Sample Category Title

Currencies: Easing Tensions On Italy And Strong US Data Keep Each Other In Balance

Rates: Positive risk sentiment, despite trade developments

Risk sentiment is positive this morning despite the collapsed trade talks between the US and China. A thin eco calendar suggests investors will start looking forward to next week's FOMC meeting. Recent eco data strength lifted odds of 3 more rate hikes this year. The new dot plot might reflect this given the tight call in March and puts a bottom below ST US yields.

Currencies: Easing tensions on Italy and strong US data keep each other in balance

On Friday , EUR/USD failed to regain the 1.1725 area as strong US data supported the dollar. Today, the eco calendar is thin. We see further EUR/USD gains as rather difficult and expect the dollar to be well supported going into next week's FOMC meeting. A new flaring up of trade tensions probably won't help the single currency as well

The Sunrise Headlines

- US markets did good on Friday, responding on the excellent macro-economic numbers that were released (ISM, payrolls). All Asian stock markets are performing well overnight, with Japan outperforming.

- A 3rd round of negotiations between the US and China ended fruitless, raising the odds of a $100bn trade war. Last week, Trump threatened to implement tariffs on Chinese industrial exports, which Beijing has promised to reciprocate.

- In Slovenia, Janez Jansa's Slovenian Democratic Party won the elections with 25% of the vote. However, the anti-immigration party, currently in the opposition, is probably short of coalition partners.

- Berlin responded to Macron's wide-ranging proposals on overhauling the single currency area. Rather than an instrument for fighting future financial crises, Merkel sees the EMF as a tool to strengthen budgetary discipline. She strongly excluded any debt relief measures for Italy.

- Moody's is considering a further downgrade of Turkey, following a previous downgrade earlier this year. The current Ba2 rating is at risk due to increasing pressures on the country's balance of payments.

- On Friday, the ISM manufacturing index rose to 58.7, which was higher than the expected 58.2 further indicating Q2 GDP will be strong, following the dip in Q1.

- On today's calendar we find Factory Orders (Apr) in the US. In Europe, PPI MoM/YoY (Apr) are released.

Currencies: Easing Tensions On Italy And Strong US Data Keep Each Other In Balance

EUR/USD rebound slows as US data stay strong

On Friday, EUR/USD neared Thursday's intraday top (1.1720/25 area) as tensions on Italy eased further, but a real test/break failed. Strong US ISM/payrolls gave a small boost to the dollar, but EUR/USD also wasn't able to break a first support area. Improving sentiment on Europe and strong US data kept each other more or less in balance. EUR/USD closed at 1.1659 (from 1.1693). The gain in USD/JPY was bigger as the pair profited from higher core yields and from a positive risk sentiment. USD/JPY finished the day at 109.54 (from 108.82).

Today, Asian equities mostly show decent gains, joining a good close in the US on Friday. Still, there is plenty of noise on next moves in the trade-war saga between the US and its trade partners/allies. USD/JPY is trading little changed (109.65 area). The euro slightly outperforms the euro. EUR/USD is again nearing the 1.17 area.

Today, there are only second tier EMU data. ECB's Nowotny speaks. Any comments on monetary policy will be closely watched as the June 14 ECB meeting is coming close. US orders data probably won't change markets' positive assessment on the economy. The gyrations in the US ‘trade strategy' are a wildcard. At least for now, investors don't anticipate an outright trade war. Last week; EUR/USD bottomed as tensions on Italy eased. A risk-on context favoured the euro (EUR/USD and EUR/JPY) more than the dollar. This repositioning might still go a bit further, but we don't expect a big leap higher of the euro as long as the ECB stays muted on policy normalisation. Concrete intentions of the Italian government remain also unclear. A flaring up in trade tensions might weigh a bit more on the euro than on the dollar. On the other hand, Friday's strong US data should prevent a big USD setback ahead of next week's Fed meeting. EUR/USD rebounded off the 1.1510/50 area, but didn't regain any important level. We're not convinced of a lasting euro rebound yet. 1.1830 is the first resistance ahead of the 1.1996/1.20 area which we consider not easy to break.

