Sample Category Title

EUR/USD Upsides Above 1.1750 Remain Limited

Key Highlights

- The Euro started an upside correction and recovered above the 1.1620 resistance against the US Dollar.

- There was a break above a bearish trend line with resistance near 1.1650 on the 4-hours chart of EUR/USD.

- The US Nonfarm Payrolls in May 2018 rose from the last revised reading of 159K to 223K.

- Today in the US, the Factory Orders figure for April 2018 will be released, which is forecasted to decline 0.3% (MoM).

EURUSD Technical Analysis

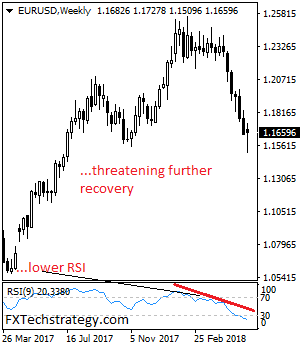

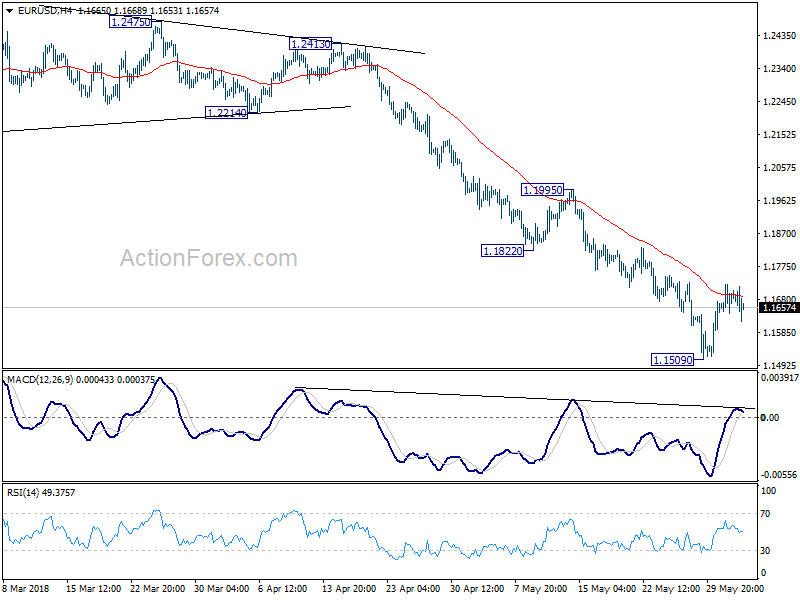

The Euro was under a lot of pressure this past month as it declined below the 1.1550 support against the US Dollar. The EUR/USD pair traded as low as 1.1509 before a fresh recovery was initiated.

Looking at the 4-hours chart, the pair moved above the 1.1600 resistance and the 23.6% Fib retracement level of the last decline from the 1.1993 high to 1.1509 low.

More importantly, there was a break above a bearish trend line with resistance near 1.1650 on the 4-hours chart of EUR/USD. The pair traded towards the 1.1725-50 resistance area where sellers appeared.

There was also an attempt to move above the 38.2% Fib retracement level of the last decline from the 1.1993 high to 1.1509 low. On the upside, there is a crucial barrier near the 1.1750 level and the 100 (red) simple moving average (4-hour).

Therefore, if the pair continues to move higher, it is likely to face hurdles near the 1.1725 and 1.1750 levels. On the downside, the previous broken resistance at 1.1640 and 1.1620 are likely to act as supports.

Recently in the US, the Nonfarm Payrolls report for May 2018 was released by the US Department of Labor. The market was looking for a decline a reading of 188K, more than the last 164K.

However, the actual result was better as the total nonfarm payroll employment increased by 223K in May 2018. The report added:

The unemployment rate edged down to 3.8 percent in May, and the number of unemployed persons declined to 6.1 million. Over the year, the unemployment rate was down by 0.5 percentage point, and the number of unemployed persons declined by 772,000.

The overall outcome was positive and it is likely put a lot of pressure on EUR/USD and GBP/USD in the near term. On the other hand, USD/JPY pair may rise further above 109.50 in the near term.

