Sample Category Title

GBPUSD Bullish Above 1.3200

The British pound has moved above the 1.3200 level against the U.S dollar, hitting 1.3229 during the Asian session. GBPUSD buying demand has returned, as the U.S dollar index weakens. and intraday sellers failed to break below the 1.3140 level during yesterday's U.S session. Price-action is currently trading around the 1.3218 level, ahead of the release of UK Retail Sales data.

The GBPUSD pair is expected to advance higher while trading clearly above the 1.3200 level. Buyers are expected to target the weekly pivot point, at 1.3233 and the 1.3268 resistance area.

If intraday GBPUSD sellers push price-action back below the 1.3200 level, the pair is expected to find support from the daily pivot point, at 1.3179, and the key 1.3149 support level.

EURO Buyers In Control Above 1.1780

The euro has moved sharply higher against the U.S dollar, hitting 1.1816 during the Asian trading session. The U.S dollar index started to move lower during the U.S session, as the Federal Reserve's Beige Book highlighted a lack of inflation in the U.S economy. The EURUSD pair currently trades around the 1.1800 mark, as traders await the U.S dollars next move, and any news coming from Catalonia.

EURUSD intraday buyers will remain in control while price-action trades above the key 1.1780 level. Further bullish advancement for the euro can be expected towards the 1.1833 and 1.1858 technical resistance levels.

Should the EURUSD pair move below the 1.1780 level for a sustained period, further declines towards the 1.1750 and 1.1736 level remain likely.

China GDP Kicks Off An Active Trade Session

High-profile Chinese data have set the tone for Thursday's session. British retail sales, a Catalan deadline and a US manufacturing survey are also scheduled to make headlines throughout the day.

China's National Statistics Bureau said third-quarter GDP accelerated 6.8% year-over-year, matching forecasts. That followed a faster than expected gain of 6.9% in Q2.

China also said retail sales rose 10.3% year-over-year. Industrial production climbed a faster than expected 6.6%, official data showed.

The Chinese economy is the world's second largest. What happens there is important to any investor with a stake in global trade, emerging markets and commodities.

Looking ahead to the rest of the day, Switzerland will release its latest trade figures at 06:00 GMT. Two hours later, Catalan authorities must confirm whether they have declared Independence or not following the referendum result.

UK retail sales will make headlines at 08:30 GMT. Receipts at retail stores are forecast to grow 2.1% in the 12 months through September. Excluding fuel, sales are expected to rise 2.4%.

Shifting gears to North America, the US Labor Department will release its weekly jobless claims report at 12:30 GMT. Claims are forecast to fall by 3,000 to a seasonally adjusted 240,000 in the week ended 14 October.

The Philadelphia Fed will also report its latest manufacturing survey at 12:30 GMT. The headline indicator is expected to fall to 22.0 from 23.7.

In terms of monetary policy, Fed Bank of Kansas City President Esther George will deliver a speech at 13:30 GMT. George is not a member of this year's Federal Open Market Committee (FOMC), which is scheduled to meet again in a few weeks.

AUD/USD

The Australian dollar gave back gains against the dollar despite upbeat China data. The AUD/USD exchange rate reached a session high of 0.7871 before paring gains later in the day. The pair is trading flat compared to Wednesday's close. The technical levels show immediate support at 0.7818, which is the low from Wednesday. The pair continues to trade within a 100-pip range between 0.7800 and 0.7900.

EUR/USD

Europe's common currency regained momentum on Wednesday, climbing back toward the 1.1800 handle. The EUR/USD touched a high of 1.1820 overnight before falling back toward 1.1800. The euro risks further downside should it break below that level. Immediate support is likely found at 1.1703.

GBP/USD

Cable edged slightly higher in overnight trade, although gains were tepid after Bank of England Governor Mark Carney issued a stark warning about Brexit risks. Those comments outweighed Britain's 3% inflation print, which was bigger than expected. The GBP/USD is up 0.1% to trade at 1.3210. Its immediate resistance trigger is 1.3250. On the opposite side of the ledger, support levels are found near 1.3130.