On Friday, sterling regained ground against the euro, supported by a decent UK manufacturing PMI. Today, the construction PMI is expected marginally lower. Brexit will also remain in the headlines as the UK should bring some clarity on the issue before the EU summit later this month. We don't see a strong case for further sustained sterling gains. More sideways trading in the 0.87 big figure might be on the cards

EUR/USD: good US eco data and easing EMU tensions keep each other in balance

Sentiment Higher On A Strong US Session Friday

General Trend:

- Asian equity markets generally track Friday’s gains in the US

- US Commerce Sec Ross said to leave China without firm commitments on imports (financial press)

- China widens collateral for medium-term lending facility (MLF) amid recent reports about corporate defaults

- China Q2 GDP growth seen in line with Q1 (Chinese press)

- Aussie rises after better than expected retail sales: Data supported by unusually warm April

- Reserve Bank of Australia (RBA) due to hold policy meeting tomorrow

- The G-7 Heads of State summit is expected to be held on June 8-9th (Friday-Saturday)

- Various airline and aerospace industry execs comment at the IATA’s World Air Transport Summit in Sydney (June 3-5th)

Headlines/Economic Data

Japan

- Nikkei 225 opened +0.9%; closed +1.4%

- Nikkei 225 Futures rolled over into the Sept 2018 contract

- TOPIX Marine Transportation index +2.8%, Iron & Steel +2.3%, Securities +1.9%, Electric Appliances +1.5%

- Japanese megabanks rise over 1%

- Toyota [7203.JP] rises over 3% following positive broker commentary

- Yamazaki Baking [2212.JP] gains over 13% after announcing price increase

- (JP) Japan May Monetary Base y/y: 8.1% v 7.8% prior; End of Period: ¥492.6T v ¥492.9Te

- (JP) Former BoJ Gov Shirakawa: Japan’s growth rate doing reasonably well given its demographic challenges; Correct measurement of inflation has become difficult

- (JP) Nikkei survey of 1.1K Japanese companies finds FY18/19 CAPEX spending to be ¥27.9T, ~16.7% y/y

- (JP) Japan Chief Cabinet Sec Suga: Will maintain policy of sanctions against North Korea; will negotiate hard to get exemption from steel tariffs

- SBI, 8473.JP Expected to begin operations for cryptocurrency exchange as of today - Japanese Press

Korea

- Kospi opened +0.2%

- (KR) Bank of Korea Gov Lee: Monetary policy has limitations, needs to be a harmonious mix of policy

- Hyosung, 004800.KR Officially launched a holding group and four affiliates, to improve transparency in management and corporate governance - Korean press

- (KR) South Korea sells KRW1.6T v KRW1.6T indicated in 5-yr treasury bonds; avg yield 2.49%

China/Hong Kong

- Hang Seng opened +1.1%, Shanghai Composite +0.3%

- Hang Seng Property/Construction index +2.2%, Telecom +1.8%, Info Tech +1.7%, Consumer Goods +1.5%, Financials +1.3%

- Shanghai Composite Property Sub-index rises over 1%

- (CN) 3rd round of trade talks between China and US end without a deal: China comments: two sides have made "concrete progress"; any move by the US to impose punitive tariffs would derail the negotiations

- (CN) China Q2 GDP growth expected 6.7-6.8% - China Daily Commentary

- (CN) Reiterates the recent move by China PBoC to expand MLF collateral was not an overall loosening – China Securities Times (reminder June 1st: China PBoC widens the collateral for Medium Term Lending Facility (MLF); to add qualified credit bonds)

- (CN) China PBoC sets yuan reference rate at 6.4208 v 6.4078 prior

- (CN) China PBoC Open Market Operation (OMO): To inject CNYB in 7 and 28-day reverse repos v CNY80B injected in 7, 14 and 28-day reverse repos prior: Net: injection CNY20B v CNY80B injected prior