Economic Releases to Watch Today

- UK's Construction PMI for May 2018 – Forecast 49.7, versus 52.5 previous.

- Euro Zone Sentix Investor Confidence for June 2018 – Forecast 20.8, versus 19.2 previous.

- US Factory Orders April 2018 (MoM) – Forecast -0.3%, versus +1.6% previous.

Chasing One’s Tail

Chasing one's tail

There's a lot less drama to start the week but still plenty of possible noisemakers in play to keep things interesting. Global trade war tensions are on the rise again so on the heels of the latest US administrations salvo of metal import tariffs, the market's focus will be directed at trade war targets, especially CAN MXN and EUR currencies. And of course, US-China trade tensions are but a spark away from reigniting once again.

Tariffs imposed by the US created a blustery G7 finance ministers meeting in Whistler over the weekend with the French finance minister saying that there were just a “few days” left to avoid a trade war. But friend or foe, the US administration is back on the mission to rebalance trade deficits and relations alike.

The US dollar could continue to benefit from a mild repricing in Fed rate hike expectations thanks to strong US employment and ISM data. The market is pricing in just over two hikes +(~2.3) for the rest of 2018 vs 1.5 before the data as we enter the Federal Reserve Board members ” blackout period” ahead of next week June 13 rate hike decision. But G10 currencies will be dotted with more PMI and trade data to digest. Global PMI's have been softening a touch (from high-levels mind you), so traders will be keenly focused on the Eurozone prints as an uptick could provide a bit of tailwind for the EUR.

Italy is stabilising, and with panic hedges all but wholly unwound and rates positioning in the US market much more balanced, traders will likely need some convincing to re-engage after an exhaustingly tricky week in the trading pit. Even more so given the markets usually unpredictable nature before the Federal Reserve Board meeting circus rolls into town.

It's always funny how things evolve in FX trading; it certainly looks like we did little more than chase our tail last week, but closing prices, in this case, paint an incomplete picture.

Regardless, the EUR sits here at 1.1665-75 on top of where it closed the Friday prior. And many other currencies are in the same boat mostly unchanged on the week. The overall market risk is much lighter in FX now, as we try and gain further clarity on the significant issues like trade wars, NK progress, EU inflation bounce, and the continued robust US economic data.

Oil Market

The bulls are starting to wave the white flag as this high-level of uncertainty around supplies going into the June 22 Vienna OPEC summit has kept the oil complex trading defensively. All discussion is centring on if Saudi Arabia and other OPEC members will turn the supply taps up. The market is nervous and thinking OPEC response will be to add more barrels which could intensify the short-term cycle of speculative long liquidation.

But still, OPEC's response may be very conditional on prices heading into the summit so, despite the recent sharp sell-off, this notion could help keep a floor under oil prices ahead of the crucial meeting.

Energy ministers from Saudi Arabia, United Arab Emirates and Kuwait met on Saturday to discuss OPEC circumstance. “They called for sustaining the current partnership to continuously adapt to ongoing market dynamics, in pursuit of the interests of consumers and producers while promoting healthy global economic growth.” The focus on consumer interest suggests that OPEC members want to stay on President Trump's right side after he suggested the cartel is keeping oil prices artificially high. But if OPEC starts increasing production, this is when compliance will be dearly tested as you may see everyone look to ramp up simultaneously. But in the absence of any definitive statement, the markets will continue to debate the June meetings outcome which could increase volatility in the weeks ahead.

US rig counts rose again the week ending Jun 1, but the modest increase will not be a significant driver.

Gold Market

Gold prices are trading lower as trader move to reprice US interest rates higher after solid NFP and SIM data which buoyed the US dollar. Gold prices could come under near-term pressure as the Fed remains on track to raise US interest rates next week. It's very common for gold to trade defensive ahead of a Fed rate hike, but with geopolitical risk premium deflating, these narratives should provide a challenge to golds ambitions this week. The markets will be reluctant, in the absence of geopolitical escalation, to add more topside risk until they get a better read on the Fed forward guidance. Keep in mind the latest run of US economic data has been very solid and has supported the US dollar. And since Gold has been little more than a US dollar trade of late, the stronger USD will continue to provide the most significant near-term headwinds.

