Sample Category Title

Fed Speeches And Earnings In Focus

- Earnings season in focus as stocks target new highs;

- USD rebound continues on prospect of hawkish new Fed Chair;

- Oil higher on inventory report but will EIA back up the numbers?

US futures are pointing to another higher open on Wall Street on Wednesday, as companies prepare to report on the third quarter at a time when indices are hitting fresh record highs on an almost daily basis.

Companies started reporting third quarter results last week and while the number has picked up this week, it will likely dominate more and more over the coming weeks. Coming on the back of impressive second quarter results and in a more positive global economic environment, expectations are quite high for Q3, even taking into account the detrimental impact of the hurricanes towards the end of the quarter.

The dollar is trading higher again this morning as the possibility of a more hawkish Federal Reserve Chair succeeding Janet Yellen in February raises the prospect of more interest rate hikes next year. Market expectations for interest rates next year are already well below those of the central bank, should Yellen be replaced by someone of a more hawkish nature, the market could find itself well behind the curve.

We've seen something of a recovery in the greenback over the last month or so but even still, it's not a million miles from its lows and has some way to go to pare the substantial losses suffered this year. A break and hold above 94 in the dollar index may signal such a correction, which may be well supported into the end of the year should a more hawkish Chair appointment be announced and Congress make progress on healthcare and, more importantly, tax reform.

In the meantime it's over to William Dudley and Robert Kaplan to provide an update on where the central bank stands on interest rates. While the Fed may have signalled an intention to raise interest rates once more this year and three times next, a number of policy makers have since expressed concern at the lack of inflation, something that also came across in the minutes from the meeting. Kaplan is among those that has shown a willingness to be patient and it's unlikely that recent data will have changed his views on this.

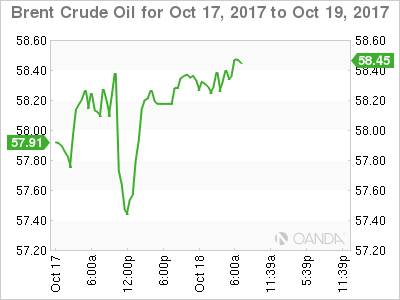

Another highlight on Wednesday will be crude inventory numbers from EIA, which come after API reported a significant drawdown on Tuesday of 7.13 million barrels. Oil has been on another impressive run as of late, supported by higher global demand, a rebalancing of the market and more recently, supply disruptions in Iraq. A similar drawdown today may provide another boost but given the moves we've seen since the summer, I do wonder how much higher we can go in the short-term.

Equities Stall, Dollar Drifts As Markets Seek Catalyst

Wednesday October 18: Five things the markets are talking about

Regional equity bourses are providing mixed results as investors patiently wait for the next catalyst to deliver directional support. A plethora of central bankers are due to speak today (ECB’s Draghi, NY Fed Dudley and Dallas Fed President Kaplan), and a deadline on Catalonia’s independence claim from Spain is forthcoming.

Note: Catalonia has until tomorrow to back down from a challenge to separate.

The ‘mighty’ dollar is little changed as the market continues to fixate on speculation about the next Fed head – volatility across G7 currency pairs is trading atop of a three-month low.

In China at the opening of the twice a decade 19th Chinese Party Congress, President Xi said that China “will push ahead with market-oriented reforms of its foreign exchange rate as well as its financial system, and let the market play a decisive role in the allocation of resources.”

Note: Later this evening, China will releases data for GDP, industrial production and retail sales.

1. Stocks mixed performance

In Japan, the Nikkei share average rallied for a 12th consecutive day overnight, finding support on hopes that this weekend’s election will produce political stability and continuation of loose monetary policy. PM Abe coalition is on track for a roughly two-thirds majority in this weekend’s general election. Both the Nikkei and broader Topix ended up +0.1% higher.

Down-under, Australia’s S&P/ASX 500 index ended flat, while South Korea’s Kospi index was little changed.

In Hong Kong, the Hang Seng index inched lower, while the Shanghai Composite Index was up +0.1%.

