Sample Category Title

Currencies: Red Alert For USD

Sunrise Market Commentary

- Rates: Some consolidation ahead of the weekend?

Today’s eco calendar probably won’t impact trading, suggesting sentiment-driven and technical action. Underlying core bond sentiment remains negative and the comeback of stock/commodity markets adds to that picture. However, with the Bund and the US Note future entering oversold conditions, we’d argue in favour of some consolidation. - Currencies: Red alert for USD

Dollar weakness prevails this morning. USD/JPY dropped below key support (106.52). EUR/USD tests the 1.2537 cycle top. The trade-weighted dollar (DXY) tests the cycle low (88.43) which coincides with the 62% retracement level of the dollar’s 2014-2016 rally. Red alert for USD!

The Sunrise Headlines

- US stock markets closed with strong gains yesterday (+1.5%), marking a fifth straight positive day. Most Asian stock markets are closed for Lunar NY. Japan copies WS’s gains despite more yen strength.

- Japanese PM Abe nominated Kuroda to lead the BoJ for another 5y term, with the Cabinet forwarding the nomination to parliament. Central bank insider Amamiya and professor Wakatabe were tapped to be deputy governors.

- The US Senate failed to break its impasse over immigration after a week of debate as a flurry of unsuccessful votes left the chamber no closer to resolving the fate of hundreds of thousands of young, undocumented immigrants. (WSJ)

- Two thirds of supporters of Germany's SPD back forming a coalition government with Merkel's conservatives, an opinion poll showed, while 78% of supporters of the conservatives back the coalition.

- The RBA expects to make only gradual progress in reducing unemployment and having inflation return to its 2-3% target band, signalling interest rates will stay at record lows for a while yet.

- The UK is ready to lay out its post-Brexit plan for the financial sector, favoring an ambitious "mutual recognition" model, the FT reported.

- Today’s eco calendar contains UK retail sales, US building permits & housing starts and university of Michigan consumer confidence. ECB Coeuré is scheduled to speak.

Currencies: Red Alert For USD

Red alert for USD

The dollar remained under some downward pressure in Asia yesterday morning, but stabilized in Europe. Mixed US eco data had no impact. New US equity strength put the greenback again slightly in the defensive. EUR/USD closed the session at 1.2506. USD/JPY remains the biggest victim of dollar weakness with USD/JPY closing below the 62% retracement level of the mid 2016 to end 2016 rally (106.52). A confirmed break suggests complete retracement towards 99.02.

Positive risk sentiment and the dollar decline remain at play overnight. Several Asian markets are closed for the Lunar NY. Japanese stocks gain 1% despite a further decline of USD/JPY. The pair trades below 106 even if Japanese PM Abe confirmed Kuroda’s extension at the head of the BoJ. One of the newly appointed deputy governors is a proponent of QE and argued in favour of increasing asset purchases. Japanese FM Aso said that they are carefully watching FX moves and will act if needed. All yen-negative signals which the market currently ignores. Dollar weakness also translates in EUR/USD testing the 1.2537 cycle top this morning. The trade-weighted dollar (DXY) tests the cycle low (88.43) which coincides with the 62% retracement level of the dollar’s 2014-2016 rally. Red alert for USD!

The US eco calendar contains housing data and Michigan consumer confidence, but that won’t change the fortunes of the dollar. ECB Coeuré speaks. He wants to end APP in September 2018. Will he refer to current euro strength? The repositioning on equity markets and technical considerations are more important. Positive risk sentiment correlates with a further decline of the dollar. USD/JPY lost important support, while EUR/USD and DXY test key hurdles. A sustained break would signal more trouble for the dollar. We don’t see a fundamental reason for EUR/USD to already break this level, but this is not a good enough reason to row against the tide. The dollar is a falling knife.

EUR/GBP traded with a small negative bias yesterday, closing at 0.8858. UK retail sales are expected to rebound 0.6% M/M and 2.4% Y/Y after a sharp setback in January. We doubt that even better than expected data will be a big help for sterling. EUR/GBP holds the 0.8690/0.9033 range. We hold our view that the 0.8690 support won’t be easy to break without big progress on Brexit. UK PM May and German Chancellor Merkel hold Brexit talks in Berlin.

