Sample Category Title

EURUSD Intra-Day Analysis

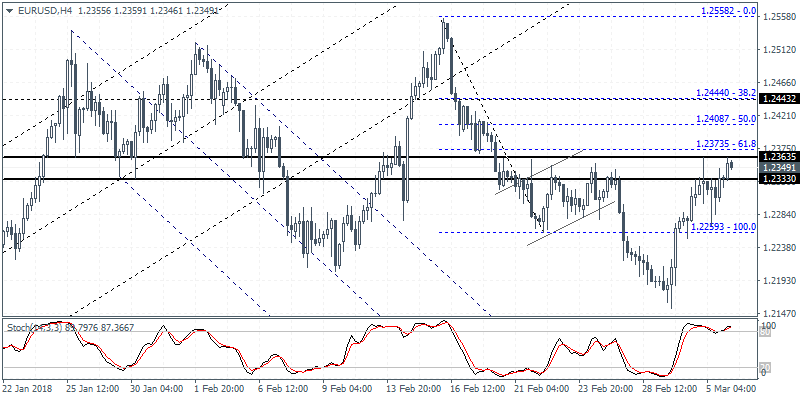

EURUSD (1.2349): The EURUSD was seen edging posting gains on the day as the common currency brushed aside the uncertainty from the Italian elections. Price action was seen recovering back to the familiar resistance level of 1.2365 - 1.2330. A close above this level could potentially signal a shift in the bias to the upside and could also invalidate the bearish flag pattern which is already showing signs of invalidation. To the downside, EURUSD will be seen targeting 1.2260 level followed by a test of the lower support near 1.2090 - 1.2070 region.

Euro Muted To Italy’s Election Results

The euro currency was seen muted to the outcome of the Italian elections which showed rising support for the anti-establishment parties while also resulting in a hung parliament. The various parties, led by the 5 Star Movement is expected to start coalition talks.

On the economic front, the UK's services PMI data improved, rising to 54.5 in February as the data beat estimates of 53.3 and gained from January's 53.0. In the Eurozone, retail sales data showed a 0.1% decline which was below estimates of a 0.3% increase.

The non-manufacturing PMI from ISM showed a flat print, as the index registered a print of 55.9, which matched estimates and was unchanged from the previous month's print.

For the day ahead, the economic calendar today will feature comments from NY Fed President; William Dudley followed the U.S. factory orders. Later in the day, the Bank of England's chief economists, Andy Haldane will be speaking. Following the RBA's decision earlier today, the RBA Governor Lowe is expected to speak later in the day.

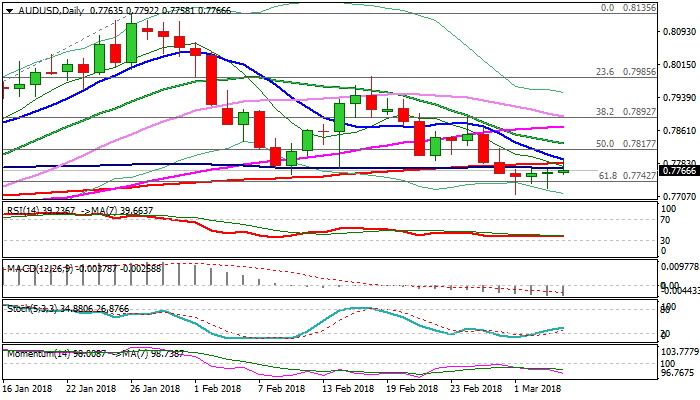

Technical Outlook: AUDUSD Remains Directionless After Little Reaction On RBA, Australian Data

The Australian dollar showed mild reaction on mixed Australian data and RBA rate decision on Tuesday.

The pair ticked above pivotal barriers at 0.7772/85 (100/200SMA’s) and hit session high at 0.7792, where rally was capped by falling 10SMA.

However, upticks were short-lived as the price returned to the levels where it traded before data at 0.7760 zone.

Australian current account surged in Q4, showing surplus of A$14 billion, up from A$11 billion surplus in Q3 and well above forecasted deficit of A$12.3 billion.

Positive impact from upbeat current account numbers was offset by weaker than expected retail sales which rose by 0.1% in Jan, undershooting forecast for 0.4% rise, but showing better result from Dec, when retail sales were down by 0.5%.

