Sample Category Title

Elliott Wave Trade Ideas Performance Update

5 positions were entered last week with total profit of 165 points and the positions are listed below.

16 Oct : AUD/USD - Short at 0.7875, exited at 0.7700 ( + 175 points)

24 Oct : EUR/JPY - Long at 133.20, exited at 133.50 (+ 30 points)

24 Oct : GBP/JPY - Long at 149.50, exited at 149.70 (+ 20 points)

26 Oct : GBP/USD - Short at 1.3175, exited at 1.3235 (- 60 points)

31 Oct : GBP/JPY - Short at 150.00,

| AUD EUR/JPY EUR/GBP CAD GBP GBPJPY

Jan - 15 -275 - 35 -120

Feb + 140 -17 - 40 +11

Mar - 20 +115 +132 - 19

Apr + 30 - 40 +120 + 45

May - 55 +100 - 6 -65 -60

Jun + 81 +150 - 10 +185 -120 +205

Jul - 40 - 60

Aug +155 +200 + 100 + 195 -45 - 50

Sep -50 + 165 + 5

Oct + 175 - 30 - 80 - 25 +140 +220

Nov

Dec

Y-T-D + 546 +38 + 87 +798 - 90 +305

Canadian GDP Fell by 0.1% Sending Loonie Lower

Despite positive data published in the Eurozone today, the EUR/USD price was still not able to lift out of the doldrums it's been in recently. The unemployment rate in the Eurozone declined to its lowest level since 2009 reaching 8.9%, which is 0.1% lower than expected. The preliminary report on GDP showed growth in the Eurozone of 0.6% in the third quarter against the 0.5% expected but was still not able to offset the negative sentiment of investors concerning the euro. Meanwhile, the consumer confidence index published by the conference board in the US improved marginally with the index now at 125.9, up from 120.6 in September. Traders are in no hurry to build up positions ahead of the FOMC statement on monetary policy which will be released tomorrow. In case of hawkish rhetoric and the rising possibility of an interest rate hike in December, we are likely to see the fall of the EUR/USD quotes continue.

The USD/JPY is trying to restore previously lost positions. The Japanese yen was under pressure following the statement of the Bank of Japan, according to which the monetary policy settings will remain ultra-soft until inflation reaches 2.0%. This stance by the Japanese regulator may result in continued rising dynamics for the pair, especially if monetary tightening in the US come through as expected.

The Canadian dollar kept falling today and the trigger for another powerful impulse has come from weak GDP data in Canada, according to which the country's economy contracted by 0.1% in August against an expected increase of 0.1%. Markets are likely to remain nervous in the next couple days and we may see sharp moves in different directions.

EUR/USD

The EUR/USD quotes are consolidating above the important 1.1620 level below which the price could not fix previously. The possible rising movement may be limited by resistance at 1.1700 but it is more likely that we'll see negative dynamics resume with the closest targets at 1.1550 and 1.1500. After the completion of the current consolidation, we are likely to see a growth in volatility.

USD/JPY

The USD/JPY quotes resumed their positive dynamics after they could not fix below the support at 113.00 and returned to the SMA100 on the 15-minute chart. The immediate objectives, if the current impulse continues, will be at 114.00 and 114.70. On the other hand, confirmation of the signal to sell may come from fixing under the support at 113.00.

USD/CAD

The USD/CAD has grown significantly after a long consolidation above 1.2800. Gaining a foothold above 1.2800 has become a strong basis for a future increase with potential targets at 1.3000 and 1.3200. The RSI on the 15-minute chart is in the overbought zone which indicates the possibility of a price correction. The amplitude of price fluctuations is likely to increase during the next couple sessions.

