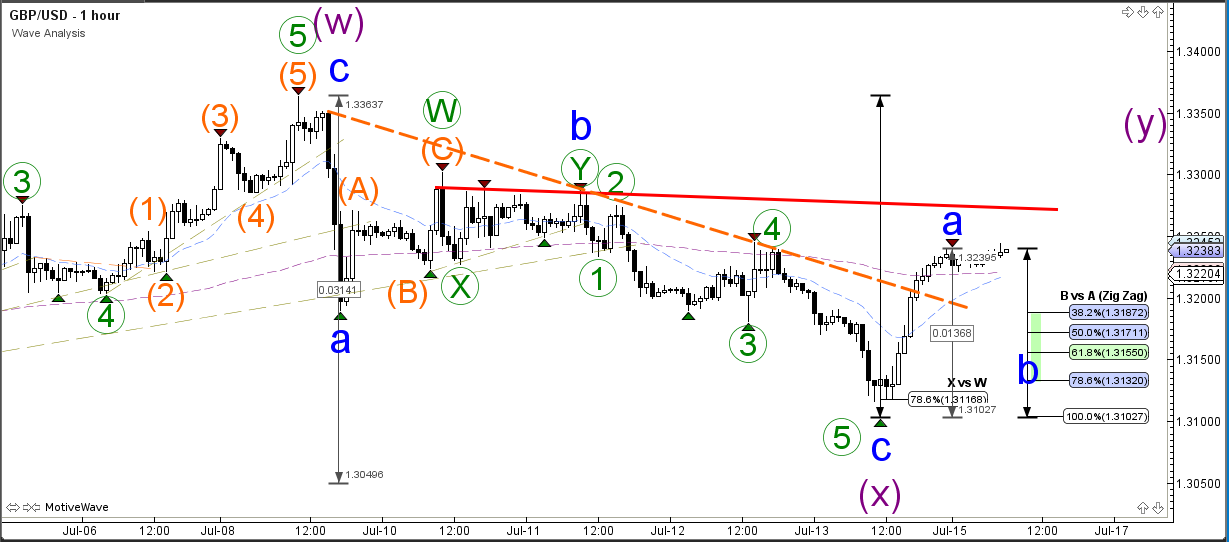

GBP/USD Bullish Reversal At 78.6% Fib After H&S Pattern

The GBP/USD made a strong bullish bounce at the 78.6% Fibonacci level of wave X vs W, which was also an inverted head and shoulders reversal pattern (purple boxes). The bullish momentum seems to be confirming a larger bullish correction within wave 2 (pink) via a WXY (purple) pattern. The break of the downtrend channel could confirm this wave pattern whereas a break below the Fib level could indicate a continuation of the downtrend.

The GBP/USD seems to have completed 5 bearish waves (green) within a wave C (blue) at the 78.6% Fib. The bullish bounce is showing strong bullish momentum and is most likely a bullish wave A (blue) of a larger ABC pattern.

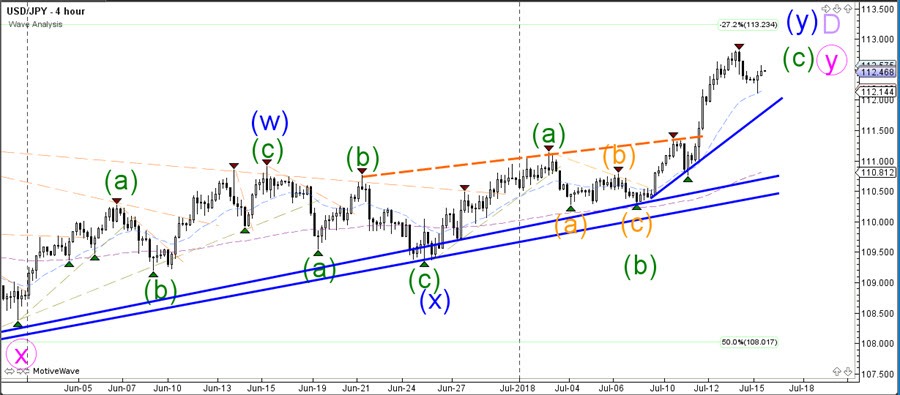

USD/JPY Bounces At 38.2% Fib And Starts Bullish Wave 5

The USD/JPY bullish momentum is moving higher and is approaching the -27.2% Fibonacci target at 113.23. One more bullish push towards the Fib target is expected.

