Sample Category Title

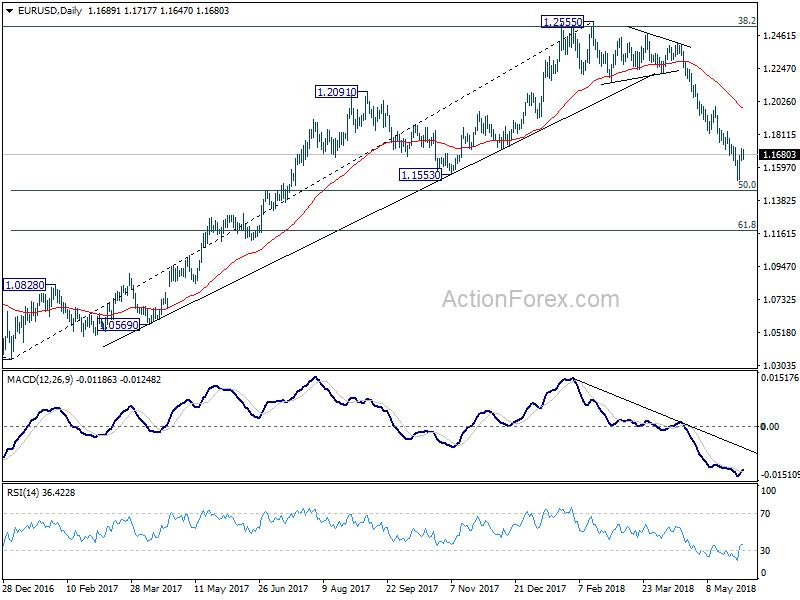

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1648; (P) 1.1686 (R1) 1.1732; More.....

No change in EUR/USD's outlook as consolidation from 1.1509 is extending. Intraday bias remains neutral at this point. Further rise cannot be ruled out. But upside should be limited by 1.1822/1995 resistance zone to bring fall resumption. Below 1.1509 will target 50% retracement of 1.0339 to 1.2555 at 1.1447 first. Break will target 61.8% retracement at 1.1186 next.

In the bigger picture, current development suggests that EUR/USD was rejected by 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. And, a medium term top was formed at 1.2555 already. Decline from there should extend further to 61.8% retracement of 1.0339 to 1.2555 at 1.1186 and below. For now, even in case of rebound, we won't consider the fall from 1.2555 as finished as long as 1.1995 resistance holds.

