Sample Category Title

CAC Edges Higher on Solid French Data

The CAC index continues to have a quiet week. Currently, the CAC is trading at 5,500.00, up 0.11% on the day. France released key economic data on Tuesday. Flash GDP remained at 0.5% in the third quarter, matching the estimate. The economy has been steady, as consumer spending has improved and business investment remains strong. Consumer Spending rebounded with a gain of 0.9%, beating the estimate of 0.6%. Preliminary CPI improved to 0.1%, matching the forecast. Eurozone data was mixed, as CPI Flash Estimate missed the estimate, while Preliminary Flash GDP beat the forecast. On Wednesday, the Federal Reserve will be in the spotlight, as the FOMC releases its monthly rate statement.

Eurozone indicators were a mix on Tuesday. CPI Flash Estimate edged down to 1.4%, shy of the forecast of 1.5%. Core CPI Flash Estimate dipped to 0.9%, short of the estimate of 1.1%. There was better news from Preliminary Flash GDP, which remained unchanged at 0.6%, above the estimate of 0.5%. On the employment front the unemployment rate head lower, dropping to 8.9%. This is the lowest level since March 2009. The ECB has announced that it will begin tapering its asset purchase program, as the eurozone economy has rebounded in 2017. Still, inflation remains persistently below the ECB's target of around 2 percent. The asset purchase program has been extended to April 2018, but the ECB could implement an extension if economic data tails off or if inflation fails to move upwards.

The uncertainty and tension remain at fever pitch in Catalonia. The central government has dissolved the Catalan government and parliament, after imposing direct rule on Catalonia. The Catalan government declared independence just before Madrid invoked Article 155 of Spain's constitution. The Spanish government has drawn up charges of rebellion against Catalan President Carles Puidgemont, but he has skipped town, and is reportedly in Belgium. It remains unclear what Puidgemont will do next – he could request political asylum or even declare a government-in-exile. Elections have been slated for December 21, and two parties from Puidgemont's coalition have declared they will participate in the election. With Catalans split down the middle on independence, this saga is likely to continue for some time.

Trade Idea: EUR/GBP – Sell at 0.8885

EUR/GBP - 0.8785

Original strategy :

Sell at 0.8900, Target: 0.8755, Stop: 0.8940

Position : -

Target : -

Stop : -

New strategy :

Sell at 0.8885, Target: 0.8755, Stop: 0.8915

Position : -

Target : -

Stop : -

As the single currency has remained under pressure after recent selloff, suggesting the decline from 0.9033 top is still in progress and may extend further weakness towards previous support at 0.8746-50, however, break there is needed to confirm early decline from 0.9307 has resumed and extend fall to 0.8720, having said that, near term oversold condition should limit downside and reckon 0.8700 would hold from here.

In view of this, we are looking to sell euro again on recovery, above 0.8845-50 would bring corrective bounce to 0.8880-85 where renewed selling interest should emerge and bring another decline later. Only above 0.8957 resistance would abort and shift risk to upside for test of 0.8976 but reckon upside would be limited to 0.9000 and said resistance at 0.933 should remain intact, bring another decline later.

Our preferred count is that, after forming a major top at 0.9805 (wave V), (A)-(B)-(C) correction is unfolding with (A) leg ended at 0.8400 (A: 0.8637, B: 0.9491 and 5-waver C ended at 0.8400. Wave (B) has ended at 0.9413 and impulsive wave (C) has either ended at 0.8067 or may extend one more fall to 0.8000 before prospect of another rally. Current breach of indicated resistance at 0.9043 confirms our view that the (C) leg has ended and bring stronger rebound towards 0.9150/54, then towards 0.9240/50.

