Sample Category Title

Elliott Wave View: USDJPY Calling For More Downside

USDJPY Short-term Elliott Wave view suggests that the rally to 110.48 high ended Intermediate wave (4) bounce on February 02.2018 peak. Below from there, the decline is unfolding as an Ending Diagonal Structure within Intermediate wave (5) lower. Where Minor wave 1 ended at 108.44 low as Zigzag structure, Minor wave 2 bounce ended at 109.77 in a Double three correction. Currently, Minor wave 3 remain in progress in a Double three correction, where internals of each leg is unfolding as Elliott Wave Zigzag pattern.

Where Minutte wave ((w)) ended at 108.03 low, Minute wave ((x)) ended at 108.87. Below from there Minute ((y)) of wave 3 remains in progress as zigzag structure. When Minutte wave (a) ended in 5 waves at 107.39 low and Minutte wave (b) ended at 107.89. Near-term cycle from 2/08 high (109.77) is mature already in Minor wave 3 lower after reaching blue box area (as shown on Chart). And pair can now start the Minor wave 4 bounce anytime soon in 3, 7 or 11 swings. However within the shorter-term cycles pair could extend lower towards 106.39-105.47 100%-161.8% Fibonacci extension area of (a)-(b) within ((y)) of 3 lower before a bounce in Minor wave 4 takes place. We don’t like buying the pair and as far as a pivot from 2/08 high 109.77 holds the wave 4 bounce should get rejected in 3, 7 or 11 swings for further downside extension in Minor 5 of (5) lower.

USDJPY 1 Hour Elliott Wave Chart

GBPUSD Looking For Gains Above 1.3892 Pivot

The British pound continues to hold above the key 1.3892 pivot level against the U.S dollar, although buyers remain cautious ahead of today’s key CPI inflation release from the American economy. The GBPUSD pair currently trades around the 1.3900 handle, although buyers again failed to take-out Tuesday’s high overnight, with price failing around the 1.3320 level. Going forward, sterling traders look to ongoing weakness in the U.S dollar index and a clear breakout from the current 1.3292 to 1.3320 price-range.

The GBPUSD pair remains intraday bullish whilst clearly trading above the 1.3892 level, further buying towards the 1.3939 and 1.4000 levels still seems possible.

Should GBPUSD price-action slip back below the 1.3892 level for an extended period, we may see sellers test back towards the 1.3855 and 1.3832 levels.

EURUSD Intraday Bullish ABove 1.2332 Level

The euro has continued to press higher against the U.S dollar overnight, hitting 1.2392, as broad-based weakness in the greenback persists. The EURUSD currently trades around the 1.2370 region, with bullish intraday momentum largely intact whilst the pair trades well above the 1.2332 technical support level. Traders now look to a slew of economic data this morning, with key German January CPI Inflation figures and fourth fiscal quarter Gross Domestic Product numbers from the eurozone.

The EURUSD pair remains intraday bullish whilst trading above the 1.2332 level, further upside towards 1.2400 and 1.2432 seems likely.

Should EURUSD price-action slip back below the 1.2332 level, we may see sellers start to target the1.2290 and 1.2255 support levels.

All Eyes On US CPI Data

US economic data will make headlines on Wednesday, as investors assess the latest inflation and retail sales trends for the world's largest economy.

The economic calendar picks up at 07:00 GMT with reports on German consumer inflation and fourth quarter GDP. Inflation in Europe's largest economy is forecast to fall 0.7% in January, resulting in a year-over-year gain of 1.6%. Germany's economic expansion is also expected to slow to 0.4% in the December quarter, down from 0.8% in Q3.

The Italian and Portuguese governments will also report Q4 GDP numbers throughout the day, leading to the official Eurozone figures at 10:00 GMT. The euro area economy likely expanded 0.6% quarter-on-quarter and 2.7% annually, based on a median forecast.

Shifting gears to North America, the US government will report on CPI inflation and retail sales at 13:30 GMT. Consumer inflation is forecast to slow to an annualized rate of 1.9% in January, down from 2.1% the previous quarter. Meanwhile, retail receipts are expected to climb 0.2%.