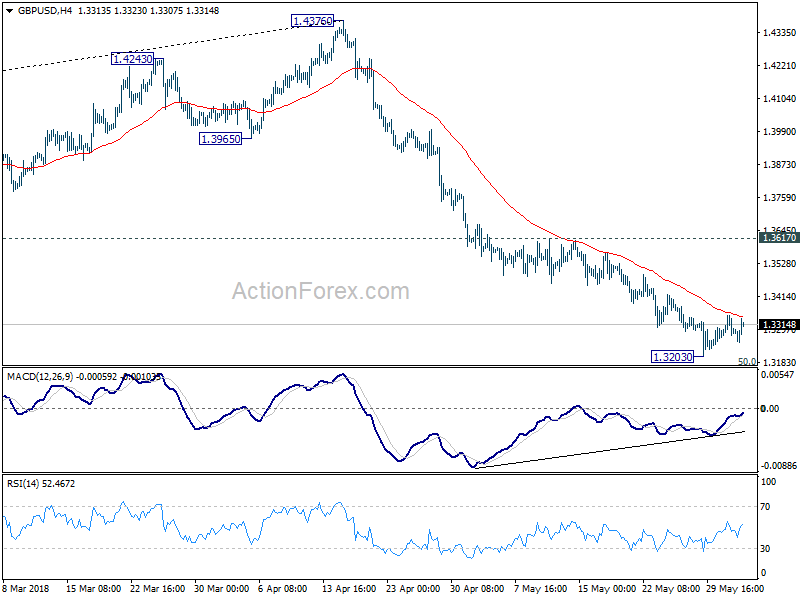

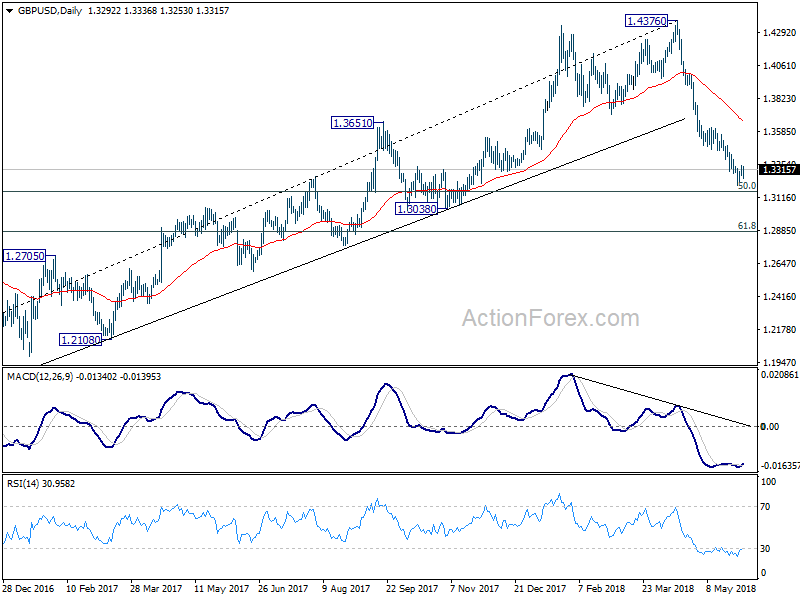

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3265; (P) 1.3306; (R1) 1.3336; More...

No change in GBP/USD's outlook as consolidation from 1.3203 is still in progress. Stronger recovery might be seen. But near term outlook stays bearish with 1.3617 resistance intact. And another fall is expected. Break of 1.3203 will resume the decline from 1.4376 and target 50% retracement of 1.1946 to 1.4376 at 1.3161 first. Break will target 61.8% retracement at 1.2875 next.

In the bigger picture, current development suggests that whole medium term rebound from 1.1936 (2016 low) has completed at 1.4376 already, with trend line broken firmly, on bearish divergence condition in daily MACD, after rejection from 55 month EMA (now at 1.4223). 61.8% retracement of 1.1936 (2016 low) to 1.4376 at 1.2874 is the next target. We'll pay attention to the reaction from there to asses the chance of long term down trend resumption. For now, outlook will stay bearish as long as 55 day EMA (now at 1.3730) holds, even in case of strong rebound.

U.S. Labor Market Heats Up in May

U.S. non-farm payrolls accelerated in May, up a solid 223k, above consensus expectations for a 190k gain. That came after 159k new jobs in April. The past two months were also revised upwards by 15k jobs in total.

Services sector hiring (+171k) was the driving force behind the acceleration, although goods sector hiring also held up relatively well (+47k). Gains across industries were widespread. Retail trade (+31k), health care (+29k), construction (+25k), professional and technical services (+23k), transportation and warehousing (+19k), and manufacturing (+18k) all posted notable gains in May.

Perhaps even more surprising was the unemployment rate falling another tick to 3.8% – the lowest reading in 18 years. The labor force rose by a modest 12k people, and the participation rate fell a tick to 62.7%. That continues the essentially flat trend that has persisted over the past several quarters as retiring babyboomers lean against an increased share of core age (25-54 yrs) people working. Focusing on core age workers, the employment-to-population ratio held steady at 79.2%, but is 0.8 percentage points higher than a year ago. It also remains about one percentage point below its pre-recession peak, suggesting there is still some labor market slack.

Rounding out the good news, wage growth accelerated in May, rising 0.3% on the month. On a year-on-year basis, growth in average hourly earnings picked up to 2.7%.

