Sample Category Title

Italy: Five Star-League Government Steering Towards a Clash With the EU

- Markets are set to focus on any indications by the new Five Star-League government on its policy agenda and priorities in coming days and weeks.

- We expect to see clashes between the Italian government and the EU on the economic ruleset over coming months.

- Abandonment of fiscal prudence could trigger more rating action in coming weeks.

- We recommend clients take a cautious stance on BTP and focus on other markets such as Spain or France, both of which have widened to Germany/swaps. We expect EUR/USD to retest the 2018 low at 1.1510 over coming weeks.

Following days of uncertainty, the Five Star Movement and League yesterday renewed their coalition deal and received approval for their cabinet from President Sergio Mattarella. Although the initial market reaction was positive, as political uncertainty subsided along with the risk of a new election, we think there will be more struggles ahead and believe that markets will continue to be very headline driven over the next few weeks and months.

EU relations—confrontations likely

The new government will be a combination of technocrats and politicians (see box above right). Following the row with the President over the appointment of Paolo Savona as Finance Minister last week, party leaders agreed on an alternative in the person of Giovanni Tria. Currently an economics professor at Rome's Tor Vergata University, he is a relatively unknown figure and reported to be close to centre-right circles. In an opinion piece in March 2017, Tria previously advocated monetary financing of government deficits if funds are spent on investment, which would be illegal under EU treaties. This leaves us to expect that he will not be averse to higher fiscal spending as envisioned by the new government. This said, we will need more information about his fiscal policy priorities and hence any comments from him in coming days and weeks on the topic of spending proposals and the relationship with the euro/EU will be of key market focus near term.

Positively, Tria is not considered an outright eurosceptic: although he has previously called for a debate on the euro in both Italy and the rest of Europe, he is not in favour of an outright euro exit ('the greatest danger is implosion, not exit'). Instead, changing the economic rulebook of the euro area is likely to be the focal point rather than leaving the euro area.

While the risk of an Italian exit from the eurozone is less likely, we think the new government will clash with Germany and other hawkish EU countries on the EU economic ruleset. The reaction of other European countries will depend on how reasonable they consider the new Italian government. There are some proposals that will be a 'no go' for the EU, such as monetary financing of deficits given the EU treaties and significant breaches of the EU deficit rules. However, on the other reform proposals such as larger EU public investments and more fiscal flexibility, the European reception of these proposals will depend on two things: (1) the new Italian government seems to respect the EU deficit rule (i.e. funds their spending proposals and income tax reforms with higher taxes in other areas) and (2) that they pick a few initiatives and do not go overboard.

Remember that France is advocating some of the same ideas on euro area integration but doing this while putting its own house in order. If the new Italian government does not do this, then it will be very difficult for France to ally with Italy and it will be an even clearer 'nein' from the German side. Our base case is that confrontations between Italy and Germany will be quite significant.

What to look out for in the next weeks and months?

The cabinet is due to be sworn in today at 16:00 and then it will face confidence votes in parliament on Monday and Tuesday. As the Five Star-League coalition has a majority in both chambers of Parliament, we think this should not constitute a big hurdle.

The euro group meeting on 21 June will surely be interesting, in terms of both the reception that other euro area finance ministers give Tria and the strategy line Italy chooses at these meetings. The next focal point is the heads of states meeting at end-June, when euro area integration and the next EU budget will be on the agenda. Surely, EU officials will now look at this meeting with heightened concerns. What may also be controversial is the renewal in early August of sanctions on Russia for another six months, which would require unanimous support from all EU countries and the new Italian government has more pro-Russia sentiment.

Another key market focus in the near term is any indication from the new government on its policy agenda and priorities. We still think it will be difficult for the Five Star- League coalition government to implement fully its programme in its current form (see also Italian Election Monitor – Rising market pressure set to challenge spending plans, 24 May). One of the government's first tasks will be to start working on the 2019 budget, which needs to be approved in the autumn and submitted to Brussels by 15 October.

Should the populist government not temper its spending proposals, we could see more action from the rating agencies. Moody's has already placed Italy on negative watch and a downgrade to Baa1 might come within weeks, if fiscal prudence is abandoned.

BTP market continues to be headline driven – we remain cautious on Italian bonds

Overall, Italian yields are now lower than before the close on Monday, when the sell-off started, and the curve has continued to steepen this morning. We agree with the initial market positive response, as we now have a government in place after months of uncertainty. The BTP market will continue to be alert to headline news on a possible revised fiscal policy programme and comments from rating agencies.

However, the genie is out of the bottle and we would recommend clients take a cautious stance on Italian bonds, until we have more clarity on a revised policy programme. We would rather focus on other periphery markets such as Spain or Portugal, where volatility-adjusted returns look more interesting. We are less concerned about the no-confidence vote against Prime Minister Rajoy today. We are likely to have a government led by the Socialist leader Sanchez and a new election within the next 12 months. However, in contrast to Italy, this could actually lead to a more stable and pro- European majority government emerging and the underlying fundamentals remain very favourable in Spain. France is another possibility after French bonds have widened.

EUR/USD set to fall back near term

Meanwhile, EUR/USD is currently trading higher than it closed one week ago. EUR/USD has been falling recently for a range of different reasons, with Italy being only one of them. Even if the Italian factor takes a backseat, we think the short-term factors for a lower EUR/USD near term – high USD carry and long EUR/USD positioning – remain intact. We expect EUR/USD to fall back over coming weeks towards the low of 1.1510 reached on 29 May.

Forex Analysis: EURUSD And Gold

Trading today will be dominated by the release of the US employment report which is expected to show a modest growth in jobs and wage inflation. Non-Farm Payrolls numbers for the month are expected at 188K while Average Hourly Earnings are expected to have grown to 0.2% month-on-month from a prior 0.1%. It would take an exceptionally large deviation from the forecasts to alter US monetary policy outlook however there is usually increased volatility around the release of this data. After this event, focus is likely to return to concerns over a trade war as the US has imposed tariffs on the EU, Canada and Mexico.