In China, blue-chip stocks ended at a 26-month high as party congress opens. Investors are pinning their hopes on reforms to boost domestic growth. The blue-chip CSI300 index rallied +0.8%, while the Shanghai Composite index added +0.3%.

Note: Despite investors seeking direction on economic and financial market reform over the next five-years, China’s leadership events historically have been light on detail.

In Europe, regional indices trade mostly higher across the board with the Spanish IBEX once again under performing, however, ranges again remain relatively tight.

U.S stocks are set to open unchanged.

Indices: Stoxx600 +0.2% at 391.3, FTSE +0.3% at 7537, DAX +0.3% at 13027, CAC-40 +0.2% at 5371, IBEX-35 -0.3% at 10184, FTSE MIB -0.1% at 22305, SMI +0.2% at 9292, S&P 500 Futures flat

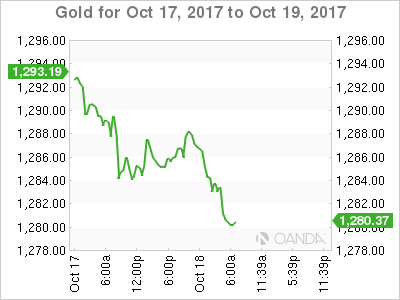

2. Oil prices rise on tighter U.S market, Middle East tensions, and gold lower

Oil prices have rallied overnight, lifted by a fall in U.S crude inventories and concerns that tensions in the Middle East could disrupt supplies.

Brent crude futures are at +$58.16, up +28c or +0.5% from their last close, while U.S West Texas Intermediate (WTI) crude futures are at +$52.03 per barrel, up +15c, or +0.3%.

Note: Trading volumes were limited during Asian hours due to a public holiday in Singapore, Malaysia and parts of India.

API data from the U.S Tuesday showed a big draw – inventories fell by -7.1m barrels in the week to Oct. 13 to +461.4m barrels.

Investors are expected to take direction from today’s EIA report (10:30 am EDT). The market is looking for another drawdown of -4.7m barrels.

Ahead of the U.S open, gold prices remain on the back foot as the dollar strengthened a tad amid speculation that the next U.S Fed chief may be a policy hawk. President Trump is likely to announce his choice before going to Asia in early November. Spot gold is down -0.1% at +$1,283.16 an ounce.

3. Sovereign yield back up

Reports that President Trump might pick John Taylor to lead the Fed after Janet Yellen’s term ends next year has sent two-year U.S Treasury yields to their highest level in nine-years this week.

Taylor is an advocate of a rules-based approach to interest rate policy that would likely see official Fed rates much higher than at present – at least +3.5% according to some observers.

The back up in short-yields (U.S 2’s +1.53%) has not been matched at the long-end. The yield on 10-year Treasuries gained +1bps to +2.31%.

With no eurozone macro-economic data on tap, the German Bund market continues to focus on speeches by ECB officials ahead of next week monetary policy meeting (Oct 26).

Note: The market’s expectations on how the ECB will taper QE have shifted to a nine-month extension at +€30B of purchases per month, rather than the previously expected six-month extension at +€40B.

Germany’s 10-year Bund yields have increased +1 bps to +0.38%, while Spain’s 10-year yield decreased less than -1 bps to +1.578%.

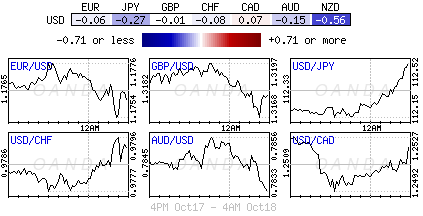

4. Dollar’s tentative support

The ‘mighty’ USD is maintaining a steady bid tone with market participants continuing to focus on Trump’s appointment for the Fed Chair position.

GBP (£1.3170) traders have been focusing on unemployment and earnings data out of the U.K this morning. The slight beat on hourly earnings has kept the door open for a possible BoE rate hike as soon as next month. The U.K’s unemployment data (see below), which is steady, did provide some underlying support, however, Brexit discussion concerns continue to provide the pound with resistance.

