- The Bank of England (BoE) kept the Bank Rate at 4.00% as widely expected.

- The vote split was 7-2 in favour of hold, also as expected.

- The BoE did not tweak the guidance more hawkish and thus further cuts remain on the table.

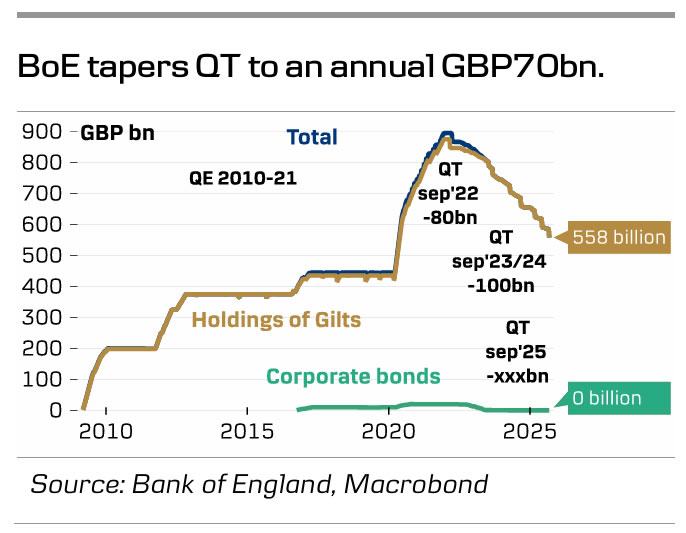

- QT was tapered from an annual pace of GBP100bn. to GBP70bn.

- The market reacted by trading Gilt yields a bit lower and EUR/GBP a bit higher, but the move later faded.

The Bank of England (BoE) kept the Bank rate at 4.00% as widely expected. The vote split was 7-2 in (keep vs. cut) with Professor Allan Taylor (who favoured a 50bp cut in August) and Swati Dhingra (notorious dove) dissenting.

The overall guidance remained unchanged, with the BoE reiterating that “a gradual and careful approach to the further withdrawal of monetary policy restraint remains appropriate”. Removing this would likely have dampened expectations for near-term rate cuts further.

The annual QT decision has been a contentious issue, given the fragile Gilt market and the government’s growing fiscal challenges, where interest payments are weighing still heavier on the fiscal space. The decision aligned with expectations set the annual pace of GBP70bn, backed by 7of 9 committee members, with one member arguing for a higher pace and one member for lower one.

BoE call. We continue to expect the BoE to deliver the next cut in the Bank Rate in November, followed by another cut in February, bringing the Bank Rate to 3.50%. However, we acknowledge that a November cut is highly dependent on more disinflationary signs in the September CPI data.

Market reaction. Gilt yields traded a couple of basis points lower and EUR/GBP a bit higher on the announcement, likely due to the absence of more hawkish guidance from the BoE. However, the initial reaction was short-lived. We expect EUR/GBP to move higher towards 0.89 on a 6-12-month horizon on a weakening of the UK growth outlook and a positive correlation to a USD-negative environment.

kept the Bank rate at 4.00% as widely expected. The vote split was 7-2 in (keep vs. cut) with Professor Allan Taylor (who favoured a 50bp cut in August) and Swati Dhingra (notorious dove) dissenting.){kind=link}