Sample Category Title

EURUSD Intraday Analysis

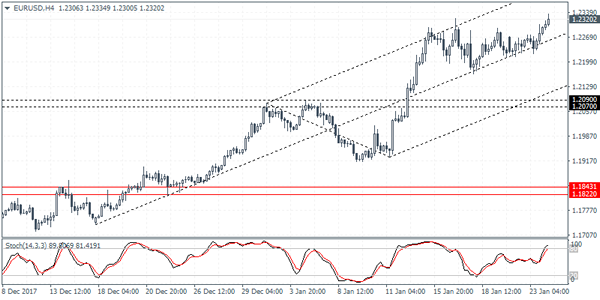

EURUSD (1.2320): The euro currency was seen turning bullish yesterday with price action seen extending the gains in the early Asian trading session today. The euro's gains came broadly from the USD's weakness. EURUSD managed to edge slightly higher trading near the 1.2300 handle. However, the current higher high posted is seen with the Stochastics oscillator forming a lower high. The divergence could potentially indicate a downside move in the euro. Price action is trading near the major resistance level of 1.2300 region. Unless there is a strong close above this level we expect to see the potential for a correction in the common currency.

UK Unemployment Rate Expected To Remain At Historic Lows

The U.S. dollar was on the defensive yesterday as the currency posted some sharp intraday volatility as the funding bill was approved for a few weeks. The USD continues to remain weak against its peers. Lack of economic data also made investors look at the broader themes.

BoJ's Kuroda held a press conference after the BoJ's statement was released. Reiterating the BoJ's commitment to its QE program, Kuroda quashed market expectations of a potential early exit to the central bank's monetary stimulus program.

The euro and the British pound managed to flirt near the highs. Data from Germany showed an improvement in the German ZEW economic sentiment. The index beat market consensus of 17.8 as it rose to 20.4, accelerating from 17.4 previously.

Looking ahead, investors will be focusing on the flash manufacturing and services PMI from Germany, France and the Eurozone. The UK's ONS will be releasing the monthly labor market statistics. The UK's unemployment rate is expected to stay put at 4.3% while average earnings are expected to rise at a steady pace of 2.5%.

Later in the evening, New Zealand will be reporting on its quarterly CPI figures. Economists have penciled a slower rate of inflation growth at 0.4% for the fourth quarter of 2017.

Fed Chair Powell Is ‘Yellen In Disguise’ Amid Discussions About Price Level Targeting

Yesterday, the US Senate officially confirmed Jerome Powell as the next Fed Chair when Yellen's term expires on 3 February. This was as expected, but it has taken a long time for the Senate to actually approve Powell as Yellen's successor (so long that Trump actually needed to renominate Powell).

We expect Powell to stick to the current monetary policy strategy in the short run by raising the Fed funds target range three times this year, as he has always voted with Yellen and expressed similar views on the economy. The first hike is expected to come at the March meeting, the first meeting he chairs. The Fed is not expected to move at Yellen's last meeting, which ends on Wednesday 31 January, as this is one of the small meetings without a press conference and updated projections (the Fed has only hiked at the larger meetings). Markets have priced in a March hike but underestimate the likelihood of a June hike, where we expect the second hike.

In the long run, there is increasing discussion among Fed members about whether to change the 2% inflation target to a price level target over the next few years in order to get ready for fighting the next crisis whenever it comes. Powell is expected to set up a subcommittee, which will dig into this.

One problem though is that Powell is less qualified than his predecessors (he is a lawyer not an economist) and the full FOMC is becoming more inexperienced, as besides a new Fed Chair there are also many new Fed governors on the board (Trump still needs to nominate a Fed Vice Chair and two ordinary board governors while Marvin Goodfriend has not been approved yet). This is not necessarily a problem when the Fed runs on autopilot but may be a problem if the economy is hit by a shock in either direction (an economic downturn or overheating) or in discussions about changing the long-run framework as mentioned in the previous bullet. We have previously argued that a more inexperienced Fed might be a drag on the dollar.

In The UK, The Jobs Report For November Is Being Released Today

Market movers today

In the euro area, the preliminary PMI figures for January are due for release. Both manufacturing and service PMIs rose yet again in December, climbing to 60.6 and 56.6 respectively. Activity remains high in the euroarea and we expect the PMIs to remain at high levels. However, in line with the decline observed in IFO expectat ions in December, we believe January’s PMI will show a decline. We estimate manufacturing PMI at 60.1 and service PMI at 56.2.

