Canadian Highlights

- Headline inflation drifted higher in June, while core inflation measures remained sticky and elevated.

- Canadian home sales gained for a third consecutive month, but price growth continued to moderate. Housing starts capped the second quarter with a record gain.

- The recent data is likely to push the Bank of Canada to the sidelines at their next meeting. We don’t expect further rate easing until later this year.

U.S. Highlights

- Economic data released this week was mixed overall, as June retail sales painted a resilient picture of U.S. consumers despite trade uncertainty.

- However, June inflation data was more troubling, as preliminary impacts of tariffs likely helped to push core goods price gains to a two-year high.

- President Trump also announced a trade deal with Indonesia, marking the third deal reached since ‘Liberation Day’.

Canada – Summer Heat Hasn’t Melted Inflation

This week, we received the second of two inflation reports that the Bank of Canada (BoC) will use to guide their next policy decision on July 30th. For the month of June, headline prices moved two ticks higher to 1.9% year-on-year (y/y), in line with market expectations. Core goods drove a majority of the upward move, as prices for components such as motor vehicles, household furniture, and apparel firmed up. Despite the increase, top-line price growth over the past several months has been tamped down below 2% thanks in part to the end of the consumer carbon tax, something we expect to linger in the coming months.

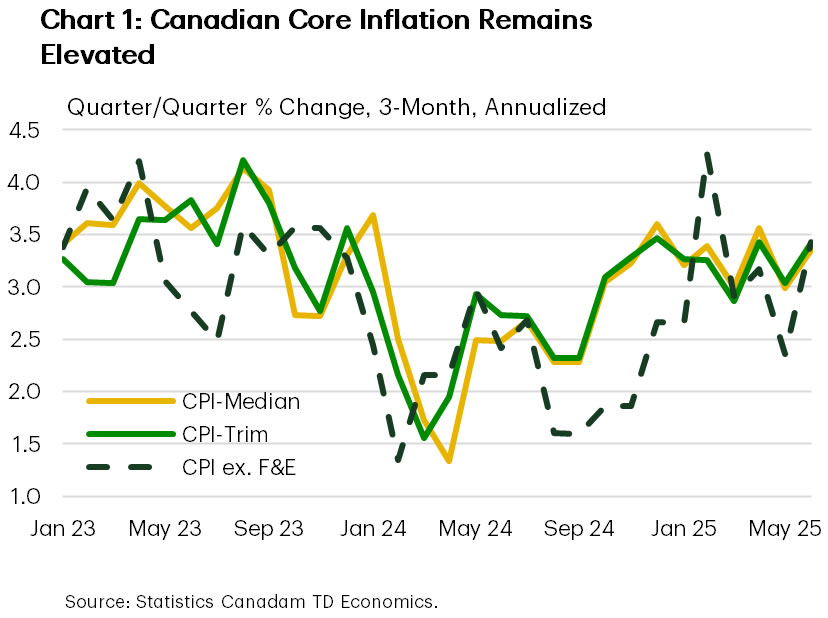

However, underlying price pressures, or core inflation, have been the thorn in the side of the BoC. The Bank’s preferred core measures (CPI-trim and CPI-median) and the traditional core measure (ex-food and energy) all moved higher to 3.4% on a three-month annualized basis (Chart 1), reversing much of last month’s move lower. Our view remains that a softening economic growth backdrop over the next two quarters should help keep a lid on further core inflationary pressure.

June’s warm inflation print was complimented by encouraging news for the Canadian housing market. Home sales advanced for a third consecutive month in June, and housing starts remained robust. However, home prices fell modestly, showing buyers still have bargaining power. We expect home sales will continue to rise in the second half of the year as pent-up demand continues to trickle into the market, though elevated uncertainty may leave sales levels subdued.

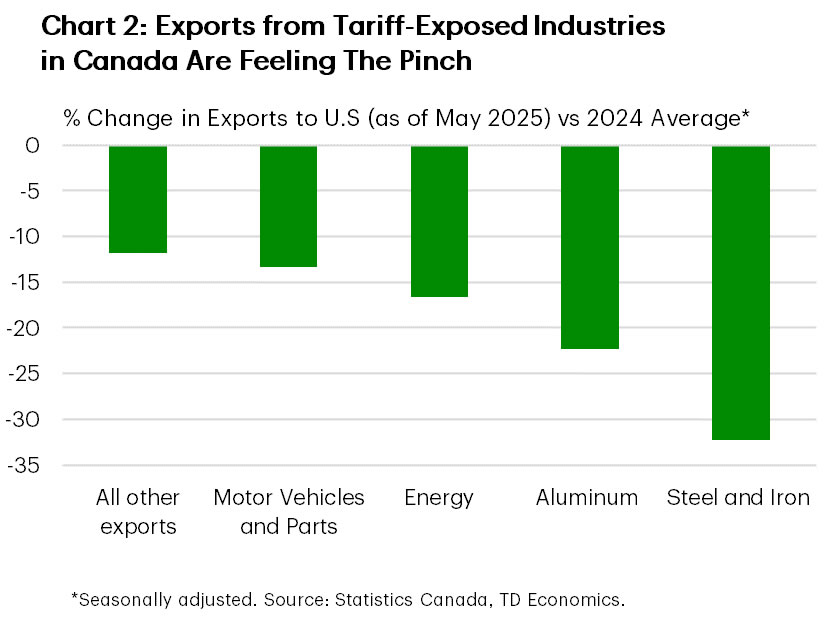

Based on the recent data, including last week’s robust employment numbers, we can make two conclusions. First, tariff-exposed industries are showing the effects of U.S. tariffs in their export and jobs data (Chart 2), while business and consumer confidence measures have also taken a hit. Second, is that when taken altogether, Canada’s economy is holding up better so far than most have feared. For this reason, the BoC will almost certainly remain on pause later this month. Markets have nearly wiped the probability of a July cut off the table after pricing a near coin flip just a few weeks ago.