The USD/JPY uptrend is expected to complete wave D (purple) of a potential triangle pattern on the daily chart. A bearish turn at the Fib target could confirm a new wave E swing as long as price stays below 118.60, which is the invalidation level of the potential contacting triangle on the daily chart.

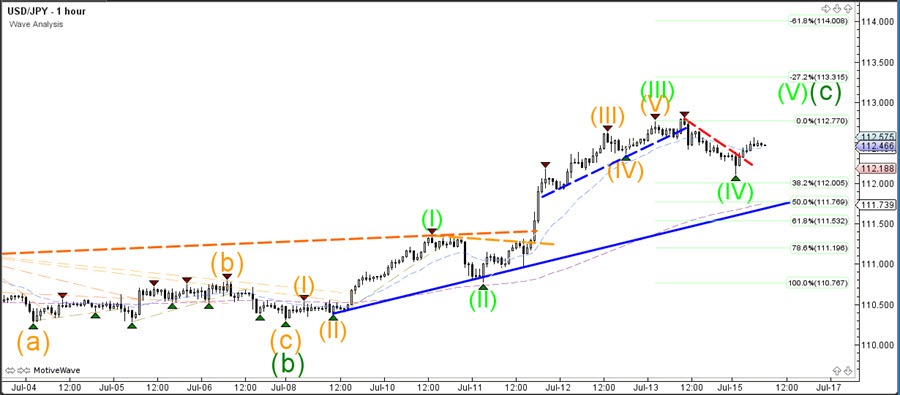

The USD/JPY broke the support trend line (dotted blue) which confirmed the end of wave 3 (green). The bearish pullback seems to be a wave 4 (green) because price bounced at a shallow 38.2% Fibonacci level and broke above the resistance trend line (dotted red), which signals a potential bullish breakout within wave 5 (green). The -27.2 and -61.8% Fibs are potential targets.

EUR And GBP Moderately So While JPY And USD Are Among The Currencies Least Exposed

Market movers today

The release of US Empire manufacturing and retail sales are the two most interesting things on today's calendar.

The week is overall rather quiet, but a few highlights include Fed Chair Powell's testimony tomorrow, the UK jobs report also due out tomorrow and UK inflation on Wednesday. In terms of events, US President Trump is meeting the Russian President Putin later this week.

Selected market news

A number of key data points for the Chinese economy were published overnight. Retail sales grew 9.0% y/y in June's slightly higher-than-consensus expectation, industrial production expanded 6.0% y/y in June, disappointing consensus, while fixed investments rose 6.0% y/y in June in line with the expectation. Overall, the Chinese economy expanded 1.8% q/q and 6.7% y/y in Q2, about as expected by consensus. This is a bit lower than the growth observed over recent quarters.

The oil market managed to recover some of the lost ground towards the end of last week, with the price on Brent crude creeping back above USD75/bbl. The oil market is likely to have found some comfort in the unchanged US oil rig count, which has not increased for a couple of months now. On the other hand, the market will stay on its toes following speculation that the US will tap into its strategic petroleum reserves.

This morning, we have published our FX forecast revisions. Overall, we have made few changes this month with the most noteworthy changes being higher near-term profiles for EUR/SEK and USD/JPY.

Tit-for-tat trade disputes and the risk of an escalating trade war are likely to stay as a market theme at least until the US mid-term elections in November. This morning, we published FX Strategy – FX ripple effects of global trade war, in which we have developed a framework for how to analyse the impact on FX markets of a wider ranging trade war. In short, our score card approach indicates that the Scandies and CHF are particularly exposed, EUR and GBP moderately so while JPY and USD are among the currencies least exposed. Specifically for the NOK, however, we will have to see a significant escalation in the conflict before Norges Bank postpones its first rate hike in September. That said, in the near term, the global risk environment and ‘summer trading' should help keep EUR/NOK in a range.