Reserve bank of Australia left interest rates unchanged as expected on today’s meeting. Australian interest rates remain at record low at 1.5% and the central bank signaled that will likely remain on hold in coming months as it is unlikely that the economy would grow 3% or more in 2018.

Techs on daily chart remain weak, with MA’s still in firm bearish setup and fresh bearish momentum building that keeps negative near-term outlook.

The pair remains in a choppy mode in past few sessions, with repeated downside rejections, keeping bears limited for now. Repeated failures to close below cracked pivot at 0.7742 (Fibo 61.8% of 0.7500/0.8135 rally) lacking firmer bearish signal which would be generated on sustained break below.

The upside actions remain limited and 100/200SMA’s still acting as active barriers, following today’s brief probe above and guard another strong barrier at 0.7817 (base of thick daily cloud).

The pair looks for a catalyst to spark fresh action to break out of current congestion and generate fresh direction signal.

Performance of the US dollar which firmed after initial fears about possible trade war started to fade, would give more clues about the near-term direction of the Aussie..

US jobs data on Friday are closely watched for fresh signals.

Res: 0.7772, 0.7785, 0.7792, 0.7817

Sup: 0.7758, 0.7742, 0.7712, 0.7700

BoJ Kuroda: No plan to hike nor abandon negative rates

BoJ Governor Haruhiko Kuroday said at upper house confirmation hearing:.

- "Underlying price moves remain weak, so our feeling is that there is some distance to achieving our price target,"

- "It's unthinkable to end or weaken the degree of monetary easing before our inflation target is met,"

- "We may adjust interest rates in the future depending on price developments"

- "But I don't have any plan now to raise short-term rates from the current minus 0.1 percent or abandon negative rates,"

- "We will continue to take whatever necessary steps to achieve our price target."

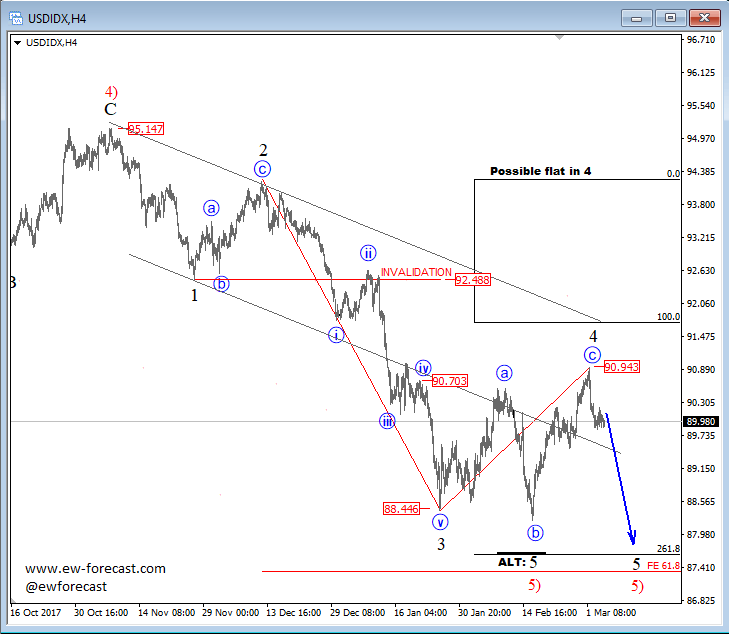

USD Index Unfolding A Bearish Reversal Towards 88.00

USD index is turning down from 91.00 area where we were looking for a top formation of a wave 4 bounce which shows evidences of a top after that nice sell-off to 90.00 which suggests that bears are not over yet. Ideally wave 5 is coming now within wave 5) towards 88.00/87.00 area.

USD Index, 4H

Swiss CPI rose 0.4% mom, 0.6% yoy. No market reaction

Swiss CPI:

- 0.4% mom vs exp 0.3% mom vs prior -0.1% mom

- 0.6% yoy vs exp 0.6% yoy vs prior 0.7% yoy

Quote from release

"The 0.4% increase compared with the previous month can be explained by several factors including rising prices for air transport. Foreign package holidays also recorded an increase, as did clothing and footwear due to the end of the seasonal sales. In contrast, prices for heating oil, coffee and overnight stays in hotels decreased."