This doesn’t mean Canada’s economy is out of the woods, it just means the BoC has been afforded more time to assess cost pressures and the overall economic impacts of the trade war. We are now dealing with a new wave of uncertainty, not least from Trump’s recent threat to raise Canadian tariffs as high as 35% by next month. Prime Minister Carney also appears to be embracing what could be the “new-normal”, acknowledging that a forthcoming trade deal will likely have tariffs included. Absent a clean and quick resolution on trade, which seems unlikely at this juncture, the economic backdrop faces downside risk and should give the BoC space to deliver more easing later this year.

U.S. – The Price of Trade

Tipping into the second half of July, we received a couple of key readings on the U.S. economy. On a positive note, retail sales in June were stronger than expected. However, we also received June’s inflation report which indicated that tariff price pressures were beginning to show up more materially in the economy. On that front, President Trump announced a third trade deal this week, while also stating that most nations would face a 10-15% reciprocal tariff rate. As of the time of writing, the S&P 500 was up 0.8% on the week, while U.S. Treasury yields were little changed.

U.S. consumer trends remained solid in June, with retail sales rising across most major product categories. Excluding the more volatile product categories, retail sales had its strongest gain in three months. This came at a time when tariff uncertainty was assumed to be fading, equity markets recovered their recent losses and consumer confidence was recovering gradually. However, these trends have since stalled in July amid renewed trade tensions, particularly in relation to the news last weekend that some of the largest U.S. trading partners will be assigned tariff rates on the higher end of the spectrum (Canada, Mexico, & E.U. all 30+%). Looking to the second half of the year, we expect consumer spending to cool as the impact of tariffs on consumer prices grows.

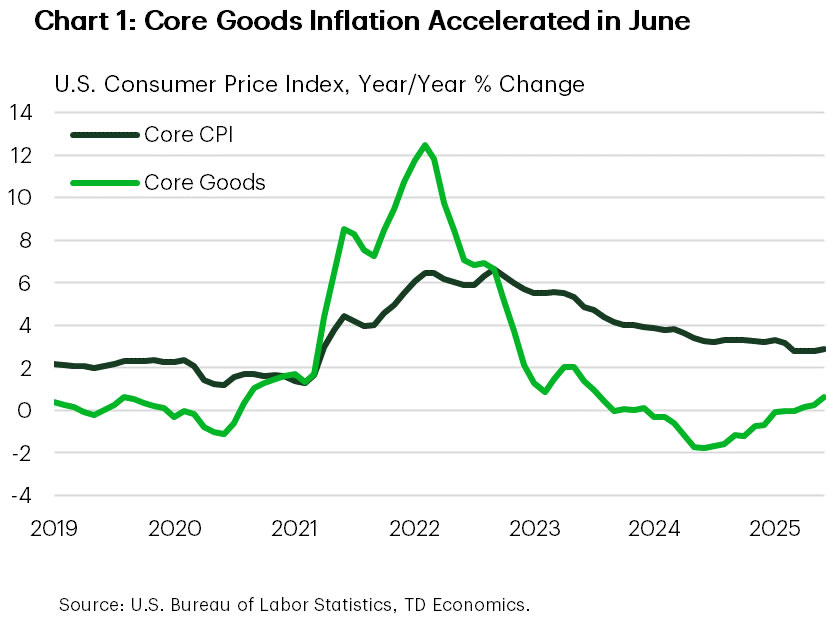

Some preliminary signs of this began to show up in the June CPI inflation report, as the monthly gain in core goods prices hit a two year high. This in turn pushed the annual growth in core CPI, which excludes the more volatile food & energy categories, up to 2.9% (Chart 1). Furthermore, this week’s Fed Beige Book noted that “contacts in a wide range of industries expected cost pressures to remain elevated in the coming months, increasing the likelihood that consumer prices will start to rise more rapidly by late summer”. With tariffs expected to rise further over the coming month, it is unlikely that the Federal Reserve will be able to shift its restrictive monetary policy stance over the near term. Markets see virtually no chance for a rate cut in two weeks, and a 60% chance of a cut in September.

Most of the Federal Reserve officials we heard from this week echoed the wait-and-see sentiment noted by Chair Powell in recent weeks. One notable exception was Governor Waller, who spoke after the release of the June CPI report and advocated for a 25-basis-point cut in July. Waller has been dovish for several months now, citing the slowdown in employment growth as the basis for easing monetary policy. However, the FOMC makes policy decisions by majority vote, and a cut in July is currently viewed as unlikely.

Lastly, the President announced a trade deal with Indonesia earlier this week, stating that it would face a tariff rate of 19%, in addition to agreeing to purchase tens of billions of dollars in American energy, agricultural, and aerospace goods. While tariffs lower than the initial April 2nd level are a positive development, these still represent notably higher levies than current levels, and trade deals with larger trading partners have remained elusive (Chart 2). Looking ahead, markets will be closely watching for additional trade deals with the August 1st deadline quickly approaching.

{kind=link}