The inflation report will be closely watched by market participants looking to make sense of the latest selloff in US stocks. The market's precipitous drop was triggered by a nonfarm payroll report on 2 February that showed an unexpected surge in average hourly earnings. The sharp rise in earnings was perhaps the clearest signal yet that inflationary pressures were building, which may compel the Federal Reserve to raise interest rates faster than previously expected.

Earlier in the day, Japan reported a much smaller than expected rise in fourth quarter GDP, as the world's third-largest economy expanded just 0.5% in October-December. Analysts in a median estimate called for a gain of 0.9% Despite the miss, Japan's economy has been in acceleration mode for eight straight quarters, the longest streak in 28 years.

EUR/USD

Europe's common currency has been regaining momentum this week, as the dollar continues to backtrack against world peers. The EUR/USD exchange rate climbed 0.3% at the start of Wednesday trading to reach 1.2382. Since bottoming at multi-week lows Friday, the EUR/USD has gained roughly 150 pips.

GBP/USD

Cable is also finding its footing again after a week of declines through Friday. The GBP/USD rose 0.2% on Wednesday to 1.3915. The bulls appear to be regaining control of the market but will need to clear multiple hurdles to new highs. The first major resistance test is likely found at the psychological 1.4000 level.

USD/JPY

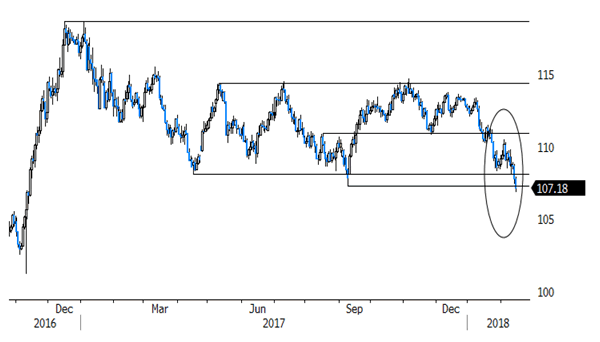

Japan's GDP miss wasn't enough to spark a rally in the USD/JPY, which extended losses on Wednesday. The pair fell 0.5% to 107.30, its lowest since 2014. The sharp downside exposes the USD/JPY to more losses. The pair is currently testing a key support level; another breakdown would likely lead to a test of the 106.80 region.

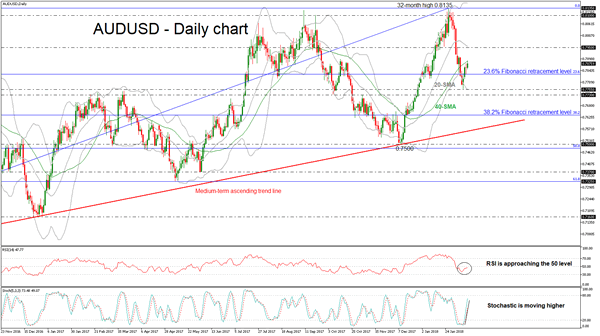

AUDUSD Bearish Correction Pauses, Further Gains Are Expected

AUDUSD has reversed back up again after finding support at the 0.7755 barrier, near the lower Bollinger Band. The price climbed above the 23.6% Fibonacci retracement level at 0.7826 of the up-leg with the low of 0.6820 and the high of 0.8100 in the medium-term timeframe.

Moreover, the downside pressure seems to be weakening, while the technical indicators are endorsing the bullish scenario. From the technical point of view, in the short-term timeframe, the RSI indicator is approaching the positive territory and is pointing north, while the stochastic oscillator is moving sharply higher slightly below the overbought zone. Also, the price has just hit the 40-day SMA near 0.7890.

Further gains could see the 0.7950 resistance barrier, which overlaps with the 20-day simple moving average. A jump above the aforementioned obstacle could reinforce the bullish structure in the short-term and open the way towards the next key resistance of 32-month high at 0.8135.

In the event of a downside reversal again, the 0.7730 – 0.7755 area could act as a critical barrier before being able to re-challenge the 38.2% Fibonacci mark around the 0.7635 level.

It is worth mentioning that AUDUSD has been developing within an ascending move since January 2016 and tested several times the diagonal line without slipping below it.

Currencies: USD/JPY Drops Below Key 107.32 Support!

Sunrise Market Commentary

- Rates: Core bond consolidate higher; more gains after US CPI?