S. Korea Worried About Trade War Impact

General Trend:

- Asian equity markets trade generally lower, Nikkei 225 closed for holiday

- Chinese equities markets decline

- Xiaomi declines over 9%, Chinese exchanges said mainland investors will not be able to invest in HK companies with super-voting shares

- China Q2 GDP in line, June industrial production slows more than expected, fixed asset investment growth slows to multi-year low

- Yuan (CNY) trades near 11-month low

- New Zealand June Performance of Services index hits lowest level since Dec 2012

- New Zealand Q2 CPI data due for release on Tuesday, along with the Reserve Bank of Australia’s policy meeting minutes

- Fed Chairman Powell is due to testify before Congress on July 17-18th (Tues-Wed)

- Farnborough International Airshow to be held July 16-22nd

- Russian President Putin and US President Trump to meet in Finland Monday starting 06:00 ET

Headlines/Economic Data

Japan

- Nikkei 225 closed for holiday

- (JP) Japan FY17/18 listed company dividend payments ¥13.58T, +13% y/y (fresh record high); payout ratio 30.4%, -4% y/y (lagging other parts of the world) - Nikkei

- (CN) China to impose anti-dumping deposit measures on rubber from South Korea and Japan, effective today; To collect deposits from 12-37.3% on some rubber imports from South Korea and 18.1-56.4% on some rubber products from Japan

Korea

- Kospi opened +0.1%

- (KR) US President Trump: "There hasn’t been a missile or rocket fired in 9 months in North Korea, there have been no nuclear tests and we got back our hostages. Who knows how it will all turn out in the end, but why isn’t the Fake News talking about these wonderful facts? Because it is FAKE NEWS!" - tweet

- (KR) Bank of Korea Gov Lee and Fin Min Kim agree to closely monitor markets and take preemptive measures against risk factors

- (KR) South Korea Jun Foreign Buyers of Korean Bonds: 6.4% v 6.3% prior; Foreign Buyers of Korean Stocks: 31.9% v 31.9% prior

- (KR) Bank of Korea (BoK) Gov Lee: Domestic economy continued sold growth path; To discuss H2 risks to the economy with South Korea Fin Min Kim

- (KR) Bank of Korea Gov Lee and Fin Min Kim agree to closely monitor markets

- (KR) South Korea Fin Min Kim: Minimum wage increase may have a negative impact

- (KR) South Korea sells KRW1.65T v KRW1.65T indicated in 10-yr Govt bonds at 2.555%

China/Hong Kong

- Hang Seng opened +0.2%, Shanghai Composite -0.1%

- Hang Seng Property/Construction index -1.1%, Materials -0.9%, Consumer Goods -0.7%, Financials -0.5%: Info Tech +0.4%

- Chinese liquor maker Kweichow Moutai [600519] rises over 1%, Guided H1 profit +40% y/y

- (CN) CHINA Q2 GDP Q/Q: 1.8% V 1.6%E; Y/Y: 6.7% V 6.7%E; YTD: 6.8% V 6.7%E

- (CN) CHINA JUN INDUSTRIAL PRODUCTION Y/Y: 6.0% V 6.5%E; YTD Y/Y: 6.7% V 6.8%E

- (CN) China Jun Retail Sales y/y: 9.0% v 8.8%e; YTD y/y: 9.4% v 9.4%e

- (CN) China Jun Surveyed Jobless Rate: 4.8% v 4.8% prior

- (CN) China Jun Fixed Assets Urban YTD y/y: 6.0% v 6.0%e (multi-year low)

- (CN) CHINA JUNE M2 MONEY SUPPLY Y/Y: 8.0% (record low) V 8.4%E; M1 MONEY SUPPLY Y/Y: 6.6% V 5.9%E (released on July 13th)

- (CN) CHINA JUNE NEW YUAN LOANS (CNY): 1.840T V 1.520TE (released on July 13th)