Loonie Falls Sharply on GDP Miss; Pound Boosted on Barnier; Eurozone Readings Mixed

The Canadian dollar lost ground versus its US counterpart as GDP figures unexpectedly reflected a contraction in the Canadian economy. Eurozone data on inflation, economic growth and unemployment out during today's session gave a mixed picture. The pound moved higher after some comments by Michel Barnier, the EU's chief Brexit negotiator, which suggested that Brexit talks are getting on the right path, while the dollar advanced following upbeat figures on consumer confidence.

The dollar's index against a basket of currencies was trading 0.05% higher on the day at 1458 GMT and was looking set to record its biggest monthly gain since February. On the month, the index is up by 1.6%. This also constitutes the second straight month of advances after retreating in the five months that preceded. Dollar/yen was last 0.2% up at 113.44, recovering from the 11-day low of 112.95 hit earlier in the day. The Fed's two-day meeting on monetary policy will be completed tomorrow. Policymakers are widely expected to hold rates steady and proceed with a 25bps rate hike in December.

Eurozone flash inflation figures for the month of October showed headline and core inflation easing to 1.4% y/y and 1.1% y/y respectively from September's 1.5% and 1.3%. The numbers were also below analysts' projections – headline inflation was expected to rise on an annual basis by 1.5% and core inflation by 1.2%.

Preliminary third quarter GDP estimates showed eurozone economies growing by 0.6% q/q. This was below Q2's upwardly revised 0.7% (from 0.6%) and above expectations of 0.5%. Year-on-year, growth accelerated by 2.5% from Q2's 2.3% and came in above the anticipated 2.4%. The unemployment rate also positively surprised, falling to its lowest since January 2009 as unemployment in the euro area continues to decline. September's unemployment rate stood at 8.9%, below the 9.0% forecasted by analysts. The respective rate in August was revised downwards to 9.0% from 9.1%.

Euro/dollar fell to the day's low of 1.1623 within minutes of the above data going public – all were released at 1000 GMT – with the weaker-than-expected inflation readings apparently carrying more weight (though the reaction in the forex markets upon data release was not significant). Soon after the euro made up for its losses relative to the greenback though. The pair last traded 0.1% lower on the day at 1.1635.

Monthly data on Canadian GDP showed the economy contracting by 0.1% m/m in August, falling short of expectations of growth by 0.1% – the economy stalled in July with the growth rate at 0%. The previous time the economy shrank was in October 2016. The contraction was partially attributed to maintenance shutdowns in the chemical and extractive industries and is consistent with last week's decision by the Bank of Canada to cut its projections for Q3 annualized growth to 1.8% from 2.0%. Figures on September producer prices released at the same time (1230 GMT), showed prices declining by 0.3% m/m, contrasting expectations for a rise by 0.4%. It should be mentioned though that many vehicles are priced in US dollars and thus become cheaper when the Canadian currency rises. In this instance, the strengthening Canadian dollar played a role in falling producer prices as had the dollar/loonie pair remained constant, the producer price index would have instead increased by 0.3% during the month.

Dollar/loonie rose sharply as the above readings went public to eventually rise to the day's high of 1.2914 (within breathing distance of Friday's three-and-a-half-month high of 1.2916). Before the release, the pair traded at 1.2837. Dollar/loonie was last 0.5% up on the day and not far below the 1.29 mark. The Governor of the Bank of Canada, Stephen Poloz, will, alongside Senior Deputy Governor Carolyn Wilkins, appear before the House of Commons Standing Committee on Finance at 1930 GMT.

In US data, the S&P CoreLogic Case-Shiller home price index showed a 6.1% annual increase in August to hit a record high. The gain was above the 5.8% anticipated by analysts while exceeding July's rise by 5.9%. Later in the session, the Conference Board's consumer confidence index outstripped expectations of 121.0 to stand at 125.9 during October, its highest since December 2000. September's reading was upwardly revised to 120.6 from 119.8. The dollar index moved higher following the release.

The British currency was boosted after Michel Barnier indicated that Brexit negotiations are ready to move forward. Pound/dollar was last up by 0.3%, trading not far below 1.3250, a level the pair breached earlier in the day. Euro/pound was 0.4% lower, trading near the one-month low of 0.8775 recorded today.