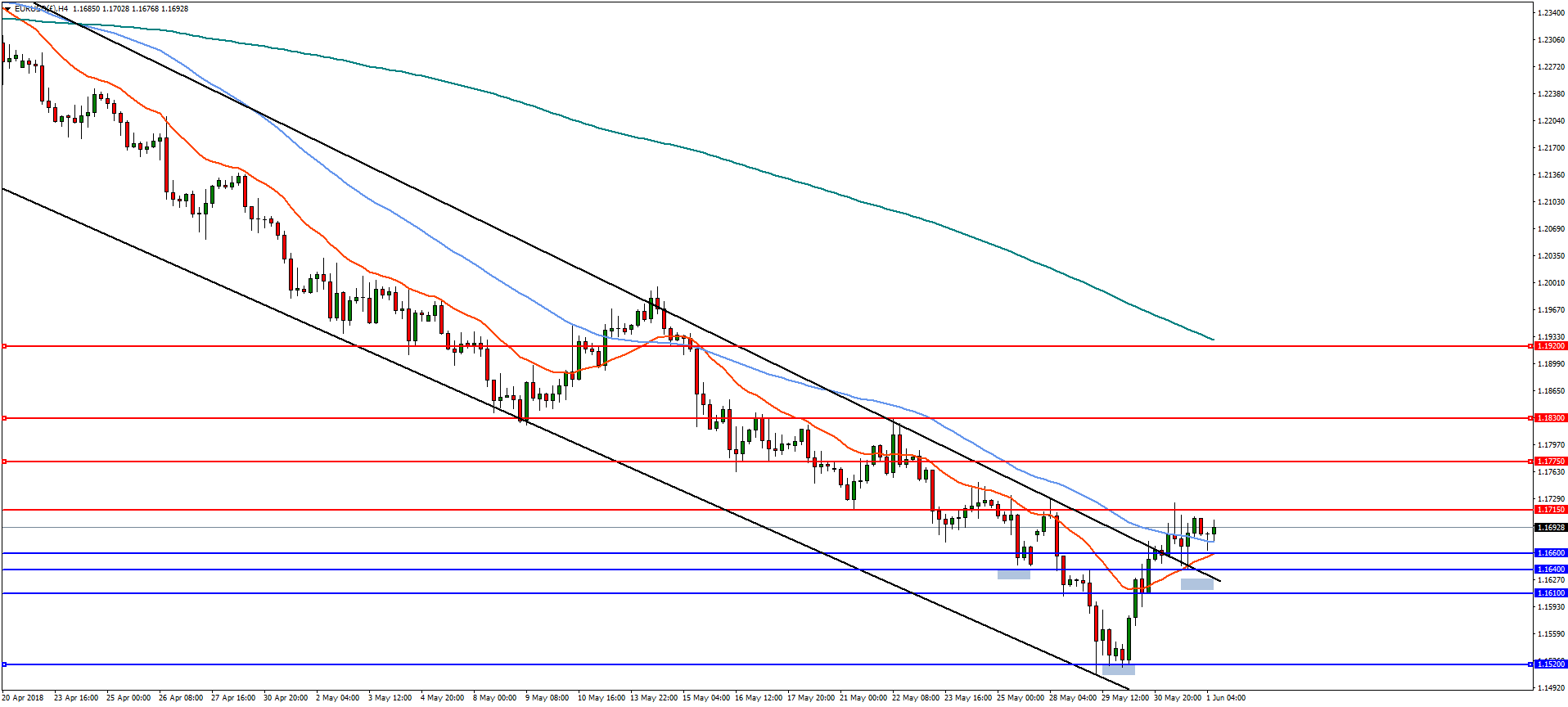

EURUSD

On the 4-hourly chart, EURUSD appears to have broken out of the descending trading channel and progress is capped at 1.1715. A break of this level would form a possible inverted head and shoulders pattern with a measured target of 1.1920 with resistance at 1.1750 and 1.1830. A reversal and break of 1.1660 would see the pair continue to the downside with support at 1.1640 and 1.1610.

