- As widely expected, the RBNZ left the OCR at 3.25%.

- No vote was required although there remains a split in views among MPC members.

- The Bank’s commentary suggests a presumption that the OCR will be cut in August subject to data evolving as it expects.

- Data on core inflation pressures and inflation expectations are likely to be key in making or breaking the case for an August cut.

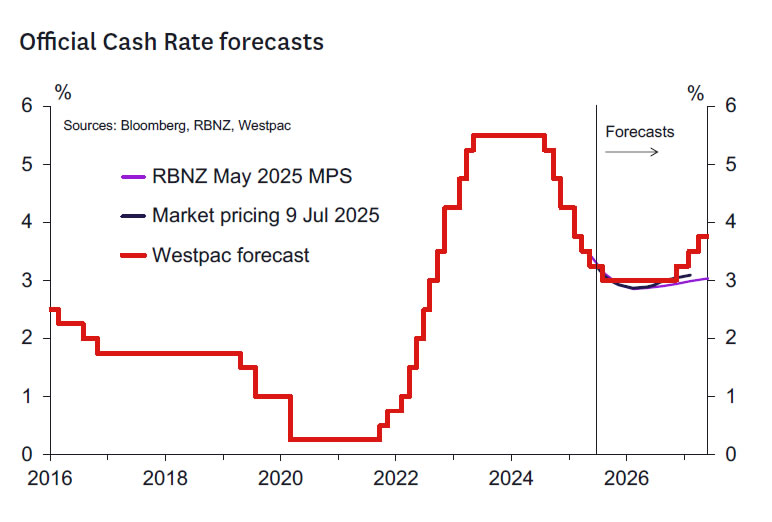

- Westpac continues to expect a final 25bp cut at the August MPS meeting.

As had seemed likely given the RBNZ’s commentary at the May Monetary Policy Statement (MPS), and as close to fully priced by markets, the RBNZ today announced that it had decided to leave the OCR at 3.25%. The decision was reached by consensus with no vote taken.

More importantly, regarding the outlook for policy at future meetings, we think that the RBNZ’s commentary indicates a reasonably strong presumption that the OCR will be cut at the August meeting.

The general view of the Monetary Policy Committee (MPC) is that the economic and inflation outlook remains broadly like that presented in the May MPS. Near-term inflation pressures seem a touch stronger than seen in May, but the RBNZ’s medium-term view remains one where mid-target inflation remains the most likely prospect by early 2026.

Risks remain but don’t seem much difference in magnitude or balance compared to the RBNZ’s thoughts back in May. Hence there remains a sense that one to two more 25bp cuts is still high in the minds of the MPC. Perhaps the hawks would see the risks as being in the zero to one cut range where the doves might see at least one, perhaps two 25bp cuts to occur by early next year.

Westpac expects a 25bp rate cut on 20 August, but not guaranteed.

Looking ahead, data that might be most likely to derail the August easing would be signs of continued strong core inflation as well as rising inflation expectations indicators (first half of August). It’s also possible that the recent weakness seen in high frequency activity indicators doesn’t persist in the July and August reads that will be available before the 20 August meeting. Finally, the MPC remains concerned about the potential for global risks to spill over to New Zealand. Should evidence continue to accumulate that these risks are reducing (the MPC seems not to recognise any reduction in global risks right now) then that might point in the direction of holding the OCR unchanged in August.

On balance though, the 25bp cut in August looks like the best bet for now (perhaps a 70% probability). Hence, we are not changing our forecast for one final cut at the August MPS to 3%.

Notable quotes from the RBNZ.

Of note, in the press statement and record of meeting the RBNZ stated the following:

- “The Committee discussed the options of cutting the OCR by 25 basis points to 3 percent or keeping the OCR on hold at 3.25 percent at this meeting.”

- “The case for lowering the OCR at this meeting highlighted weak near-term growth momentum and the risk of prolonged weakness in economic activity from excess caution by households and businesses in the face of economic uncertainty.”

- “The case for keeping the OCR on hold at this meeting highlighted the elevated level of uncertainty, and the benefits of waiting until August in light of near-term inflation risks.”