Core bonds continue consolidating higher in a fragile risk sentiment. Today's eco calendar heats up with US CPI and retail sales. A below or at consensus inflation figure argues in favour of a continuation of the short term correction higher. As long as risk sentiment remains vulnerable, it's even doubtful that core bond sellers will already return on higher CPI readings. - Currencies: USD/JPY drops below 107.32 neckline

A sharp decline of USD/JPY kept the dollar under pressure yesterday across the board. This trend continues this morning. USD/JPY dropped below the key 107.32 support. Later today, the focus of FX trading turns the US January inflation data. The dollar probably needs a figure above consensus to change sentiment for the better.

The Sunrise Headlines

- US equities managed to recover some more ground despite the worrying rise of the Japanese yen. USD/JPY hits the lowest level since end 2016 this morning. Asian bourses are mixed with China outperforming ahead of Lunar NY.

- Cleveland Mester is being considered for the central bank's vice chair post, sources said. Mester is known for her mildly hawkish views on monetary policy. SF Fed Williams and Mohamed El-Erian have also been considered.

- The Japanese economy grew less than forecast in Q4 (0.1% Q/Q vs 0.2% Q/Q)., but both consumption (0.5% Q/Q) and investments (0.7% Q/Q) contributed positively. The current Japanese expansion is the longest since the 80s boom.

- German SPD leader Schulz resigned, hoping to end turbulence that has rocked the centre-left party since it agreed a coalition deal with Chancellor Merkel's conservatives.

- NZD/USD hit a one-week high this morning above 0.73 after a quarterly central bank survey showed that 2-yr inflation expectations rebounded from 2.02% to 2.11%.

- Israeli police recommended charging PM Netanyahu with bribery, fraud and breach of trust in two separate cases, a decision that could spark the biggest fight of his political life.

- Today's eco calendar contains US CPI inflation and retail sales. The Swedish Rikskbank is expected to keep its interest rate unchanged at -0.5%. EMU industrial production and the second reading of Q4 GDP will also be released.

Currencies: USD/JPY Drops Below Key 107.32 Support!

USD/JPY drops below key 107.32 support!

USD weakness prevailed yesterday, driven by a sharp USD/JPY decline. The pair dropped from the 108.75 area to fill bids below 107.50 before European noon. The USD/JPY decline weighed also on other USD cross rates. EUR/USD trended higher in the 1.23 figure. We didn't see a clear trigger for this yendriven repositioning, but it created uncertainty on European equity markets. The USD decline slowed after a strong US NFIB confidence and ‘hawkish' comments from Fed's Mester (no impact yet from recent turmoil), but USD sentiment remained weak. EUR/USD closed at 1.2352. USD/JPY finished at 107.82.

Overnight, most Asian equities indices are in positive territory in line with WS. Several markets are heading for a holiday period (Lunar New Year) starting tomorrow. Japan underperforms as the rise of the yen continues. USD/JPY dropped below the 107.32 support, reaching the lowest level since November 2016. Japan Q1 GDP was soft (0.5% Q/Qa), but domestic spending OK. For now, there are few comments from Japanese officials on the rise of the yen. The USD/JPY slide still weighs on other USD cross rates. EUR/USD trades in the 1.2375 area. EUR/JPY is nearing the key 132/131 support area.

Today, Q1 GDP releases in Germany, Italy and EMU are interesting, but the focus for global trading will be on the US CPI, and to a lesser extent US retail sales. Headline CPI is expected to ease from 2.1% Y/Y to 1.9% (core from 1.8% to 1.7%). The dollar probably needs above consensus inflation to change fortunes for the better. We also keep an eye at the strange combination of yen-strength and at the same time relative equity resilience (in Asia ex-Japan and in the US). How long will this pattern persist? Technically, EUR/USD consolidates between 1.2165 and 1.2537. The pair dropped below 1.2323/35 support but followthrough price action was modest. Next support at 1.2165 looks far away for now. We assume that current USD weakness won't push EUR/USD beyond the 1.2537 top yet.

UK CPI printed slightly above consensus yesterday (headline 3.0%), but didn't help sterling. The report won't change the BoE's rate hike path. After a brief dip, EUR/GBP returned to the 0.89 area. Today, there are no UK eco data. EUR/GBP is trending higher in the 0.8690/0.9033 range, with intermediate resistance at 0.8930. We hold our view that the 0.8690 support won't be easy to break without big progress on Brexit.