- (CN) China has started inspections related to local implicit debt - China Securities Journal

- (CN) China investors to be barred from trading in shares of a dozen foreign companies and those with weighted voting rights, in order to protect retail investors using HK stock link from less understood securities - Shanghai Stock Exchange

- (CN) China National Bureau of Stats (NBS): H1 rise lays sound foundation for meeting 2018 target; Prudent monetary policy will help keep CPI steady in H2

- (CN) China PBoC Open Market Operation (OMO): Injects CNY300B in 7-day and 14-day reverse repos v skips prior (1st injection after 5 consecutive skips, highest injection since Feb): Net: CNY300B injects v CNY0B drain prior

- (CN) China PBoC set yuan reference rate at 6.6758 v 6.6727 prior

- (CN) China Premier Li: Reiterates China and EU to uphold multilateralism and free trade

Australia/New Zealand

- ASX 200 opened +0.1%

- ASX 200 Resources index -0.9%, Energy -0.8%, REIT -0.7%, Financials -0.5%; Telecom +1%, Consumer Discretionary +0.5%

- WHC.AU Reports Q4 ROM coal production 5.9Mt v 6.6Mt y/y; saleable coal production 4.7Mt v 5.5Mt y/y [+1.1%]

- (AU) Australia AOFM announces details to this week's debt syndicate: To issue new 2.75% May 2041 bond, pricing guidance is 39.5-44.5bps/primary 10-yr Futures

- SMA.AU Announces agreement with 2WayWorld Technologies for the proposed divestment of Smarttrans China Ecommerce business structure; consideration is equal to A$300K, plus a transaction expense allowance of A$60K [+14%]

North America

- LMT Said to have reached prelim agreement with US Govt for F-35 jets, that under a larger multi-year deal would bring the cost per jet to $80M by 2020 - US press

- (US) Sec of State Pompeo and Treasury Sec Mnuchin are said to have rejected Iran sanction carve outs – FT

- Arconic [ARNC]: Reportedly getting takeover interest from private equity firms; could get a $10B valuation in any deal - press

- GS Expected to name David Solomon as the new CEO as soon as this week - NY Times

Europe

- (EU) US President Trump: "I think the European Union is a foe, what they do to us in trade. Now you wouldn't think of the European Union, but they're a foe." "Russia is a foe in certain respects. China is a foe economically, certainly they are a foe. But that doesn't mean they're bad. It doesn't mean anything. It means that they are competitive. They want to do well and we want to do well." - CBS interview

- (EU) EU President Tusk: Trade wars can lead to hot wars, Europe seeking support for thorough reform to WTO; EU, Russia, US and China have duty to uphold order - visiting China

- (ES) Fitch affirms Spain sovereign rating at A-; outlook Stable (from July 13th)

- (IT) Canadian ratings agency DBRS affirms Italy sovereign rating at BBB (high), Stable trend (from July 13th)

- (NO) Union adds 900 workers to ongoing strike related to oil and gas workers in Norway, no agreement was reached by deadline - financial press

- (UK) Tory MP Greening said to call for 2nd UK referendum - UK Press

- (UK) Jul Rightmove House Prices m/m: 0.1% v 0.4% prior; y/y: 1.4% v 1.7% prior

- RR.UK Planning to offer maintenance credits to airlines that were impacted by 787 groundings - press

- (EU) EU Commission President Juncker: China knows how to open up, can do so if it wishes - visiting China

- (RU) Kremlin Spokesperson: Hope that Putin/Trump summit will be some sort of step away from current crisis in relations

Levels as of 01:30ET

- Hang Seng -0.3%; Shanghai Composite -0.8%; Kospi -0.3%; Nikkei225 closed; ASX 200 -0.5%

- Equity Futures: S&P500 +0.0%; Nasdaq100 +0.1%, Dax +0.1%; FTSE100 -0.2%

- EUR 1.1613-1.1695; JPY 1112.21-112.56; AUD 0.7409-0.7436;NZD 0.6758-0.6777

- Aug Gold +0.3% at $1,244/oz; Sept Crude Oil -0.7% at $69.44/brl; Sept Copper +0.1% at $2.78/lb