Trade Idea: USD/CAD – Buy at 1.2755

USD/CAD - 1.2893

Trend: Near term up

Original strategy :

Buy at 1.2755, Target: 1.2955, Stop: 1.2695

Position: -

Target: -

Stop: -

New strategy :

Buy at 1.2755, Target: 1.2955, Stop: 1.2695

Position: -

Target: -

Stop:-

As the greenback has maintained a firm undertone after recent rally, adding credence to our view that the rise from 1.2061 low is still in progress and mild upside bias remains for this move from there (wave iii trough) to extend gain to 1.2950, having said that, as we are still treating this rebound from 1.2061 as wave iv, reckon 1.2975-80 (61.8% Fibonacci retracement of wave iii) would limit upside and 1.3000 should hold, bring selloff later in wave v. We are keeping our count that wave v as well as wave (C) ended at 1.3794 and impulsive wave (i ii, i ii) is now unfolding with minor wave iii ended at 1.2414, followed by wave iv correction ended at 1.2778, wave v has reached our indicated downside target at 1.2100 and may extend to 1.2000.

In view of this, we are looking to reinstate long on subsequent pullback as 1.2750-55 should limit downside and bring another rise. Below 1.2725-30 would defer and suggest a temporary top is possibly formed, bring correction to 1.2690-00 but break of support at 1.2635-40 is needed to confirm, bring weakness to 1.2610-15, then test of 1.2591.

To recap, wave B from 1.3066 is unfolding as an a-b-c and is sub-divided as a: 1.2192, b: 1.2716 and wave c is a 5-waver with i: 1.1983, ii: 1.2506, extended wave iii with minor iii at 1.0206, wave iv ended at 1.0781 and wave v as well as wave iii has ended at 0.9931, hence the subsequent choppy trading is the wave iv which is unfolding as (a)-(b)-(c) with (a) leg of iv ended at 1.0854, followed by (b) leg at 1.0108 and (c) leg as well as the wave iv ended at 1.0674. The wave v is sub-divided by minor wave (i): 0.9980, (ii): 1.0374, (iii): 0.9446, (iv): 0.9913 and (v) as well as v has possibly ended at 0.9407, therefore, consolidation with upside bias is seen for major correction, indicated target at 1.3700 and 1.4000 had been met and further gain to 1.4700 would be seen later.

US: ECI Shows More Signs of Rising Labor Costs

Employment costs rose 0.7 percent in the third quarter and are up 2.5 percent over the past year. A tight labor market points to further strengthening ahead.

Compensation Costs Quicken in Q3

In another sign of a tight labor market, employment costs rose 0.7 percent in the third quarter. At 2.5 percent, the employment cost index (ECI) is just shy of the post-recession high hit briefly in 2015 and is ahead of the 2.3 percent increase registered this time last year.

The third quarter increase was driven by a pickup in both wages & salaries and benefits. Wages & salaries rose 0.7 percent, one of the strongest quarterly gains this expansion. Excluding incentive paid occupations, wages & salaries rose a bit more modestly (up 0.6 percent), but have increased in line with all workers at 2.5 percent over the past year. Growth in wages & salaries was led by the private sector, with particularly strong gains in professional & business services, manufacturing and transportation & warehousing.

Wage costs in the private sector continue to outpace the government sector. In contrast, benefit costs continue to rise more quickly for government workers, up 0.8 percent versus 0.7 percent for private sector workers in Q3. In recent years, benefits costs have been growing more in line with wages & salaries as employer spending on health benefits has slowed to its lowest rate on record. This may be due in part to employers passing more of the cost burden onto employees and/or employees switching to slimmer plans in an effort to reduce their own spending on healthcare.

Employment Costs Expected to Pick Up Further

The strengthening in employment costs, particularly the wages & salaries component, is consistent with the firming in average hourly earnings. Looking at the drivers of both average hourly earnings and the ECI, we expect to see wages and compensation costs pick up over the coming year. The unemployment rate has fallen below both the Fed and Congressional Budget Office's estimates of full employment, indicating labor has become relatively scarce. That scarcity has been echoed in the share of small businesses reporting that they have at least one hard to fill job opening.