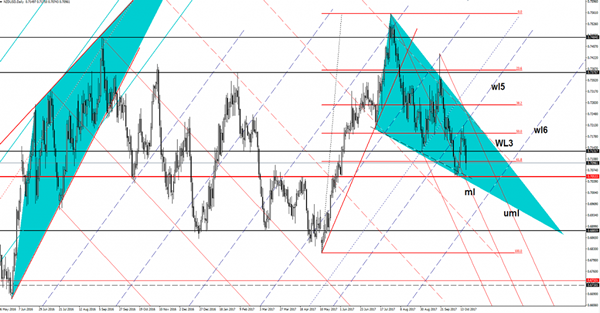

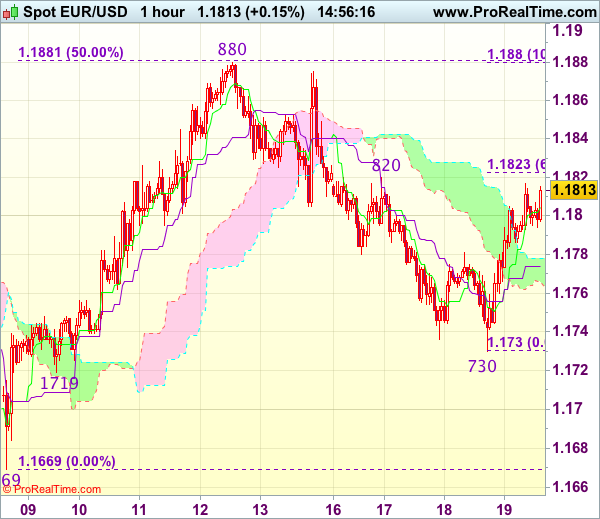

Trade Idea : EUR/USD – Sell at 1.1850

EUR/USD - 1.1815

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 1.1808

Kijun-Sen level : 1.1777

Ichimoku cloud top : 1.1778

Ichimoku cloud bottom : 1.1765

Original strategy :

Buy at 1.1745, Target: 1.1820, Stop: 1.1725

Position : -

Target : -

Stop : -

New strategy :

Sell at 1.1850, Target: 1.1750, Stop: 1.1885

Position : -

Target : -

Stop : -

Although the single currency has risen again and near term upside risk remains for the rise from this week’s low at 1.1730 to extend gain to 1.1845-50, if our view that top has been formed at 1.1880 is correct, upside would be limited and bring retreat later, below the Kijun-Sen (now at 1.1777) would suggest an intra-day top is formed, bring weakness to 1.1755-60 but said support at 1.1730 should remain intact.

In view of this, we are inclined to turn short on further rise but one should exit on subsequent decline. Above said resistance at 1.1880 would shift risk back to upside and extend early rise from 1.1669 to 1.1900-10 first.

New Zealand Dollar Trend Overwhelmingly Negative

Key Highlights

- The New Zealand Dollar corrected towards 0.7200 against the US Dollar where it found sellers.

- A connecting bearish trend line with current resistance at 0.7160 on the 4-hours chart of NZD/USD is preventing an upside break.

- The US Building Permits in Sep 2017 posted a 4.5% decline, compared with the -2.9% forecast.

- Today in the US, the Initial Jobless Claims for the week ending Oct 14, 2017 will be released, which is forecasted to decline from 243K to 240K.

NZDUSD Technical Analysis

The New Zealand Dollar after forming a base above 0.7050 against the US Dollar started a correction. The NZD/USD pair traded above 0.7150, but upside remains capped by 0.7200.

During the upside move, the pair was able to break a bearish trend line at 0.7115 on the 4-hours chart. It also succeeded in moving past the 50% Fib retracement level of the last decline from the 0.7243 high to 0.7059 low.

However, the upside move was capped by the 100 simple moving average near 0.7185 (4-hour, red) and 0.7200. Moreover, there is a connecting bearish trend line with current resistance at 0.7160 on the same chart, acting as a barrier for more gains.

Overall, it seems like the pair might continue to struggle near 0.7180-0.7200 and will most likely resume its downtrend.