The EUR/USD (€1.1747) is little changed in the session, as ECB chief Draghi provided no clues on monetary policy ahead of next week’s rate decision. USD/JPY (¥112.73) is higher with focus on the upcoming Japanese elections (Oct 21/22) seen as maintaining its Abenomics path to recovery.

CNY is a tad firmer as Chinese President Xi pledged to deepen reforms in his address at the 19th Party Congress.

5. U.K real wages fall, job growth peaks

Data from the ONS (Office of National Statistics) revealed that real wages in the U.K fell in August for the fifth month in row. Wage growth after inflation in August was -0.3% as inflation once again outpaced pay increases.

Other data suggests that the U.K’s buoyant job growth may be coming to an end. The number of people in work in the month of August was -108k fewer than in May, while there were +208k more people saying they were not looking for work.

Note: Monthly labor market statistics can be volatile. The ONS puts more emphasis on three-month averages, which continued to show gains in employment and a decline in inactivity in the three months through August.

Nevertheless, many continue to question how the U.K could sustain its growth streak given a slowing economy and uncertainty around Brexit.

CAC Gains Ground As Markets Digesting Q3 Earnings

The CAC index has inched lower in the Wednesday session. Currently, the CAC is trading at 5,382.30, up 0.40% on the day. On the release front, there are no French or eurozone events on the schedule. Earlier in the day, ECB President Mario Draghi spoke at an ECB conference in Frankfurt. Draghi addressed structural reforms in the eurozone economy, but did not discuss the ECB’s monetary policy.

The CAC has not posted a winning daily session in almost two weeks, but that streak could be over on Wednesday. European stock markets are in green territory, as European corporate earnings for the third quarter are being released. Earnings for the third quarter are expected to be 4.5 percent higher than a year ago, and the positive sentiment has led to gains for almost all of the companies on the CAC. In the financial sector, BNP Paribas is leading the way, with a strong gain of 1.37%. Credite Agricole is also higher, up 0.58%.

What’s next for Catalonia? The cat-and-mouse game between the Spanish and Catalan governments continues, as a Thursday deadline looms. The Spanish has given Catalan President, Carles Puigdemont until Thursday to recant his declaration of independence. If Puigdemont refuses, Madrid has threatened to trigger Article 155 of the Spanish constitution, which would allow the central government to disband the Catalan parliament and impose direct rule. However, this clause has never been used, and could set off a violent reaction in Catalonia, with emotions already at a fever pitch. The deepening constitutional crisis has led hundreds of companies to start leaving Catalonia, and the Standard and Poor’s rating agency has said that the region could face a recession if the situation is not resolve. Investment projects are at a standstill in the region, and if the situation worsens, investors could get nervous and the European stock markets could respond with losses.

Technical Outlook: Spot Gold – Bears Probe Below Daily Cloud: Fed Speakers In Focus Today

Spot Gold extends weakness into third straight day and probes below strong support at $1281 (daily cloud base). Long bearish daily candles of past two days weigh, with Tuesday's fall marking the biggest one-day loss in three weeks. Gold remains under pressure on stronger dollar and speculations about successor of Janet Yellen as chair person of US Federal Reserve, as President Trump favors more hawkish person and John Taylor is currently a front-runner. Daily Ichimoku studies are turning into full bearish setup on daily chart and favor further downside. Firm break below daily cloud and violation of another pivotal support at $1277 (Fibo 61.8% of $1260/$1306 upleg) will be strong bearish signal for extension towards $1271 (Fibo 76.4%). Speeches from several FOMC members will be in focus today for further signal of rate hike in December, which is widely expected as the latest data show around 90% chance of FOMC action in December.

Res: 1285, 1288, 1290, 1296

Sup: 1279, 1277, 1275, 1271

Technical Outlook: US CRUDE – Bulls Are Pausing Ahead Of Crude Inventories Data

WTI oil holds positive tone on Wednesday and holding in tight range around $52.00 handle but without clear-near-term direction.

Underlying bull-trend remains intact but Tuesday’s close in long-legged Doji signaled indecision under fresh nearly three-week high at $52.35.