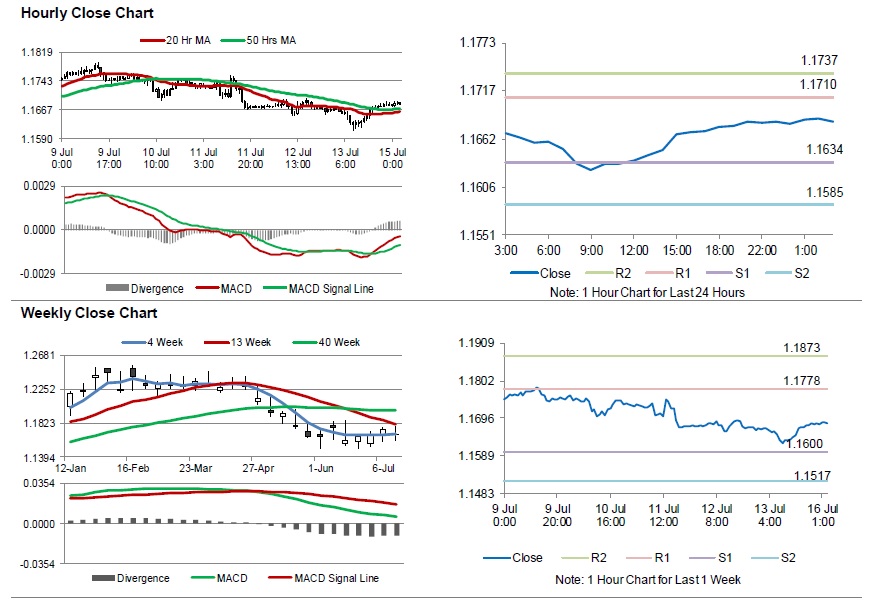

Euro Trading Flat In The Asian Session

For the 24 hours to 23:00 GMT, the EUR rose 0.17% against the USD and closed at 1.1682 on Friday.

In the US, data showed that the US preliminary Reuters/Michigan consumer sentiment index eased to a level of 97.1 in July, amid concerns over the impact of recent tariffs on the economy. Markets had expected the index to drop to a level of 98.0. In the prior month, the index had recorded a level of 98.2.

The Federal Reserve, in its semi-annual Monetary Policy Report, indicated that the US economic activity increased “at a solid pace” over the first half of this year and reiterated the central bank’s expectations for gradual rate hikes. However, the report highlighted concerns over domestic and global risks from trade tensions and increasing oil prices.

In the Asian session, at GMT0300, the pair is trading at 1.1682, with the EUR trading flat against the USD from Friday’s close.

The pair is expected to find support at 1.1634, and a fall through could take it to the next support level of 1.1585. The pair is expected to find its first resistance at 1.1710, and a rise through could take it to the next resistance level of 1.1737.

Moving ahead, investors would await the Euro-zone’s trade balance data for May, due to be released in a few hours. Also, the US advance retail sales for June and the NY Empire State manufacturing index for July, slated to release later in the day, will keep traders on their toes.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