US Building Permits and Housing Starts

Recently in the US, the Building Permits and Housing Starts report for Sep 2017 was released by the US Census Bureau, at the Department of Commerce. The forecast was slated for a 2.9% decline in the Building Permits compared with the previous month.

The actual result was lower than the forecast, as there was a decline of 4.5% in Building Permits. Looking at the Housing Starts, there was a decline of 4.7%, compared with the -0.5% forecast.

The report stated:

Privately-owned housing units authorized by building permits in September were at a seasonally adjusted annual rate of 1,215,000. This is 4.5 percent (±1.6 percent) below the revised August rate of 1,272,000 and is 4.3 percent (±1.7 percent) below the September 2016 rate of 1,270,000. Single-family authorizations in September were at a rate of 819,000; this is 2.4 percent (±1.7 percent) above the revised August figure of 800,000.

The NZD/USD pair might correct a few pips in the short term, but upsides should be limited by 0.7180-0.7200.

Economic Releases to Watch Today

- UK Retail Sales for Sep 2017 (YoY) – Forecast +2.1%, versus +2.4% previous.

- UK Retail Sales for Sep 2017 (MoM) – Forecast -0.1%, versus +1.0% previous.

- UK Retail Sales ex-fuel for Sep 2017 (YoY) – Forecast +2.4% versus +2.8% previous.

- US Initial Jobless Claims – Forecast 240K, versus 243K previous.

Trade Idea : USD/JPY – Buy at 112.70

USD/JPY - 113.00

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 113.01

Kijun-Sen level : 112.69

Ichimoku cloud top : 112.23

Ichimoku cloud bottom : 112.07

Original strategy :

Buy at 112.50, Target: 113.50, Stop: 112.15

Position : -

Target : -

Stop : -

New strategy :

Buy at 112.70, Target: 113.70, Stop: 112.35

Position : -

Target : -

Stop : -

As dollar has maintained a firm undertone after yesterday’s rally, above previous resistance at 112.83, adding credence to our view that low has been formed at 111.65 and consolidation with upside bias remains for the rise from 111.65 low to extend gain towards 113.30, however, near term overbought condition should limit upside to resistance at 113.44 and reckon 113.75-80 would hold on first testing.

In view of this, we are looking to buy dollar on pullback as the Kijun-Sen (now at 112.69) should limit downside and bring another rise. Below previous resistance at 112.48 (now support) would defer and signal top is formed instead, bring test of there upper Kumo (now at 112.25 but price should stay above support area at 112.03-13.

Forex: Bank of England Faces Conundrum

On Wednesday, data released by the UK Office for National Statistics (ONS) showed average weekly earnings (excluding bonuses) rose 2.1% in August – slightly higher than the 2% forecast. However, in real terms, due to higher inflation, they fell 0.4% on the year before. The swaps market is expecting an 80% chance of a rate rise next month but the prospect of hiking rates when real wages are in negative territory will make any potential hike difficult to justify. The conundrum faced by the Bank of England is: raise rates because inflation is high and unemployment is low, but, if you raise rates it puts extra pressure on the consumer and a sharp break on the economy as we close out 2017. The markets are convinced there will be a rate hike in November but, faced with the above conundrum, this may be difficult for the Central Bank to impose.

Data released early on Thursday showed economic growth in China slowed marginally as expected in Q3. The National Bureau of Statistics data showed the Chinese economy grew at 6.8%, slightly down on the previous release of 6.9%. The markets had been expecting a slight slowdown in growth as borrowing costs have been pushed higher, following a government campaign against riskier lending and a cooling in housing prices, as property investment and construction has softened. GDP in Q3 grew 1.7% quarter-on-quarter, compared with growth of 1.8% in Q2, which was revised up from an initially reported 1.7% growth.

EURUSD is 0.12% higher in early trading. Currently, EURUSD is trading around 1.1800.

USDJPY is little changed overnight, currently trading around 112.98.

GBPUSD is currently trading around 1.3216, marginally higher from last nights close.

Gold is 0.25% lower in early trading, currently trading around $1,278.

WTI is unchanged from last nights close, currently trading around $52.24.