EUR/USD tests ST range top

GBP/JPY Daily Outlook

Daily Pivots: (S1) 148.99; (P) 149.58; (R1) 150.25; More...

With 151.19 minor resistance intact, deeper decline is expected for 146.96 support. Considering bearish divergence condition in daily MACD, firm break of 146.96 will be another sign of medium term trend reversal. On the upside, break of 151.19 will indicate short term bottoming and turn bias back to the upside for rebound.

In the bigger picture, as long as 146.96 key support holds, medium term outlook remains bullish. Rise from 122.36 is in favor to extend to 61.8% retracement of 195.86 to 122.36 at 167.78. However, break of 146.96 support will indicate trend reversal after rejection by 55 month EMA. In that case, deeper fall would be seen to 38.2% retracement of 122.36 to 156.59 at 143.51 and then 61.8% retracement at 135.43.

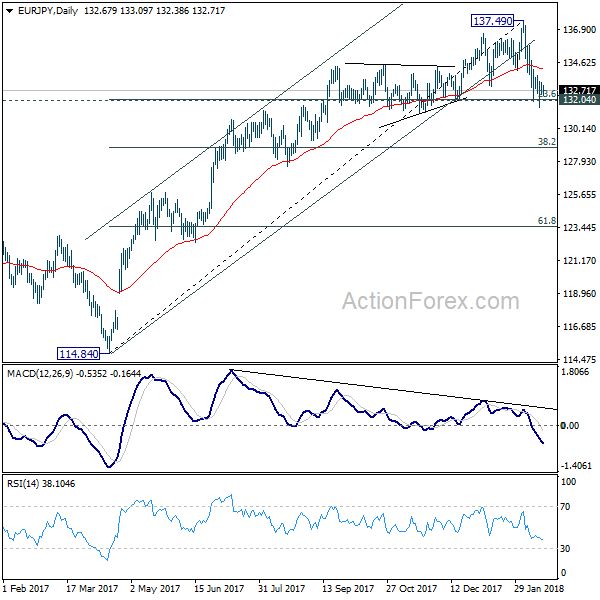

EUR/JPY Daily Outlook

Daily Pivots: (S1) 132.41; (P) 132.84; (R1) 133.18; More....

At this point, EUR/JPY cannot sustain below 132.04 cluster support (23.6% retracement of 114.84 to 137.49 at 132.14) yet. Intraday bias remains neutral first. Deeper fall is still expected with 134.16 resistance intact. Decisive break of 132.04/14 will indicate larger trend reversal on bearish divergence condition in daily MACD. In such case, outlook will be turned bearish for 38.2% retracement at 128.38 first. Nonetheless, rebound from 132.04 will retain near term bullishness. Break of 134.16 minor resistance will bring retest of 137.49 high instead.

In the bigger picture, bearish divergence condition in week EMA indicates lost up medium term up trend momentum. But there is no clear sign of completion of up trend from 109.03 yet. Break of 137.49 will target 141.04/149.76 resistance zone. However, sustained break of 132.04 will be the early sign of long term reversal and should bring deeper fall back to retest 124.08 key support level.

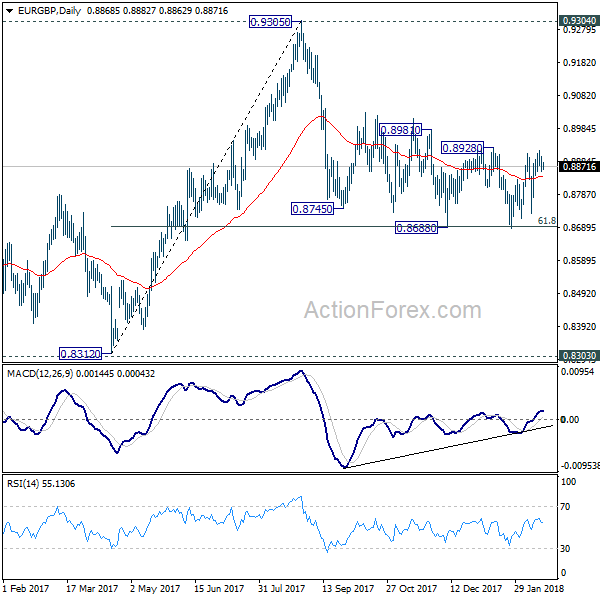

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8850; (P) 0.8876; (R1) 0.8894; More...