Full release: Consumer prices increased by 0.4% in February

Comments: No impact on the markets, nor would it change SNB's neutral stance

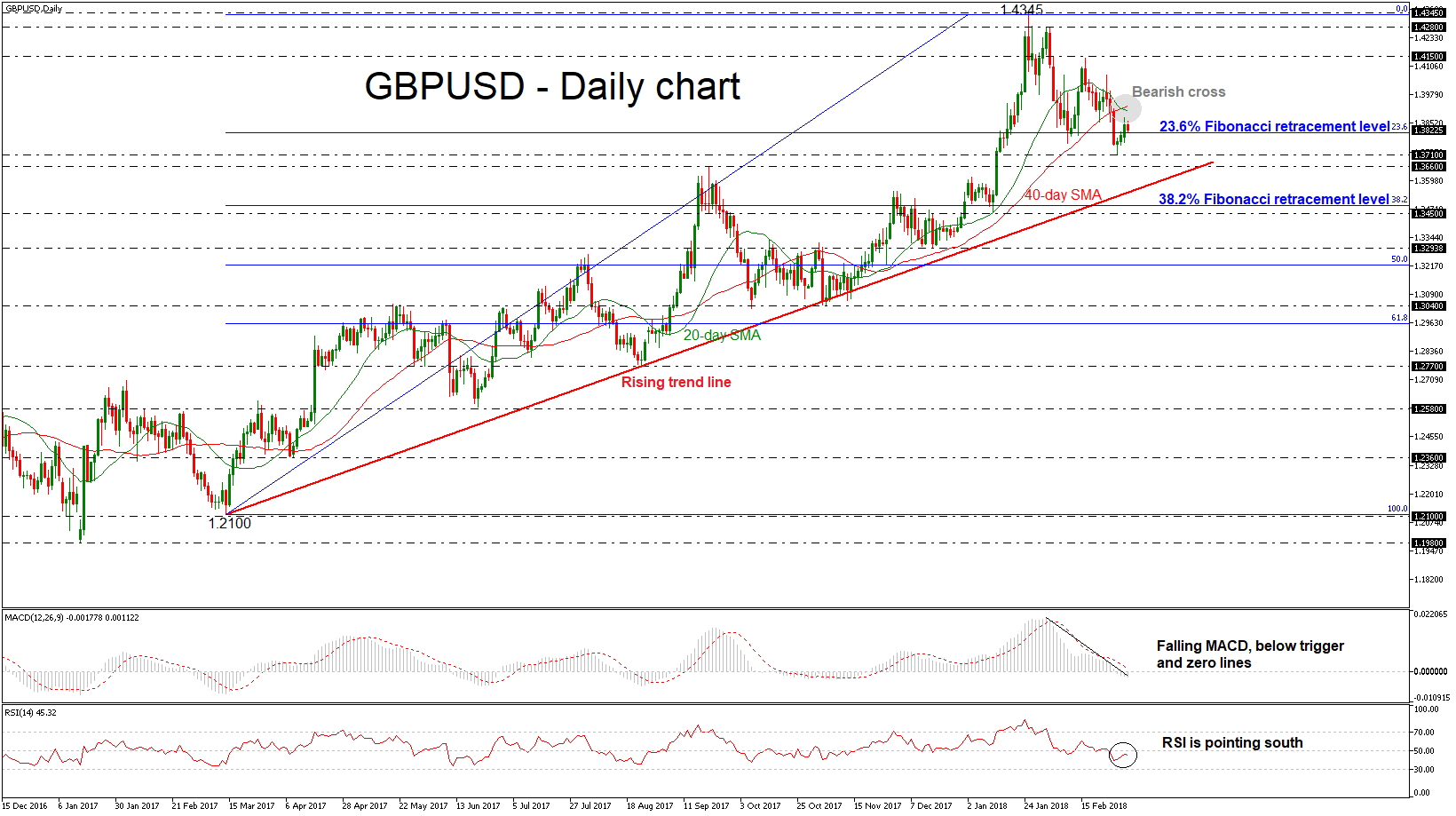

GBPUSD Bearish Correction Mode Holds, Indicators Endorse Further Losses

GBPUSD completed three green trading days in a row, while during today’s European session is moving marginally lower. The price is capped by the 20 and 40 simple moving averages in the daily timeframe, but it jumped above the 23.6% Fibonacci retracement level at 1.3810 of the upleg with the low of 1.2120 and the high of 1.4345.

