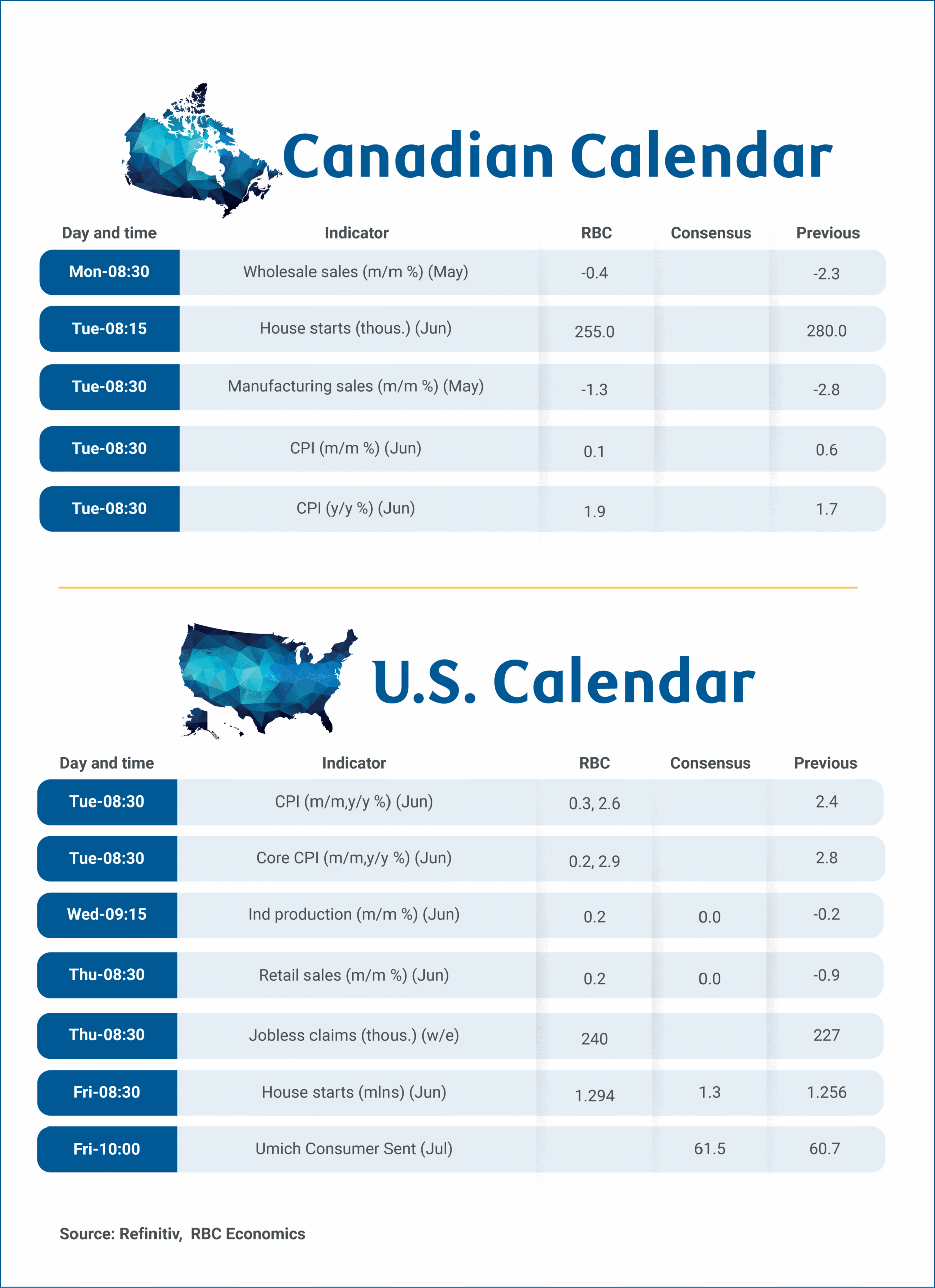

We expect it is likely too early to see a significant increase in prices due to tariffs in Canadian and U.S. inflation data for June on Tuesday.

There have been signs of tariffs raising prices for some Canadian food products, and vehicle prices have been climbing steadily since March. But, the broader impact of tariffs on prices has been limited. Canadian retaliatory tariffs announced earlier this year were measured and targeted, and in many cases, have been paused to avoid raising costs for Canadian consumers and producers.

Tariff hikes in the U.S. have been much larger and broader, but data from the U.S. Department of the Treasury suggests tariff revenues collected have lagged tariff announcements in April, but ramped up by 40% in May and another 20% in June. We expect the increases will ultimately raise consumer prices this year, but not right away with pre-tariff inventory building limiting the immediate impact.