Key Implications

This was an unambiguously strong report. May's healthy hiring tally in part represents a catch up from some weather-related weakness in recent months. Looking at the six-month trend, hiring has averaged 202k new jobs per month, similar to its 12-month average pace. We do expect monthly payroll tallies to slow in line with a maturing expansion, as the economy runs out of people to pull back into the labor force.

With wage pressures picking up and the unemployment rate falling again, May's employment report confirms that the Fed's bias to raise rates on June 13th. This type of payrolls report would normally lend fodder to the four hikes in 2018 camp if it were not for the trade war cloud that risks raining on the U.S. economy's parade.

May Non-farm Payroll (NFP) by the Numbers

It’s another strong U.S employment report

- US Labor May Nonfarm Payrolls +223K; Consensus +190K

- US May Unemployment Rate 3.8%; Consensus 3.9%

- US May Average Hourly Earnings +0.3%, or +$0.08 to $26.92; Over Year +2.7%

- US May Private Sector Payrolls +218K and Government Payrolls +5K

- US May Average Workweek Unchanged at 34.5 Hours

- US May Labor-Force Participation Rate 62.7%

- US Apr Payrolls Revised to +159K; Mar Revised to +155K

- US Apr Unemployment Unrevised at 3.9%

U.S unemployment rate fell to an 18-year low last month and U.S employers steadily added jobs.

Non-farm payrolls rose a seasonally adjusted +223k in May and the unemployment rate ticked down to +3.8%.

Wages in May improved modestly, growing +2.7% y/y. Revised figures show employers added +159k jobs in April and +155k in March, a net upward revision of +15k.

Digging deeper

Average hourly earnings for all private-sector workers increased +8c last month to $26.92. The +2.7% annual again is small compared to pre-recession readings.

Note: The last time unemployment was near current levels wages rose +4.3% from a year earlier.

Net result, the low unemployment rate and modest wage increases should keep Fed in line to hike rates at a meeting later this month. Consumer inflation has strengthened in recent months to reach the Fed’s +2% annual target.

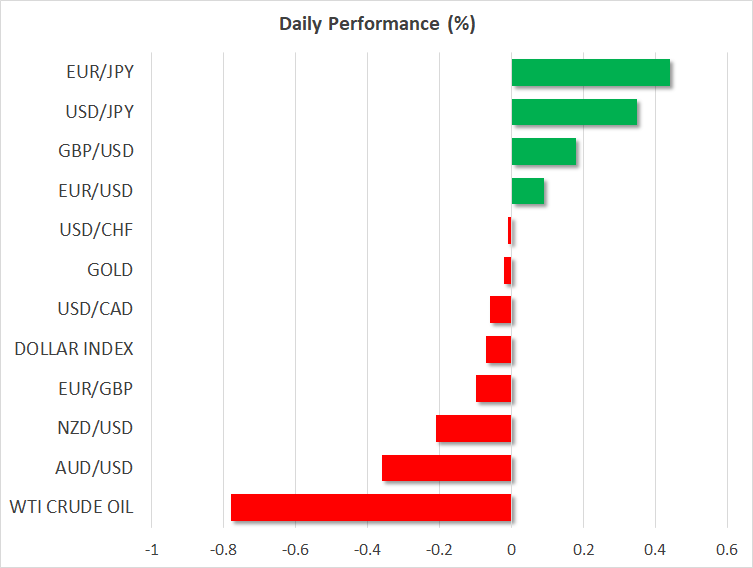

The USD has extended its gains against some G7 currency pairs (€1.1670, C$1.2971, ¥109.60, £1.3317).

U.S 10-year yield trades up at 2.91%.