- (CN) NDRC: China cuts solar power prices of newly-built station (from June 1st)

- (CN) China banks making a push to set up independent asset management subsidiaries to cope with tighter regulations on wealth management that aim to break implicit guarantees on banking products - SCMP

- (HK) Hong Kong Government: Reiterates prepared to deal with any capital outflows

- (HK) 3-month HIBOR at 1.78% (highest level since 2008)

Australia/New Zealand

- ASX 200 opened +0.4%, closed +0.5%

- ASX 200 REIT index +1.3%, Resources +0.8%, Consumer Discretionary +0.7%, Financials +0.6%; Utilities -1.8%, Telecom -0.7%

- CBA.AU [+2%],Resolves AML/CTF proceedings with Austrac, to pay civil penalty of A$700M (higher than the A$375M expected) with Austrac legal costs totaling A$2.5M

- ANZ.AU Core of ACCC case said to be a recorded video conference between ANZ's treasurer Rick Moscati and investment banks JPMorgan, Deutsche and Citigroup for allegedly striking a criminal cartel - AFR

- (AU) AUSTRALIA Q1 COMPANY OPERATING PROFIT Q/Q: 5.9% V 3.0%E; INVENTORIES Q/Q: 0.7% V 0.0%E

- (AU) AUSTRALIA APR RETAIL SALES M/M: 0.4% V 0.3%E

Other Asia

- (ID) Indonesia May CPI m/m: 0.2% v 0.3%e; y/y: 3.2% v 3.3%e

North America

- IATA: Cuts global airline 2018 profit guidance 12% to $33.8B (prior $38.4B) due to rising costs; Sees passenger air travel 7.0% v 8.1% y/y

- (US) On Saturday at the G7 meeting, 6 countries (ex the US) issued a formal statement which expressed their unanimous concern and disappointment with the US steel and aluminum tariffs – financial press

Europe

- (DE) German Chancellor Merkel: US has withdrawn from multilateral agreements and imposed new tariffs on steel and aluminum imports, including from Europe - Frankfurter Allegemeine

- (US) On Saturday at the G7 meeting, 6 countries (ex the US) issued a formal statement which expressed their unanimous concern and disappointment with the US steel and aluminum tariffs – financial press

- (TR) Moody's placed Turkey Ba2 sovereign rating on review for downgrade (from June 1st)

- Bayer, BAYN.DE Resolves capital increase with subscription rights against cash contributions in the amount of €6.0B to finance the acquisition of Monsanto

- SocGen [GLE.FR]: UniCredit said to be seeking merger with SocGen - FT

Levels as of 02:00ET

- Hang Seng +1.4%; Shanghai Composite +0.5%; Kospi +0.4%

- Equity Futures: S&P500 +0.2%; Nasdaq100 +0.3%, Dax +0.1%; FTSE100 +0.2%

- EUR 1.1696-1.1654; JPY 109.77-109.45; AUD 0.7621-0.7559;NZD 0.7008-0.6977

- Aug Gold -0.3% at $1,295/oz; Jul Crude Oil -0.1% at $65.75/brl; Jul Copper +0.4% at $3.10/lb

Trade War Fears To Dominate Market Moves This Week

Intense G7 meeting

After imposing tariffs on steel and aluminum imports on its closest allies, the U.S. will be facingenormous criticism at the G7 summit on Friday in Quebec or, as the French Finance Minister Bruno Le Maire likes to call it, “G6 plus one.”

“When you're almost 800 Billion Dollars a year down on Trade, you can't lose a Trade War! The U.S. has been ripped off by other countries for years on Trade, time to get smart!” Donald Trump

Whether President Trump is playing a smart strategic game oris seriously considering getting into a trade war remains unknown, but the probability of a full-blown trade war has undoubtedly increased significantly.

