Canadian Highlights

- After last week’s downbeat employment report, market watchers wait for an update on inflation next Tuesday.

- Data out this week suggest the housing market’s freeze is starting to thaw.

- The push (tariffs and trade) and pull (excess supply) on consumer prices is the focus in the coming months, with July’s inflation report hopefully providing a solid glimpse of what might be to come.

U.S. Highlights

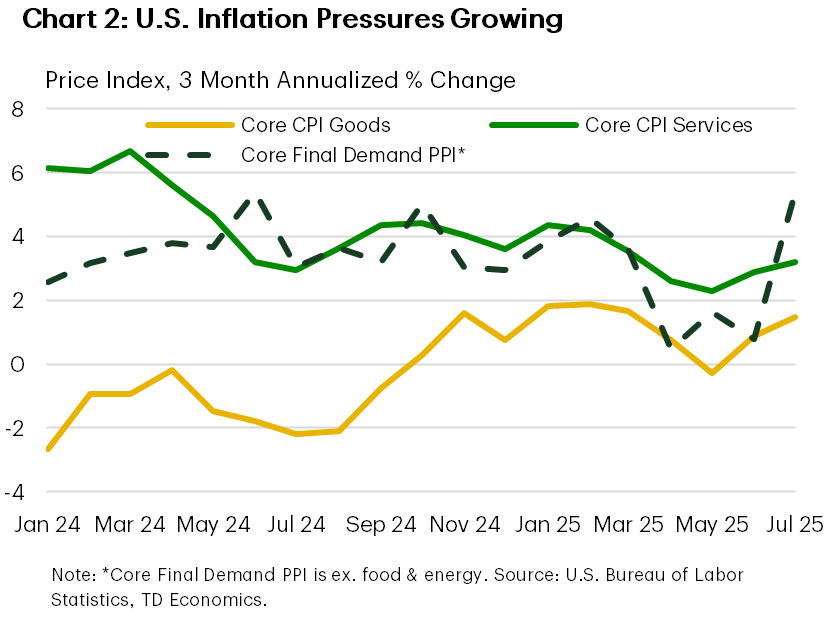

- Inflation pressures rose in July, with core CPI rising above 3% for the first time since February. Meanwhile the uptick in PPI suggests a shift to higher tariff passthrough by companies.

- Retail sales recorded healthy growth in July despite growing price pressures.

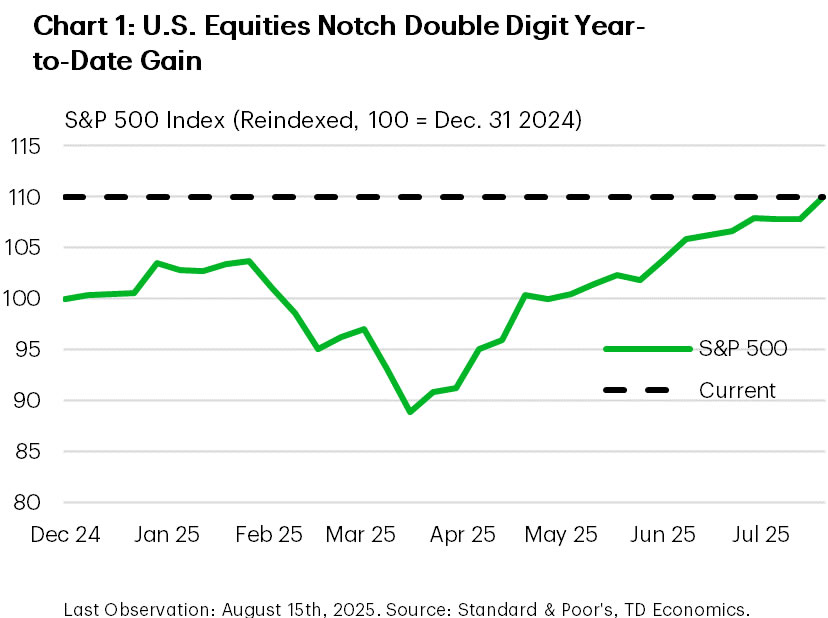

- The S&P 500 hit a double-digit year-to-date return after rising 1% on the week, which would mark the third consecutive annual double digit return if unconceded by year-end.