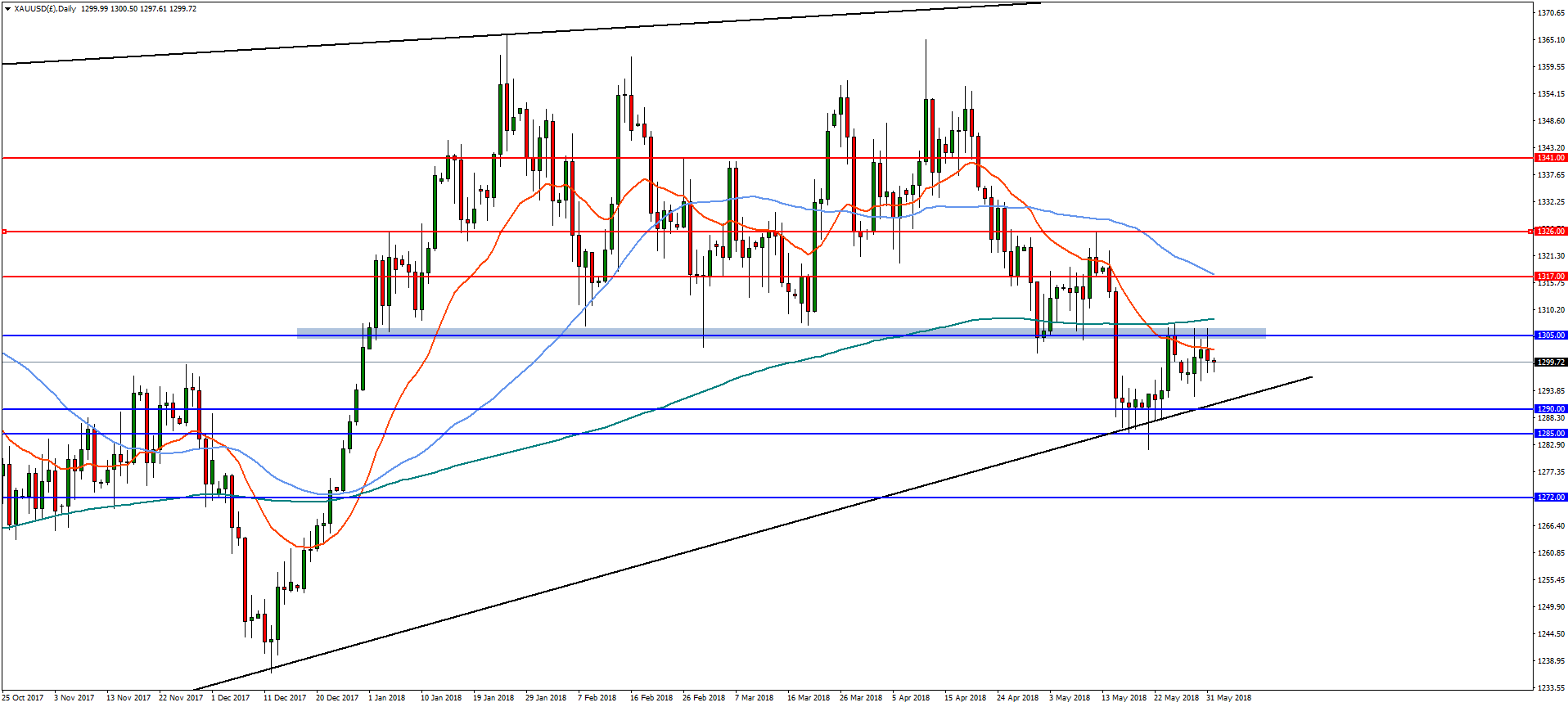

GOLD

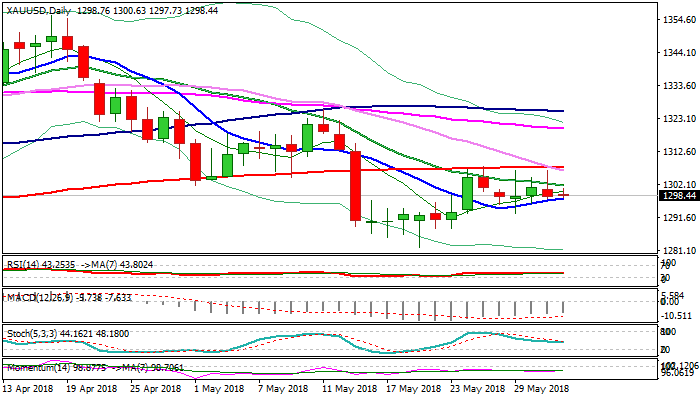

Gold is denominated in U.S. dollars so it is likely to react to the NFP report later today. Higher interest rates usually result in a strong dollar and can reduce the appeal of non yielding precious metals. In the daily timeframe, Gold is trading below the major horizontal resistance near 1305. A decisive break of 1305 is needed to open the way to a move towards resistance at 1317 and then 1326. On the flip side, a bearish reversal and break of trend line at 1290 would see a downside continuation to supports at 1285 and then the 38% retracement from the Oct 2016 lows at 1272.

Forex Analysis: EURJPY Wave Analysis

EUR/JPY reversed from support zone

Further gains are likely

EUR/JPY recently reversed up sharply from the support zone lying between the major support level 125.00 (former key resistance level from May and June of 2017), support trendline of the daily down channel from February and the lower daily Bollinger Band.

The upward reversal from this support zone completed the previous primary ABC correction ② from February – which belongs to the multi-month impulse sequence from June of 2017.

Having recently broken the resistance level 127.00 – EUR/JPY is likely to continue to rise toward the next powerful resistance level 129.50 (former strong support from March).

Euro Steady As German Manufacturing PMI Within Expectations

EUR/USD has recorded small gains in the Friday session. Currently, the pair is trading at 1.1709, up 0.12% on the day. On the release front, Manufacturing PMIs in Germany and the eurozone were within expectations. In the U.S, the focus will be on job numbers, with the release of nonfarm payrolls and wage growth. Both indicators are expected to climb, with estimates of 189 thousand and 0.2%, respectively.

After a brief hiatus, the markets are again facing the nasty reality of a trade war between the U.S. and its major trading partners. On Thursday, the Trump administration made good on its threats and imposed stiff tariffs on the European Union, Mexico and Canada. The EU and Canada fired back quickly, saying they would retaliate with tariffs on U.S products. The U.S had granted all three trading partners a temporary extension, but cited insufficient progress on trade talks as the reason for the tariffs. There are renewed fears that these moves could trigger a global trade war.

The drama continues in Italy, as political leaders scramble to avoid another election, after an inconclusive vote in March. The two largest parties, the League Nord and the Five Star Movement proposed a eurosceptic finance minister, but this was blocked by the pro-European President Sergio Matterella. This triggered a political crisis which led to a selloff of Italian stocks and bonds. The prime minister-elect, Giuseppe Conte, then announced that he had withdrawn his mandate to form a government, and Mattarella invited Carlo Cottarelli, a former IMF economist, to form a temporary technocrat government. There was talk of an election in the fall or even earlier, but Mattarella has agreed to let the two parties have a second go at forming a coalition government.

Trade War On, But Non-Farm Payroll (NFP) Up Next

Friday June 1: Five things the markets are talking about

U.S fire the first shot in trade war

Euro equities are looking to close out this wild week in the ‘black,’ a week in which Euro politics and escalating trade tensions have shook markets.

U.S Treasuries have edged lower and the ‘big’ dollar trades somewhat steady for the time being.

Italy’s benchmark index has aggressively rallied to five-month highs on news Italy’s populist parties have reached a deal on forming a government, ending concerns about possible new elections. Even U.S stocks are set to open higher as President Trump pushes ahead with tariffs on imports of metals from its key trading partners – CAD, MXN and EUR.

Even Spanish assets have dismissed the uncertainty surrounding PM Rajoy, who has just been replaced by the Socialist Pedro Sanchez after a no-confidence motion.

The positive overnight market moves would suggest that investors remain optimistic that threats of more international tariffs will not materialize into an all-out trade war, however, only time will tell.

Aside from trade and politics, investors will be focusing on today U.S payroll numbers (08:30 am EDT) for short-term market direction. Payrolls are expected to rise (+190ke) and the unemployment rate is to hold steady at its 18-year low (+3.9%e).

1. Stocks get the green light

In Japan, the Nikkei share average ended lower overnight, as selling in large cap stocks and concerns about U.S tariffs on metal imports erased earlier gains made after a weaker yen (¥109.17) supported exporter firms. The Nikkei fell -0.1%. For the week, it dropped -1.2%. The broader Topix added +0.1%.

Down-under, Australia’s S&P/ASX 200 has recorded its first three-week losing streak in three-months. The index fell -0.4%, putting the week’s drop at -0.7%, with commodities and financials being key pressure points. In S. Korea, the Kospi rallied +0.7% on stronger export data.