USD/JPY drops below107.32 neckline, a warning signal

All Eyes On U.S. Inflation Figures

After wiping off more than $5 trillion in market cap past week and volatility hitting the roof, global equities are finally showing signs of stabilization. U.S. stocks continued to recover from the correction levels on Tuesday with main indices posting a three-day winning streak. Confidence was restored yesterday, after the new Fed Chair Jerome Powell declared that the central bank would keep watching for financial stability risks. Meanwhile, Asian equities were mixed today with shares rising in Hong Kong and Seoul but falling in Japan due to strengthening Yen.

The rising Yen is impressive, especially that we have not seen a run to haven assets. USDJPY hit 106.85 earlier today, a level last seen in November 2016. This came after Japan’s GDP showed economic expansion slowed in the final quarter of 2017, reporting a 0.5% annualized growth from 2.2% in the past quarter. I don’t think these figures justify a stronger Yen. After all, the Japanese economy has recorded its longest expansion streak in almost three decades, and despite the slowdown, consumption is now contributing a significant portion to growth, which is good news.

The BoJ will probably need to remind investors that the central bank is still far from reaching its inflation target, and thus it’s too early to begin unwinding monetary policy. Today’s comments from Japan’s Chief Cabinet Secretary that stable currency moves were extremely important, failed to drag the Yen, but as we approach 105, I think verbal interventions will become more aggressive.

All eyes on U.S. inflation figures

The U.S. inflation figures release is the key event of the week, if not the month. Investors’ fear of inflation which triggered the global selloff will be tested again today.

Inflation expectations have risen to highest levels since 2014 after U.S. jobs report showed wage growth accelerated at its strongest pace since 2009. While many economists agree that the phase of low prices is behind us, there’s some anxiety that prices might appreciate at a faster pace than previously anticipated.

Economists expect the annual coreCPI has eased to 1.7% in January from 1.8% in December and the headline figure also to decline by 0.2% to 1.9%. If we didn’t see any surprise on this front, markets should relax, stocks will likely spike higher, and the U.S. dollar is likely to give up on recent gains. However, any surprise to the upside, particularly on the Core inflation, will prove economists wrong and lead to higher bond yields and further selloff in equities.

All Focus On US Inflation Data As USD Weakens

The USD has weakened further overnight as the market awaits important US Data at 13:30 GMT. USDJPY broke down under 107.000, while GBPUSD made another attempt to stay above 1.39000. EURUSD advanced to 1.23900, while Gold followed suit to reach a high at 1336.80. The US CPI data later is expected to point to an Inflation figure that maintains the path of rate increases being travelled by the US Fed. Any surprise in the number can spark an increase in volatility comparable to the last week and a half of trading. If the number is a dud, the market can become indecisive and may attempt to test support and resistance before a direction is found. Any trend currently being traded may be altered by the market reaction to the data release.

Bank of Japan Governor Kuroda spoke in parliament saying: Cryptocurrencies are mostly used for speculative investing and should be called crypto assets. Cryptocurrencies like bitcoin are not seen as currencies. Japanese economic fundamentals, company profits are strong. The risk-off sentiment in the US led to stock falls and the BOJ will continue to closely monitor developments in markets because financial market moves can have an impact on the real economy. Japan's economy needs the BOJ to continue current policy. The Bank of Japan is still a long way from price target. Japan's economy needs persistent monetary easing.

UK Consumer Price Index (YoY) (Jan) was out at 3.0% v an expected 2.9%, from 3.0% previously. Core Consumer Price Index (YoY) (Jan) was 2.7% v an expected 2.6%, from 2.5% prior. Consumer Price Index (MoM) (Jan) was -0.5% v an expected -0.6%, from 0.4% prior. Producer Price Index – Output (MoM) n.s.a. (Jan) was 0.1% v an expected 0.2%, from 0.4% previously. Producer Price Index – Output (YoY) n.s.a. (Jan) was 2.8% v an expected 3.0%, from 3.3% previously. Producer Price Index – Input (MoM) n.s.a. (Jan) was as expected at 0.7%, from 0.6% previously, which was revised up from 0.1%. Producer Price Index – Input (YoY) n.s.a. (Jan) was 4.7% v an expected 4.2%, from 4.9% previously, which was revised up to 5.4%. PPI Core Output (MoM) n.s.a. (Jan) was as expected at 0.3%, from 0.3% previously, which was revised down to 0.2%. PPI Core Output (YoY) n.s.a. (Jan) was 2.2% v an expected 2.3%, from 2.5% previously, which was revised down to 2.4%. Retail Price Index (MoM) (Jan) was -0.8% v an expected -0.7%, from 0.8% previously. Retail Price Index (YoY) (Jan) was 4.0% v an expected 4.1%, from 4.1% prior. GBP crosses experienced movment upon the release of this data.