Kiwi/dollar was last trading 0.6% down on the day at 0.6833 ahead of Q3 employment figures for New Zealand due at 2145 GMT.

In commodities, gold was 0.5% lower, trading at $1,269.31 an ounce. The dollar-denominated metal tends to record losses whenever the greenback strengthens. WTI was lower by 0.2% and Brent crude down on the margin. The two benchmarks traded at $54.02 and $60.89 a barrel respectively. Despite the fall, they were both near their recently recorded multi-month highs. The American Petroleum Institute's (API) weekly data, including on crude stocks, will be released at 2030 GMT.

Candlesticks and Ichimoku Trade Ideas Performance Update

3 positions were entered among all 4 currency pairs with total loss of 65 points and the positions are listed below:

25 Oct : GBP/USD - Short at 1.3185, exited at 1.3220 (- 35 points)

25 Oct : USD/JPY - Long at 113.80, exited at 113.50 (- 30 points)

31 Oct : GBP/USD - Short at 1.3255,

| JPY EUR CHF GBP

Jan + 167 - 85 - 10 + 50

Feb + 200 +150 +93 - 59

Mar -23 -70 -23 - 35

Apr + 65 + 93 + 50 - 40

May - 65 - 35 + 100 -175

Jun -100 -10 - 10 +175

Jul + 85 - 35 - 8

Aug + 35 +210 + 35 +65

Sep +129 +210 +200 - 70

Oct - 35 +2 - 90 - 65

Nov

Dec

Y-T-D + 427 +425 +337 -144

EUR/USD Drifts Slightly Lower in Wait-and-SeeSession

- European equities had a dull session, as recent gains are digested. Nevertheless some new (cycle or all-time) highs were registered (EuroStoxx), but daily gains are minor. Madrid still outperforms. US equities opened virtually unchanged (S&P/Dow) to slightly higher (NASDAQ).

- The euro zone economy grew faster than expected last quarter (0.6% Q/Q from an upwardly revised 0.7% Q/Q in Q2) and unemployment fell to its lowest (8.9%) in almost nine years. Inflation disappointed though with an unexpected setback in both headline (1.4% Y/Y) and core (0.9% Y/Y) readings.

- US eco data printed very strong. The Chicago PMI rose from 65.2 to 66.2 in October, the highest level since 2011. Consumer confidence rose to its highest level since 2000 (125.9) with both "present situation" and "expectations" components increasing. US labour costs accelerated in Q3 (0.7% Q/Q), leading to the biggest Y/Y increase in 2-1/2 years and offering hope that wage growth was finally gaining momentum amid a tightening labour market.

- Carles Puigdemont has said he will carry on the struggle for Catalan independence from Brussels, styling himself as the turbulent region's legitimate leader despite being ousted by the Spanish government over the weekend. He signalled that he would accept the regional election on Dec. 21

- Britain is speeding up preparations for leaving the EU, employing thousands more workers to make sure customs posts, laws and systems work on day one of Brexit, PM May's spokesman said. EU's chief Brexit negotiator, Barnier, said he was ready to speed up divorce negotiations with Britain.

Rates

EMU/US eco data fail to leave trace on markets

Global core bonds lost marginal, technically insignificant, ground today. European trading was muted because of a German holiday. Several EMU/US eco data failed to leave permanent traces. We've argued before that the ECB downgraded the significance from EMU eco data for the next couple of months by extending its APP-programme by 9 months. The mixed bag of strong GDP, a drop in the unemployment rate and disappointingly low (core) inflation was easily put aside. The impact of very strong US eco data was even smaller. Tomorrow's FOMC meeting will be a non-event while a December rate hike is largely discounted (87% probability). To wrap up: activity data remain strong on both sides of the Atlantic while (EMU) inflation is invisible. The trading session though is one to rapidly forget about.