Range trading continues in EUR/GBP, inside 0.8686/8928. Intraday bias remains neutral. Near term outlook will remain mildly bearish as long as 0.8928 resistance holds. On the downside, firm break of 0.8686 will resume whole decline from 0.9305. As 61.8% retracement of 0.8312 to 0.9305 should then be taken out too. Deeper decline would be seen to retest 0.8303/8312 support zone. Nonetheless, on the upside, break of 0.8928 will indicate near term reversal and turn outlook bullish for 0.9304 resistance.

In the bigger picture, there are various ways to interpret price actions from 0.9304 high. But after all, firm break of 0.9304/5 is needed to confirm up trend resumption. Otherwise, range trading will continue with risk of deeper fall. And in that case, EUR/GBP could have a retest on 0.8303. But we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside.

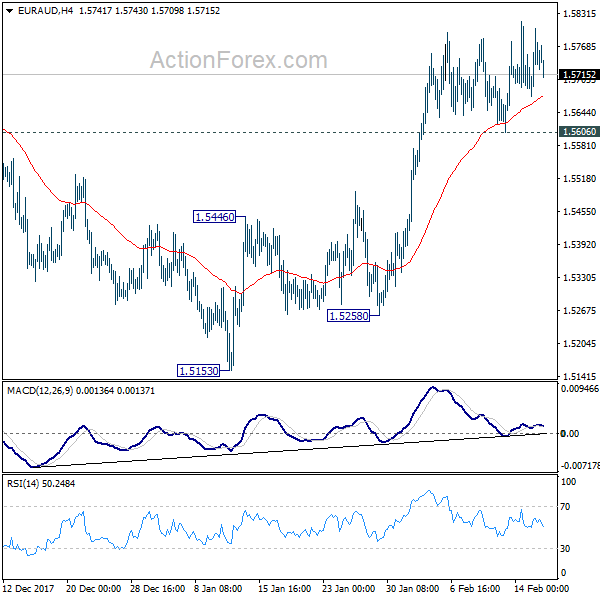

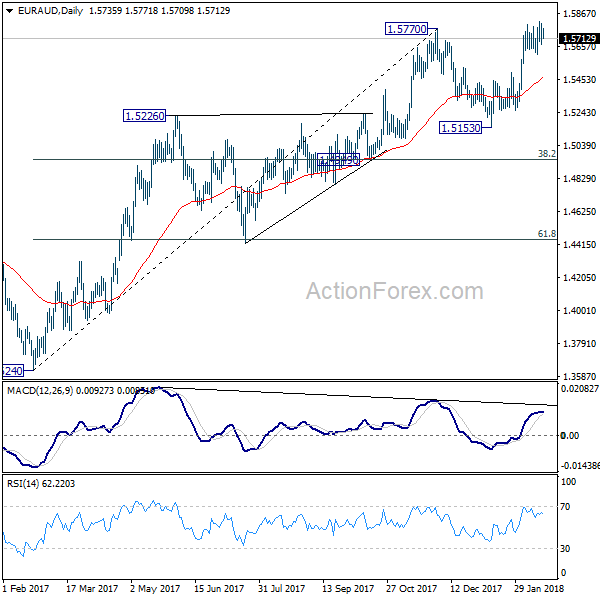

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.5674; (P) 1.5739; (R1) 1.5803; More....