Asia Market

Asia markets direction is very much undetermined and remains jaded by trade tensions, but in general, volumes have remained very light and could even dry up further with Summer upon us and a busy World Cup schedule that should keep both local traders and investors glued to their television day and night. While support remains intact, there are few catalysts to trigger a significant bounce higher for regional sentiment.

In Hong Kong markets will come under the glare today following the large rebalances in the MSCI and Hang Seng indices which saw the inclusion of A-shares into the MSCI index.

But in general, local market should remain guarded ahead of a range of Chinese Macro data with the Caixin PMI, FX reserves, trade figures, PPI, CPI due out this week. Markets in Indonesia will re-open following holidays, and PMI figures will be out in Malaysia and Indonesia.

A statement released by Chinese trade officials is making the rounds this morning. While a bit vague and lacking in specifics, the general take way is that of tit for tat. “If the US launches trade sanction measures, including the imposition of tariffs, then all the economic and trade benefits negotiated by both sides are not going to take effect.”

Malaysia Market

After the recent round of policy statements, there is greater clarity on what Malaysia growth driver will be. Much lower public spending is a definite but the negative economic impact should be offset by strong internal and external drivers explicitly relating to private consumption and trade. But given that inflation is running at a tepid pace BNM will hold interest rates level through 2018 on moderating core inflation. However, fiscal deficit expectation will be the wild card. But so far market expectations are not sounding any alarm bells and its expected even the worst case deficit scenarios are not sufficient to signal a rating downgrade.

But with BNM likely to sit idle through 2018 and uncertainty over the fiscal outlook, I'm shifting gears from neutral – slightly bullish Ringgit to neutral over the near term as the currency remains in the dreaded do not trade zone.

As far as domestic markets are concerned, it looks like we're going to have another repeat of the past few weeks with foreign interest sidelined until cleared signals develop.

MYR: Holding pattern suggesting current ranges remain intact.

Currencies

EUR: With calm engulfing Eurozone markets, the Euro could find some relief over the short term but indeed the wear and tear from election crisis, and the waves of populism gripping Europe do point to some longer-term structural issues for the single currency. None the less, short date trends will continue to be driven by near-term growth sentiment. So with the Eurozone inflation spiked towards ECB targets in May. And while policy markets disregard oil price shocks, if this inflation data will support a hawkish case to reduce bond buys over coming months, which should cause the EURUSD to base. Not to suggest Euro bears beware, but worth keeping a lookout.

JPY: Risk trade and US bond yields are driving sentiment.

AUD: The Australian dollar remained entirely off the radar and given just how uninteresting domestic developments are ranges should remain very much intact.

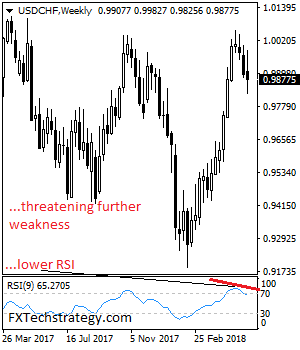

USDCHF – Remains Vulnerable On Pullbacks

USDCHF - The pair looks to weaken further as it closed lower the past week. On the downside, support lies at the 0.9850 level. A turn below here will open the door for more weakness towards the 0.9800 level and then the 0.9750 level. On the upside, resistance resides at the 0.9950 level where a break will clear the way for more strength to occur towards the 1.0000 level. Further out, resistance comes in at the 1.0050 level. Above here if seen will turn attention to 1.0100. All in all, USDCHF faces further corrective downside pressure.