At the time of writing, changes on the German yield curve range between -0.1 bp (30-yr) and +1.3 bps (5-yr). The US yield curve flattens with yield changes varying between + 1 bp (2-yr) and -0.5 bps (30-yr). On intra-EMU bond markets, 10-yr yield spreads versus Germany narrow up to 3 bps.

Currencies

EUR/USD drifts slightly lower in wait-and-see session

The euro traded with a negative bias against the dollar today, but losses were minimal. EMU activity data were strong with GDP up 0.6% Q/Q in Q3 and the unemployment rate dropping below 9% for the first time since the financial crisis. This was intrinsically euro positive news, but it came alongside weaker-than-expected EMU inflation. Headline inflation dropped to 1.4% Y/Y and core inflation dropped below 1% again. The latter was still a bit of a surprise even after the weak German inflation figures released yesterday. That was euro negative and the combination actually kept EUR/USD little changed in the tight 1.1625 to 1.1650 range. The early US data releases, employment cost index (0.7% Q/Q) and the S&P house prices were bang in line with expectations, leaving once more the dollar unchanged. However, the mid-session Chicago PMI (66.2 versus 60 expected) and the Consumer confidence (setting a 17-year high) were very strong and stronger than expected. EUR/USD briefly went to the session lows (1.1625), but conviction was once more missing. Concluding, eco data had little impact, as investors await the Fed and BoE meeting and the US payrolls. The sharp two day post ECB sell-off in the euro is over.

USD/JPY had an uneventful session, even if it gained minor ground in the European and early US session. It rose from 113.20 to 113.50 and now trades at 113.40. The Bank of Japan left its monetary stimulus program, as expected, unchanged today (8-to-1) and trimmed its inflation forecasts, echoing the European Central Bank's cautious tone. Kuroda contributed to the dovishness at his press conference. He rejected the notion the BOJ should start discussing its exit plan as it is still far from its inflation target. So, the dollar performance against the yen was in fact very weak. Ever since the pair rejected the 114.55 resistance last week, dollar bulls saw no reason to go for another test. Yields, EUR/USD rate differentials and nearly unchanged equities were another reason for the unattractive FX session.

Sterling makes headway ahead of BoE meeting

Sterling extended its winning streak against the euro to 5 sessions. Technicals still underpin the sterling rally as do fundamentals with markets awaiting a rate hike on Thursday and the ECB still firmly on the dovish side, pushing forward any serious normalization of its ultra-easy policies. EUR/GBP dropped from openings levels around 0.8820 to 0.8780 currently. The lion part of the sterling gains followed comments of EU chief Brexit negotiator Barnier who said he is ready to speed up negotiations. The going will soon get tougher for sterling. For the UK currency to extend recent gains, the BoE should signal that this is more than a one-and-done deal. That's unlikely. Inflation is above 2%, but largely on the back of a weaker sterling, not due to an overheating economy. Inflation expectations look well anchored and Brexit risk remains as high as it was. Growth is rather subdued and probably will slow further as households' spending capacity is retrenching. Technically, EUR/GBP has now approached the 0.8756 support with the target of the double top at 0.8677 and the June low support at 0.8652. We expect the sterling correction to fizzle out before/at these supports after the BoE meeting Thursday. A buy EUR/GBP on dips closer to these levels is favoured.