- “The economic outlook remains highly uncertain. Further data on the speed of New Zealand’s economic recovery, the persistence of inflation, and the impacts of tariffs will influence the future path of the Official Cash Rate”.

- “Subject to medium-term inflation pressures continuing to ease in line with the Committee’s central projections, the Committee expects to lower the Official Cash Rate further, broadly consistent with the projection outlined in May.”

- “While inflation is expected to approach the top of the target band in Q2 and Q3 of 2025, spare productive capacity and declining core inflation are consistent with headline inflation returning to the midpoint over the medium term. The Committee noted that the outlook for medium-term inflation pressures in New Zealand has evolved broadly in line with the May MPS projections.”

- “The Committee noted that there were upside and downside risks to the medium-term outlook for inflation. With higher inflation expected in the near term, some members underlined a risk that this could lead to more persistently elevated price- and wage-setting behaviour….However, other members emphasised the large negative output gap, moderate wage inflation and job insecurity, and continued weakness in house prices.”

There was little reaction in either interest rate markets or the NZ dollar, suggesting that the RBNZ’s commentary largely met expectations.

Key things to watch ahead.

Looking ahead to the 20 August MPS, the key domestic economic indicators to watch are:

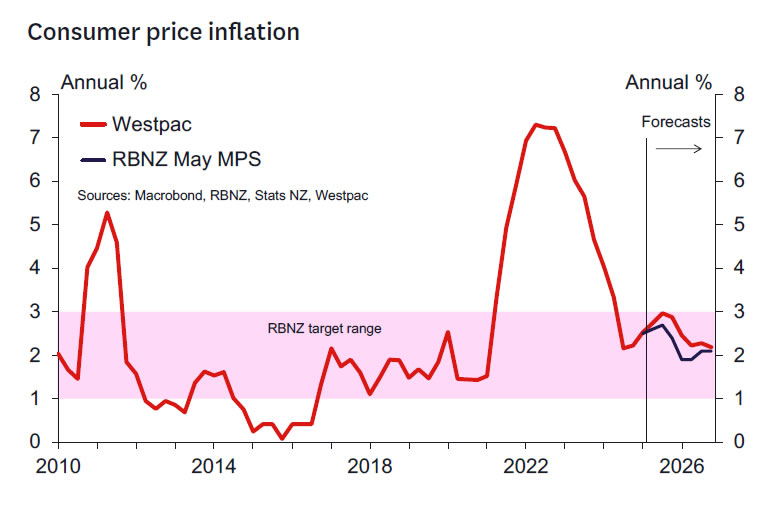

- The Q2 CPI (released 21 July) and July Selected Prices (15 August). We currently expect the CPI to rise 0.6%q/q in Q2, compared to the RBNZ’s May forecast of 0.5%q/q.

- The Q2 labour market surveys (released 6 August). We currently expect that the unemployment rate will rise 0.2ppts to 5.3%, compared to the RBNZ’s May forecast of 5.2%, with filled jobs data suggesting that employment will likely disappoint the RBNZ’s forecast of 0.2%q/q.

- The Q3 RBNZ Survey of Expectations (released 7 August) and Q3 RBNZ Survey of Business Expectations (released 18 August), with a particular emphasis on the inflation expectations measures in these surveys following a lift in Q2.

In addition to these major quarterly releases, we expect the RBNZ will pay close attention to the developments in the BusinessNZ PMIs, consumer spending, housing market and migration (reports for June released in mid- July and for July in mid-August). The various activity and inflation indicators contained in the ANZ business and consumer confidence surveys (released late July) will also be of interest.

Aside from domestic economic data, developments in US tariff policy and any clarity regarding how this is impacting the outlook for trading partner growth and inflation will also have an impact on the RBNZ’s deliberations at the August meeting. Movements in prices for New Zealand’s key commodity exports will be important in gauging the extent to which less favourable international conditions are beginning to impact the economy.

, and as close to fully priced by markets, the RBNZ today announced that it had decided to leave the OCR at 3.25%. The decision was reached by consensus with no vote taken.){kind=link}