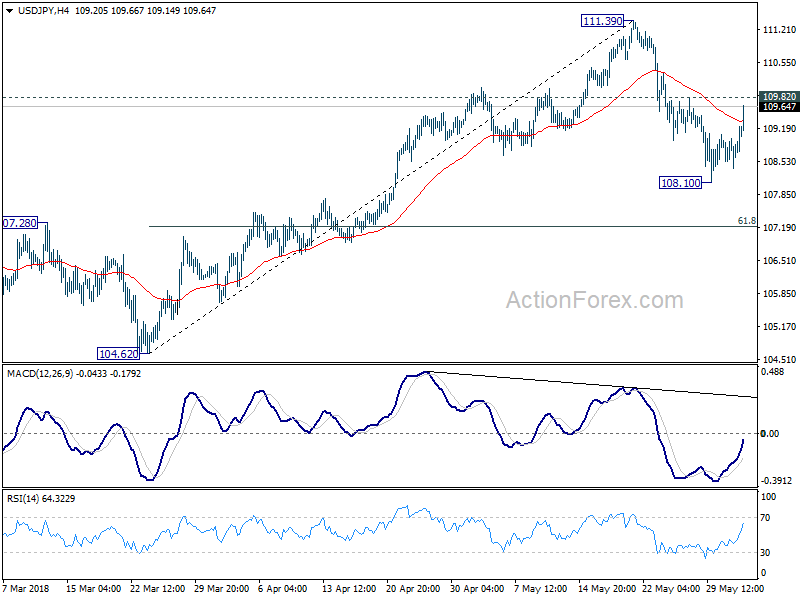

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 108.46; (P) 108.74; (R1) 109.09; More...

USD/JPY's rebound from 108.10 extends higher and focus is now back to 109.82 resistance. Break there will indicate completion of the pull back from 113.39. And that will revive the bullish case that rise from 104.62 is still in progress. On the downside, though, break of 108.10 will extend the fall from 108.10 to 61.8% retracement of 104.62 to 111.39 at 107.20 instead.

In the bigger picture, USD/JPY remains bounded in medium term falling channel from 118.65 (2016 high). Current deeper than expected fall from 111.39 argues that fall from 118.65 is not finished. Break of 104.62 low would target 98.97 or even below. Though, break of 111.39 will revive the case that fall from 118.65 has completed and turn focus to 114.73 for confirmation.

Dollar Jumps on All Round Better than Expected NFP

Dollar surges in early US session after non-farm payroll report beat market expectation on all front. The job market grew 223k in May, above expectation of 190k. Unemployment rate dropped to 3.8%, beat expectation of 3.9%. That's also the lowest level in 18 years. More importantly, wage growth was solid. Average hourly earnings rose 0.3% mom, beat expectation of 0.2% mom. Fed is widely expected to raise interest rate again on June 13 even though market pared back some bets. Today's data will put Fed back on track for another hike in September.

While dollar is strong today, for now, it's overwhelmed by Sterling which was lifted by better than expected PMI manufacturing earlier today. On the other hand, yen is trading as the weakest one as global stock markets shrugged off trade war threats. German-Italian yield spread also narrowed as Italy finally formed a government. Spain's Prime Minister Mariano Rajoy was vote out of office today and Pedro Sánchez will take over. The change is also well received by the markets.

EU Juncker committed to work with new Italian government

A European Commission spokesperson said that they have "full confidence in the capacity and willingness of the new government to engage constructively with its European partners and EU institutions to uphold Italy's central role in the common European project." Also, President Jean-Claude Juncker "is committed to work with the new Italian government to take on the many common challenges that Italy and Europe are facing, from trade to migration and many more." Juncker will meet new Italian Prime Minister Giuseppe Conte next week at a G7 meeting in Canada.

UK PMI manufacturing rose to 54.4, rebound far from convincing

UK PMI manufacturing rose to 54.4 in May, up from 53.9 and beat expectation of 53.5. Markit noted in the release that output growth ticks higher despite slower expansion of new work received. And, supply-chain constraints and cost pressures intensify. Rob Dobson, Director at IHS Markit, noted in the statement that "scratch beneath the surface and the rebound in the PMI from April's 17-month low is far from convincing." In particular, "manufacturers have yet to fully adjust their production to the weakening trend in new business growth". Also "manufacturers will also likely be constrained if the resurgence in both cost inflation and supply-chain pressures becomes more firmly embedded."