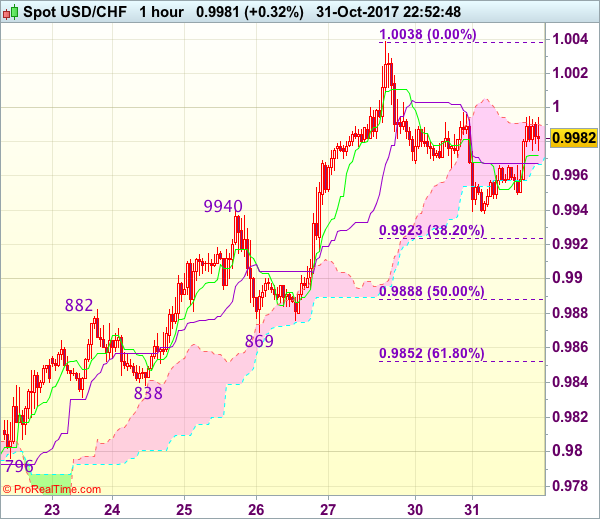

Trade Idea Wrap-up: USD/CHF – Buy at 0.9915

USD/CHF - 0.9982

Most recent candlesticks pattern : N/A

Trend : Up

Tenkan-Sen level : 0.9972

Kijun-Sen level : 0.9967

Ichimoku cloud top : 0.9990

Ichimoku cloud bottom : 0.9967

Original strategy :

Buy at 0.9915, Target: 1.0030, Stop: 0.9880

Position : -

Target : -

Stop : -

New strategy :

Buy at 0.9915, Target: 1.0030, Stop: 0.9880

Position : -

Target : -

Stop : -

Although dollar has recovered from 0.9938, reckon 1.0000 would limit upside and near term downside risk remains for the corrective fall from 1.0038 (last week’s high) to bring retracement of recent rise to 0.9920-25 (38.2% Fibonacci retracement of 0.9737-1.0038), however, reckon 0.9905-10 would limit downside and bring another rise later, above 1.0000 would bring retest of said resistance at 1.0038, break there would extend recent rise from 0.9421 low to 1.0050-55, then towards 1.0075-80 but price should falter below 1.0100 resistance.

In view of this, we are looking to buy dollar again on pullback as 0.9915-25 should limit downside, bring another rise later. Below 0.9885-90 (50% Fibonacci retracement of 0.9737-1.0038) would defer and suggest top is possibly formed, risk test of support at 0.9869.

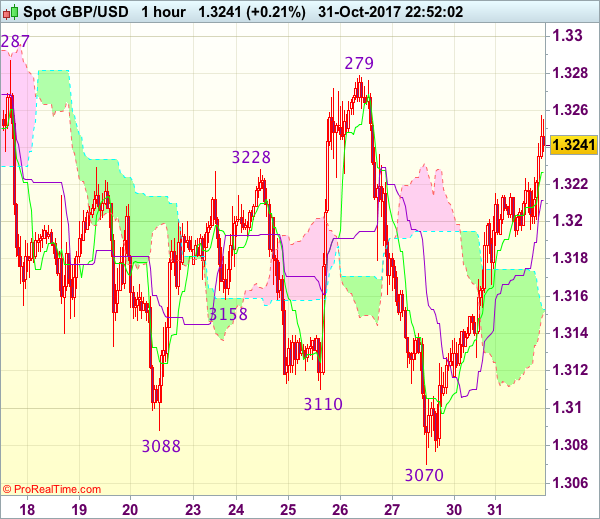

Trade Idea Wrap-up: GBP/USD – Hold short entered at 1.3255

GBP/USD - 1.3243

Most recent candlesticks pattern : N/A

Trend : Sideways

Tenkan-Sen level : 1.3227

Kijun-Sen level : 1.3212

Ichimoku cloud top : 1.3153

Ichimoku cloud bottom : 1.3152

Original strategy :

Sold at 1.3255, Target: 1.3135, Stop: 1.3290

Position : - Short at 1.3255

Target : - 1.3135

Stop : - 1.3290

New strategy :

Hold short entered at 1.3255, Target: 1.3135, Stop: 1.3290

Position : - Short at 1.3255

Target : - 1.3135

Stop : - 1.3290

As cable has maintained a firm undertone after staging a strong rebound from 1.3070, suggesting near term upside risk remains for marginal gain, however, as broad outlook remains consolidative, reckon upside would be limited and indicated strong resistance at 1.3279-87 would remain intact, bring retreat later, below 1.3190 would suggest an intra-day top is formed, bring weakness to 1.3150-55 but break of 1.3120-25 is needed to signal the rebound from 1.3070 has ended, then further fall to 1.3100, then retest of 1.3070 would follow.

