- We expect the RBNZ to leave the OCR unchanged at its July meeting.

- The RBNZ will likely retain an easing bias but stay noncommittal on when it might act on that bias.

- The RBNZ will likely note the uncomfortably high near-term inflation outlook and upweight this factor relative to more recent indicators of weaker economic momentum.

- This should point markets towards inflation and inflation expectations indicators when determining if a further cut will occur in August or sometime later.

RBNZ decision and communication.

The RBNZ will likely leave the OCR unchanged at its July meeting and take a wait-and-see attitude to the outlook for the OCR. While we expect the RBNZ to retain the easing bias it showed in its May Monetary Policy Statement communications, we don’t expect the RBNZ will give a strong guide on the timing on when it might cut the OCR further. Instead, we expect the RBNZ will give the market room to determine for itself, based on data released up until the August Monetary Policy Statement, whether a cut to 3% will happen in August, be delayed until later in the year, or be cancelled altogether.

The RBNZ will likely note that economic activity was stronger than expected in the first quarter of 2025, but that activity indicators since then have pointed to the slow down in economic momentum foreshadowed in their May forecasts. We doubt it will judge recent economic momentum as materially weaker than previously expected – but its likely they will point to some risk that such evidence might accumulate in coming months.

The RBNZ will also likely note that the near-term inflation outlook looks uncomfortably high. We think it will retain confidence that medium-term inflation will recede through 2026 – but will express uncertainty around that as well as the path of inflation expectations while headline inflation remains close to 3%.

The key in determining the timing of when (or if) the next 25bp rate cut occurs will be the relative weight the RBNZ places on the degree of concern about the near-term activity outlook versus the short-term inflation picture. We expect more weight will be placed on the inflation outlook given the single mandate the Monetary Policy Committee is working to.

A hawkish scenario would be one where the RBNZ said nothing about the potential for further easing. We don’t think the RBNZ will want to call time on the easing cycle just yet. But if the RBNZ were not to mention the potential for future easing at all, this would likely be interpreted as a hawkish signal by the market.

A dovish scenario would be one where the RBNZ plays down concern about the near-term inflation outlook and instead expresses comfort with the medium-term inflation outlook. In this scenario, the RBNZ would likely note the weaker short-term activity outlook and leave the impression that further policy easing is more likely than not at the August meeting provided that upcoming data meets expectations.

Recent data flow and impact

Key data that has accumulated since mid-May include:

Stronger Q1 2025 GDP (0.8%q/q vs 0.4%q/q expected, albeit with a downward revision to growth in Q4) which implies stronger economic momentum and a slightly lower level of excess capacity than appreciated.

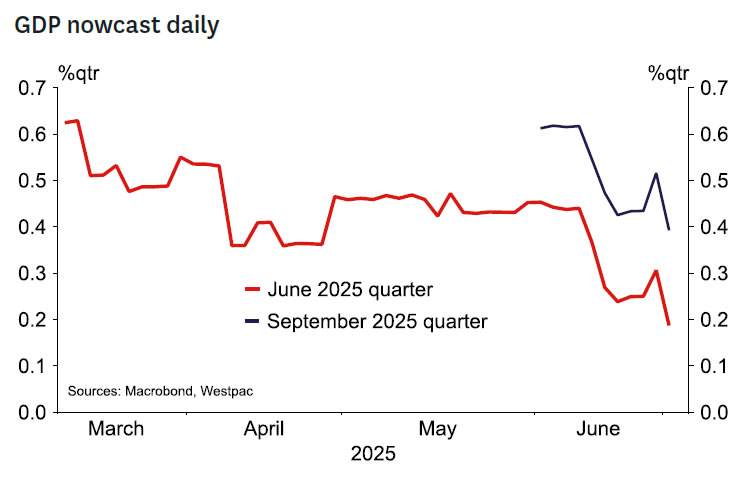

Weaker high frequency activity indicators for the May month (PMI’s, filled jobs, house prices and days to sell, consumer spending, business confidence). These look consistent with weaker activity in Q2 compared to Q1 and the RBNZ’s soft GDP growth expectations for Q2 and Q3 2025 (0.3% and 0.2% respectively). Nowcasts have accordingly been revised down in recent weeks.