While at cycle highs, the quit rate implies a more moderate pace of strengthening in compensation as it has moved sideways since the start of the year and remains a bit below the levels of the past expansion. Voluntary quits tend to be associated with higher wage growth as most workers do not switch jobs without being offered higher compensation. Indeed, the Atlanta Fed's Wage Growth Tracker shows the typical job switcher has seen earnings increase nearly a full percentage point faster than job stayers over the past year. The extent of the upturn in employment costs will also be limited, however, by low inflation expectations. Without much pricing power, businesses will remain cautious about raising compensation.

Canadian Economy Unexpectedly Dips in August

Highlights:

- Canadian GDP unexpectedly dropped 0.1% with goods-production sinking 0.7% reflecting declines in manufacturing (-1.0%) and mining (-0.8%).

- Service-producing industries managed an increase though the 0.1% gain was down from the 0.2% average gain evident over the last three months.

- Q3 GDP annualized growth is expected to remain positive though dropping to 1.7% from Q2's 4.7%.

Our Take:

August GDP unexpectedly dropped 0.1% following July's disappointing flat reading. Expectations going into the report were for a 0.1% increase. A key downward surprise was the 1.0% decline in manufacturing activity with the chemical component particularly weak. Some of the latter weakness was attributed to maintenance shutdowns which will eventually reverse though Statistics Canada also highlighted lower export demand. Mining activity was also weaker than expected dropping 0.8% with conventional oil and gas extraction sinking 5.2%. This weakness was partly attributed to maintenance shutdowns in some Newfoundland and Labrador production facilities.

As the various maintenance production shutdowns end, monthly activity should return to positive territory. This along with earlier strength assures that the Q3 average GDP increase will remain positive though in the wake of today's data we have lowered our annualized rate to 1.7% that is about one third of the 4.7% recorded in Q2. Given that the surge in activity in Q2 likely absorbed what slack was remaining in the economy resulting in a closing of the so-called output gap, the slowing is a not unwanted development. In fact, the Bank of Canada's latest forecast update indicated the expectation of such with a projected Q3 growth rate of 1.8%. Thus today's report remains generally consistent with the central bank's outlook as outlined in last week's policy statement of a likely further tightening though with the pace very gradual. In the wake of today's data there is the increasing probability of the next hike being delayed until 2018.

Canadian GDP Takes a Dip in August

The Canadian economy contracted 0.1% month-on-month in August.

The declines were fairly concentrated, as 12 of 20 major industries (representing about 60% of output) expanded during the month.

Indeed, it was the goods sector that held things back again in August, contracting 0.7% with all major sectors reporting a contraction in output. Manufacturing saw the largest decline, with chemical manufacturing particularly weak (recording the largest decline in 20 years, per Statistics Canada), reflecting both plant maintenance and softer export demand. Elsewhere, mining, quarrying and oil and gas recorded a third month of declining output. This was largely attributable to declines in convention oil and gas extraction resulting from maintenance shutdowns in Newfoundland and Labrador.

In contrast, the stalwart service side of the economy notched up a 17th straight month of expansion. Arts and entertainment (+0.7%) and wholesale trade (+0.4%) led the way. Of note, the real estate and rental/leasing sector gained 0.2% in August, as activity at real estate agents and brokers ticked up 0.3%, breaking a four month streak of declines.

Key Implications

Notch this one up for the Bank of Canada. With a number of shutdowns in the goods producing side of the economy leading to a modest contraction, third quarter growth is now tracking around 1.9% - in line with the Bank of Canada's forecast in last week's Monetary Policy Report.

With much of the Q3 weakness seemingly down to temporary factors, and growth still tracking above potential, there is no reason for Canadians to worry. Indeed, although there remain some wildcards, such as the impact of a strike in the auto sector, it is likely that output will come back to life in coming months, particularly given still encouraging signs from labour and housing markets.