In view of this, we are holding on to our short position entered at 1.3255. Only above indicated strong resistance at 1.3279-87 would abort and shift risk to the upside for the erratic rise from 1.3027 low is still in progress for further gain to 1.3300-10, then towards 1.3340-50.

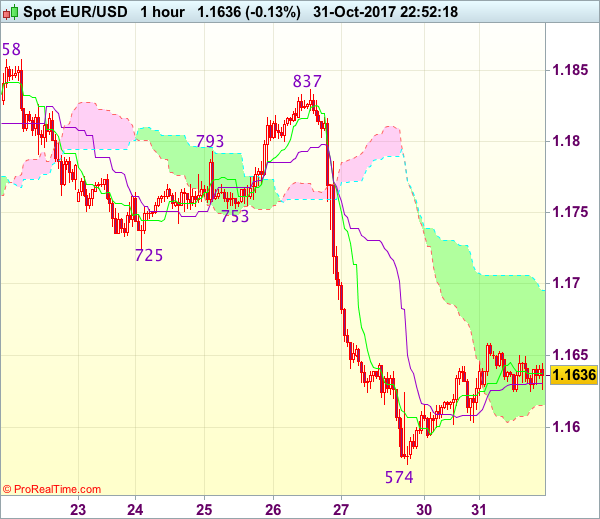

Trade Idea Wrap-up: EUR/USD – Sell at 1.1700

EUR/USD - 1.1635

Most recent candlesticks pattern : N/A

Trend : Down

Tenkan-Sen level : 1.1637

Kijun-Sen level : 1.1631

Ichimoku cloud top : 1.1696

Ichimoku cloud bottom : 1.1615

Original strategy :

Sell at 1.1700, Target: 1.1595, Stop: 1.1735

Position : -

Target : -

Stop : -

New strategy :

Sell at 1.1700, Target: 1.1595, Stop: 1.1735

Position : -

Target : -

Stop : -

Euro’s recovery after falling to 1.1574 late last week has retained our view that further consolidation above this level would be seen and corrective bounce to 1.1660-65 cannot be ruled out, however, reckon upside would be limited to the upper Kumo (now at 1.1706) and bring another decline later, below said support at 1.1574 would extend recent decline from 1.2093 top to 1.1550-55 but loss of downward momentum should prevent sharp fall below 1.1520-25 and reckon 1.1500 would hold from here.

In view of this, we are looking to sell euro on subsequent recovery as the upper Kumo (now at 1.1706) should limit upside and bring another decline. Only above previous support at 1.1725 (now resistance) would signal low is formed instead, bring retracement of recent decline to 1.1750-55 first.

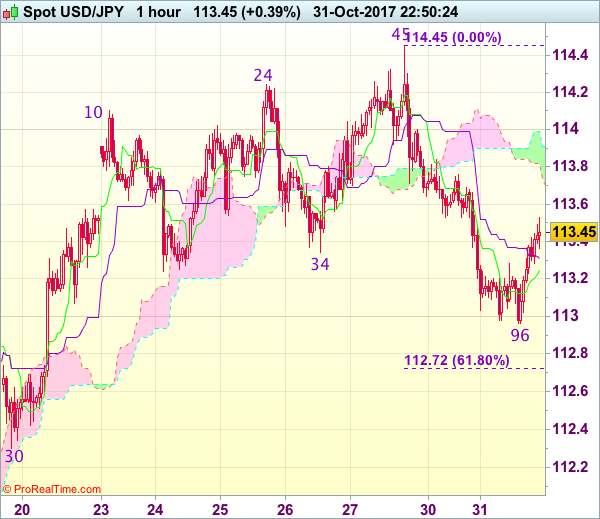

Trade Idea Update: USD/JPY – Sell at 114.10

USD/JPY - 113.43

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 113.25

Kijun-Sen level : 113.31

Ichimoku cloud top : 113.99

Ichimoku cloud bottom : 113.82

Original strategy :

