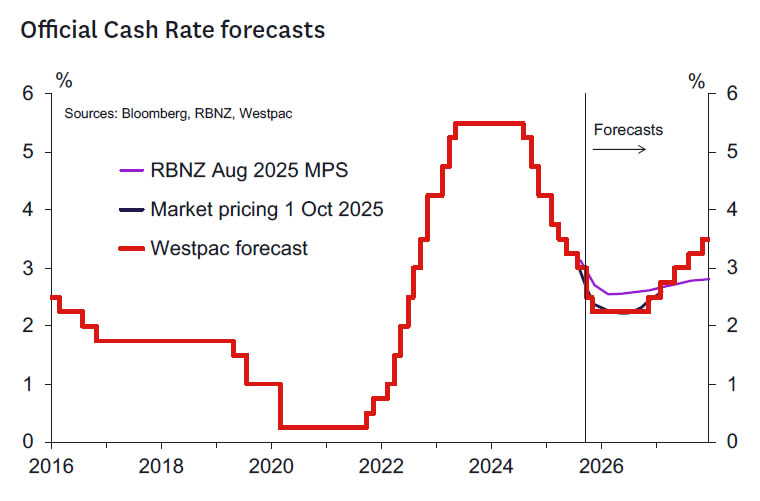

- We expect the RBNZ to cut the OCR by 50bp to 2.5% at its October meeting.

- An easing bias will likely be maintained that’s dependent on data to come.

- Signs of greater than expected excess capacity will be highlighted and the prospect of subdued medium-term inflation pressures will motivate the MPC’s decision.

- The arguments for a “circuit breaking” shift in the OCR to levels more consistent with boosting demand should remain prominent and tip the balance on the MPC.

- Quickly moving the OCR to a stimulatory level will generate confidence and activity ahead of the important Christmas and summer trading period.

RBNZ decision and communication.

In the August Monetary Policy Statement (MPS) the RBNZ indicated that it expected to reduce the OCR to 2.5% by year end. On balance, the data flow since August – notably the very disappointing June quarter GDP report – has supported the RBNZ’s forecast. Indeed, commentators seem united in the belief that the OCR needs to go to 2.5%, with downside risk beyond. The market has similar views regarding the policy outlook, having quickly moved to price a terminal OCR of 2.25% in the wake of the GDP report.

In our view, there doesn’t seem to be a good reason to delay a move to 2.5%. Quickly moving the OCR to a stimulatory level will boost confidence and activity ahead of the important Christmas and summer trading period. This may also reduce the likelihood that even further monetary policy support is required in the new year – a year in which domestic political uncertainty is likely to grow if opinion polls continue to point to a tight General Election.

In the August MPS, two MPC members voted for a “circuit breaking” shift in the OCR to levels more consistent with boosting demand. Those views should hold even greater sway this meeting, helping to tip the balance on the MPC towards a 50bps cut. Hence, we expect the RBNZ to cut the OCR by 50bp to 2.5% at its 8 October meeting.

We also note that the composition of the MPC has shifted since August. The most hawkish member, Dr Bob Buckle, has ended his term and there is a new member, Hayley Gourley, who may be happy to move with the consensus while getting familiar with the process. Similarly, we expect Governor Christian Hawkesby will give weight to the views of the members of the MPC who will be carrying on post November, since they will be the ones remaining to deal with the consequences of policy decisions taken now. We suspect this might increase the weight the most dovish MPC members carry this time.

We expect the Bank to maintain an easing bias, with the prospect of a further reduction in the OCR at the 26 November meeting conditional on the flow of data to come (which will include the September quarter inflation and labour market reports). We doubt the MPC will want to be seen as delaying stimulus and encouraging the public and businesses to hold back spending, hiring and investment decisions in anticipation of more policy action later. This type of behaviour has been a feature of the easing cycle to date and may have contributed to a slower than ideal response to the 250bp of cuts already implemented.

It’s also worth noting that given current market pricing, it’s probably hard for the RBNZ to cut the OCR by just 25bp and not cause interest rates to rise somewhat. What would be required is a relatively strong commitment to cut rates significantly in November. This would raise the question of why a greater easing wasn’t occurring now? There might also be criticism of the RBNZ in this circumstance that the MPC might be sensitive to.

We think our central scenario of a 50bp cut and an easing bias for November has around a 70% likelihood. There are also other scenarios to be considered.

- A hawkish outcome would be a 25bp cut and indications of another 25bp coming in November (20% chance). This would indicate that the MPC see the path depicted in the August forecasts as remaining reasonable. There would be a decent backup in interest rates given markets currently price the OCR to bottom out around 2.2-2.25% at the time of writing.

- A dovish outcome would be the RBNZ coupling the 50bp cut at this meeting with a strong presumption of at least a 25bp cut in November (10% chance). This would indicate that the MPC interpret recent data as implying significant downside risks to the timing of the recovery forecast in the second half 2025 and into 2026. Hence this would imply an amping up of the circuit breaking easing discussed in August beyond what we see as more likely right now.

Recent data flow and impact.