Major data releases for today:

At 09:30 BST, the UK Office of National Statistics will release Retail Sales (MoM) for September. Consumer spending is forecast to come in at -0.1% from the previous reading of 1.0%. August’s robust release surprised the markets. The recent 5-year high CPI release of 3.0% and the fact that basic pay is lagging is putting a squeeze on UK consumers, thus resulting in an expected poor Retail Sales figure for September. A release significantly outside of the consensus will result in GBP volatility.

At 13:30 BST, Initial Jobless Claims for the week ending October 13th will be released by the US Department of Labor. The consensus is calling for a slight decrease to 240K from the previous release of 243K. The US Labor market continues to demonstrate robustness and there is nothing to suggest that this release will be any different than expected. If we see a markedly different release we will expect to see USD volatility.

Currencies: EUR/USD Resilient Despite Catalan Uncertainty

Sunrise Market Commentary

- Rates: Shun Catalan political risk

Eco data and central bankers won't impact trading today. The Catalan-Madrid stand-off could escalate to a new phase. Cautiousness might be warranted. The Bund might profit in a daily perspective, with more outperformance vs the US Note future while Spanish spreads could widen. - Currencies: EUR/USD resilient despite Catalan uncertainty

Yesterday, the dollar rebound was a bit different from earlier this week. USD/JPY profited from higher core yields and a risk-on sentiment, but the US currency lost ground against the euro. Today, the focus for global FX trading will be on Catalonia. (Currency) markets are positioned for a non-disruptive outcome. This is far from sure. So, we see downside risk for the euro.

The Sunrise Headlines

- US stock markets ended positive, but with big differences between S&P (+0.07%), Nasdaq (+0.01%) and Dow (+0.7%). Asian stock markets are mixed overnight with China underperforming (-0.3%).

- China's economy expanded at a robust 6.8% pace in Q3, meeting expectations, as traditional growth drivers such as manufacturing and exports gained steam. September retail sales (10.3% Y/Y) and industrial production (6.6% Y/Y) were close to consensus while investments (7.5% Y/Y) slightly disappointed.

- Australia enjoyed another month of solid jobs growth in September (+19.8k), with the annual pace of gains sprinting ahead to the fastest in almost a decade and nudging the unemployment rate lower (5.5%).

- Catalonia is on the precipice of losing its autonomy. Regional President Puigdemont has until 10 a.m. local time to renounce his independence claims or have Madrid take control.

- While the Bank of Korea held interest rates at a record low, higher GDP/CPI forecast, hawkish comments from the governor and a dissenter calling for a rate hike indicate that a change in monetary policy is getting closer.

- Republicans in Congress are examining how to block a potential move by Trump to pull the US out of NAFTA as members of the president's own party also warn him that any such move could put a joint push for tax cuts at risk.

- Today's eco calendar contains UK retail sales, US weekly jobless claims and Philly Fed Business Outlook. Spain and France tap the market. EU leaders hold a Summit in Brussels.

Currencies: EUR/USD Resilient Despite Catalan Uncertainty

EUR/USD resilient despite Catalonia

The dollar initially stayed well bid yesterday. However the relative performance of individual USD cross rates was different from earlier this week. The dollar struggled to make further headway against the euro, despite the Catalan uncertainty. Some ‘hawkish' ECB comments blocked the euro decline. There was also talk of substantial EUR/JPY buying. EUR/USD closed the day slightly higher at 1.1787 (from 1.1766). USD/JPY outperformed, supported by higher core US/EMU yields and by a strong risk sentiment. The pair finished the session at 112.94 (from 112.10).

Overnight, the Chinese Q3 GDP was in line with expectations. The composition was OK. September retail sales and production were also as expected. Even so, the Chinese data were not enough to enhance the Asian risk rally. Most regional indices show modest losses of less than 0.5%. Japan outperforms on overall yen weakness. USD/JPY is testing the 113 level. EUR/JPY is trading well north of 133. EUR/USD maintains yesterday's intraday gain and trades in the 1.18 area. The Aussie dollar profited temporary from good labour data but failed to maintain the initial gain. AUD/USD trades again in the mid 0.78 area.