The summit is due to take place after the U.S. and China trade negotiations endedon Sunday without any significant progress made. In fact, China warned the U.S. that any move to implement tariffs on Chinese products would ruin the negotiations.

Although markets in Asiaare rallying after the U.S employment report released on Friday showed a robust surge in numbers and new elections were avoided in Italy, thisoptimism will soon disappear if the Trump administration pulls the trigger on the threatened tariffs on $50bn worth of Chinese exports. So, keep a close eye on Trump's Twitter account for updates.

Europe's Politics and data to be in focus

The Euro struggled last week, with Italian and Spanish political turmoil sending the single currency to itslowest levels since July 2017. The compromise reached betweenthe Italian President and the populist coalition prevented further losses as a new election seems to be off the cards for now. This relief was reflected in Italian bonds where 2-year yields fell 200 basis points from Tuesday's high. However, the Euro's recovery may be short-lived if the new Italian government moves ahead with its proposedmassive spending agenda and tax reductions. These actions will not only create conflict with Brussels but will also invite credit rating agencies to cut their debt ratings.

On the data front, the Eurozone Services PMI is likely to confirm that the economy continued to slowdown as it entered Q2. Another round of negative economic releases will lead the ECB to postpone ending QE and thus drag the Euro further. The UK services PMI, Germany's industrial production and factory orders will also be in focus this week.

EUR/USD Is Trading Almost At 1.17 At The Time Of Writing

Market movers today

This week has mainly tier-2 data on the agenda, but despite this, interesting developments lie ahead.

Italian politics will remain in focus, even after the coalition deal being reached last week. Attention will be on any comments on policy priorities, particularly whether we will see a toning down of some of the spending proposals. We should also keep an eye on any news from the rating agencies. On Friday, we held a conference call on the development in Italy, which you can listen to here (duration 20 minutes).

Also, the disappointing developments this weekend on the US-China trade conflict will be closely monitored, on top of the already looming EU-US trade war.

In Denmark, FX reserves data for May are due out at 16:00 CEST.

Selected market news

Despite the political turmoil around the globe, markets are mainly positive this morning. Asian stocks are higher and S&P500 futures are also slight ly up. The US 10-year Treasury yield has moved above 2.9%. EUR/USD is trading almost at 1.17 at the time of writing. Some of the positive mood this morning may stem from the strong US jobs report Friday, which was strong in all direct ions: Jobs growth was higher than expected (223,000 versus 188,000 expected), the unemployment rate dropped to 3.8% from 3.9% and average hourly earnings rose 0.3% m/m (0.2% expected).

The US-China meeting on trade ended without any joint statement, as was the case at the last meeting. Much have happened since then, where it seemed we were headed for a solution at the negotiationtable. China has said it will withdraw from its commitments to buy more US backs if the US implements the proposed tariffs on imported goods from China. The US is now fighting the trade war on several fronts: China, EU, Mexico and Canada. The opposition against US protectionism from other countries is also clear form the G7 finance ministers and central bank governors meeting, which concluded this week But to be fair, it is not only the US against the rest , at the moment it seems more like all against all. The EU has for instance complained to the WT O about China's technology transfer practice (something the US has also criticised China on).

In the UK, the Brexit department's scenario analyses on ‘no deal' Brexit has been leaked to The Sunday Times (paywall) and it is not cheerful reading. In the worst scenario (labelled Armageddon), the Dover port will break down on day 1, leading to too little supply of e.g. food and medicine. We st ill believe the probability of a ‘no deal Brexit ' is limit ed, but the coming weeks are going to be important , as the next EU summit is approaching (28-29 June).

The Financial Times reports the Italian bank UniCredit may want to merge with Societe General (French bank). Italian banks have been in focus for years due to weak profits, bad loans etc.

Euro-Zone’s Manufacturing Sector Activity Posted A 15-Month Low In May

For the 24 hours to 23:00 GMT, the EUR declined 0.38% against the USD and closed at 1.1658 on Friday, following downbeat economic data.