Eurozone PMI manufacturing finalized at 55.5, 15-month low

Eurozone PMI manufacturing was finalized at 55.5, unrevised from initial reading. The Netherlands, Germany and Austria remain strongest performing nations despite some deterioration. Netherlands PMI manufacturing, despite hitting an 8-month low, was at 60.3. Austria PMI manufacturing hit 14-month low at 57.3. Germany PMI manufacturing hit 15 month low at 56.9. Chris Williamson, Chief Business Economist at IHS Markit noted in the release that "some of the weakness may have been related to a higher than usual number of holidays during the month, but risks appear tilted towards growth remaining subdued or even cooling further in coming months."

Also released in European session, German PMI manufacturing was revised up by 0.1 to 56.9. France PMI manufacturing was revised down by 0.7 to 54.4. Italy PMI manufacturing dropped to 52.7 in May, down from 53.5. Swiss PMI manufacturing dropped to 62.4 in May, down from 63.6.

China Caixin manufacturing PMI unchanged at 51.1, export situation still disappointing

China Caixin manufacturing PMI was unchanged at 51.1 in May, slight below expectation of 51.2, indicating modest expansion. Dr. Zhengsheng Zhong, Director of Macroeconomic Analysis at CEBM Group noted that "the index for new export orders picked up in May, but remained in contraction territory, reflecting that the export situation was still grim." And, "overall, operating conditions across the manufacturing sector remained stable. The growth in the price of industrial products has gained momentum, however, the export situation was still disappointing."

Also release in Asian session, Japan PMI manufacturing was finalized at 52.8, revised up from 52.5. Japan capital spending rose 3.4% in Q1. New Zealand terms of trade dropped -1.90% qoq in Q1. Australia PMI manufacturing dropped to 57.4 in May, down from 58.3.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 108.46; (P) 108.74; (R1) 109.09; More...

USD/JPY's rebound from 108.10 extends higher and focus is now back to 109.82 resistance. Break there will indicate completion of the pull back from 113.39. And that will revive the bullish case that rise from 104.62 is still in progress. On the downside, though, break of 108.10 will extend the fall from 108.10 to 61.8% retracement of 104.62 to 111.39 at 107.20 instead.

In the bigger picture, USD/JPY remains bounded in medium term falling channel from 118.65 (2016 high). Current deeper than expected fall from 111.39 argues that fall from 118.65 is not finished. Break of 104.62 low would target 98.97 or even below. Though, break of 111.39 will revive the case that fall from 118.65 has completed and turn focus to 114.73 for confirmation.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:30 | AUD | AiG Performance of Manufacturing Index May | 57.5 | 58.3 | ||