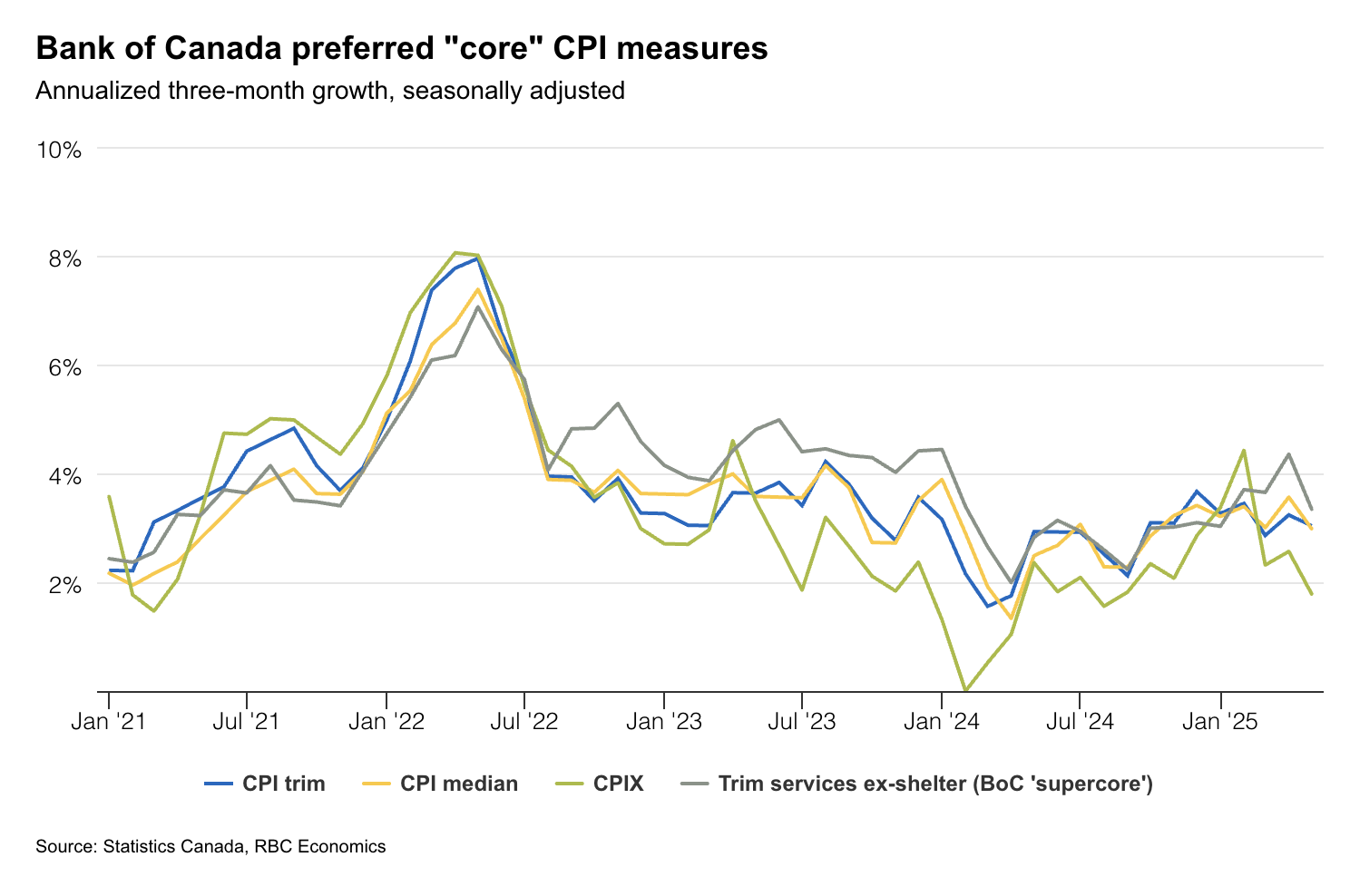

Removal of carbon tax continues to distort Canadian CPI growth

For June, we expect a slight increase in the consumer price index to an annual 1.9% following a lower-than-expected 1.7% reading in May.

Gasoline prices edged down 0.9% from May despite a 10% jump in oil prices due to conflict in the Middle East, and were still more than 10% lower from a year ago, reflecting the removal of the consumer carbon tax in April.

Food price inflation—which picked up earlier this year due to higher costs for groceries potentially related to Canadian retaliatory tariffs on imports from the U.S. and dining out—eased slightly in May on an annual basis. We expect this softening to persist in June.

More focus on BoC measures

With tax changes significantly distorting annual price growth, the Bank of Canada’s preferred core inflation metrics (which exclude the impact of indirect tax changes) will continue to be watched closely for signs of changes in underlying trends.

We expect month-over-month increases in the trim and median measures close to the 0.2% increases posted for both in May. That would leave annual rates little changed from May and still significantly above the BoC’s 2% inflation target. Excluding food and energy, inflation is forecast to rise slightly to 2.7% from May’s 2.6%.

U.S. inflation to head higher

In the U.S., rising costs from tariffs will ultimately be paid by U.S. purchasers. But, it will likely be spread across the supply chain from transport companies to wholesalers/manufacturers/retailers with only a portion finally showing up in consumer prices.

We expect year-over-year growth in U.S. consumer prices to rise to 2.6% in June from 2.4% in May on a 0.3% monthly increase from May. We expect core (excluding food and energy products) prices to post a 0.2% increase from May and gain 2.9% from a year ago.

Week ahead data watch:

Canadian manufacturing sales likely dropped again in May, with the largest decreases observed in the petroleum and coal product subsector, the transportation equipment subsector, and the food product subsector. Part of the headline sales decline was price-related, as the IPPI (price of manufactured goods) dipped 0.5% during the month.

We look for Canadian housing starts to come in at 255,000 units in June, down about 9% from the prior month. This decline partially offsets the surge observed at the beginning of this quarter.

We expect the Canadian core wholesale sales to decrease by 0.4% in May, in line with StatsCan’s early indicator, and this was driven by lower sales in the machinery, equipment, and supplies subsector.

U.S. retail sales are expected to have increased by 0.2% in June after dropping 0.9% in May. Higher gasoline prices likely boosted sales at gasoline stations, but unit auto sales edged lower again after an almost 9% drop in May.

A modest recovery in U.S. industrial production is expected for June (+0.2%), bouncing back after a 0.2% decline in May. While the ISM manufacturing index improved during the month, it remained below 50. We anticipate slight improvement in manufacturing (excluding autos) sector output.

{kind=link}