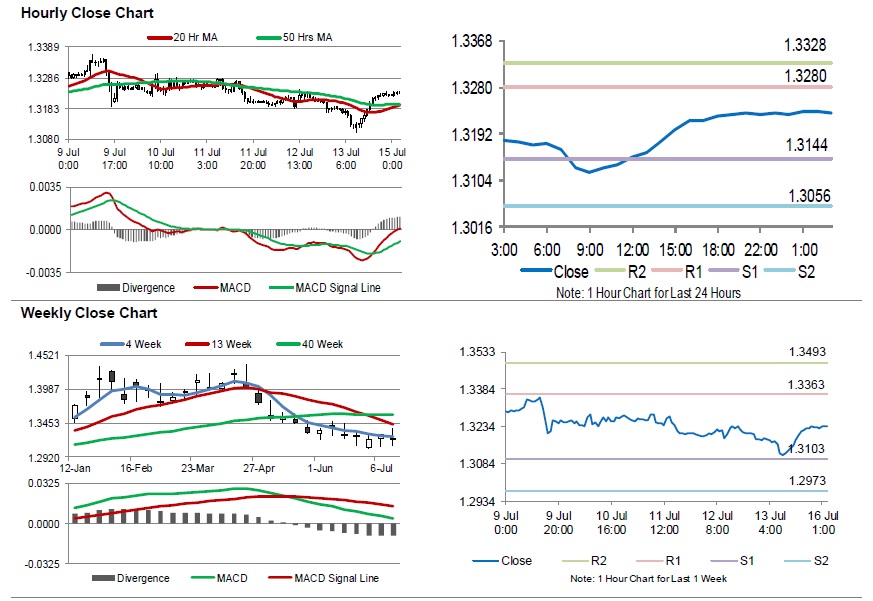

UK’s Rightmove House Price Index Dropped To A 7-Month Low Level In June

For the 24 hours to 23:00 GMT, the GBP rose 0.39% against the USD and closed at 1.3233 on Friday.

In the Asian session, at GMT0300, the pair is trading at 1.3233, with the GBP trading flat against the USD from Friday's close.

On the data front, UK's Rightmove house price index retreated 0.1% on a monthly basis in June, marking its largest drop in 7 months. In the previous month, the Rightmove house price index had recorded a rise of 0.4%.

The pair is expected to find support at 1.3144, and a fall through could take it to the next support level of 1.3056. The pair is expected to find its first resistance at 1.3280, and a rise through could take it to the next resistance level of 1.3328.

Amid lack of economic releases in the UK today, traders would focus on global macroeconomic events for further direction.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

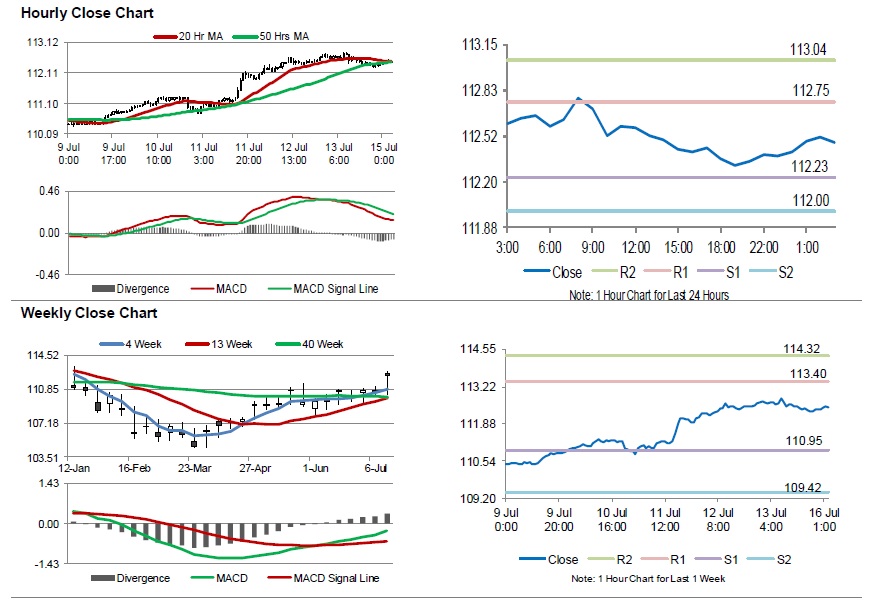

Japanese Yen Reverses Its Gains In The Asian Session

For the 24 hours to 23:00 GMT, the USD declined 0.26% against the JPY and closed at 112.34 on Friday.

In the Asian session, at GMT0300, the pair is trading at 112.47, with the USD trading 0.12% higher against the JPY from Friday’s close.

The pair is expected to find support at 112.23, and a fall through could take it to the next support level of 112.00. The pair is expected to find its first resistance at 112.75, and a rise through could take it to the next resistance level of 113.04.

The currency pair is showing convergence with its 20 Hr and 50 Hr moving averages.