| 22:45 | NZD | Terms of Trade Index Q/Q Q1 | -1.90% | -2.00% | 0.80% | 1.50% |

| 23:50 | JPY | Capital Spending Q1 | 3.40% | 3.20% | 4.30% | |

| 00:30 | JPY | PMI Manufacturing May F | 52.8 | 52.5 | 52.5 | |

| 01:45 | CNY | Caixin PMI Manufacturing May | 51.1 | 51.2 | 51.1 | |

| 07:30 | CHF | PMI Manufacturing May | 62.4 | 62.5 | 63.6 | |

| 07:45 | EUR | Italy Manufacturing PMI May | 52.7 | 53 | 53.5 | |

| 07:50 | EUR | France Manufacturing PMI May F | 54.4 | 55.1 | 55.1 | |

| 07:55 | EUR | Germany Manufacturing PMI May F | 56.9 | 56.8 | 56.8 | |

| 08:00 | EUR | Eurozone Manufacturing PMI May F | 55.5 | 55.5 | 55.5 | |

| 08:30 | GBP | PMI Manufacturing May | 54.4 | 53.5 | 53.9 | |

| 12:30 | USD | Change in Non-farm Payrolls May | 223K | 190K | 164K | 159K |

| 12:30 | USD | Unemployment Rate May | 3.80% | 3.90% | 3.90% | |

| 12:30 | USD | Average Hourly Earnings M/M May | 0.30% | 0.20% | 0.10% | |

| 13:30 | CAD | Manufacturing PMI May | 55.5 | |||

| 13:45 | USD | Manufacturing PMI May F | 56.7 | 56.6 | ||

| 14:00 | USD | Construction Spending M/M Apr | 0.80% | -1.70% | ||

| 14:00 | USD | ISM Manufacturing May | 58.1 | 57.3 | ||

| 14:00 | USD | ISM Prices Paid May | 77.9 | 79.3 |

Dollar surges as non-farm payrolls beat expectation on all front

Dollar jumps immediately after an all round solid job report.

Non farm payrolls grew 223k in May, above expectation of 190k.

Unemployment rate dropped to 3.8%, beat expectation of 3.9%. That's also the lowest level in 18 years.

Average hourly earnings rose 0.3% mom, beat expectation of 0.2% mom.

Fed is widely expected to raise interest rate agian on June 13 even though market pared back some bets. Today's data will put Fed back on track for another hike in September.

Dollar Up On Yen Despite Trade Noise, NFP Employment Report The Next Challenge

Here are the latest developments in global markets:

FOREX: The US dollar edged higher by 0.38% on Friday against the Japanese yen and jumped above the 109.00 psychological level ahead of the US employment report for May later in the day. It is the last NFP data before the June Fed meeting. The US dollar index – which tracks the greenback’s performance versus a basket of six major currencies – traded slightly higher by 0.07% at 94.05. Meanwhile, euro/dollar is poised to post its first week of gains after six consecutive negative weekly sessions as worries over Italy’s political crisis ease. The pair today is trading higher by 0.15%. Sterling gained 0.16%, inching up to 1.3328 versus the greenback. UK’s Manufacturing PMI provided support to the pair after the measure rose to 54.4 in May from the previous month’s 17-month low of 53.9, and well above market expectations of 53.5. The Antipodean currencies traded lower with aussie/dollar and kiwi/dollar declining by 0.32% and 0.21% respectively. Dollar/loonie was up by 0.02%.

STOCKS: European equities came under strong buying interest on Friday at 1100 GMT. The UK’s FTSE 100, the German DAX and French CAC 40 were up by 0.67%, 0.94% and 1.23% respectively, paring some of the previous days’ losses. Also, the Italian FTSE MIB, overperformed and was up by a hefty 2.66%, while the Spanish IBEX 35 surged by 2.18%. The pan-European STOXX 600 was up by 0.99%, while the blue-chip Euro STOXX 50 traded higher by 0.98%. Futures on the Dow, S&P 500 and Nasdaq 100, are pointing to a higher open on Wall Street.

COMMODITIES: Oil prices were mixed at 1100 GMT, West Texas Intermediate (WTI) was down by 0.55% at $66.67 per barrel, whereas d Brent crude was up by 0.40% at $77.86 . In precious metals, gold was flat on the day at $1,297.18 per ounce.

Day ahead: Nonfarm payrolls to spell good news for dollar; Trade and political developments eyed

Nonfarm payrolls out of the US at 1230 GMT will be the most important data release in the remainder of the day, giving a last glance on the US labor market before the Fed concludes its two-day monetary policy meeting on June 13. Analysts believe the numbers will underline the strength of the labor market once again, projecting a rise of 183k in nonfarm job positions in May compared to 178k in the previous month and a faster wage growth of 0.2% versus the 0.1% increase in March. The unemployment rate though, is forecast to remain unchanged at 3.9%, at the lowest level reached since 2000. Markit and ISM manufacturing PMIs due at 1345 GMT and 1400 GMT will attract some interest as well. Figures on total vehicles sales will be delivered at 1930 GMT.