Canada – The Week Between Labour and Inflation

With an employment report in the rearview and an update on inflation due next Tuesday this was a quiet week for Canadian economic data. In terms of news, China updated tariffs on Canada’s canola, the Bank of Canada’s Summary of Deliberations doubled down on the wait-and-see approach, and we got a bit of good news from the housing market. With consumer and producer price inflation south of the border garnering attention this week, it’s worth taking stock of where things stand and what’re we’re looking for from the CPI report next week.

First things first, an update from the housing market. After some glimmers of hope in late 2024, the market was broadsided by tariff threats and the resulting economic uncertainty earlier this winter. Data out this week suggest this year’s freeze might just be starting to thaw. Sales rose again in July, with strength in Ontario showing that pent-up demand might be starting to soak up some of the ample supply on the market. That said, a signal that the housing market might be finding bottom is not the same as one that it is rising again. A gradual recovery remains our base case, with the associated impacts on housing costs, and inflation.

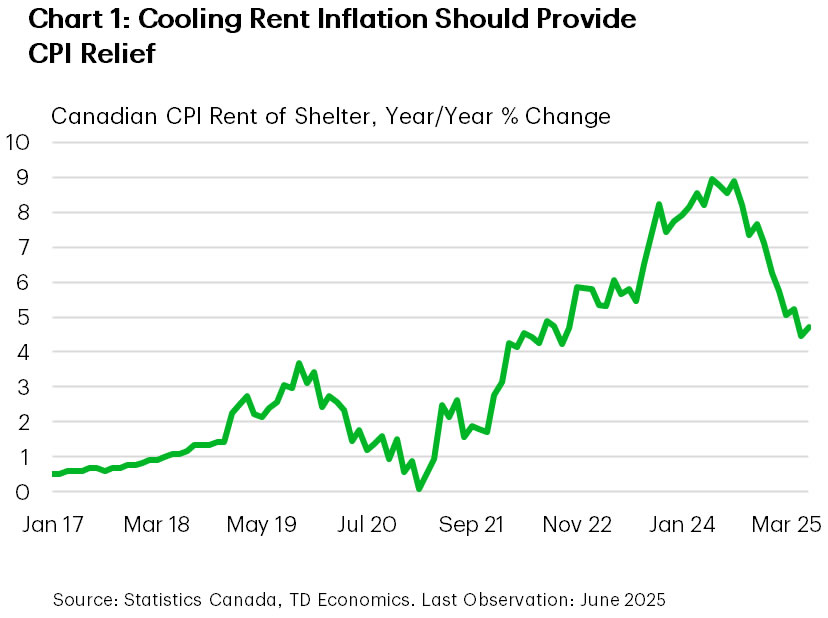

In particular, one key component we’re looking to is rent inflation. CMHC’s mid-year rental report cited the ongoing churn of tenants vacating rent controlled units that are then relisted at current market rates, contributing to propping up the month-on-month gains in average rents. This helps explain, in part, the still elevated readings in the CPI shelter component (Chart 1). That said, with supply on the market rising, falling asking rents should continue to exert influence on the metric, and as less of the rental stock is left to reset, help it continue moderating in the coming months. Beyond rents, we will also be looking for signs that inflation in cyclically sensitive services (excluding shelter) slowed in July.