For the Bank of Canada, as encouraging as it will likely be to see their near-term outlook confirmed, "data dependency" likely implies that they will want ongoing confirmation of their expectations, particularly the expected tick-up in growth in the fourth quarter. Such an outcome appears likely at this juncture, but requiring confirmation means that the most likely trigger point for the next rate increase remains January.

Dollar Trying to Strengthen after Solid Employment Cost Growth

Dollar is trying to regain upside momentum in early US session after positive economic data. But it's being overwhelmed by Sterling and struggles against Euro. US Employment cost index rose 0.7% in Q3, in line with expectation. Meanwhile, in annualized term, employment cost rose 2.5%, hitting a nine-year high. Wages as 70% of employment cost rose 0.7% in Q3 while benefits rose 0.8%. Steady rise in labor costs and wage is supportive to more rate hike by Fed to prevent the economy from being overheating. S&P Case-Shiller 20 cities house price rose 5.9% yoy in August.

The greenback is also supported by talks that US President Donald Trump will announce, on Thursday, to nominate current Fed Governor Jerome Powell to succeed Janet Yellen as Fed chair after next February. Powell is seen as a more hawkish policy maker than Yellen and could speed up Fed's tightening pace.

On the other hand, Canadian Dollar weakens again after GDP showed -0.1% mom in August, below expectation of 0.1% mom rise. IPPI dropped -0.3% mom in September versus expectation of 0.5% mom. RMPI dropped -0.1% mom versus expectation of 0.4% mom rise.

Eurozone growth strong, but inflation sluggish

Euro lacks a clear direction today after mixed economic data that show solid growth but sluggish inflation. Eurozone GDP growth slowed to 0.6% qoq in Q3, down from upwardly revised 0.7% qoq, beating expectation of 0.5% qoq. Annualized, Eurozone economic expanded by 2.5%, highest since 2011. Unemployment rate dropped to 8.9% in September, beating expectation of 9.0%. That's the lowest level in nearly 9 years since January 2009.

However, headline CPI slowed to 1.4% yoy in October, down from 1.5% yoy and missed expectation of 1.5% yoy. Core CPI slowed to 0.9% yoy, down from 1.1% yoy and below expectation of 1.1% yoy. The set of data gives a nod to ECB's plan in tapering asset purchase. But sluggish inflation also supports ECB's cautious stance in keeping options open for extending and expanding asset purchases again.

BOJ left stimulus unchanged, downgraded inflation forecasts

BoJ again voted 8-1 to leave the monetary policies unchanged today. The targets for short- and long-term interest rates stay at -0.1% and around 0%, respectively while the guideline for JGB purchases remains at an annual pace of about 80 trillion yen. Again, BoJ revised lower its inflation forecasts for FY 2017 and FY 2018 but maintained that for FY 2019. The central bank upgraded the GDP growth outlook for FY 2017 while leaving others unadjusted.

The new member Goushi Kataoka was the lone dissent as he voted against the yield curve control measure for two meetings in a row. He judged that 'monetary easing effects gained from the current yield curve were not enough for 2% inflation to be achieved around fiscal 2019'.

At the press conference, Governor Kuroda defended the yield curve control policy and the 2% target. As he suggested, the "main objective is to achieve 2% inflation and stably maintain price growth at that level. There's no change to our view that monetary policy must be guided to achieve this objective' and there is no need to change the yield targets".

More in BOJ Left Stimulus Unchanged, Downgraded Inflation Forecasts

Also released from Japan, household spending dropped -0.3% yoy in September versus expectation of 0.7% yoy. Industrial production dropped -1.1% mom versus expectation of -1.6% mom. Housing starts dropped -2.9% yoy versus expectation of -2.9% yoy.

China and South Korea to normalize relationship

China and South Korea agreed to restore normal diplomatic relationship, after a year of stand-off on South Korea's deployment of the so called Terminal High Altitude Area Defense (THAAD) system of the US. China disputed on it on worries that the powerful radar of THAAD could penetrate into its territory. South Korean Foreign Minister said in a statement today that "both sides shared the view that the strengthening of exchange and cooperation between Korea and China serves their common interests and agreed to expeditiously bring exchange and cooperation in all areas back on a normal development track."