Buying positions on the dollar could strengthen if the NFP report beats expectations.– especially on the wage front – as that could boosting confidence in the US economy and chances for at least two more rate hikes this year. But further escalation in trade tensions is likely to cap any major rally in the greenback. Yesterday, the US President fired another salvo in a trade dispute, slapping tariffs on steel and aluminum imports from the EU, Canada, and Mexico. The move came a month after Trump decided to temporarily exempt those allies from tariffs, postponing the imposition until June 1. However, the negotiating teams failed to reach a common ground during that period and the EU, Canada, and Mexico are now set to face import tariffs going into effect today. Yet the story did not end there as Canada, the biggest steel exporter to the US, retaliated immediately, announcing tariffs on $16.6 billion products imported from the US (taking effect in July), while Mexico said it is activating equivalent measures with the US until Washington removes its levies. The EU who has not taken any steps yet, announced it would fight back. Trade relations with China are likely to come to the surface again during the weekend as the US Commerce Secretary, Wilbur Ross, will be in Beijing in an attempt to increase US exports to China.

Meanwhile, in the eurozone, political risks took the back seat on Thursday after the populists parties, the anti-establishment Five-Star Movement and the right-wing League finally agreed to form a new government, avoiding early elections and revising their coalition plans, which were considered as more Euro-friendly. The parties kept the law professor Giuseppe Conte as the next Prime Minister, though they decided to replace Paolo Savona with Giovanni Tria as the new Finance Minister. Note that the Italian President, Sergio Mattarella, rejected Savona on Sunday for taking the position, halting initial coalition attempts. In Spain, political turmoil continues, with the Spanish Prime Minister, Mariano Rajoy resigning from the role after being defeated in a no-confidence vote in Parliament. Pedro Sanchez, a socialist and pro-European, was named early today to fill the position. Conte will be sworn on Friday along with Cabinet Ministers.

Brexit updates will be in focus as well following reports Northern Ireland may be allowed to trade freely with both the EU and the UK under a common regime of customs regulations with those regions. Moreover, the idea includes a ten-mile-wide economic zone on the border with the Republic of Ireland, a measure to avoid checks.

In oil markets, Baker Hughes is scheduled to deliver its report on US oil rigs count at 1700 GMT, while on Saturday the focus will turn to Kuwait, where Saudi Arabia, Kuwait, and the United Arab Emirates will be holding discussions on supply.

As of today’s public appearances, Minneapolis Fed President Neel Kashkari – non-voting FOMC member in 2018 – will be participating in a panel discussion at 1255 GMT, while at 1310 GMT Bank of England Chief Economist Andy Haldane will be giving a lecture.

A G7 meeting between finance ministers and central bankers with a theme “Investing in Growth that Works for Everyone” will gather attention as well. The meeting is scheduled to conclude on June 2.

Canada, Mexico, and Europe no Longer Exempt from Steel and Aluminum Tariffs

Earlier today the U.S. administration announced that it had failed to reach an arrangement with Canada, Mexico, and the EU regarding steel and aluminum imports from these regions. Starting tomorrow, the U.S. will impose a 10% ad valorem (proportional to price) tariff on aluminum imports and a 25% ad valorem tariff on steel imports from these regions.

The U.S. administration announced that arrangements have been reached to limit steel imports from South Korea, Australia, Argentina, and Brazil. Similarly, Australia and Argentina arranged to limit aluminum exports to the U.S. As such, these countries will avoid the tariffs.

Steel and aluminum imports into the U.S. totaled US $52 billion last year, 2.2% of total goods imports, but only about 0.3% of total gross domestic product. In 2017, Canada exported $12.6 billion in steel and aluminum to the U.S., or about 24% of total U.S. imports. Mexico exported $3 billion (5.4%), and the EU $6.5 billion (12.4%).