Sell at 114.00, Target: 113.00, Stop: 114.35

Position : -

Target : -

Stop : -

New strategy :

Sell at 114.10, Target: 113.00, Stop: 114.45

Position : -

Target : -

Stop : -

As the greenback has rebounded after finding support just below 113.00, suggesting consolidation above 112.96 intra-day low would be seen and initial recovery to 113.70-75 is likely, however, reckon upside would be limited to 114.00-10 and price should falter well below resistance at 114.45-50, bring another retreat later, below said support at 112.96 would add credence to our view that top has been made, bring retracement of recent upmove to 112.70-75 (61.8% Fibonacci retracement of 111.65-114.45) but oversold condition should limit downside to 112.50 and reckon previous support at 112.30 would hold.

In view of this, we are looking to sell dollar on recovery but at a higher level as 114.00-10 should cap upside and bring another decline. Above 114.25 would signal the retreat from 114.45 has ended, bring retest of indicated strong resistance at 114.45-50 which is likely to hold on first testing.

Eurozone GDP Accelerates in Q3, but Inflation Remains Weak

Third quarter GDP growth in the Eurozone beat consensus expectations, rising 2.5 percent year-over-year. The recovery appears to be increasingly broad-based, but inflation has remained quite tame.

Third Quarter Print Reaches New Cycle High

Real GDP in the Eurozone expanded 2.5 percent year-over-year in Q3, the fastest year-over-year growth rate since Q1-2011. Real GDP grew 0.6 percent on a quarterly basis (not annualized), and both the quarterly and year-ago growth rates were above the Bloomberg consensus.

While Q3 GDP data broken down into its underlying demand components are not yet available, today's print is in line with the continued improvement in the Eurozone economy over the past few quarters. Data released this morning on the French economy, one of the largest in the Eurozone, offer a glimpse into economic growth in the Eurozone on a more detailed level. Real GDP in France accelerated to a 2.2 percent year-overyear pace, the strongest growth since 2011, and the underlying data affirmed continued broad-based growth for the quarter, with household consumption, business fixed investment and public sector expenditures all accelerating on a year-over-year basis.

A strengthening labor market in the Eurozone likely helped boost Q3 output. Eurozone unemployment data released today showed the unemployment rate at 8.9 percent for September, down from a revised 9.0 percent in August and the 9.6 percent rate registered to start 2017.

Stagnant Price Pressures Remain Area to Watch

Overall output growth and unemployment data reinforce positive economic trends, but inflation in the Eurozone maintained its sluggish pace of growth in October. Advance estimates for CPI inflation showed price growth of just 1.4 percent year-over-year, below the consensus of 1.5 percent. Core CPI excluding food and energy also displayed weakness, with inflation of just 0.9 percent year-over-year. Core CPI growth had been showing some signs of accelerating over the past few months with readings north of 1 percent, but this morning's reading shows a loss of momentum.

Tame inflation was a key factor in the European Central Bank's (ECB) decision last week to reduce its monthly asset purchases but extend the program through September 2018 "or beyond, if necessary". The ECB's move to taper its purchases from €60 billion a month to €30 billion a month starting in January reflects the strengthening and broad-based economic recovery taking hold in Europe. However, with inflation in the euro area remaining benign, a complete removal of policy accommodation remains too aggressive a move for policymakers. The central bank kept its three policy rates unchanged, and it continued to stress that they would "remain at their present levels for an extended period of time, and well past the horizon of our net asset purchases." In short, rate hikes in the Eurozone are likely some ways off still.