EURUSD – Risk Remains Higher On Correction

EURUSD - The pair faces recovery higher leaving risk higher. On the upside, resistance comes in at 1.1700 level with a cut through here opening the door for more upside towards the 1.1750 level. Further up, resistance lies at the 1.1800 level where a break will expose the 1.1850 level. Conversely, support lies at the 1.1600 level where a violation will aim at the 1.1550 level. A break of here will aim at the 1.1500 level. Below here will open the door for more weakness towards the 1.1450. All in all, EURUSD faces further upside pressure

Eco Data 6/4/18

[php_everywhere instance="1"]

Bulls Added Bets on USD Appreciation

Traders added more bets for higher USD, as suggested in the CFTC Commitments of Traders report in the week ended May 29. Net LENGTH for USD Index (DXY) futures added +1 338 contracts to 3 924. During the week, the DXY index gained +1.3%, as the greenback strengthened against major currencies with the exception of Japanese yen.

NET LENGTH for EUR futures plunged -16 707 contracts to 93 037 for the week, as the increase in short positions (+21 674 contracts) outweighed that in longs (+4 967 contracts). Bets on GBP futures gained on both sides but the bulls got an upper hand, leading to an increase, by +3 776 contracts, of NET LENGTH to 9 477 contracts.

Traditional safe-haven currencies stayed in Net SHORT positions and bearishness exacerbated. Net SHORT for JPY futures soared +5 269 contracts to 8 036 while that for CHF futures rose +6 120 contracts to 43 431. Interestingly, Japanese yen jumped almost +2% against the US dollar, while Swiss franc depreciated modestly against the greenback for the week.

On commodity currencies, NZD futures drifted to NET LENGTH of 1 401 contracts, as the rise in speculative long positions (up +3 868 contracts) tripled that of the shorts (up +1 104 contracts). NET SHORT for AUD futures added +2 123 contracts to 23 235 while that for CAD futures dropped -10 522 contracts to 15 690 for the week. all three currencies depreciated against US dollar during the week.

Traders Reduced Bets for Higher Crude Oil Price

According to the CFTC Commitments of Traders report for the week ended May 29, net LENGTH for crude oil futures fell -25 558 contracts to 607 828. Net LENGTH for heating oil futures added +2 729 contracts to 45 311 while that for gasoline dropped -4 617 contracts to 103 729. Net SHORT for natural gas decreased -639 contracts to 62 186 for the week.

Concerning the precious metal complex, speculators were bullish over gold and silver. Net LENGTH for the gold futures soared +24 173 contracted to 115 130 while that for silver gained +2 228 contracts to 17 453 for the week. For PGMs, net LENGTH for platinum rose +2 554 contracts to 4 016 while that for palladium slipped -722 contracts to 9 993.