The amount of trade affected is quite small. About 0.8% of annual Canadian output, 0.3% of Mexican output, and 0.04% of EU output is affected by these tariffs. As such, these tariffs are likely to have a very minor direct effect on economic activity, jobs, and consumer price inflation in these regions. However, there is a chance of a more outsized negative impact on economic activity if the imposition of these tariffs dents confidence and therefore results in the delay or cancellation of new investment in these regions.

Our past analysis assumed that the tariffs would have a muted direct impact on U.S. economic activity and inflation. But, these estimates assumed exemptions would persist for Canada, Mexico, and the EU. As a result, this morning's announcement makes us more confident that while these tariffs are likely to have a limited impact on U.S. economic activity, they are likely to boost consumer price inflation by at least 0.1 percentage points this year and next.

Retaliatory Measures Promptly Announced

Although the direct impacts of the announced tariffs on the U.S. economy are anticipated to be small, equivalent tariffs announced by affected regions and the potential for further escalation could amplify the estimated drag on output and lift to consumer price inflation.

Retaliatory measures target a wide swath of U.S. exports. Mexico has announced "equivalent" tariffs on pork legs, apples, grapes, cheeses, and steel. Canada has responded by imposing surtaxes or similar trade-restrictive countermeasures on up to C$16.6 (US$12.6) billion of imports of steel, aluminum, and other products set to take effect on July 1st. Europe is likely to impose reciprocal tariffs on about €6.5 (US $7.7) billion of a variety of goods as early as mid-June.

Trade War Risk Looms Large

Today's announcement that the U.S. administration will go ahead with steel and aluminum tariffs on its allies and largest trading partners is another sign that trade tensions are escalating. Last week the U.S. administration announced an investigation in automobile imports on national security grounds, and earlier this week it announced intentions to proceed with tariffs on up to $50 billion in Chinese technology imports in mid-June.

The probability of a cold trade war turning hot has now risen, but still remains a worst case scenario. The opportunity for dialog remains, and the U.S. administration appears to be using these tariffs to encourage progress in trade talks with its allies.

DAX Soars As Italy Resolves Political Crisis

The DAX has posted strong gains in the Friday session, after sliding on Thursday. Currently, the DAX is at 12,738, up 1.06% on the day. In economic news, Manufacturing PMIs in Germany and the eurozone were within expectations. In the U.S, the focus will be on job numbers, with the release of nonfarm payrolls and wage growth. Both indicators are expected to climb, with estimates of 189 thousand and 0.2%, respectively.

It's been a roller-coaster road for the DAX this week. European stock markets were down sharply during the week, as a political crisis in Italy almost resulted in another election after an inconclusive vote in March. President Sergio Matterella had vetoed the choice of the prime minister-elect for finance minister, stunning the political establishment and sending Italian stocks and bonds tumbling lower. In a dramatic breakthrough, the President has given his approval to a new choice for finance minister. This has paved the way for two euro-sceptic parties, the League North and Five Star Movement, to form a coalition government as soon as Friday.

German numbers showed some weakness in the first quarter, but there was positive news on Wednesday. Retail sales were unexpectedly strong in April, with a sharp gain of 2.3%. This reading ended a nasty streak of four declines. The gain is the strongest since December and raises hopes that second-quarter growth will rebound after a sluggish first quarter. Inflation is also expected to improve, with German Preliminary CPI forecast to rise to 0.3% in May after a flat reading of 0.0% in April. On the inflation front, Eurostat is projecting a surge this month, with CPI Flash Estimate rising to 1.9%, its highest level since April 2017. Core CPI Flash Estimate improved to 1.1%, marking an 8-month high. Still, inflation remains well below the ECB target of around 2 percent. Inflation levels are being closely watched by the ECB, which is scheduled to wind up its stimulus program in September. The ECB reduced its stimulus in January, from EUR 60 billion to 30 billion each month.