No change in EUR/AUD's outlook even though upside momentum is very unconvincing. As long as 1.5606 support holds, further rally is expected. Sustained break of 1.5770 resistance will confirm resumption of medium term rise from 1.3264. In that case, EUR/AUD should target 1.6587 key long term resistance. However, below 1.5606 minor support minor support will dampen this bullish case and turn bias to the downside.

In the bigger picture, medium term rise from 1.3624 is not completed yet. Break of 1.5770 will extend the rise to retest 1.6587 (2015 high). However, considering bearish divergence condition in daily MACD, sustained break of 1.4949 cluster support (38.2% retracement of 1.3624 to 1.5770 at 1.4950) will indicate medium term reversal. And there is prospect of retesting 1.3624 low in that bearish case.

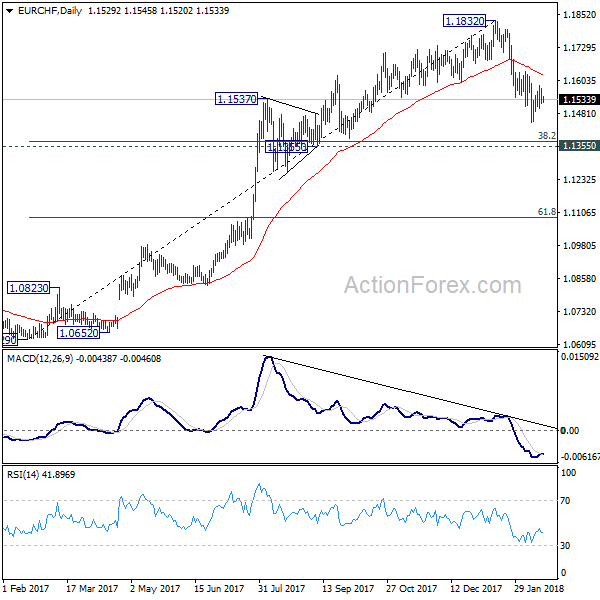

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.1508; (P) 1.1540; (R1) 1.1561; More...

EUR/CHF is still bounded in the consolidation from 1.1445 and intraday bias remains neutral. With 1.1639 resistance intact, outlook remains bearish and further decline is expected. Below 1.1445 will extend the corrective fall from 1.1832 to 1.1355 cluster support (38.2% retracement of 1.0629 to 1.1832 at 1.1372.) At this point, we'd expect strong support from there to contain downside and bring rebound.

In the bigger picture, a medium term top should be in place at 1.1832 on bearish divergence condition in daily MACD. But there is no indication of long term reversal yet. As long as 1.1198 resistance turned support holds, we'd still expect another rise through prior SNB imposed floor at 1.2000.

Bank Of Japan Re-Appoint Governor Kuroda As USDJPY Breaks 106.000

There was reduced liquidity in the Asian session due to the observance of the Chinese New Year festivities. However, there was still business to be attended to as the Bank of Japan re-appointed Governor Kuroda for a second term at the helm. There were also two deputy governors nominated: Amamiya is the current Bank of Japan Executive Director and Masazumi Wakatabe is a university academic. Both are quite dovish in their outlook so the current monetary policy is unlikely to change. The subsequent move lower in USDJPY drove price under the 106.000 level to hit a low of 105.545. Japanese Finance Minister Aso made the comment that the Yen's strength was not enough to require intervention.

ECB's Lautenschlager spoke yesterday, making the following comments: That there might be a need for more macroprudential policy, meaning a tightening of existing borrower-based measures. The toolbox defined by the EU legal framework may be too small to address all types of systemic risk. Stability risks are not too pronounced for now.

US Continuing Jobless Claims (Feb 2) were 1.942M v an expected 1.925M, from a previous number of 1.923M, which was revised up to 1.927M. Initial Jobless Claims (Feb 9) were as expected at 230K, from a prior reading of 221K, which was revised up to 223K. Philadelphia Fed Manufacturing Survey (Feb) was 25.8 v an expected 21.1, from a prior 22.2. EURUSD moved higher from 1.24619 to 1.24867 after this data release.