There are no important data in the EMU and the US calendar is also thin. Jobless claims are expected little changed. The Philly Fed business outlook is expected slightly softer at 22.0 from 23.8. These data won't change the global picture for the dollar. The deadline expires for Catalonia to renounce its independence claim. If it doesn't, Madrid said it will activate laws to suspend the region's autonomy. Until now, the impact of the Catalan tensions on broader European markets was limited. Yesterday's price action of the euro suggests that markets assume that any action from Spain against the region will be modest/non-disruptive. Even so, uncertainty on the next steps will probably persist. This might still be a (slightly?) negative for the euro. On the dollar side of the story, the picture remains diffuse as well. USD/JPY finally gained some traction on higher yields core yields (US & Europe). EUR/JPY also profits. At the same time, the dollar struggles to extend gains against the euro even as interest differentials are at cycle highs (2-y USD/Germ) or at a ‘multi-month' top (10-y). This is disappointing for USD bulls. Earlier this week, we kept a neutral-to-tentatively negative bias for EUR/USD. We maintain this call, but due to uncertainty on Catalonia rather than on assumed USD strength. We remain cautious on USD/JPY despite this week's better performance. Event risk from whatever source might weigh on the pair

From a technical point of view, EUR/USD dropped below the 1.1823/ 1.2070 consolidation pattern, but no real test of the 1.1662 support occurred. Last week, the pair even returned (temporary?) above the 1.1823 previous range bottom, which was disappointing for EUR/USD bears. We maintain a cautious sell-on upticks bias. The pair needs to drop below 1.1670/62 support to really give comfort to EUR/USD bears. The USD/JPY momentum was constructive in September. The pair regained 110.67/95 (previous resistance), a short-term positive. The 114.49 correction top is the next important resistance. The rally lost momentum last week. A break beyond 114.49 looks ever more difficult.

EUR/USD: holding up well despite Catalan uncertainty

EUR/GBP

UK retail sales and EU summit in focus for sterling trading

Balanced comments from BoE gouvernor Carney earlier this week convinced markets that any BoE tightening will be modest. This continued to weigh on sterling yesterday. UK labour data were mixed. Wage growth was marginally stronger than expected at 2.2% Y/Y, but real wages remain negative (-0.4%). The small beat in wage growth didn't change market expectations that any BoE tightening will be very limited (probably only one hike). EUR/GBP temporary dropped a few ticks, but the move was soon reversed. The pair was further supported by a broader euro rebound later in the session. EUR/GBP finished the session at 0.8926 (from 0.8920). Cable was mainly driven by the overall swings in the dollar. The pair closed the session at 1.3205.

UK retail sales will be published today. Monthly data are very volatile. For September, a modest decline (-0.1% M/M) is expected after a strong rebound in August (1.0%). September CBI retail data were strong. So, the report shouldn't be too bad. Markets will also keep a close eye at the comments from the EU Summit. The UK will probably press to start with negotiations on trade and a transition period. The EU will probably repeat that there hasn't been made enough progress on the terms of the separation, but maybe the tone might be quite reconciliatory. We don't expect the data or the EU summit to bring any breaking news for sterling. We hold on to the view that any upside of sterling will be difficult as the recent rally has run into resistance. We look to buy EUR/GBP on dips.

EUR/GBP staged a strong uptrend from April till late August to set a top at 0.9307. Rising UK inflation data and hawkish BoE comments reinforced a sterling rebound, but this rebound has run its course. EUR/GBP supports at 0.8743 and 0.8652 proved difficult to break. The recent rebound above 0.89 improved the ST technical picture of EUR/GBP, but for now there were no convincing follow-through gains. EUR/GBP 0.9026 is 50% retracement of the recent countermove

EUR/GBP: sterling rebound runs into resistance as BoE tightening will be limited.

Market Update – Asian Session: China Q3 GDP Comes In As Expected

Asia Summary

Asian equity markets opened the session mixed. Chinese equity markets have traded somewhat lower as GDP in Q3 met expectations. Recall, there were some expectations that the figure could be better than expected.