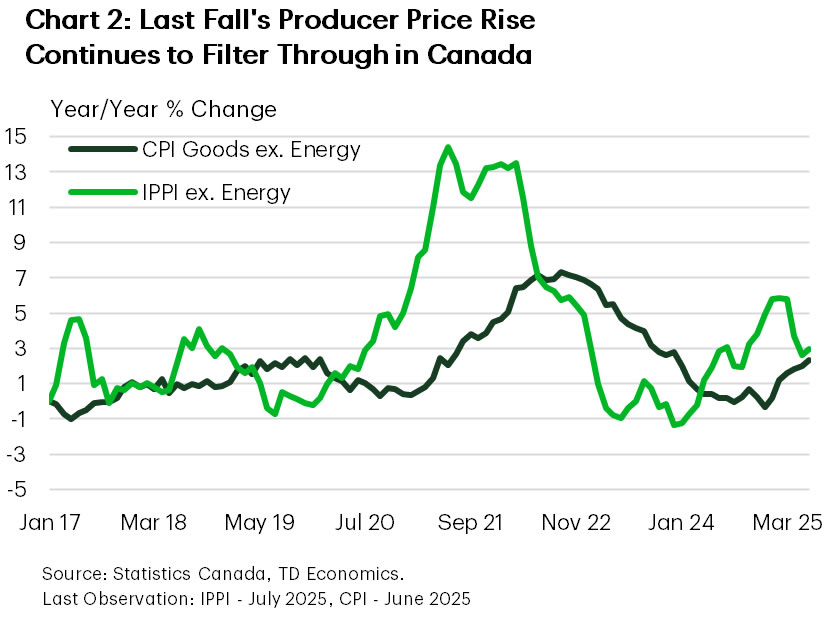

These factors ultimately lead to the most important question, “What are we going to see from tariffed goods?” The Canadian government has imposed tariffs on a wide swath of imports from the U.S., and a run-up in producer prices last fall (Chart 2) suggests some degree of margin compression that firms could be looking to recoup. So, we’re going to be looking for evidence that higher prices are being passed on by firms, rather than absorbed.

There are, of course, complicating factors. The BoC’s monetary policy report noted past depreciation of the Canadian dollar as another factor in the current price gains, but given the recent rally vis-à-vis the U.S. dollar, and our outlook, a firmer currency should act as somewhat of a salve against faster inflation. Further complicating things is the chance that firms could opt to raise prices as their tariff-exposed competitors are forced to pass on higher costs. The push (tariffs and trade) and pull (excess supply) on consumer prices is the focus in the coming months for the BoC. For those of us watching, July’s inflation read will hopefully provide a solid glimpse of what might be to come.

U.S. – Price Pressure Firms in July, Equity Markets Undeterred

It has been one week since the full complement of reciprocal tariff policies went into effect. Those tariffs will not have an influence on the economic data for a few months, but the tariffs that prevailed through the first half of the year continued to show up in the July inflation readings released this week. This included the CPI and PPI, both of which showed signs of rising price pressures that are expected to trend higher over the coming months with the new tranche of tariffs now in effect. Largely undeterred, equity markets continued to probe record highs, with the S&P 500 rising 1.0% on the week and notching a double digit return year-to-date (Chart 1).

The first inflation report we received on Tuesday showed consumer price growth accelerating in July, with the annual percentage change in core CPI rising above 3% for the first time since February. This was driven by stronger core goods prices, largely related to higher tariff passthrough, while core services inflation also trended higher (Chart 2). Producer prices, which we received on Thursday and measure the prices charged by U.S. businesses, also began to trend notably higher in July with the monthly change hitting a 3-year high. This likely suggests that businesses are shifting to pass on more of the higher costs associated with tariffs to consumers after largely absorbing the costs in the first half of the year. Moving forward, with the effective U.S. tariff rate nearly 10 percentage-points higher after last week’s reciprocal tariffs came into force, inflationary pressures are expected to remain elevated through the second half of the year.

The Federal Reserve has been acutely attuned to these developments, with the central bank remaining on hold since the start of the year. Although a few Federal Reserve officials have advocated for rate reductions, the balance of the FOMC continues to voice caution regarding the uncertainty surrounding the outlook for inflation and the economy. The officials we heard from this week, including regional Fed presidents Schmid (Kansas City) and Goolsbee (Chicago) who are voting members of the FOMC this year, noted that caution was still warranted. Market pricing fluctuated this week, but currently has 90% odds for a rate cut in September. The annual Jackson Hole Symposium next week will be watched closely after this week’s inflation reports for any signs on the leanings of officials in the run-up to the next Federal Reserve decision in one month.

On a more positive note, retail spending appeared to remain healthy in July, growing 0.5% month-on-month. However, July also had Amazon’s multi-day Prime day event which tends to boost sales activity. A non-outsized reading could suggest that consumption is beginning to slow in line with the downward revisions to the labor market recorded in the second quarter. This is part of the reason why Federal Reserve officials have continued to advocate for caution, noting that it will take time to properly assess the state of the U.S. economy amid the fog of various shifts in trade policy.

Next week, we’ll receive the FOMC meeting minutes for July as well as the July reading for PCE inflation which should help formulate expectations for September’s Fed meeting. With trade policy uncertainty waning gradually, the attention of markets will shift back towards the Fed.

.){kind=link}