US Industrial Production (MoM) (Jan) was released coming in at -0.1%. The consensus was for 0.2%, from 0.9% previously, which was revised down to 0.4%. Capacity Utilization (Jan) was also released at this time, coming in at 77.5% with an expectation for 78.0%, from 77.9% prior, which was revised down to 77.7%.

US NAHB Housing Market Index (Feb) was released, with the value remaining unchanged, as expected, at 72. EURUSD dropped from 1.25054 to 1.24739.

Canadian BOC Governing Council Member Schembri spoke at the Manitoba Association for Business Economics in Winnipeg. Some of the comments made were: Subdued growth may change how central banks react. Higher debt levels, a decline in interest rates and decreasing economic growth could challenge policy framework. If cyclical forces coming out of a downtrend are less powerful than historically because of demographics and debt, central banks might have to be more aggressive. BOC's 2% target is symmetric. Negative policy rates in some jurisdictions appear to be less effective in stimulating economic growth.

New Zealand Business NZ PMI (Jan) was released coming in at 55.6. The prior number was 51.2.

Australian RBA Governor Lowe testified before the House of Representatives' Standing Committee on Economics in Sydney. Some of the comments were: it is more likely the next interest rate move will be up. Improvement in the global economy has continued. The labour market is noticeably stronger than the RBA had expected. The strength of consumer spending remains uncertain. There will be slow growth in household incomes for some time yet. Less monetary stimulus will be appropriate at some point. The outlook for US budget deficits is very problematic and the RBA would not want tax cuts in Australia to lead to higher deficits.

Foreign Investment in Japan stocks (Feb 9) was ¥-429.5B from a previous number of ¥-125.6B, which was revised down from ¥-126.7B. Foreign Bond Investment (Feb 9) was ¥-973.2B from a prior number of ¥-866.6B, which was revised up from ¥-864.9B. USDJPY moved down from 106.408 to 106.051 after this data was published.

EURUSD is up 0.24% overnight, trading around 1.25361.

USDJPY is down -0.37% in early session trading at around 105.731.

GBPUSD is up 0.21% to trade around 1.41292.

AUDUSD is up 0.40% overnight, trading around 0.79740.

Gold is up 0.32% in early morning trading at around $1,357.50.

WTI is up 0.07% this morning, trading around $61.35.

Major data releases for today:

At 07:00 GMT, Wholesale Price Index (MoM) (Jan) is expected to be 0.2% from -0.3% previously. Wholesale Price Index (YoY) (Jan) was 1.8% previously. EUR pairs could have positions opened or closed due to this data.

At 08:20 GMT, ECB's Coeure will speak and this may impact on moves in EUR crosses.

At 09:30 GMT, UK Retail Sales (YoY) (Jan) is expected to be 2.6% from 1.4% previously. Retail Sales (MoM) (Jan) is expected at 0.5% from a prior -1.5%. Retail Sales Ex-Fuel (YoY) (Jan) is expected to be 2.5% from 1.3% previously. Retail Sales Ex-Fuel (MoM) (Jan) is expected at 0.6% from a prior -1.6%. GBP crosses could experience an increase in volatility following this data release.

At 13:30 GMT, US Housing Starts (MoM) (Jan) is expected at 1.234M from a previous number of 1.192M. Building Permits (MoM) (Jan) is expected to come in at 1.300M from a prior reading of 1.302M. Housing Starts Change (Jan) is expected at 3.4% from a previous number of -8.2%. Building Permits Change (Jan) is expected to come in at 3.5% with a prior reading of -0.1%. USD crosses could see increased volatility around this data release.

At 18.00 GMT, Baker Hughes US Oil Rig Counts will be released, with a headline number from last week of 791. WTI Oil can become volatile around this data release and will be in traders' minds when trading resumes on Monday.

US CPI Data On Wednesday

Market movers today

Today we get a number of tier two data releases. In the US, the release of import prices in January is likely to attract at least some attention given the focus on 'reflation' in the markets.

Also in the US, we get housing data for January as well as preliminary consumer confidence indicator from University of Michigan.