Chinese Foreign Ministry maintained the opposition and reiterated that "China's position on the THAAD issue is clear, consistent and has not changed. But it also softened the stance and bit and hoped that South Korea would handle the issue appropriately. Overall, the news is seen as positive signal that China and South Korea are interested in improving their relationship, days before US President Donald Trump travel across the Pacific to visit the region.

China PMIs disappoint

The official China manufacturing PMI dropped to 51.6 in October, down from 52.4 and missed expectation of 52.1. Non-manufacturing PMI dropped to 54.3, down from 55.4. Overall, the data suggests that China's growth is on track to meet the government's target of 6.5% this year. Mild slowdown in manufacturing activity is seen as partly due to tighter environmental supervision, in particular in the north-eastern regions. While the stricter regulations will dampen growth in manufacturing sector, the overall impact should be negligible in the near term.

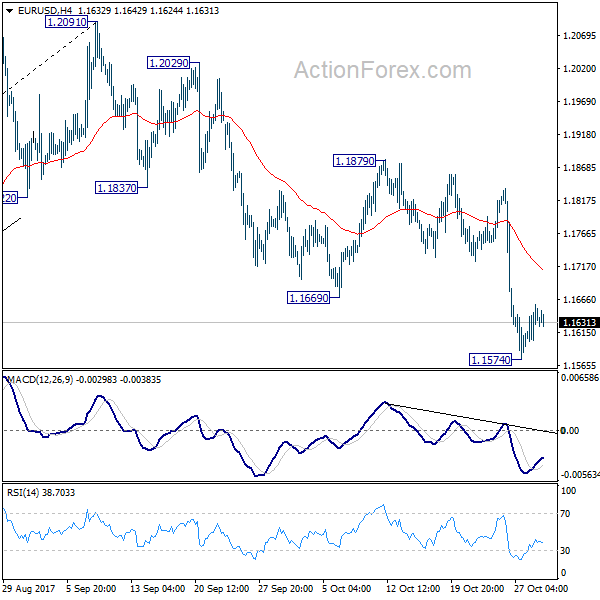

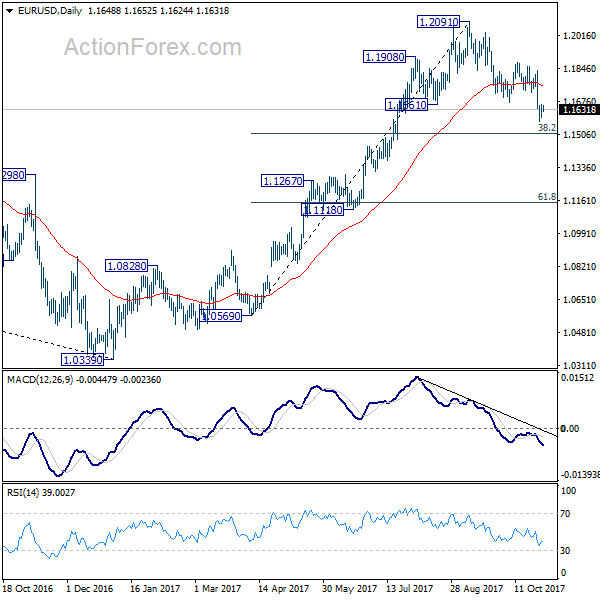

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1610; (P) 1.1634 (R1) 1.1675; More...

Intraday bias in EUR/USD remains neutral for consolidation above 1.1574 temporary low. Some consolidations could be seen. But still, break of 1.1879 resistance is needed to confirm completion of the decline from 1.2091. Otherwise, near term outlook will stay bearish. Below 1.1574 will target 38.2% retracement of 1.0569 to 1.2091 at 1.1510.