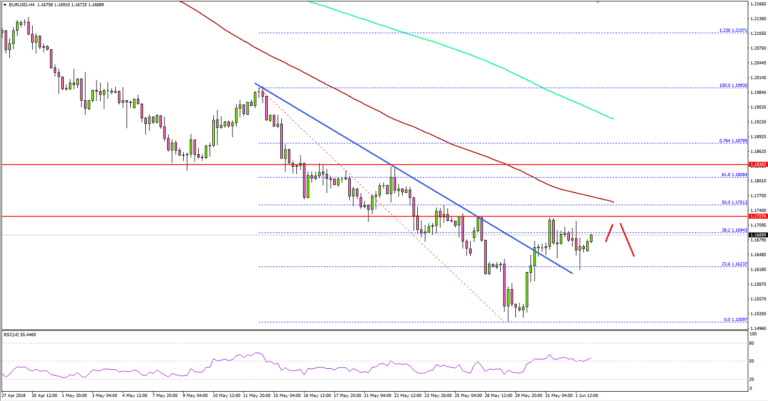

EUR/USD Weekly Outlook

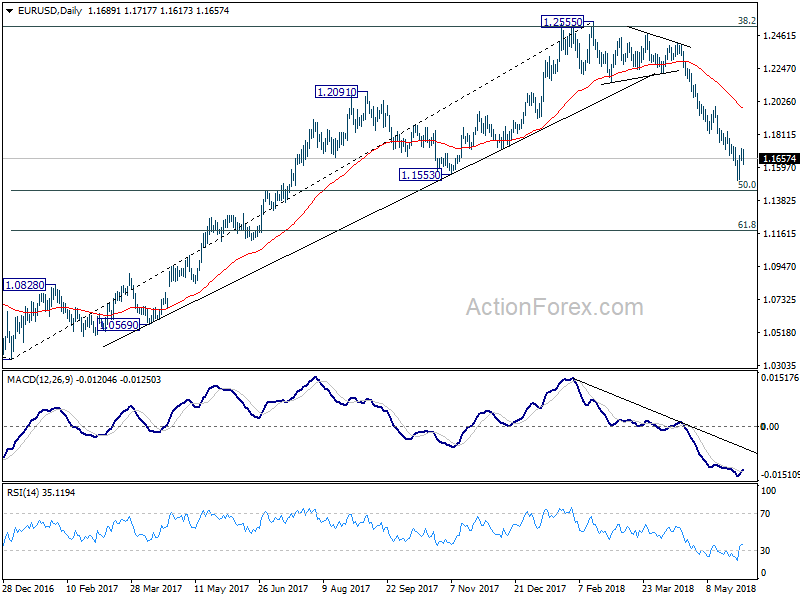

EUR/USD dropped further lower to 1.1509 last week but formed a short term bottom there and rebound. Initial bias is neutral this week for consolidation and stronger recovery cannot be ruled out. But we'd expect strong resistance from 1.1822/1995 resistance zone to limit upside and bring fall resumption eventually. On the downside, break of 1.1509 will resume the decline from 1.2555 and target 50% retracement of 1.0339 to 1.2555 at 1.1447 first. Break will target 61.8% retracement at 1.1186 next.

In the bigger picture, current development suggests that EUR/USD was rejected by 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. And, a medium term top was formed at 1.2555 already. Decline from there should extend further to 61.8% retracement of 1.0339 to 1.2555 at 1.1186 and below. For now, even in case of rebound, we won't consider the fall from 1.2555 as finished as long as 1.1995 resistance holds.

In the long term picture, the rejection from 38.2% retracement of 1.6039 to 1.0339 at 1.2516 argues that long term down trend from 1.6039 (2008 high) might not be over yet. EUR/USD is also held below decade long trend line resistance. Focus will now turn to 1.1553 support. Sustained break there would raise the chance of retesting 1.0339 low. It's early to tell, but the chance of long term bullish reversal is fading.