Having a look on the short-term indicators, the bearish correction remains in focus as both are endorsing the downside movement. The MACD oscillator is falling below the trigger and zero lines, while the RSI indicator is pointing south in the negative zone. It is worth mentioning that the 20-SMA is recording a bearish cross with the 40-SMA, suggesting further decline.

If price continues the downside retracement and extends its losses below the 23.6% Fibonacci mark, it could open the door for the 1.3660 – 1.3710 support area. If there is a fall below the latter level, there would be scope to test the next immediate support of 38.2% Fibonacci level slightly above the 1.3450 barrier.

Conversely, if cable penetrates to the upside the aforementioned bearish cross within the simple moving averages, it could then move towards the 1.4150 resistance level, taken from the peak on February 16. A break above this area could take the price towards the 1.4280 resistance barrier.

Looking at the bigger picture, the cable has been developing within an ascending move over the last year, hitting the uptrend line several times in the previous months.

Sunrise Market Commentary

Markets

Yesterday, global trade tensions and an inconclusive outcome of the Italian elections caused a good start for core bonds, but the flight to safety bid eased soon as European equities (ex-Italy) returned into positive territory. The EMU PMI was revised to 57.1 (from 58. 8 in January), but had no impact on bonds. The US non-manufacturing ISM printed at a strong 59.5. US equities started an intraday up-leg as several high-ranked Republican politicians tried to convince President Trump no the implement tariffs on steel and aluminum. At the end of the day, US yields rose about 1.5 bp, the 2-year outperforming (-0.4bp). German yields declined less than 1 bp, 30 yr underperforming (+0.7 bp). Italian 10-y yield spreads versus Germany widened 4 bps.

Today, the eco calendar is thin. European investors look forward to Thursday's ECB meeting. Given the ongoing low inflation, the ECB is unlikely to make a U-turn in its communication. In the US, factory orders will be published and Fed's Dudley will speak. Global risk sentiment and the US debate on trade and tariffs will likely set the tone for trading. Markets are growing more confident that Trump's announcement last week won't have a big impact on global trading. Some further losses in core bond might be on the cards. However, bonds probably won't break key support until the tariffs' issue is really out of the way. 119-14 is the cycle low in the 10-y Note future (corresponds with the 2.95 % 10-y yield). The bund might slightly outperform ahead of the ECB meeting.

Yesterday, EUR/USD showed no clear trend. The pair dropped temporary below 1.23 early in Europe as the political uncertainty in Italy weighed. However the setback was short-lived. EUR/USD settled in the lower half of the 1.23 big figure. Later, the USD didn't succeed any meaningful gains against the euro even as US equities rallied and as fear for a trade war eased. USD/JPY (and EUR/JPY) profited from the intra-day rise in core yields and the equity rebound. USD/JPY regained the 106 barrier. This morning, the risk rebound continues in Asia. For now it doesn't help the dollar much. USD/JPY reversed opening gains is again trading in the low 106 area. EUR/USD is gaining marginally further ground. With few eco data on the calendar and the US ‘tariffs' issue still pending, we expect more technical trading in EUR/USD. Expectations for a relatively soft ECB might cap further euro gains. EUR/USD trades in neutral territory (middle of the 1.2155/1.2555 trading range).

Sterling traded with a slight positive bias yesterday. Brexit moved temporary to the background and the UK services PMI rebounded more than expected, keeping the door open for a BoE rate hike in May. EUR/GBP declined from mid 0.89 to the 0.89 area. There are no important UK data today. BoE's Haldane will speak in London this evening. The EUR/GBP 0.8930 intermediate resistance was extensively tested last week, but no sustained break occurred. This suggests that further GBP losses are maybe not that evident as long as the EU and UK are on speaking terms.

News Headlines

U.S. President Trump is facing pressure from political allies and U.S. companies not to implement proposed steel and aluminum tariffs. White House adviser Cohn is preparing a meeting with US companies that depend on steel and aluminum in an attempt to make the President change his mind. The meeting will probably take place on Thursday.