In the bigger picture, rise from 1.0339 medium term bottom is seen as a corrective move for the moment. Therefore, in case of another rally, we'd be cautious on 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 to limit upside and bring reversal. Meanwhile, sustained trading below 55 week EMA will suggest that such medium term rebound is completed and could then bring retest of 1.0339 low.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | Building Permits M/M Sep | -2.30% | 10.20% | 5.90% | |

| 23:30 | JPY | Unemployment Rate Sep | 2.80% | 2.80% | 2.80% | |

| 23:30 | JPY | Household Spending Y/Y Sep | -0.30% | 0.70% | 0.60% | |

| 23:50 | JPY | Industrial Production M/M Sep P | -1.10% | -1.60% | 2.00% | |

| 00:01 | GBP | GfK Consumer Confidence Oct | -10 | -10 | -9 | |

| 01:00 | CNY | Manufacturing PMI Oct | 51.6 | 52.1 | 52.4 | |

| 01:00 | CNY | Non-manufacturing PMI Oct | 54.3 | 55.4 | ||

| 03:05 | JPY | BoJ Policy Balance Rate | -0.10% | -0.10% | -0.10% | |

| 05:00 | JPY | Housing Starts Y/Y Sep | -2.90% | -3.20% | -2.00% | |

| 06:30 | EUR | French GDP Q/Q Q3 A | 0.50% | 0.50% | 0.50% | 0.60% |

| 06:30 | EUR | French GDP Y/Y Q3 A | 2.20% | 2.10% | 1.80% | |

| 10:00 | EUR | Eurozone Unemployment Rate Sep | 8.90% | 9.00% | 9.10% | 9.00% |

| 10:00 | EUR | Eurozone GDP Q/Q Q3 A | 0.60% | 0.50% | 0.60% | 0.70% |

| 10:00 | EUR | Eurozone CPI Estimate Y/Y Oct | 1.40% | 1.50% | 1.50% | |

| 10:00 | EUR | Eurozone CPI Core Y/Y Oct A | 0.90% | 1.10% | 1.10% | |

| 12:30 | CAD | GDP M/M Aug | -0.10% | 0.10% | 0.00% | |

| 12:30 | CAD | Industrial Product Price M/M Sep | -0.30% | 0.50% | 0.30% | 0.40% |

| 12:30 | CAD | Raw Materials Price Index M/M Sep | -0.10% | 0.40% | 1.00% | 0.90% |

| 12:30 | USD | Employment Cost Index Q3 | 0.70% | 0.70% | 0.50% | |

| 13:00 | USD | S&P/CS Composite-20 Y/Y Aug | 5.90% | 5.90% | 5.80% | |

| 13:45 | USD | Chicago PMI Oct | 60 | 65.2 | ||

| 14:00 | USD | Consumer Confidence Oct | 121 | 119.8 |

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1610; (P) 1.1634 (R1) 1.1675; More...

Intraday bias in EUR/USD remains neutral for consolidation above 1.1574 temporary low. Some consolidations could be seen. But still, break of 1.1879 resistance is needed to confirm completion of the decline from 1.2091. Otherwise, near term outlook will stay bearish. Below 1.1574 will target 38.2% retracement of 1.0569 to 1.2091 at 1.1510.

In the bigger picture, rise from 1.0339 medium term bottom is seen as a corrective move for the moment. Therefore, in case of another rally, we'd be cautious on 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 to limit upside and bring reversal. Meanwhile, sustained trading below 55 week EMA will suggest that such medium term rebound is completed and could then bring retest of 1.0339 low.