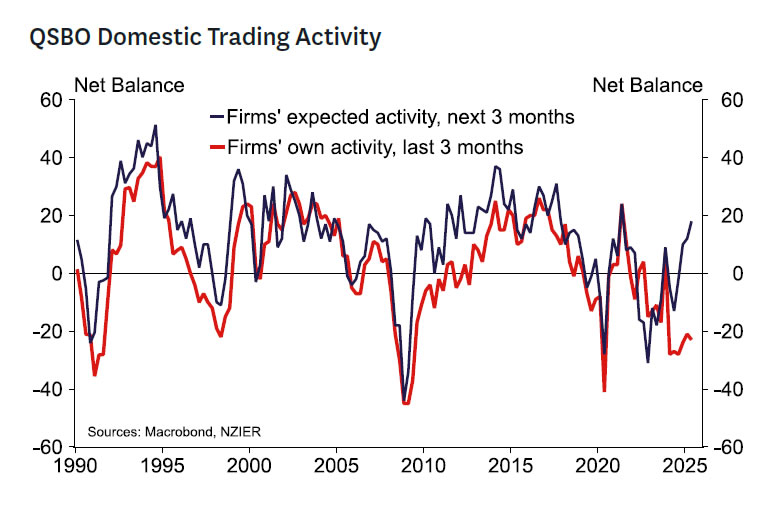

The still downbeat but also optimistic NZIER Quarterly Survey of Business Opinion. This survey showed firms perceive that they experienced weak activity in Q2 while optimism about the future improved from what was already relatively optimistic levels. It’s very much in the eye of the beholder which of these indicators best represents the underlying activity outlook – although recent experience suggests that the more positive forward-looking indicator has been closer to the mark.

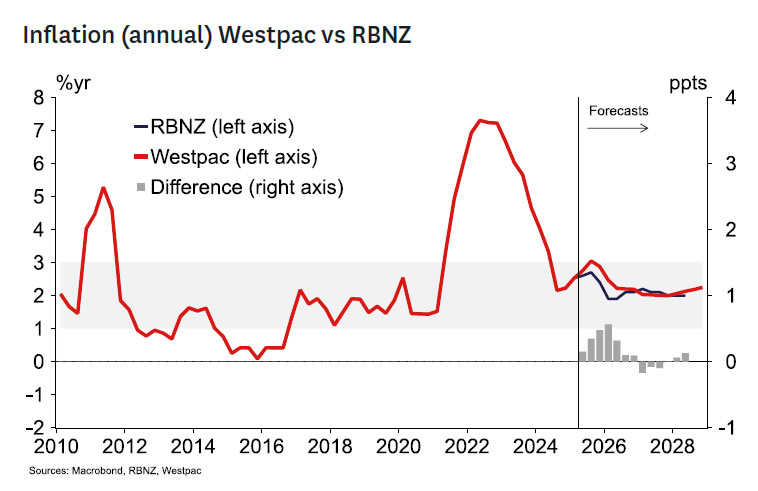

Stronger short-term inflation indicators. The monthly selected price indices suggest a more robust short-term inflation outlook than the RBNZ anticipated in May when they forecasted a 0.5%q/q and 2/6%y/y CPI outcome for the June quarter. Westpac has revised up its own CPI forecast from 0.4%q/q to 0.6%q/q since late May, especially reflecting strong food prices. It’s likely the RBNZ will have made a similar-sized adjustment. The outlook shows that headline inflation will rise to 3% in Q3 and be at 2.9% in Q4 2025. Inflation expectations continued to track higher in the June ANZ consumer survey.

Improved/less uncertain global growth and trade environment. High on the MPC’s mind in May was global uncertainty and the potential for weak global growth and a lower terms of trade. Since then, the outlook has improved somewhat. Progress has been made on trade deals such that the risks of very high and retaliatory tariffs look lower. Progress has been made in reducing risks to global security now Middle East tensions have reduced. Global equity markets are at record highs. Consensus forecasts for global growth have increased in the last 6 weeks – although these remain lower than forecasts seen before April.

Kelly’s take

A pause at this meeting is appropriate. There seems little risk of inflation moving very far into the bottom half of the target range in the next year or two. The global economic environment looks less threatening than might have been feared a month or two ago. And importantly, it’s not clear when inflation will peak and at what level.

There has been volatility in high frequency activity indicators, but also plenty of short-term news that might have driven sentiment in ways that may not prove to be long-lived.

Growth has been more solid than expected in the last couple of quarters and there are tangible signs of higher commodity prices and lower interest rates supporting the economy. Examples include strong agriculture sentiment and increased borrowing as well as rising demand for credit from investors in the housing market.

Strong commodity markets and the current level of interest rates will likely translate into trend to above-trend growth outcomes with time. This should be especially evident as global uncertainties continue to recede. The relatively high level of inflation limits the need to impart further stimulus at this time.

{kind=link}