Data showed that Euro-zone's t final manufacturing PMI fell to a level of 55.5 in May, at par with market expectations. The preliminary figures had also indicated a fall to 55.50. The PMI had recording a level of 56.2 in the prior month. Meanwhile, in Germany, the final manufacturing PMI declined to a level of 56.9 in May, hitting a 15-month low, after registering a level of 58.1 in the previous month. Markets had expected the PMI to fall to a level of 56.8. The preliminary figures had recorded a drop to 56.8.

On Friday, the US Dollar climbed against a basket of currencies, following upbeat US jobs data and as trade war fears eased.

In the US, data revealed that unemployment rate unexpectedly slid to a rate of 3.8% in May, touching an 18-year low. In the previous month, unemployment rate had recorded a reading of 3.9%.

Additionally, the nation's average hourly earnings advanced 0.3% on a monthly basis in May, higher than market expectations. In the preceding month, average hourly earnings recorded a rise of 0.1%.

Further, the US non-farm payrolls increased to a level of 223.0K in May, exceeding market anticipations of an advance to a level of 190.0K. Non-farm payrolls had recorded a revised increase of 159.0K in the prior month.

On the data front, the US final Markit manufacturing PMI dropped surprisingly to a level of 56.4, compared to a level of 56.5 in the prior month. Markets were expecting PMI to climb to 56.6.

In the Asian session, at GMT0300, the pair is trading at 1.1687, with the EUR trading 0.25% higher against the USD from Friday's close.

The pair is expected to find support at 1.1630, and a fall through could take it to the next support level of 1.1573. The pair is expected to find its first resistance at 1.1731, and a rise through could take it to the next resistance level of 1.1775.

Looking forward, investors would look forward Euro-zone's Sentix investor confidence index for June and the producer price index for May, set to release in few hours. Also, the US durable goods orders for April, scheduled to release later in the day, will be on investors radar.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

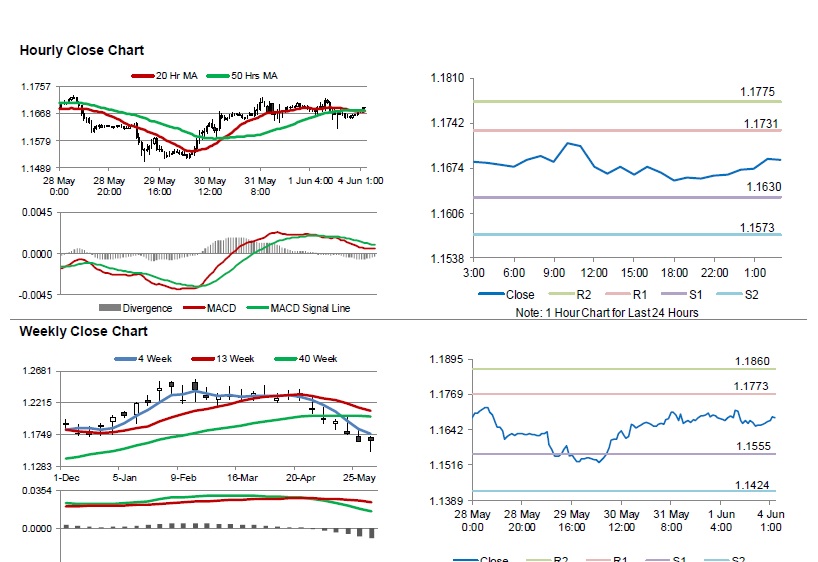

Britain’s Manufacturing PMI Unexpectedly Climbed In May

For the 24 hours to 23:00 GMT, the GBP rose 0.39% against the USD and closed at 1.3349 on Friday.

In economic news, UK's Markit manufacturing PMI sector unexpectedly rose to a level of 54.4 in May. Markets had anticipated the index to drop to a level of 53.5. In the prior month, the PMI registered a reading of 53.9.