The Reserve Bank of Australia left its policy rate unchanged at 1.5% , as expected. The RBA downgraded its assessment on future growth. The RBA now expects the Australian economy to "grow faster in 2018 than it did in 2017". In its previous assessment it assumed growth to be "above 3 percent" over the next couple of years.

Fed Vice Chairman Randal Quarles said U.S. financial agencies are preparing to make “material changes” to the Volcker Rule. “The regulation implementing the Volcker Rule is an example of a complex regulation that is not working well”, he said at a banking conference.

U.S. Tariffs – A Political Show?

The 1.1% surge in the S&P 500, the 336 points rally in the Dow Jones Industrial Average and the strong bounce in European markets on Monday are hard to justify, after President Trump announced plans to slap tariffs on steel and aluminum imports last week. He followed this up with a statement saying that trade wars are good and easy to win.

History has taught us that trade wars are not good and in fact, not easy to win. In March 2002, President George W. Bush took a similar approach to Trump, imposing tariffs of 8-30% on steel to revive the domestic industry and exempted Canada, Mexico and a few other countries. These temporary duties were scheduled to remain in effect until 2005. As a result, the EU threatened to impose retaliatory tariffs on U.S. products and a case was filed at the World Trade Organization, which ruled in November 2003, that more than $2 billion in sanctions would be levied if the U.S. did not remove tariffs. Less than a month after the ruling President Bush backed down and withdrew the tariffs.

The S&P 500 dropped more than 30% from March until July 2002, U.S. 10-year treasury yields fell 100 basis points, and the U.S. dollar lost more than 12% in the same period. Of course, many other factors led to these declines, but surely the tariffs did not benefit the economy as Bush thought it would.

Investors seem to believe that President Trump is using his “Art of the Deal” skills to get a better trade deals with the rest of the world or, as Ray Dalio, the Bridgewater Associates founder, wrote on Monday: “what is happening now is more for political show than for real threatening."

Trump tweeted yesterday that “Tariffs on steel and aluminum will only come off if new & fair NAFTA agreement is signed”. This confirms my belief that this mess will likely end up with Mexico, E.U. and China taking a less protectionist stance, rather than the U.S. taking a stronger one.

House Speaker Paul Ryan and other conservatives are not falling in line behind Trump, only time will tell how the situation will evolve, given the unpredictability of Trump. Although I am optimistic that things won't degenerate to a full scale trade war, caution is warranted at this stage.

Futures indicate that equities will continue the rebound when Europeans markets open, but there's little action in currency markets. I think investors are holding off from big bets ahead of the European Central Bank meeting on Thursday and the U.S. jobs report release on Friday. With no tier-one data on the economic calendar today, expect range-bound trading to resume unless we see a surprise on the political front.

RBA Leaves Rates On Hold At 1.5%

The Market has shrugged off any fears of Trade Wars arising from the proposals that were released by the White House last week, with the consensus that they are being used as a threat to force trading partners to accept the demands of the US and strengthen its hand at the negotiating table. However, this could be a dangerous belief if it looks like the tariffs will be implemented and the market panics. President Trump is meeting with Industry representatives today, amid growing opposition from the international community.

The Reserve Bank of Australia has left Interest Rates on hold at 1.5% this morning. The Rate Statement mentioned that inflation was likely to remain low for some time. The risks are that household consumption remains a source of uncertainty and the appreciating exchange rate could slow economic activity and inflation. Markets had a mixed reaction, with AUDUSD first moving higher from 0.77777 to 0.77920 before reversing the move and dropping to 0.77684, suggesting that the outcome of the event was priced-in to a large extent. Retail Sales s.a. (MoM) (Jan) came in at 0.1% v an expected 0.4%, against -0.5% prior. AUDUSD initially moved higher on this data release from 0.77693 to 0.77845 before partially reversing to 0.77667 and settling around 0.77835 ahead of the Rate Decision.

Spanish Markit Services PMI (Feb) was 57.3 v an expected 56.4, from 56.9 previously. This was a welcome increase which beat market expectations.