In Hong Kong, equities rallied overnight, aided by strong China manufacturing data, while worries over Italy cooled. The Hang Seng index rose +1.4%, while the China Enterprises Index gained +1.8%.

In China, stocks slid as U.S tariffs reignited fears of a global trade war, which has overshadowed China A-shares’ inclusion in MSCI’s benchmark market indexes – its expected to attract a lot of foreign capital inflows. The Shanghai Composite Index fell -0.5%, while the benchmark CSI300 dropped -0.8%.

In Europe, stocks have rallied sharply after Italy’s populist parties reached a deal on forming a government. Italy’s FTSE MIB jumps +2.7%, reversing much of the steep slide it suffered earlier this week. The U.K’s FTSE 100 and Germany’s DAX are up +0.7%, and even Spain’s Ibex 35 has rallied +1.3%.

U.S stocks are set to open in the ‘black (+0.4%).

Indices: Stoxx600 +0.9% at 386.35, FTSE +0.6% at 7725, DAX +0.8% at 12709, CAC-40 +1.1% at 5457; IBEX-35 +1.4% at 9594, FTSE MIB +2.7% at 22373, SMI +1.4% at 8571, S&P 500 Futures +0.4%

2. Oil prices mixed on inventories, gold unchanged

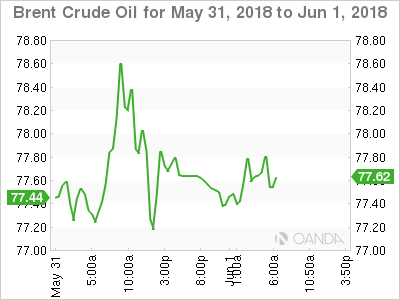

Oil prices have rallied overnight, supported by a surprise drawdown in U.S crude inventories and by expectations that OPEC may not be able to finalize an increase in output later this month (June 22).

Brent crude is up +20c at +$77.30 per barrel, after settling the last session up +2.8%. U.S West Texas Intermediate crude is down -10c at +$68.01 a barrel.

The Energy Information Administration yesterday reported a draw in crude oil inventories of -4.2m barrels for the week to May 25; a day after the API pressured benchmarks by estimating an unexpected inventory increase of +1m barrels for the same period.

The market was anticipating a build of +1m for last week, after a +5.8m increase a week earlier.

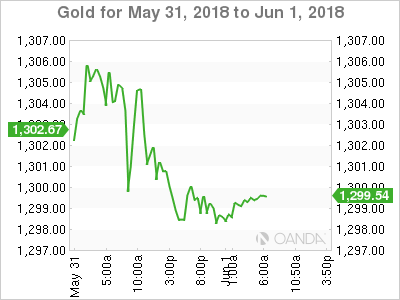

Ahead of the U.S open, gold prices remain steady on renewed fears of a global trade war, while a U.S firm dollar and positive U.S economic data continues to cap market gains. Spot gold is unchanged at +$1,298.29 per ounce, while U.S gold futures for June delivery are down -0.2% at +$1,298 per ounce. Spot gold is down slightly this week.

3. Focus on Spanish yields

Spanish government bond yields trade lower this morning, pulled along by the relief rally triggered by the setup of the new Italian government and ahead of PM Rajoy’s parliamentary confidence vote. The 10-year Spanish bond yield is trading -9.5 bps lower at +1.42%.

Elsewhere, the yield on U.S 10-year notes have gained +1 bps to +2.87%. In the U.K, the 10-year Gilt yield has advanced +3 bps to +1.263%, while in Italy, the 10-year BTP yield has dipped -15 bps to +2.641%, the lowest in a week. In Germany, the 10-year Bund yield has backed up +3 bps to +0.37%, the highest in a week.

4. Euro, CAD and MXN fall on U.S tariffs

In the long run, an isolationist U.S trade policy is bearish for the ‘big dollar.’

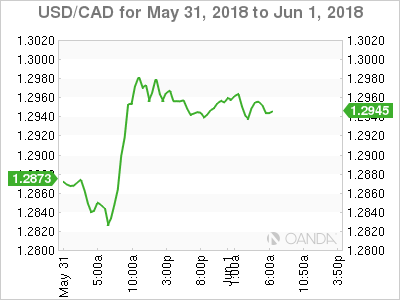

Nevertheless, the EUR (€1.1685), Canadian dollar (C$1.2951) and Mexican peso ($19.9190) have all fallen after the U.S announced tariffs on steel and aluminum imports from Canada, Mexico and the E.U starting today.

Canada and Mexico retaliated within hours after Washington imposed tariffs on steel and aluminum imports. While in Germany, the Economy Minister said today that the E.U might look to coordinate its response with Canada and Mexico.

Note: With the political situation remaining the primary focus in Europe, political uncertainties in E.U’s periphery is expected to keep the EUR under pressure and this despite a stronger-than-expected acceleration in the EMU’s May inflation print yesterday.

GBP/USD (£1.3297) has failed to gather any upward momentum despite a better-than-expected manufacturing PMI reading this morning (see below).

5. U.K manufacturing PMI rises

Data releases this morning showed that U.K manufacturing PMI rose above market expectations to 54.4 (53.5e) in May, but the pound still trades around the same level it was before the release. Why? The data came with warnings.

According to Markit, “although growth of production accelerated to its best during the year-so-far, this was mainly achieved through the steepest build-up of finished goods inventories in the 26-year survey history and a sharp reduction in backlogs of work.”

Moreover, “growth of incoming new business remained solid in May, but the pace of expansion eased to an 11-month low” and “the pace of job creation in the manufacturing sector also lost momentum,” it said.

Spot Gold Outlook – Extended Directionless Mode And Narrowing Range Ahead Of US Jobs Data

Spot Gold trades within extended triangular consolidation with tight range on Friday, in expectation of US jobs report which is expected generate stronger direction signal.

The price is holding between converging 10SMA ($1297) and 20SMA ($1301) which mark initial support/resistance.

Near-term action was repeatedly capped by sideways-moving 200SMA ($1307), with barrier being reinforced by formation of 30/200SMA bear-cross, but directionless near-term mode is maintained by flat momentum and RSI.