The Nikkei 225 opened higher, as the index attempts to gain for the 13th straight session, which would be the longest winning streak in over 20 years.

Japanese banks have traded broadly higher amid the recent gains in government bond yields and earlier rise in some of the larger US banks. Australian banks are also generally trading higher.

Australian energy company quarterly updates were in focus. Santos has gained after raising its FY production forecast, while Woodside Petroleum has declined after reporting lower Q3 revenues and naming a new CFO.

In terms of technology, Taiwanese companies that supply Apple are generally lower following a press report that the US tech firm is said to have cut iPhone 8 orders for Nov and Dec. Also, South Korean chip makers are once again trading lower on today's session. LG Electronics has gained over 5% on reports that the company will partner with Qualcomm on self-driving auto components.

Chinese telecom ZTE Corp has declined by over 3%, despite reporting y/y growth in its 9-month net profits and revenues.

In describing China's GDP data, the Stats Bureau said in the Jan-Sept period consumption contributed 64.5% to GDP. It also expects the domestic economy to maintain improving momentum. Amid the data, China's 10-year bond yield has declined.

Australia's 3-year bond yield has risen by over 4bps, after the September employment change beat expectations, while the unemployment rate unexpectedly fell. Yields have also moved higher following the gains seen in US Treasury yields on Wednesday's session amid comments from influential NY Fed President Dudley. Dudley said the Fed is on the path to achieve 3 rate hikes in 2017 (implying one more rate increase this year). Recall when Dudley previously spoke on Oct 6th, he did not comment on the timing for rate hikes.

At the longer end of the curve, earlier today, Japan's 20 and 30-year JGB yields hit highs not seen since July. Bank of Japan (BoJ) official Nakaso said the central bank will adjust the shape of the yield curve as needed. He added that the BoJ can achieve the same rate with smaller amount of JGB purchases.

Meanwhile, in South Korea the 10-year bond yield has risen over 3bps, as even though the Bank of Korea (BOK) left rates unchanged (as expected), there was a hawkish dissenter at today's policy meeting, who voted for a rate hike. The central bank additionally raised its 2017 GDP growth and inflation forecasts as it believes the impact of souring trade relations with China will ease in 2018.

In foreign exchange, the PBoC's Sept Net Forex Purchase Position saw its first m/m rise since Oct 2015. The data comes amid other signs of easing capital outflows from China. PBoC Gov Zhou said the yuan's trading band (currently 2%) is not too important and the expansion of it is not a current focus.

The Aussie traded toward session highs following the better than expected Sept employment change. However, the currency has since pared gains after the in line China GDP data. The Kiwi has traded lower, as the government formation process in New Zealand continues. On yesterday's session, a NZ First Party official said an announcement was expected during this afternoon.

Looking ahead, US companies due to report earnings today include Bank of NY Mellon, Intuitive Surgical, Nucor, PPG Industries, PayPal, Philip Morris and Verizon.

Key economic data

(CN) CHINA Q3 GDP Q/Q: 1.7% V 1.7%E; Y/Y: 6.8% V 6.8%E

(JP) JAPAN SEPT TRADE BALANCE: ¥670.2B V ¥556.8BE; ADJ: ¥240.3B V ¥367.3B PRIOR

(AU) AUSTRALIA SEPT EMPLOYMENT CHANGE: +19.8K V +15.0KE; UNEMPLOYMENT RATE: 5.5% V 5.6%E

(AU) Australia Sept RBA Govt FX Transactions (A$): -762M v -581M prior

(KR) BANK OF KOREA (BOK) LEAVES 7-DAY REPO RATE UNCHANGED AT 1.25%; AS EXPECTED

(CN) CHINA SEPT FIXED ASSETS EX RURAL YTD Y/Y: 7.5% V 7.7%E

(CN) CHINA SEPT RETAIL SALES Y/Y: 10.3% V 10.2%E; YTD Y/Y: 10.4% V 10.3%E

(CN) CHINA SEPT INDUSTRIAL PRODUCTION Y/Y: 6.6% V 6.5%E; YTD Y/Y: 6.7% V 6.7%E

(CN) China PBoC Sept Net Forex Purchase Position (CNY): +0.9B m/m (first rise since Oct 2015)