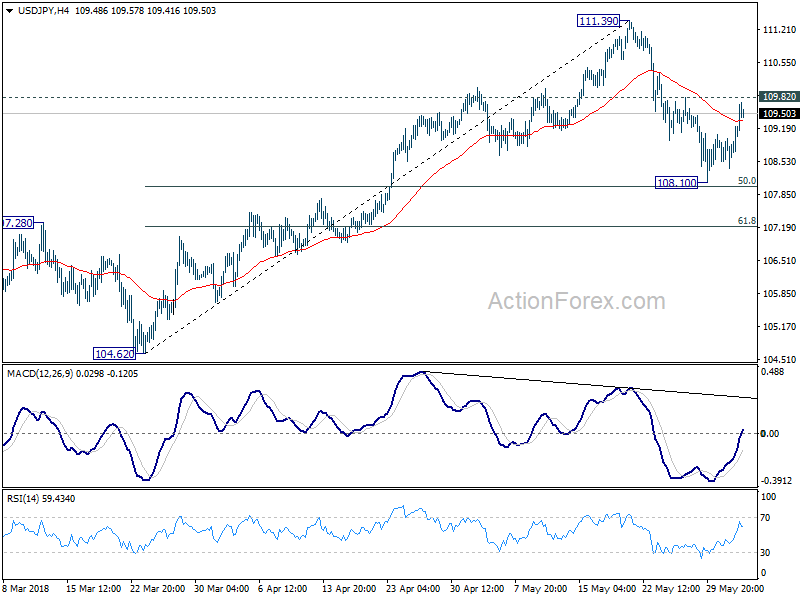

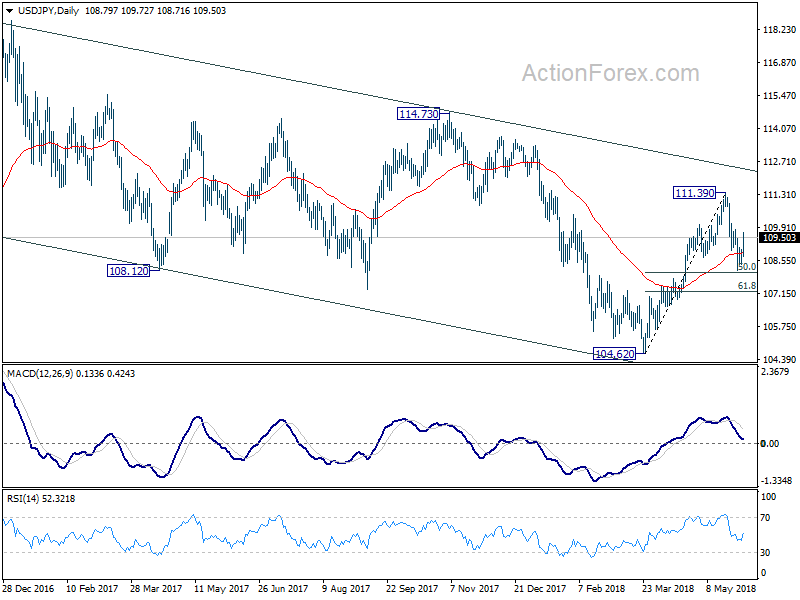

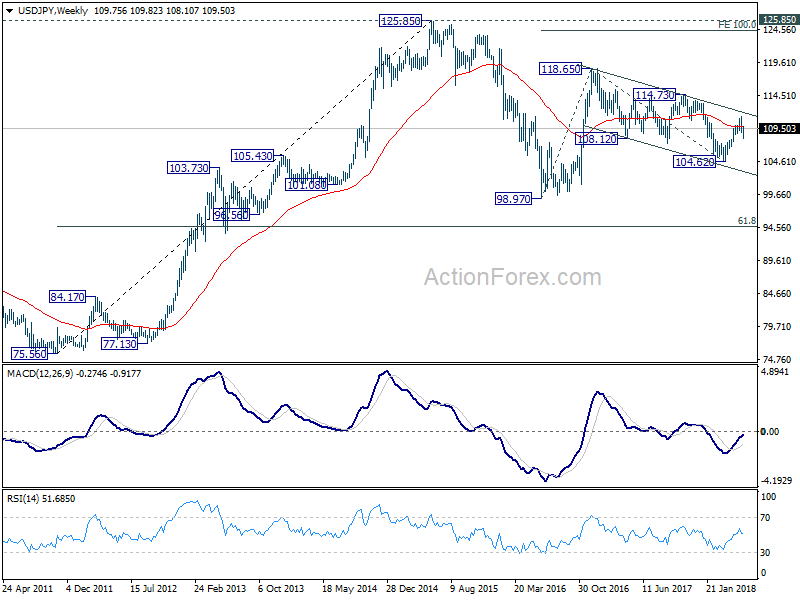

USD/JPY Weekly Outlook

USD/JPY dropped to as low as 108.10 last week but failed to sustain below 55 day EMA and recovered. Initial bias is neutral this week with focus on 109.82 minor resistance. Break there will indicate completion of the pull back from 113.39. And that will revive the bullish case that rise from 104.62 is still in progress. Retest of 111.39 should be seen first. On the downside, though, break of 108.10 will extend the fall from 108.10 to 61.8% retracement of 104.62 to 111.39 at 107.20 instead.

In the bigger picture, at this point w;'re slightly favoring the case that corrective decline from 118.65 (2016 high) has completed with three waves down to 104.62. Above 111.39 will affirm this week and target 114.73 for confirmation. However, it should be noted that USD?JPY is bounded in medium term falling channel from 118.65 (2016 high). Sustained break of 61.8% retracement of 104.62 to 111.39 at 107.20 will likely resume the fall from 118.65 through 104.62 low.