In the UK, the jobs report for November is being released today. There are some signs that employment is no longer increasing at the same pace as previously or possibly has even stagnated. So, in this jobs report we will look for signs of whether this was just transitory or not . We est imate the unemployment rate (three-month average) was unchanged at 4.3%. We estimate the annual growth in average weekly earnings ex bonuses (three-month average) declined to 2.2% y/y from 2.3% y/y, underlining that there is no big wage pressure present in the UK yet .

In the US, the important preliminary PMIs release for January are due out . Although Markit PMI manufacturing trended up over the past six months, it is st ill a puzzle that the index is below the equivalent ISM manufacturing index. Given the big discrepancy, we think Markit PMI could rise further although the bad weather may have pulled in the other direct ion. We estimate an increase to 55.7 from 55.1. Since August , Markit PMI services has fallen 2.3 index points to 53.7, which we think is too much – we expect a rebound to 54.5.

In Sweden, Flodén is due to talk about monetary policy and the economic out look and Prospera inflation expectations are due out.

Selected market news

Earnings set the tone for US equity markets last night with both the S&P500 and the NASDAQ indices trading higher. The bearish momentum in the fixed income market seems to have faded ahead of tomorrow’s ECB meeting and after the dovishtone from the Bank of Japan yesterday. Yields on 10Y US Treasuries were little changed last night , still trading around 2.62%.

In Asia, risk sentiment is generally weaker this morning. In particular, Japanese equity markets are trading lower along with an appreciation in JPY. USD generally sells off and the broadbased dollar index, the DXY index, has dropped below 90 for the first time since January 2015. The sell-off in Japanese equities comes after the Nikkei index yesterday rose to the highest level since 1991 and thus looks very much like a correct ion driven by profit taking and a weaker USD.

Yesterday, the US Senate officially confirmed Jerome Powell as the next Fed Chair when Yellen’s term expires on 3 February. This was as expected, but it has taken a long time for the Senate to actually approve Powell as Yellen’s successor. We expect him to stick to the current monetary policy strategy in the short run by raising the Fed funds target range three times this year. The first one is expected to come at the March meeting, the first meeting he chairs.

Australia’s Westpac Leading Index Rose In December

For the 24 hours to 23:00 GMT, the AUD declined 0.25% against the USD and closed at 0.7995.

LME Copper prices declined 2.0% or $144.0/MT to $6905.0/MT. Aluminium prices declined 1.0% or $21.5/MT to $2213.5/MT.

In the Asian session, at GMT0400, the pair is trading at 0.8001, with the AUD trading 0.08% higher against the USD from yesterday's close.

Overnight data indicated that Australia's Westpac leading index recorded a rise of 0.27% on a monthly basis in December, after advancing by a revised 0.05% in the previous month.

The pair is expected to find support at 0.7968, and a fall through could take it to the next support level of 0.7935. The pair is expected to find its first resistance at 0.8023, and a rise through could take it to the next resistance level of 0.8045.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

Euro-Zone’s Economic Sentiment Jumped To A 6-Month High Level In January, While Germany’s Investor Mood Improved To An 8-Month...

For the 24 hours to 23:00 GMT, the EUR rose 0.32% against the USD and closed at 1.2297, following better-than-expected ZEW economic sentiment surveys across the common currency region as well as robust consumer confidence data in the Euro-zone.

The Euro-zone's ZEW economic sentiment index climbed to a 6-month high level of 31.8 in January, thus pointing to a strong pick-up in economic confidence as the region continues its strong growth momentum. The index had recorded a reading of 29.0 in the prior month.

Another data revealed that the region's flash consumer confidence index climbed more-than-anticipated to a level of 1.3 in January, highlighting the increasingly positive mood among consumers as the region is in the midst of a solid economic expansion. In the previous month, the index had registered a level of 0.5, while investors had envisaged for a rise to a level of 0.6.

Separately, ZEW investor morale in Germany surged to an 8-month high level of 20.4 in January, beating market expectations for an advance to a level of 17.7, as investors shrugged off political uncertainty in Berlin and focused on brighter economic prospects in the Euro-bloc's largest economy. In the previous month, the index had registered a level of 17.4. Also, the nation's ZEW current situation index jumped to an all-time high level of 95.2 in January, topping market anticipation for a rise to a level of 89.6 and compared to a level of 89.3 in the prior month.

In the US, data indicated that the Richmond Fed manufacturing index registered a more-than-anticipated drop to a level of 14.0 in January, compared to a reading of 20.0 in the prior month, while markets were expecting the index to fall to a level of 19.0.

In the Asian session, at GMT0400, the pair is trading at 1.2317, with the EUR trading 0.16% higher against the USD from yesterday's close.