In the Asian session, at GMT0300, the pair is trading at 1.337, with the GBP trading 0.16% higher against the USD from Friday's close.

The pair is expected to find support at 1.3290, and a fall through could take it to the next support level of 1.3211. The pair is expected to find its first resistance at 1.3413, and a rise through could take it to the next resistance level of 1.3457.

Trading trend in the Pound today is expected to be determined by UK's construction PMI data for May, scheduled to release in a while.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

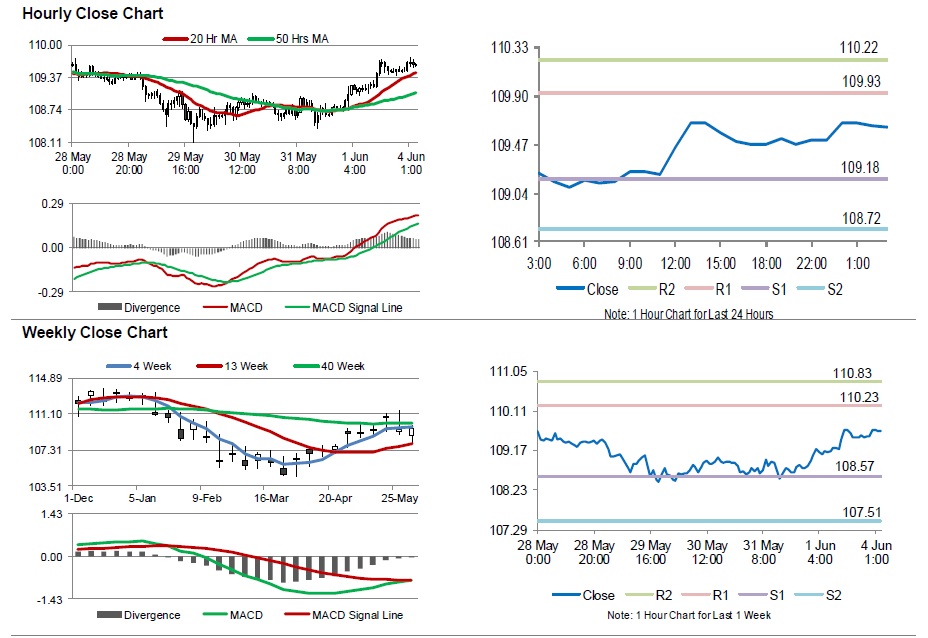

Japanese Yen Extends Its Losses In The Asian Session

For the 24 hours to 23:00 GMT, the USD rose 0.67% against the JPY and closed at 109.48 on Friday.

In the Asian session, at GMT0300, the pair is trading at 109.63, with the USD trading 0.14% higher against the JPY from Friday’s close.

The pair is expected to find support at 109.18, and a fall through could take it to the next support level of 108.72. The pair is expected to find its first resistance at 109.93, and a rise through could take it to the next resistance level of 110.22.

Moving forward, traders would focus on Japan’s Nikkei services PMI for May, slated to release overnight.

The currency pair is trading above its 20 Hr and 50 Hr moving average.