Solid US non-farm payrolls and especially wages would keep Fed’s hawkish mode for June rate hike which would boost dollar and sent yellow metal’s price lower.

Break and close below $1297 pivot (10SMA / Fibo 38.2% of $1282/$1307 upleg) would generate negative signal for fresh weakness towards supports at $1291 (Fibo 61.8%) and $1282 (21 May low) in extension.

Weaker than expected US jobs data would depress the greenback and open way for retest of the upper pivot, provided by 200SMA ($1307).

Res: 1301, 1307, 1309, 1315

Sup: 1297, 1295, 1291, 1288

Risk Appetite Improves Ahead Of US Jobs Data

- Italy Forms Government While Spain's Rajoy Loses No Confidence Vote;

- Investors Unconcerned By Imposition of Tariffs By the US;

- Wages Once Again Eyed in US Jobs Report.

You may not guess it based on the current levels in financial markets but it's been quite a week for investors which has been reflected by a spike in volatility, with politics being the main driver of the unrest.

Over the course of this week, we've seen coalition talks in Italy fall apart, restart and reach a successful conclusion – although other eurozone leaders may not quite agree with the label “successful” – Spanish Prime Minister Mariano Rajoy toppled in parliament following a no-confidence vote and replaced by Socialist leader Pedro Sanchez and finally, the US impose steel and aluminium tariffs on its allies, the EU, Canada and Mexico.

While many markets may now be trading back at levels they opened the week at, there has been volatility along the way with Italian 2-year yields peaking above 2.7% having been in negative territory two week ago, the Italian FTSE MIB falling more than 6.5% from Monday's open before reversing these as a deal was agreed and the euro slipping to 10-month lows against the euro.

There have been other casualties along the way as well with overall risk appetite having taken a hit at the prospect of Italy returning to the polls in what was being labelled a vote on the euro. This naturally got investors all over quite nervous with the eurozone debt crisis still very much fresh in the memory. While this week has been a stark reminder of how quickly things can unravel in pockets of the European political scene and reminds us of the risks that still exist in Italy, there is a sense of relief that some form of stability has resumed for now.

We can now get back to concerning ourselves with more trivial matters like trade wars and the economy. The imposition of steel and aluminium tariffs by the US on Europe, Canada and Mexico has drawn plenty of criticism from officials but maybe in a sign of how markets can become less sensitive to certain issues, the response has so far been fairly muted. Focus will now be on the retaliatory measures that these countries have lined up and whether that in turn triggers a larger and quite unnecessary trade war. Investors currently appear at ease with the situation but that could quickly change.

On the economy we have a rather significant set of data out today that rarely takes a back seat to other things but that has certainly been the case this week. The US jobs report is one of the most highly anticipated releases we get as it provides important insight into the strength of the US economy, labour market and potential inflationary pressures. With unemployment already at 3.9% and the labour market looking quite tight, there is likely to be more emphasis on the wages number as opposed to job creation, although that never falls entirely under the radar.

Strong wage growth has completely eluded this particular economic recovery, despite the apparent lack of slack in the labour market. Earnings are expected to have ticked slightly higher to 2.7% last month which is little changed on the last 18 months and doesn't represent any shift that would be indicative of labour market tightness flowing through into higher inflation. Aside from the jobs report we'll also get manufacturing PMIs from the US today.

New Italian Govt To Be Sworn In, Spain’s PM Rajoy On His Way Out

Notes/Observations

- Major European PMI Manufacturing data continues to decelerate from recent record levels. (Beats: Germany, UK, Spain, Netherlands, Sweden, Poland, Czech; Misses: France, Swiss, Norway, Russia; in-line: Euro Zone)

- Italian President Mattarella accepted the coalition government led by PM-designate Conte proposed by Five Star Movement and the League; uncertainty reduced but not over

- Spanish Parliament said to have gathered enough votes to pass the no-confidence vote against PM Rajoy

- US steel and aluminum tariffs on Canada, Mexico, and the EU yet to weigh on risk sentiment in session

Asia:

- China PBoC may additionally cut the reserve ratio requirement (RRR) by 50-150bps by the end of 2018

Europe:

- Italy President Mattarella formally gave PM-designate Conte mandate to form a Five Star/League coalition govt; face votes of confidence in both houses next week

- Italian Cabinet make-up has Five Star' leader Di Maio as Economic Development Min and Deputy PM; League leader Salvini to be Interior Min and Deputy PM. Salvona (euro skeptic) named European Affairs Min, Moavero Milanesi to be Foreign Min and Giovanni Tria named Fin Min

- Spain PM Rajoy reportedly did not plan to resign his post ahead of confidence vote on Friday

- Spain's PSOE (Socialist) Party Leader Sanchez reportedly said to be willing to negotiate date when new Spanish elections are held

- UK Brexit Min Davis reportedly devising new plan that would give Northern Ireland joint EU/UK status and border buffer zon

- European Stability Mechanism (ESM) Chief Economist: Crucial for Greece stick to their reforms in the coming months and following the end of the bailout. Hoped IMF could come on board during the final stretch of Greece's ESM program

- Greece PM Tsipras: Govt to vote all prior actions to conclude the last bailout review by mid-June . To have the final by end of June and a definite decision for Greece’s debt relief

Americas:

- Commerce Sec Ross: Trump administration imposed metal tariffs on Canada, Mexico and EU as of midnight, Jun 1st (as speculated). Set 25% tariff on steel, 10% tariff on aluminum. Arrangements made for Argentina, Brazli and Australia to have non-tariff limits on metal exports putting constraints on volume of shipments

- Mexico Econ Min Guajardo: The worst trade scenario has been implemented; Mexico will announce tariff targets as soon as next week

- Canada Economy Minister Freeland: to impose 25% or 10% surtax on steel and aluminum products and tol take effect on July 1st (matching US tariff rates); to also impact food products including orange juice and whiskey

- Fed Bullard (dove, non-voter): Trade talks creating more uncertainty in economy; difficult to see if too much will change after talks. Inflation would need to surprise to upside for rate hikes

- Fed's Mester (hawk, FOMC voter): Italy political situation hasn't changed view of US economic fundamentals

Economic Data:

- (PE) Peru May CPI M/M: 0.0% v 0.1%e; Y/Y: 0.9% v 1.0%e

- (IE) Ireland May Manufacturing PMI: 55.4 v 55.3 prior (60th month of expansion)