At 13:00 GMT, US FOMC Member Mester spoke about the economic outlook and monetary policy at the Dayton Area Chamber of Commerce Government Affairs Breakfast. Audience questions followed and some of the comments made were: Inflation to gradually rise to 2% over next 1-2 years and further rate hikes needed this year and next. US economic fundamentals are very strong and Mester sees economy working through latest turmoil. Latest market moves haven't curbed risk-taking or spending, and trading has been relatively orderly. Tax cuts adding to growth and could be upside risk. GBPUSD sold off from 1.38969 to 1.38519 after the comments.

Australian Westpac Consumer Confidence (Feb) was released coming in at -2.3%, the prior number was 1.8%. AUDUSD moved up to 0.78686 but sold off to 0.78532 after the release, eventually erasing the move and reaching 0.78890.

RBNZ Inflation Expectations (QoQ) (Q4) were released, coming in at 2.1% from a prior reading of 2.0%.

EURUSD is up 0.20% overnight, trading around 1.23750.

USDJPY is down -0.60% in early session trading at around 107.161.

GBPUSD is up 0.08% to trade around 1.39021.

AUDUSD is up 0.20% overnight, trading around 0.78746.

Gold is up 0.37% in early morning trading at around $1,334.40.

WTI is up 0.29% this morning, trading around $59.05.

Major data releases for today:

At 07:00 GMT, German Harmonised Index of Consumer Prices (YoY) (Jan) will be released. The consensus is for an unchanged value of 1.4%. Gross Domestic Product (QoQ) (Q4) is expected to be 0.6% from 0.8% previously. Gross Domestic Product (YoY) (Q4) is expected to be 2.2% from 2.3% previously. EUR pairs could have positions opened or closed due to this data.

At 08:00 GMT, German Bundesbank President Weidmann is due to deliver opening remarks at the Bundesbank Cash Symposium, in Frankfurt. EUR pairs may be moved by his comments.

At 08:50 GMT, SNB Governing Board Member Zurbrugg will deliver a speech titled 'Cash – a means of payment yesterday, today, and tomorrow' at the Bundesbank Cash Symposium in Frankfurt. His comments could move CHF crosses.

At 09:00 GMT, Italian Gross Domestic Product (QoQ) (Q4) is expected to be 1.6% from 1.7% previously. Gross Domestic Product (YoY) (Q4) is expected to be unchanged at 0.4%. EUR pairs could be moved by this data.

At 10:00 GMT, Eurozone Gross Domestic Product (QoQ) (Q4) is expected to be unchanged at 0.6%. Gross Domestic Product (YoY) (Q4) is expected to be 2.7% from 2.6% previously. Industrial Production w.d.a. (YoY) (Dec) will be released with a consensus number coming in at 4.2% and a prior of 3.2%. Industrial Production s.a. (MoM) (Dec) is expected at 0.2% from 1.0% previously. The EUR could be moved by this data.

At 11:20 GMT, SNB Governing Board Member Zurbrugg will take part in a panel discussion at the Bundesbank Cash Symposium in Frankfurt. His comments can move CHF crosses.

At 12:45 GMT, ECB's Mersch will speak and this may impact EUR crosses.

At 13:30 GMT, US Retail Sales (MoM) (Jan) will be released with an expected 0.2% from 0.4% previously. Retail Sales ex Autos (MoM) (Jan) is expected to be unchanged at 0.4%. Retail Sales Control Group (Jan) is expected at 0.4% from 0.3% prior. Consumer Price Index (MoM) (Jan) is expected at 0.3% from 0.1% previously, which was revised up to 0.2%. Consumer Price Index (YoY) (Jan) is expected at 1.9% from 2.1% previously. Consumer Price Index Ex Food & Energy (YoY) (Jan) is expected to be 1.7% from 1.8% prior. Consumer Price Index Ex Food & Energy (MoM) (Jan) is expected to be 0.2% from 0.3% previously, which was revised down to 0.2%. USD crosses could see increased volatility around this data release.