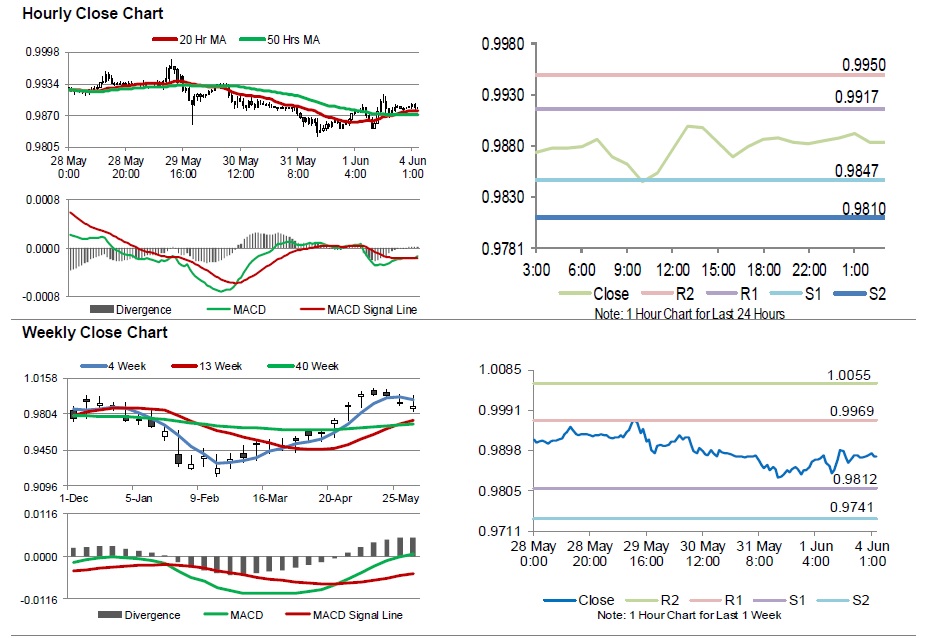

Switzerland’s Manufacturing Sector Activity Slowed In May

For the 24 hours to 23:00 GMT, the USD rose 0.41% against the CHF and closed at 0.9883 on Friday.

On the macroeconomic data front, Switzerland's manufacturing PMI fell to a level of 62.4 in May, lower than market expectations of a drop to a level of 62.5. The PMI had registered a level of 63.6 in the previous month.

In the Asian session, at GMT0300, the pair is trading at 0.9884, with the USD trading marginally higher against the CHF from Friday's close.

The pair is expected to find support at 0.9847, and a fall through could take it to the next support level of 0.9810. The pair is expected to find its first resistance at 0.9917, and a rise through could take it to the next resistance level of 0.9950.

Moving ahead, investors would eye Switzerland's total sights deposits for June, set to release in few hours.

The currency pair is showing convergence with its 20 Hr moving average and trading above its 50 Hr moving averages.

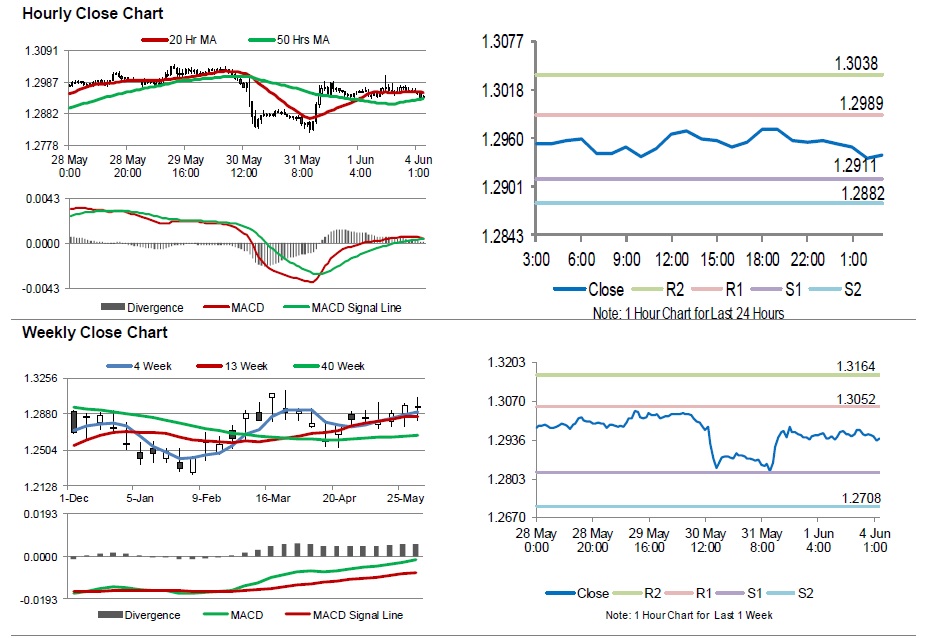

Loonie Trading Higher In The Morning Session

For the 24 hours to 23:00 GMT, the USD rose 0.10% against the CAD and closed at 1.2958 on Friday.