- (IN) India May Manufacturing PMI: 51.2 v 51.6 prior (10th month of expansion)

- (JP) Japan May Vehicle Sales Y/Y: -0.6% v +0.5% prior

- (RU) Russia May Manufacturing PMI: 49.8 v 51.1e (1st contraction in 23 months and lowest since July 2016)

- (AU) Australia May Commodity Index (AUD): 109.3 v 109.0 prior; Commodity Index SDR Y/Y: +3.6 v -1.4% prior

- (SE) Sweden May Manufacturing PMI: 55.8 v 55.0e

- (CZ) Czech Q1 Preliminary GDP Q/Q: 0.4% v 0.5%e; Y/Y: 4.4% v 4.5%e

- (NL) Netherlands May Manufacturing PMI: 60.3 v 59.9e (57th month of expansion)

- (NO) Norway May Manufacturing PMI: 55.8 v 56.5e

- (PL) Poland May Manufacturing PMI: 53.3 v 53.2e (42nd month of expansion)

- (TR) Turkey May Manufacturing PMI: 46.4 v 48. 5 prior (30th month of expansion)

- (HU) Hungary Mar Final Trade Balance: €0.6B v €0.6B prelim

- (ES) Spain May Manufacturing PMI: 53.4 v 54.0e (55th month of expansion)

- (CZ) Czech May Manufacturing PMI: 56.5 v 56.2e (22nd month of expansion)

- (CH) Swiss May Manufacturing PMI: 62.4 v 62.5e

- (CN) Weekly Shanghai copper inventories (SHFE): 272.4K v 268.4K tons prior

- (TH) Thailand May Business Sentiment Index: 51.5 v 49.5 prior

- (IT) Italy May Manufacturing PMI: 53.0e v 53.5 prior (21st month of expansion but lowest since Nov 2016)

- (FR) France May Final Manufacturing PMI: 54.4 v 55.1e (confirmed its 20th month of expansion)

- (DE) Germany May Final Manufacturing PMI: 56.9 v 56.8e (confirmed 41st month of expansion but lowest since Feb 2017)

- (EU) Euro Zone May Final Manufacturing PMI: 55.5 v 55.5e (Confirmed 58th month of expansion)

- (GR) Greece May Manufacturing PMI: 54.2 v 52.9 prior (12th month of expansion)

- (IT) Italy Q1 Final GDP Q/Q: 0.3% v 0.3%e; Y/Y: 1.4% v 1.4%e

- (NO) Norway May Unemployment Rate: 2.2% v 2.2%e

- (UK) May Manufacturing PMI: 54.4 v 53.5e (22nd month of expansion)

- (ZA) South Africa May Manufacturing PMI: 49.8 v 50.7e (1st contraction in 3 months)

- (DK) Denmark May PMI Survey: 47.5 v 55.9 prior

Fixed Income Issuance:

- (IN) India sold total INR120B vs. INR120B indicated in 2020, 2026, 2031, 2033 and 2055 bonds

- (ZA) South Africa sold total ZAR600M vs. ZAR600M indicated in I/L 2022, 2033 and 2050 bonds

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

- Indices [Stoxx600 +0.9% at 386.35, FTSE +0.6% at 7725, DAX +0.8% at 12709, CAC-40 +1.1% at 5457; IBEX-35 +1.4% at 9594, FTSE MIB +2.7% at 22373, SMI +1.4% at 8571 , S&P 500 Futures +0.4%]

Market Focal Points/Key Themes:

- European stocks rallied and bond yields eased on Friday as investors welcomed an apparent end to a political crisis in Italy. Trade war concerns kept gains modest.

Equities

- Financials: Deutsche Bank DBK.DE +3.1%(S&P cuts rating)

- Healthcare: Elekta AB EKTAB.SE -3.6% (Q4) results

Speakers

- Germany Foreign Min Altmaier: EU might seek to answer US on trade by working with Mexico and Canada

- North and South Korea to hold military talks on Jun 14th

Currencies

- The political situation remained the focus in Europe. Political uncertainties in Europe’s periphery was keeping the Euro facing headwinds and yet to find any momentum to the upside despite a stronger-than-expected acceleration in the EMU's May inflation print

- EUR/USD remained below the 1.17 level as the new Italian govt likely to propose significantly higher fiscal spending which could still widen the BTP-Bund spread and reduce prospects around EMU reforms. The looming change in leadership in Spain less of distraction as analysts note that most Spanish parties were in favor of respecting EU fiscal rules

- GBP/USD failed to muster any upward momentum despite a better-than-expected Manufacturing PMI reading. Dealers noted that inside the details the picture was not as rosy for the UK data. GBP/USD at 1.3280 just ahead of the NY morning.

- USD/JPY holding above the 109 level and shrugging off escalating protectionism as the US imposed its metal tariffs.

Fixed Income

- Bund Futures trade 26 ticks lower at 161.49 after Italy agrees to form a government and Socialist chief Pedro Sanchez set to become Spain's Prime Minister. Upside targets 163.75 followed by 164.50, while a return lower targets the 160.25 level.

- Gilt futures trade at 124.05 lower by 28 ticks after better than expected manufacturing data. Support continues stands at 123.75 then 123.25, with upside resistance at 125.85 then 127.35.

- Friday’s liquidity report showed Thursday’s excess liquidity rose from €1.845T to €1.890T. Use of the marginal lending facility increased from €120M to €145M.