Upbeat release of API Crude stocks data on Tuesday (7.1 mln bls draw vs 4.2 mln bls draw forecasted) was not enough to push the price higher as concerns of supply disruption from Iraqi oilfields eased after Iraqi troops took control of Kirkuk area.

Also, overbought slow stochastic on daily chart weighs on near-term action and may generate bearish signal on reversal.

Focus turns towards EIA Crude stocks report, due later today. Forecasts show draw in crude inventories for 1.45 million barrels, signaling oil stocks fell for the fourth straight week, which is expected to be supportive for final push towards key barrier at $52.84.

Near-term action is supported by thick hourly cloud (spanned between $51.88 and $51.60) which should ideally limit downside attempts.

Deeper dips are expected to find ground at $51.00 zone (rising 20SMA).

Res: 52.15, 52.35, 52.84, 53.18

Sup: 51.88, 51.60, 51.20, 51.00

XAUUSD Analysis: Tests Ascending Channel

Due to release of better than expected data on import prices the buck appreciated quite sharply against the gold and has practically reached the bottom boundary of a medium ascending channel. From daily perspective it seems that bears are going to try to drag the pair to the 61.8% Fibonacci retracement level at 1,278.96. On hourly chart such scenario is supported by the 200-hour SMA, which is now located above the current market price. However, in order to reach that target the rate has to pass through a combined support set up by the above channel’s boundary and the weekly S1. Although the average market sentiment is 61% bullish, it is unlikely that this support will manage to turn around the exchange rate (unless some unexpected fundamental event will occur).

USDJPY Analysis: Tries To Reach 112.60

During previous trading session, the Greenback continued to strengthen against the Yen, fluctuating in two minor ascending channels. At the moment, the turnaround of the rate seems unlikely, as the southern side is reliably secured by a combination of the 55- and 100-hour SMAs in conjunction with the weekly PP at 112.13. In contrast, the closest resistance level except for the 200-hour SMA is located only near the 112.57 and is formed by the weekly R1 and the upper boundary of one of the above patterns. In larger perspective there is a need to take into account that the pair is approaching the upper boundary of a dominant falling wedge pattern, which means that another rebound most probably is going to happen in the nearest future.

GBPUSD Analysis: Loses 100 Points

Although inflation report matched with forecasts and Gov Carney again admitted possibility of interest rate hike, the Pound lost almost 100 points against the Dollar just in couple of hours. Such keen reaction shows that the main investors’ concern is related to success of the Brexit talks. From technical perspective, the cable passed through the 200-hour SMA and now is facing to other support barriers on its way up until the 38.2% Fibonacci retracement level at 1.3145. In this sense, the pair is expected to continue to slip to the bottom. However, there is a need to take into account that after such sharp falls traders usually tend to restore lost positions, which means that an area near 1.326 might become a target once again (as long as market sentiment remains predominantly bullish)

EUR/USD Breaks Through 200-Hour SMA

In accordance with expectations, the Dollar continued to gain value against the common European currency, experiencing pressure from the 55-, 100- and 200-hour SMAs as well as the weekly PP. Despite the fact that the pair failed to pass through the weekly S1 at 1.1735 from the first attempt, it is still expected to move in the southern direction, trying to reach the 100% Fibonacci retracement level at 1.1715. This scenario is supported not only by the average market sentiment, which remains 57% bearish, but also by an aggregate of technical indicators, which sends strong sell signal for this trading session. The only event than might add some volatility in the markets and lead to short-term recovery of the Euro are opening remarks that will be delivered by Mr. Draghi at the ECB conference.

EUR/USD: US Import Prices, Industrial Production

The Euro kept falling against the Greenback after the row of releases showing mostly strong results for the US. The EUR/USD currency pair lost 12 base points to touch the weekly low of 1.1744. Though, bulls managed to change the direction of the trend.

The Labour Department showed that the US import prices grew at the strongest pace of 0.7% in more than a year in September, due to higher costs of food and petroleum. Meanwhile, underlying inflation marked a modest increase of 0.3% in the reported period. The following report from the Fed showed that the US industrial production gained 0.3% in the prior month amid fading effects of Hurricanes Irma and Harvey, allowing utilities output to bounce back.