Data indicated that Canada’s manufacturing PMI climbed to 56.2 in May. The manufacturing PMI had recorded a level of 55.50 in the previous month.

In the Asian session, at GMT0300, the pair is trading at 1.2941, with the USD trading 0.13% lower against the CAD from Friday’s close.

The pair is expected to find support at 1.2911, and a fall through could take it to the next support level of 1.2882. The pair is expected to find its first resistance at 1.2989, and a rise through could take it to the next resistance level of 1.3038.

Amid no major economic releases in Canada today, investor sentiment would be determined by global macroeconomic events.

The currency pair is trading below its 20 Hr moving average and showing convergence with its 50 Hr moving average.

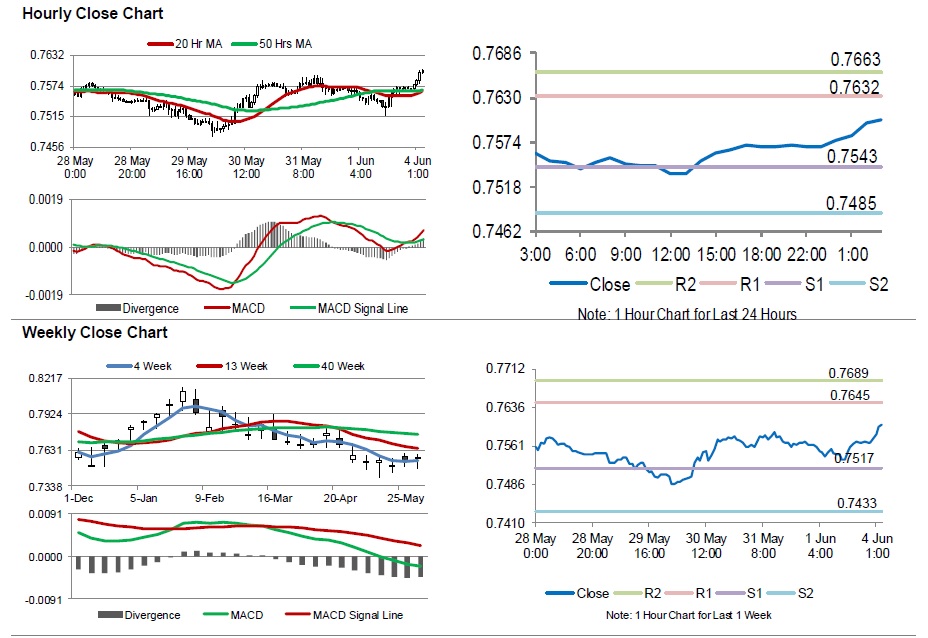

Australia’s Retail Sales Advanced More Than Expected In April

For the 24 hours to 23:00 GMT, the AUD declined slightly against the USD and closed at 0.7570. LME Copper prices declined 0.16% or $11.0/MT to $6814.0/MT. Aluminium prices declined 0.3% or $68.5/MT to $2217.0/MT.

Macroeconomic news indicated that Australia's seasonally adjusted retail sales rose by 0.4% on a monthly basis in April, compared to an unchanged reading in the previous month. Market had envisaged retail sales to rise by 0.3%.

In the Asian session, at GMT0300, the pair is trading at 0.7602, with the AUD trading 0.42% higher against the USD from Friday's close.

The pair is expected to find support at 0.7543, and a fall through could take it to the next support level of 0.7485. The pair is expected to find its first resistance at 0.7632, and a rise through could take it to the next resistance level of 0.7663.

Moving ahead, traders would closely monitor Australia's AiG services PMI for May, scheduled to release overnight.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.