- Corporate issuance saw 1 issuer raise $1.5B

Looking Ahead

- (IT) Italy May Budget Balance: No est v -€3.1B prior

- (AR) Argentina May Government Tax Revenue (ARS): No est v 236.2B prior

- (RU) Russia May Sovereign Wealth Funds: Wellbeing Fund: No est v $63.9B prior

- (ES) Spain Parliament to hold no-confidence vote on PM Rajoy

- G7 Finance Ministers meet in Canada

- 06:00 (SE) Sweden Central Bank (Riksbank) Gov Ingves

- 06:00 (UK) DMO to sell combined £4.0B in 1-month, 6-month and 12-month Bills (£0.5B, £1.5B and £2.0B respectively)

- 06:45 (US) Daily Libor Fixing

- 07:30 (IN) India Weekly Forex Reserves

- 08:00 (CZ) Czech May Budget Balance (CZK): No est v 0.8B prior

- 08:00 (PL) Poland Central Bank (NBP) May Minutes

- 08:00 (EU) EU top trade official Malmstrom press conference on tariffs

- 08:00 (IN) India announces upcoming bill issuance (held on Wed)

- 08:00 (ES) Spain Debt Agency (Tesoro) announces upcoming bond issuance

- 08:15 (UK) Baltic Dry Bulk Index

- 08:30 (US) May Change in Nonfarm Payrolls: +190Ke v +164K prior; Private Payrolls: +190Ke v +168K prior; Manufacturing Payrolls: +20Ke v +24K prior

- 08:30 (US) May Unemployment Rate: 3.9%e v 3.9% prior

- 08:30 (US) May Average Hourly Earnings M/M: 0.2%e v 0.1% prior; Y/Y: 2.6%e v 2.6% prior; Average Weekly Hours: 34.5e v 34.5 prior

- 08:30 (CA) Canada Apr MLI Leading Indicator M/M: No est v 0.1% prior

- 08:30 (US) Weekly USDA Net Export Sales

- 08:55 (US) Fed’d Kashkari (non-voter, dove)

- 09:00 (BR) Brazil May Manufacturing PMI: No est v 52.3 prior

- 09:00 (CL) Chile Apr Retail Sales Y/Y: 4.8%e v 4.1% prior; Commercial Activity Y/Y: No est v 3.4% prior

- 09:30 (CA) Canada May Manufacturing PMI: No est v 55.5 prior

- 09:45 (US) May Final Markit Manufacturing PMI: 56.6e v 56.6 prelim

- 10:00 (US) Apr Construction Spending M/M: +0.8%e v -1.7% prior

- 10:00 (US) May ISM Manufacturing: 58.2e v 57.3 prior; Prices Paid: 78.0e v 79.3 prior

- 10:00 (MX) Mexico Apr Total Remittances: $2.5Be v $2.6B prior

- 10:00 (MX) Mexico Central Bank Economist Survey

- 10:00 (IT) Italy PM Conte’s government to be sworn in

- 10:30 (MX) Mexico May Manufacturing PMI: No est v 51.6 prior

- 11:00 (CO) Colombia Apr Exports: $3.5Be v 3.3B prior

- 11:00 (EU) Potential sovereign ratings after the European close (Hungary Sovereign Debt to be rated by Moody's; Ireland Sovereign Debt to be rated by S&P; Portugal and Belgium Sovereign Debt to be rated by Fitch

- (BE) Belgium Sovereign Debt to be rated by Fitch

- 12:00 (IT) Italy May New Car Registrations Y/Y: No est v 6.5% prior

- 13:00 (US) Weekly Baker Hughes Rig Count data1-Jun

- 13:00 (MX) Mexico May IMEF Manufacturing Index: 52.0e v 51.7 prior; Non-Manufacturing Index: 52.6e v 52.4 prior

- 14:00 (BR) Brazil May Monthly Trade Balance: $7.2Be v $6.1B prior; Total Exports: $21.4Be v $19.9B prior; Total Imports: $14.8Be v $13.8B prior

Global Stocks Shrug Off Trade War Fears, NFP In Focus

This has certainly been a rollercoaster trading week for financial markets thanks to geopolitical uncertainty and renewed trade war fears.

Easing political tensions in Italy have rekindled risk appetite, ultimately resulting in global equity markets venturing higher. However, global sentiment is likely to remain cautious after the United States announced it would impose steel and aluminium tariffs on Canada, Mexico and the EU. With Canada and Mexico immediately retaliating against the US tariffs and the EU threatening a similar response, fears could intensify over a global trade war. While stock markets could nudge higher on relief over Italy narrowly avoiding snap elections, gains are likely to be capped by renewed trade war concerns.

Euro strengthens as Italy fears ease

The Euro was thrown a lifeline this week after a last-minute coalition agreement between Italy's two anti-establishment parties eased fears of a snap election.

While the Euro has scope to extend gains as Italian political tensions ease, the question is - for how long? With uncertainty likely to mount following the Spanish Parliament forcing Mariano Rajoy out of office in a vote of no confidence, the Euro remains exposed to downside risks. Taking a look at the technical picture, the EURUSD remains bearish on the daily charts despite the rebound witnessed this week. A technical bounce could be in play, with the next key levels of interest at 1.1750 and 1.1820.

Dollar weakens ahead of NFP report

Today's main risk event for the Dollar will be the monthly US jobs report for May, which could offer fresh insight into the health of the US labour market.

Markets expect the US economy to have added 189k jobs in May, up from 164k in April, while the unemployment rate is predicted to remain steady at 3.9%. Much attention will be directed towards wage growth figures which could shape US rate hike expectations beyond June. Any signs of accelerating wage growth may boost speculation over the Federal Reserve adopting a more aggressive approach towards monetary policy normalization this year. With the Dollar highly sensitive to monetary policy speculation, expectations over the Fed raising rates faster than expected could provide the currency a boost.

Taking a look at the technical picture, the Dollar Index remains bullish on the daily charts. A solid US jobs report could inspire bulls with enough inspiration to challenge the 95.00 level. Alternatively, sustained weakness below 94.00 could invite a decline towards 93.40.

Commodity spotlight – Gold

Gold has been pushed and pulled by a variety of fundamental drivers this week with prices trading marginally below $1300 as of writing.

While geopolitical uncertainty and trade war fears continue to boost appetite for the precious metal, gains have been limited by expectations of higher US interest rates. Price action suggests that the yellow metal is searching for a fresh directional catalyst, and this could come in the form of the US jobs report that is scheduled for release today. Investors will continue to closely observe how prices react around the psychological $1300 level.

From a technical standpoint, repeated weakness below $1300 could encourage a decline towards $1280. Alternatively, a solid breakout above $1300 may invite an incline higher towards $1324.