The pair is expected to find support at 1.2254, and a fall through could take it to the next support level of 1.2191. The pair is expected to find its first resistance at 1.2349, and a rise through could take it to the next resistance level of 1.2381.

Trading trends in the Euro today is expected to be determined by the release of the flash Markit manufacturing and services PMIs for January across the Euro-zone, scheduled in a few hours. Later in the day, the release of US preliminary Markit manufacturing and services PMIs for January, followed by the existing home sales data for December, would garner significant amount of investor attention.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

UK Public-Sector Net Borrowing Reported A Deficit In December

For the 24 hours to 23:00 GMT, the GBP rose 0.13% against the USD and closed at 1.4002.

Macroeconomic data revealed that UK’s public sector net borrowing posted a deficit of £1.0 billion in December, falling short of market anticipations for a deficit of £4.3 billion. In the prior month, public sector net borrowing had registered a revised deficit of £6.6 billion.

Meanwhile, the nation’s CBI industrial trends total orders fell less-than-anticipated to a level of 14.0 in January, compared to a level of 17.0 in the prior month, while markets were anticipating it to ease to a level of 12.0.

In the Asian session, at GMT0400, the pair is trading at 1.4037, with the GBP trading 0.25% higher against the USD from yesterday’s close.

The pair is expected to find support at 1.3954, and a fall through could take it to the next support level of 1.3872. The pair is expected to find its first resistance at 1.4081, and a rise through could take it to the next resistance level of 1.4126.

Ahead in the day, all eyes would be on the release of UK’s ILO unemployment rate and average weekly earnings data for the three months to November, to gauge strength in the nation’s labour market.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

Japan’s Manufacturing Activity Hit Highest Level In Almost 4 Years In January

For the 24 hours to 23:00 GMT, the USD declined 0.6% against the JPY and closed at 110.28.

In the Asian session, at GMT0400, the pair is trading at 109.95, with the USD trading 0.3% lower against the JPY from yesterday's close.

The Japanese Yen climbed against the USD, following strong manufacturing sector report in Japan.

Data revealed that Japan's preliminary Nikkei manufacturing PMI climbed to a level of 54.4 in January, notching its highest level since February 2014 and pointing to a strong economic activity in the new year. The PMI had recorded a reading of 54.0 in the previous month.

On the other hand, the nation's adjusted merchandise trade surplus narrowed more-than-anticipated to ¥86.8 billion in December, after recording a surplus of ¥364.1 billion in the previous month. Markets were anticipating the country's adjusted merchandise trade surplus to drop to ¥276.7 billion.

Other data showed that the nation's exports advanced 9.3% on an annual basis in December, missing market expectations for a gain of 10.0%. In the previous month, exports had risen 16.2%. Also, the nation's imports climbed 14.9% YoY in December, higher than market estimates for a rise of 12.4%. Imports had advanced 17.2% in the previous month.

Early morning data revealed that Japan's final leading economic index climbed to a level of 108.3 in November, while the preliminary print had indicated a rise to a level of 108.6. The index had registered a level of 106.5 in the previous month. Additionally, the nation's final coincident index was revised lower to a level of 117.9 in November, compared to a level of 116.4 in the prior month. The preliminary figures had recorded a rise to 118.1.

The pair is expected to find support at 109.49, and a fall through could take it to the next support level of 109.04. The pair is expected to find its first resistance at 110.79, and a rise through could take it to the next resistance level of 111.64.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

Swiss Franc Extends Its Gains In The Morning Session

For the 24 hours to 23:00 GMT, the USD declined 0.45% against the CHF and closed at 0.9578.

In the Asian session, at GMT0400, the pair is trading at 0.9554, with the USD trading 0.25% lower against the CHF from yesterday’s close.

The pair is expected to find support at 0.9527, and a fall through could take it to the next support level of 0.9499. The pair is expected to find its first resistance at 0.9608, and a rise through could take it to the next resistance level of 0.9661.

Amid no macroeconomic releases in Switzerland today, investor sentiment would be determined by global macroeconomic factors.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

Loonie Trading On A Stronger Footing This Morning

For the 24 hours to 23:00 GMT, the USD declined 0.18% against the CAD and closed at 1.2425.

In the Asian session, at GMT0400, the pair is trading at 1.2414, with the USD trading 0.09% lower against the CAD from yesterday’s close.

The pair is expected to find support at 1.2384, and a fall through could take it to the next support level of 1.2353. The pair is expected to find its first resistance at 1.2468, and a rise through could take it to the next resistance level of 1.2521.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.