At 23:50 GMT, Japanese Machinery Orders (YoY) (Dec) will be released with a consensus of 2.2% expected from 4.1% prior. Machinery Orders (MoM) (Dec) will be released with a consensus of -2.3% expected, from 5.7% previously. JPY pairs could see an increase in price movement after this data.

Daily Wave Analysis: EUR/USD Develops Bullish Momentum And Wave 3 Pattern

Currency pair EUR/USD

The EUR/USD bullish breakout is continuing with momentum towards the previous top and next resistance trend line (red). A break above that could confirm a full uptrend continuation within wave 5 (purple).

The EUR/USD bullish breakout above the resistance levels and fractals of wave 4 (orange) is indeed acting as a wave 3 (blue) so far with price going above the 161.8% Fibonacci target. Price could make a retracement but if price uses the support zone (purple lines) as a bouncing spot, then price could see another potential rally towards the resistance and Fib targets.

Currency pair GBP/USD

The GBP/USD seems to be respecting the Fibonacci levels of wave 4 vs 3 (green) and a bullish breakout above the previous tops (dotted orange) indicate the start of wave 5 (green). A break above the next resistance (red) trend line could confirm a bullish breakout.

The GBP/USD broke above resistance (dotted orange) and completed wave C (grey). The next bullish breakout could confirm a wave 3 (blue) pattern.

Currency pair USD/JPY

The USD/JPY broke below the strong supportzone (dotted green). The break below this support zone invalidates the previous wave pattern and indicatesa bearish continuation within waveB (red).

The USD/JPYcould pullback to the broken support (dotted green) and use the same levels as potential resistance.

Asian Stocks Are Retreating After Two Days Of Trading Higher

Market movers today

After a few quiet days in terms of data releases, today is more interesting, not least Sweden, where Prospera inflation expectations are due at 08:00 CET, Valueguard house prices at 09:00 and the Riksbank rate decision at 09:30 (see page 2).

In the US, we estimate CPI core index rose 0.2% m/m in January, implying a fall in CPI core inflation to 1.7% y/y from 1.8%. Retail sales data is also due out today.

At 11:00, the second release of euro area Q4 GDP growth figures is due out, where will we for the first time get details of the GDP components. We expect the first estimate of 0.6% q/q growth to be confirmed.

In Denmark, we will get the GDP indicator for Q4, which we expect to show that growth rebounded to 1.0% q/q after the surprise fall of 0.5% in Q3 (see page 2).

Selected market news

Asian stocks are retreating after two days of trading higher, while the S&P 500 barely rose yesterday (+0.26%) and volatility was slightly lower, with VIX falling settling around 25. The yen strengthened to 107.1 overnight, not seen since 15 month ago. Officials still need to express concern for the appreciation. EUR/USD was higher at 1.238 amid treasury yields being lower yesterday. European rates were mixed, with the longer end suffering relative to the shorter end. Oil was broadly unchanged over the day as a whole at around 63 dollar per barrel. The rand was relatively calm amid the ANC’s decision to replace now-former South African President Jacob Zuma with ANC leader Cyril Ramaphosa, although no time for the transition has been yet .

Fed Chair Jerome Powell’s swearing-in remarks yesterday reflected comments on the Fed being alert to developing risks to financial stability as well as to go ahead with a process of gradual normalisation on both interest rates and balance sheet reduction. This has to be seen in light of recent lower equities. The Fed fund futures point to a virtual 100% probability of the FOMC hiking rates in the March meeting.

On a new Fed Vice-Chair, sources indicate that Loret ta Mester (Cleveland Fed) is to be considered by the White House.

We published Yield Outlook yesterday. We argue that the rapid rise in yields seen this year is now slowing down but that risk is still seen on the upside, especially if we look six to 12 months forward. We forecast that 10Y US Treasury yields will rise to 3.30% (previously 2.90%) on a 12-month horizon. We expect German 10Y Bund yields to rise to 1.20% (previously 1.0%) on a 12-month horizon.