Forex Analysis: EURJPY And USDMXN

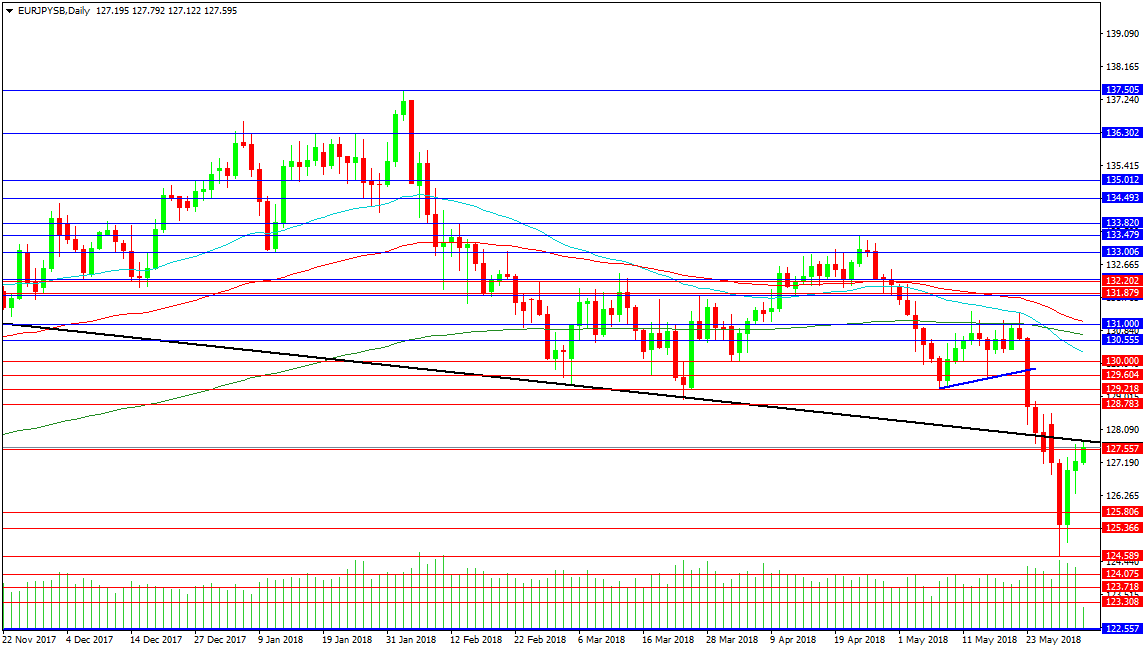

EURJPY

The EURJPY pair is at an interesting spot today, retesting the broken black support trend line as resistance at 127.792. The implication here is that a failure to break back higher will drive price to new lows. After falling below the 127.000 area on Wednesday price entered a barren zone on the chart where there was little in the way of support/resistance. After price fell through this zone it found support around 124.600 and rebounded higher to retest the trend line today once again rapidly moving through the barren zone. A move down to the low of this week could see price find some support along the way but with rallies being sold and the trend being to the downside it is likely that a push under 123.000 towards 122.557 is on the cards.

The price tumbled down last week when it rejected the moving averages around 131.000 with a loss of the blue trend line support at 129.750 sealing its faith. A recovery above 128.000 and a successful retest of the black trend line as support would encourage long positions. But ultimately the 131.000 area has to be overcome in order to have any chance of creating a higher high. Political instability and Trade Tariffs are creating turmoil in markets with the distinct chance that trend may be about to break.

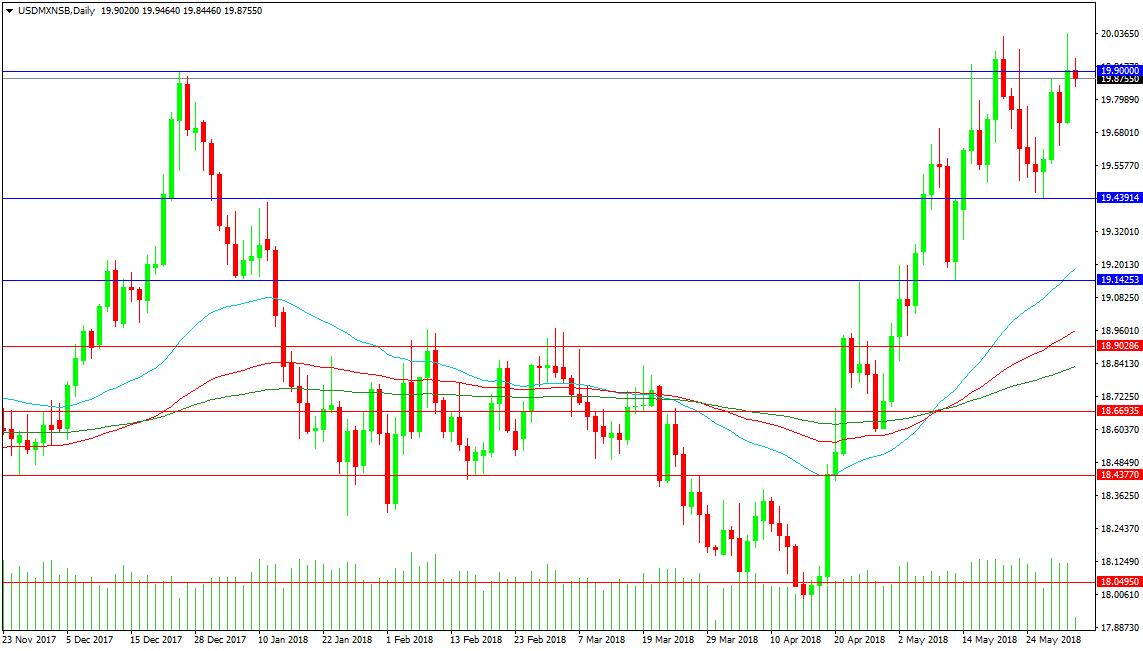

USDMXN

The USDMXN pair was the first to react to news that the US was going to apply Trade Tariffs to the EU, Canada and Mexico. The pair has tested 20.03900 as resistance and pushed back down to 19.90000. A continuation of the trend would see a breakout higher towards 20.11760 followed by 20.27173. These levels are key lows from December 2016 and January 2017. The swing high from early 2017 is found at 20.53710.

A loss of 19.43914 would see a reversal of the trend down to the 19.14250 area and the 50 DMA. The 100 DMA is at 18.96338 with the 19.00000 level a key psychological level in between. A loss of this region would target supports at 18.66935 and 18.43770. There is a chance price could consolidate in this area and even reverse higher once again. A push down to support at 18.00000 would need to see buyers return to avoid a retest of long term trend line support at 17.77000.