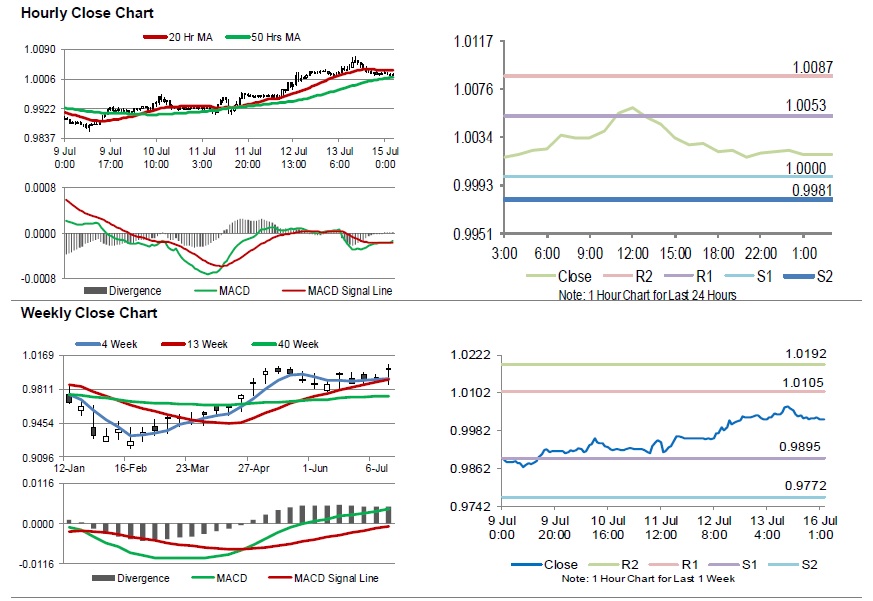

Swiss Franc Is Trading Between Its MA’s

For the 24 hours to 23:00 GMT, the USD declined 0.11% against the CHF and closed at 1.0017 on Friday.

On the data front, Switzerland's producer and import price index rose 3.5% on a yearly basis in June, after registering a gain of 3.2% in the previous month.

In the Asian session, at GMT0300, the pair is trading at 1.0019, with the USD trading slightly higher against the CHF from Friday's close.

The pair is expected to find support at 1.0000, and a fall through could take it to the next support level of 0.9981. The pair is expected to find its first resistance at 1.0053, and a rise through could take it to the next resistance level of 1.0087.

Going forward, traders would keep an eye on Switzerland's total sight deposits, set to release in a while.

The currency pair is trading in between its 20 Hr and 50 Hr moving averages.

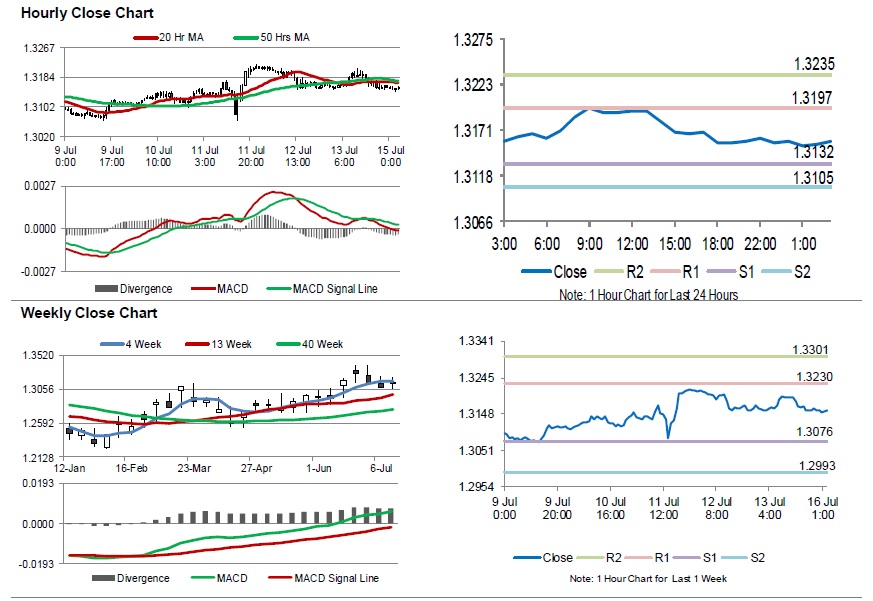

Loonie Trading Flat In The Morning Session

For the 24 hours to 23:00 GMT, the USD declined 0.09% against the CAD and closed at 1.3158 on Friday.