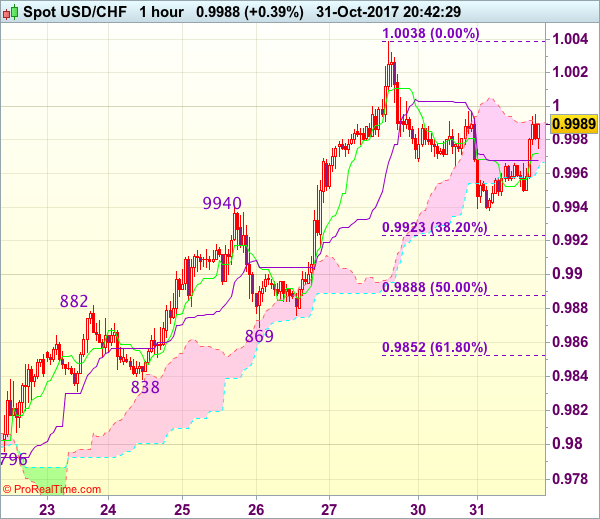

Trade Idea Update: USD/CHF – Buy at 0.9915

USD/CHF - 0.9988

Original strategy :

Buy at 0.9915, Target: 1.0030, Stop: 0.9880

Position : -

Target : -

Stop : -

New strategy :

Buy at 0.9915, Target: 1.0030, Stop: 0.9880

Position : -

Target : -

Stop : -

Although dollar has recovered from 0.9938, reckon 1.0000 would limit upside and near term downside risk remains for the corrective fall from 1.0038 (last week’s high) to bring retracement of recent rise to 0.9920-25 (38.2% Fibonacci retracement of 0.9737-1.0038), however, reckon 0.9905-10 would limit downside and bring another rise later, above 1.0000 would bring retest of said resistance at 1.0038, break there would extend recent rise from 0.9421 low to 1.0050-55, then towards 1.0075-80 but price should falter below 1.0100 resistance.

In view of this, we are looking to buy dollar again on pullback as 0.9915-25 should limit downside, bring another rise later. Below 0.9885-90 (50% Fibonacci retracement of 0.9737-1.0038) would defer and suggest top is possibly formed, risk test of support at 0.9869.

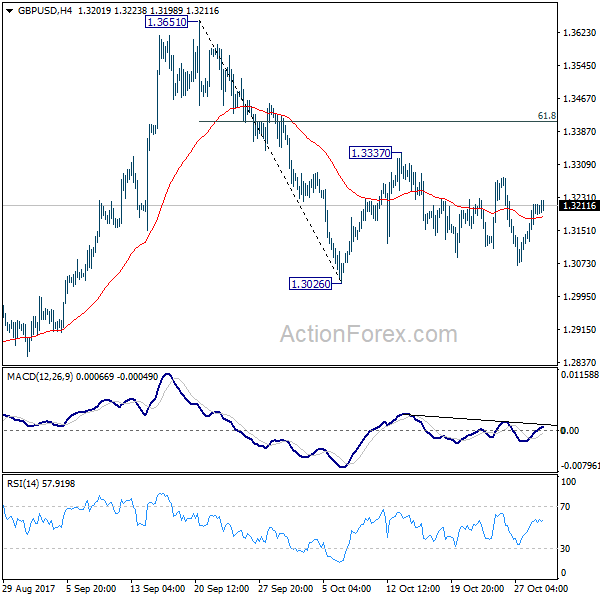

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3140; (P) 1.3177; (R1) 1.3243; More....

No change in GBP/USD's outlook as it's still bounded in range of 1.3026/3337. Intraday bias remains neutral for the moment. On the downside, firm break of 1.3026 support will resume the decline from 1.3651 and target 1.2773 key support level. This will also revive the case of medium term reversal. On the upside, in case of another rally, upside should be limited by 61.8% retracement of 1.3651 to 1.3026 at 1.3412 to bring fall resumption finally.

In the bigger picture, while the medium term rebound from 1.1946 was strong, GBP/USD hit strong resistance from the long term falling trend line. Outlook is turned a bit mixed and we'll stay neutral first. On the downside, decisive break of 1.2773 key support will argue that rebound from 1.1946 has completed. The corrective structure of rise from 1.1946 to 1.3651 will in turn suggest that long term down trend is now completed. Break of 1.1946 low should then be seen. On the upside, break of 1.3835 support turned resistance will revive the case of trend reversal and target 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466 .