In the UK, retail sales in January are due out today. The markets sometimes move on the number, although it is a poor indicator for actual private consumption growth.

In Sweden, governor Ingves' has cancelled his speech due to influenza.

Selected market news

After the US CPI data on Wednesday, equity indices continued the risk-on sentiment yesterday, with Eurostoxx 50 up 0.6% and S&P 500 up 0.9%. 10Y treasury yields were slightly lower on the day at 2.89%, while European bond yields were marginally higher. Overnight, Japanese equities rose 1%, with many markets closed for the Chinese New Year. The ZAR traded around its strongest level in almost three years following the resignation of Zuma. More here

The awaited speech by Norway's central bank governor Olsen yesterday evening did not contain news and gave only the high-level/broad picture.

Oil prices have rebounded significantly in the past days with the price of Brent crude recovering to USD65/bbl level. The main culprit has been the steep drop-back in USD and positive turnaround in risk sentiment. The weekly EIA report on Wednesday did not offer much for the market to trade on. In the short-term, we look for oil prices to mirror development in risk sentiment and USD.

The confidence indicators released in the US yesterday showed a mixed picture. The Empire manufacturing declined to 13.1 from 17.7, while Philly rose to 25.8 from 22.2. The Empire details show that they are stronger than the headline (recall that the headline is an index in itself, not calculated as a weighted sum of other components). Employment rose to 10.9 from 3.8, inventories declined, new orders slightly up. Prices paid rose significantly from 36.2 to 48.6 (highest in nearly six year).

Yesterday, the European Parliament stated that they found 'The majority of the political groups considered Governor Lane's performance more convincing. Some groups expressed reservations for Minister De Guindos appointment', after an informal hearing by the candidates to replace ECB vice-president Constancio in June this year. Next important step in the process is on Monday when the Eurogroup will decide on which candidate to recommend.

Daily Wave Analysis: EUR/USD Bullish Price Action Breaks Above 1.25 Resistance Zone

Currency pair EUR/USD

The EUR/USD broke above the top and resistance zone at 1.25 (red), which is confirming an uptrend continuation. The uptrend could complete a wave 5 (purple) of a wave 3 (pink), which could leave space for one more potential wave 4 and 5 (pink).

The EUR/USD made a bullish break above the resistance trend line (dotted red) and is close to hitting the 161.8% Fib target. The broken resistance zone at 1.25-1.2525 could now become a support zone.

Currency pair GBP/USD

The GBP/USD is now testing a new resistance trend line (red).The bullish price action is showing decent momentum and could indicate a likely chance of continuation once price breaks above resistance.

The GBP/USD is probably in a bullish wave 3 (blue) at the moment.

Currency pair USD/JPY

The USD/JPYbreakout broke below the -27.2% Fibonacci target is continuing towards the next target at the-61.8% Fib near 105.

The USD/JPY indeed made a retracement towards the top of the falling wedge pattern before continuing lower and breaking below the -27.2% Fib target.

AUD Trading On A Stronger Footing In The Morning Session

For the 24 hours to 23:00 GMT, the AUD rose 0.14% against the USD and closed at 0.7941.

LME Copper prices rose 1.95% or $136.0/MT to $7098.0/MT. Aluminium prices rose 1.22% or $26.0/MT to $2164.0/MT.

In the Asian session, at GMT0400, the pair is trading at 0.7958, with the AUD trading 0.21% higher against the USD from yesterday’s close.

Overnight, the Reserve Bank of Australia (RBA) Governor, Philip Lowe warned that any move to lower the corporate tax rate should not increase budget deficits. Additionally, he stated that the RBA aims for further reduction in the unemployment rate and an increase in inflation towards the mid-point of the target range and expects to keep interest rates at record lows for a while yet.

The pair is expected to find support at 0.7911, and a fall through could take it to the next support level of 0.7864. The pair is expected to find its first resistance at 0.7986, and a rise through could take it to the next resistance level of 0.8014.

The currency pair is trading above its 20 Hr and 50 Hr moving average.