In the Asian session, at GMT0300, the pair is trading at 1.3158, with the USD trading flat against the CAD from Friday's close.

The pair is expected to find support at 1.3132, and a fall through could take it to the next support level of 1.3105. The pair is expected to find its first resistance at 1.3197, and a rise through could take it to the next resistance level of 1.3235.

Looking ahead, investors will closely monitor Canada's existing home sales for June, due to be released later in the day.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

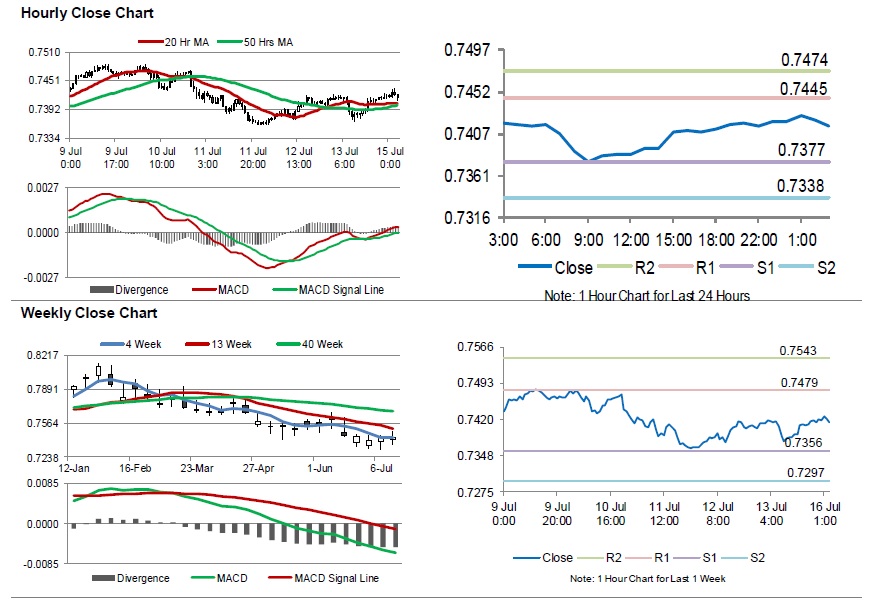

Aussie Trading A Tad Lower In The Asian Session

For the 24 hours to 23:00 GMT, the AUD rose 0.20% against the USD and closed at 0.7418 on Friday.

LME Copper prices declined 0.1% or $2.5/MT to $6166.0/MT. Aluminium prices rose 0.1% or $7.0/MT to $2102.0/MT.

In the Asian session, at GMT0300, the pair is trading at 0.7415, with the AUD trading marginally lower against the USD from Friday’s close.

Overnight data showed that, China’s gross domestic product (GDP) expanded by 6.7% on an annual basis in 2Q 2018, in line with market expectations. In the previous quarter, GDP had registered a rise of 6.8%. Meanwhile, the nation’s retail sales advanced 9.0% on a yearly basis in June, higher than market expectations for an advance of 8.8%. In the previous month, retail sales had registered a rise of 8.5%.

Meanwhile, China’s industrial production climbed of 6.0% on an annual basis in June, rising at its slowest pace in 2-years and undershooting market expectations for a rise of 6.5%. In the previous month, industrial production climbed 6.8%.

The pair is expected to find support at 0.7377, and a fall through could take it to the next support level of 0.7338. The pair is expected to find its first resistance at 0.7445, and a rise through could take it to the next resistance level of 0.7474.

Looking forward, investors would keep an eye on the Reserve Bank of Australia’s (RBA) July meeting minutes, scheduled to release overnight.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.