In the long term picture, the rise from 75.56 (2011 low) long term bottom to 125.85 top is viewed as an impulsive move, no change in this view. Price actions from 125.85 are seen as a corrective move which could still extend. In case of deeper fall, downside should be contained by 61.8% retracement of 75.56 to 125.85 at 94.77. Up trend from 75.56 is expected to resume at a later stage for above 135.20/147.68 resistance zone.

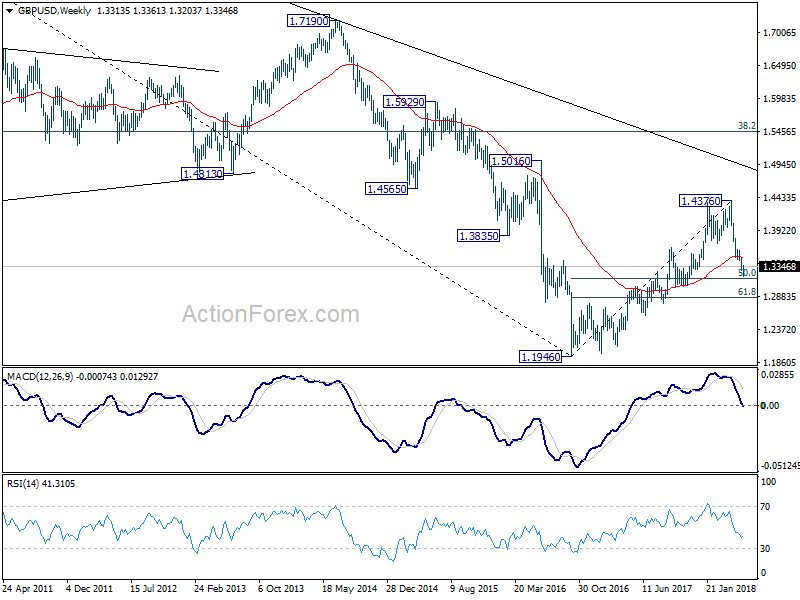

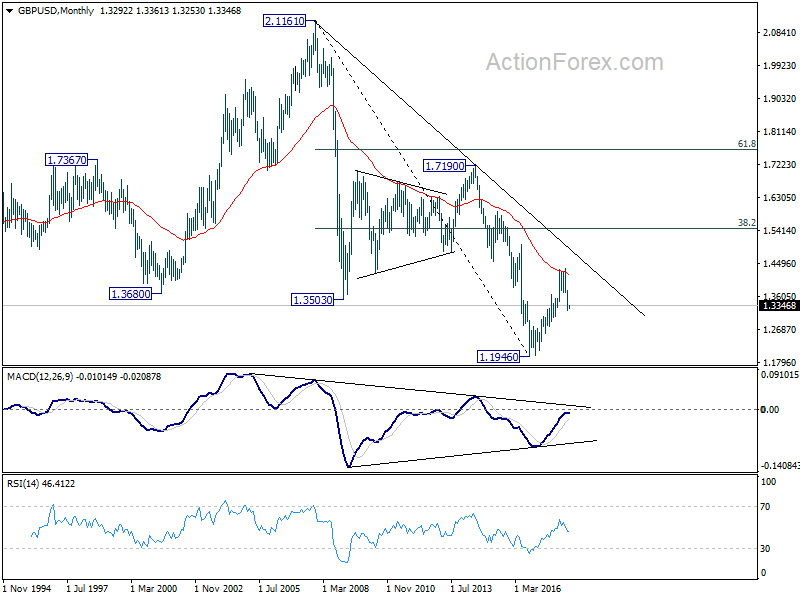

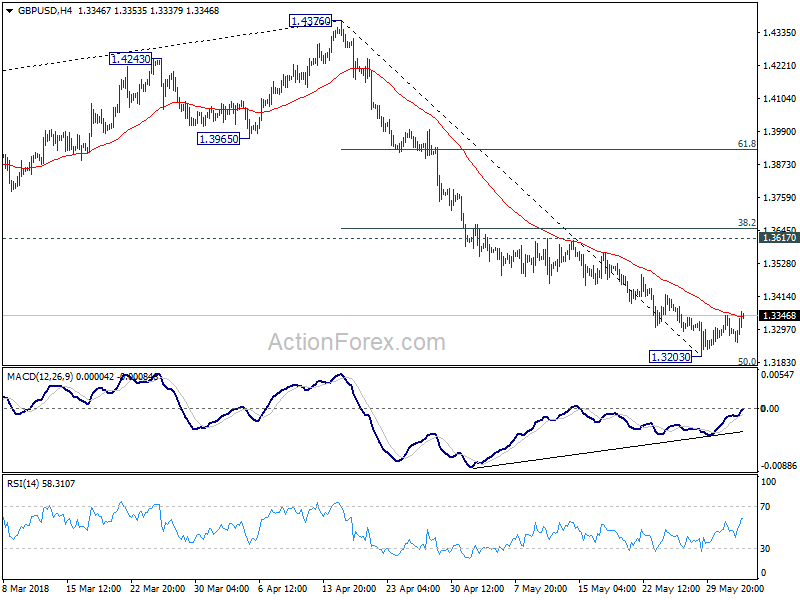

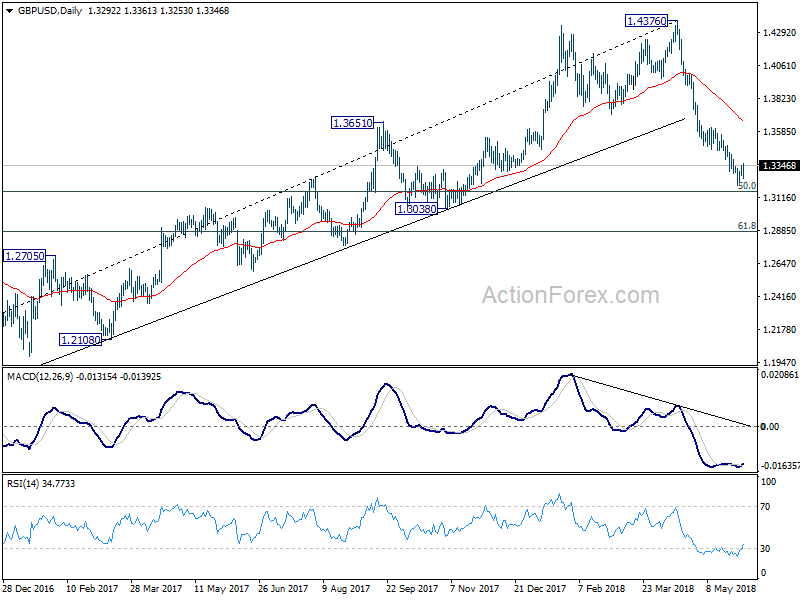

GBP/USD Weekly Outlook

GBP/USD dropped to as low as 1.3203 last week but formed a short term bottom there and recovered. Initial bias remains neutral this week for some more consolidation first. In case of further recovery, upside should be limited by 1.3617 resistance to bring reversal. On the downside, break of 1.3203 will resume the fall from 1.4376 for 50% retracement of 1.1946 to 1.4376 at 1.3161 first, and 61.8% retracement at 1.2875 next.

In the bigger picture, current development suggests that whole medium term rebound from 1.1936 (2016 low) has completed at 1.4376 already, with trend line broken firmly, on bearish divergence condition in daily MACD, after rejection from 55 month EMA (now at 1.4223). 61.8% retracement of 1.1936 (2016 low) to 1.4376 at 1.2874 is the next target. We'll pay attention to the reaction from there to asses the chance of long term down trend resumption. For now, outlook will stay bearish as long as 55 day EMA (now at 1.3670) holds, even in case of strong rebound.

In the longer term picture, rise from 1.1946 (2016 low) is viewed as a corrective move, no change in this view. Rejection from 55 month EMA argues that it might be completed already. Larger down trend from 2.1161 (2007 high) could extend to a new low. This will now be the preferred case as long as 1.4376 resistance holds.