Speakers and Press

Japan

(JP) Japan PM Abe Cabinet approval rating declines 2 pct points to 38% - Asahi Poll

(JP) BoJ Nakaso: Will adjust shape of yield curve as needed; BoJ can impact rates even if JGBs to buy become scarce

South Korea

(KR) South Korea Finance Ministry: While North Korean tensions have persisted, financial markets have been stable and the impact on the economy has been limited - statement ahead of parliamentary audit due Oct. 19-20

China/Hong Kong

(CN) China Economist sees China avg annual GDP growth at 5% from 2020-2035 - Chinese press

(CN) PBOC Yi Gang: Price stability not equal to financial stability -speaking at 19th Party Congress

(CN) China Banking Regulatory Commission (CBRC) Guo: China to deepen reform, opening up banks - speaking at 19th Party Congress

(CN) China Wind data shows Q3 performance forecast reports from China's listed companies have beaten market expectations – Xinhua

USD/CNY (CN) PBOC Gov Zhou: Yuan trading band is not too important, band expansion is not a current focus

(CN) China FX Regulator SAFE Chief/PBoC Pan: China FX market supply and demand basically balanced

(CN) China Stats Bureau (NBS) Xing: Jan-Sept consumption contributed 64.5% to GDP growth, 32.8% for capital formation and 2.7% for net exports; Domestic economy to maintain steady and improving momentum

Australia/New Zealand

(NZ) New Zealand National Party Leader English: Does not know whether NZ First will support National; Will present to caucus the ‘broad parameters' of agreement with NZ First and will seek their support

Asian Equity Indices/Futures (00:00ET)

Nikkei +0.4%, Hang Seng -0.2%; Shanghai Composite -0.4%; ASX200 +0.0%, Kospi -0.4%

Equity Futures: S&P500 -0.0%; Nasdaq100 -0.1%, Dax -0.1%; FTSE100 -0.1%

FX ranges/Commodities/Fixed Income (00:00ET)

EUR 1.1816-1.1792; JPY 113.09-112.88; AUD 0.7871-0.7841;NZD 0.7171-0.7123

Dec Gold -0.1% at $1,281/oz; Nov Crude Oil -0.1% at $51.98/brl; Dec Copper -0.1% at $3.17/lb

(NZ) New Zealand sells NZ$200M in 2.75% 2025 bonds; avg yield 2.7545%; bid-to-cover 2.66x

(CN) China PBOC injects CNY140B in combined 7-day and 14-day reverse repos v CNY300B prior; injects net CNY100B v CNY270B prior

USD/CNY (CN) PBOC SETS YUAN REFERENCE RATE AT 6.6093 V 6.5991 PRIOR

(JP) Japan MoF sells ¥1,78T in 5-yr JGBS; avg yield -0.0820% v -0.110% prior; bid-to-cover 4.24x v 4.07x prior

Equities notable movers

Australia/New Zealand

RCR.AU Awarded gas-fired power plant contract with PT Kartanegara Energi Perkasa in Indonesia worth ~A$75M; +6%

PEN.AU To divest 74% stake in South Africa Karoo projects through an active process; -4.8%

Korea

047810.KR Will not to put co. under evaluation for possible delisting, trading resumes; +14.3%

China/Hong Kong

763.HK Reports 9-month (CNY) Net 3.91B v 2.86B y/y, Op 5.29B v 952M y/y, Rev 76.6B v 71.6B y/y; -5%

US

AAPL Said to cut orders for iPhone 8 and Plus by around 50% for Nov and Dec to 5-6M units/month - Taiwanese Press; -0.9% after hours

NZD/USD Falling Wedge?

The NZD/USD drops like a rock and should reach the 0.7053 static support. Remains to see what will happen in the upcoming days because a USDX’s drop will force the pair to increase again. Price could move in range on the short term, I’ve drawn a Falling Wedge pattern, but this is far from being confirmed. The behavior could change if the rate will start to make higher lows and could signal another leg higher.