German Markit Services PMI (Feb) came in as expected, unchanged at 55. Markit PMI Composite (Feb) was 57.6 v an expected 57.4, from 57.4 previously. EURUSD moved lower to find support at 1.27687 following this data release. This data was largely in line with expectations.

Eurozone Markit Services PMI (Feb) was 56.2 v an expected 56.7, from 56.7 previously. Markit PMI Composite (Feb) was 57.1 v an expected 57.5, from 57.5 previously. EURUSD moved high to settle around 1.23225 following this data. The Services PMI number released last month was the highest level reached since September 2007, which indicates the strong performance of the Eurozone economy’s services sector.

US Markit Services PMI (Feb) was 55.9 v an expected 54.6, from 55.9 previously. Markit PMI Composite (Feb) was 55.8 v an expected 55.5, from 55.9 previously. USDJPY moved lower from 105.895 to a low of 105.710 with the release of this data. This release provided a slight downward move as the data beat expectations, and, ultimately, could indicate an increase in inflation, which has prompted dollar weakness and equity market selling recently.

US ISM Non-Manufacturing PMI (Feb) was released at 59.5 v a consensus of 59.0 expected, against a prior reading of 59.9.

UK BRC Like-For-Like Retail Sales (YoY) (Feb) was 0.6% against an expected 0.4%, from 0.6% previously. The release, which was above expectations, saw GBPUSD move higher from 1.38303 to a high of 1.38470. This data point charts the change in the value of same-store sales.

EURUSD is unchanged overnight, trading around 1.23390.

USDJPY is largely unchanged in early session trading at around 106.228.

GBPUSD is down -0.11% this morning, trading around 1.38328.

Gold is up 0.17% in early morning trading at around $1,322.50.

WTI is up 0.06% this morning, trading around $62.58.

Major data releases for today:

At 08:15 GMT, Swiss Consumer Price Index (MoM) (Feb) is expected to be 0.2% from -0.1% previously. Consumer Price Index (YoY) (Feb) is expected to be 0.6% from 0.7% previously. This data could see moves in the CHF currency crosses. CPI data is a breakdown of the effect of inflation on consumer prices, which makes up a substantial portion of inflation overall. Increases in inflation can lead central banks to raise interest rates in an effort to contain the increase and reduce price pressure on consumers.

At 12:30 GMT, US Fed’s Dudley is scheduled to speak about the economic impact of the 2017 hurricanes at the United States Virgin Islands Non-profit Leaders Breakfast Roundtable, in St. Thomas, USVI. His comments, on this occasion, may have a limited effect on the market.

At 15:00 GMT, US Factory Orders (MoM) (Jan) is expected to be -1.3% from 1.7% previously. USD crosses could be moved by this data. If the expected decrease comes to pass, it represents a small drop, as the recent range of this data point over the last three years has been between +3% and -3.5%.

At 15:00 GMT, Canadian Ivey Purchasing Managers Index s.a.(Feb) data will be released, with a consensus of 56.3 expected, against a prior reading of 55.2. Ivey Purchasing Managers Index (Feb) will be released with a prior reading of 51.3. This data may cause the CAD pair to increase in volatility. Seasonally, this data has weakened at the beginning of each year since 2015 but it has remained in expansion above 50 since June of 2016. The softness in the data since reaching the high of 64.0 in November suggests that there is a slowing in demand in the Canadian economy.

At 18:15 GMT, UK MPC Member Haldane is due to speak at the Royal Society for the Encouragement of Arts, Manufactures, and Commerce, in London. Any comments made may affect GBP pairs.

At 21:35 GMT, Australian RBA Governor Phillip Lowe is due to deliver a speech titled “The Changing Nature of Investment” at the Australian Finance Review Business Summit, in Sydney. Audience questions are expected and comments made could affect the AUD.

At 22:30 GMT, US FOMC Member Brainard is due to deliver a speech titled “Economic and Monetary Policy Outlook” at New York University’s Money Marketeers event. Audience questions are expected and USD pairs could be moved by the answers and any comments made.

At 22:30 GMT, Australian AIG Performance of Construction Index (Feb) will be released, with a previous number of 54.3. This data point has remained in expansion above 50 since the March 2017 reading, in what is the longest period of growth over the last decade. The peak was reached in August 2017 at 60.6.