Key data and developments that have accumulated since the August MPS include:

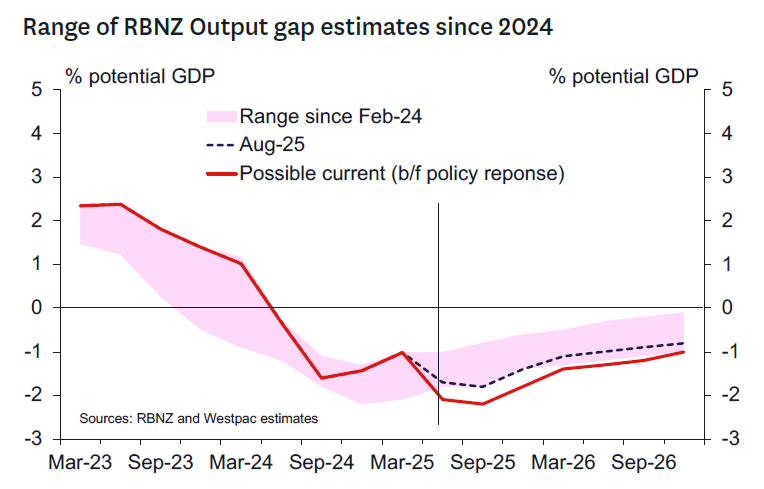

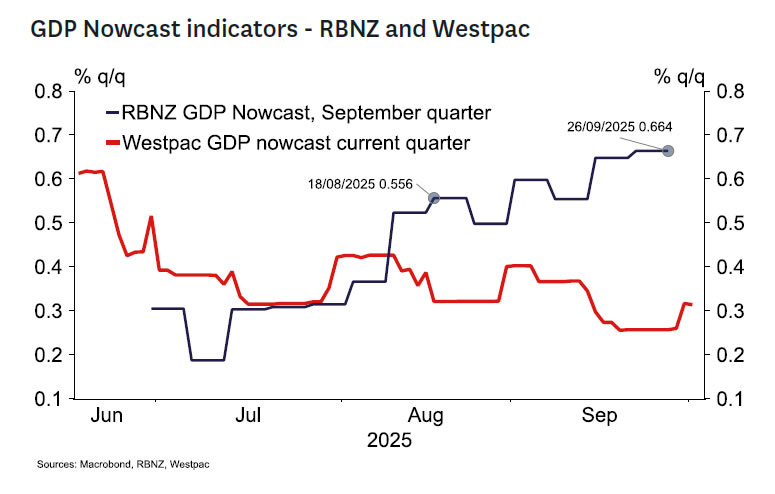

- The June quarter GDP outcome of -0.9%q/q was 0.6ppts weaker than the RBNZ had forecast. While there are reasonable prospects that September quarter GDP growth will exceed the RBNZ’s August MPS forecast of 0.3%q/q, we don’t think growth will be strong enough to offset the June quarter error. As a result, the negative output gap will remain larger than the RBNZ had expected.

- Adjusted for the bias in the latest monthly outcome, filled jobs data from the Monthly Employment Indicator suggests that employment is tracking consistent with the RBNZ’s August forecast of zero growth in the September quarter, which will likely lead to a further modest rise in the unemployment rate. The number of job advertisements remain exceptionally low but have turned factionally higher in recent months.

- High frequency activity indicators, such as the Business NZ PMIs and the ANZ’s past activity indicator have been mixed, but in all cases remain consistent with no more than modest GDP growth.

- House sales have declined slightly in recent months, selling times have remained longer than normal and house prices have been flat at best.

- Sentiment surveys continue to point to firm business optimism, boosted slightly since the RBNZ’s August MPS pivot, but still weak levels of consumer confidence (likely reflecting the weak state of the labour market and pressures on household budgets from higher food and energy prices and sharp increases in council rates).

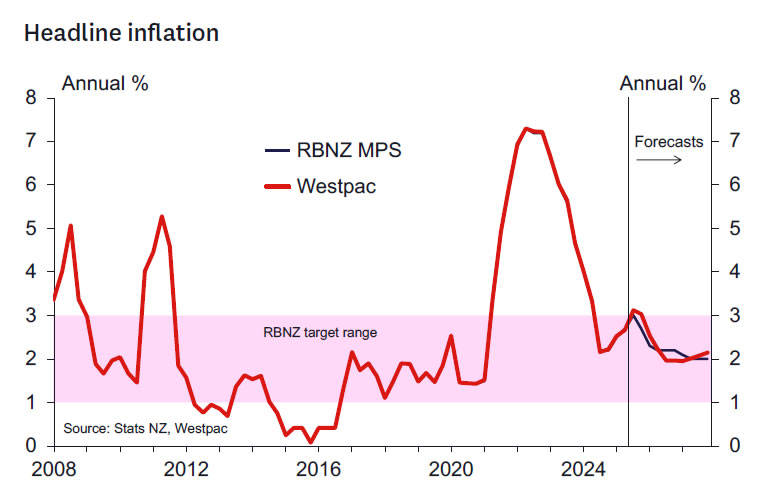

- Monthly price data continues to suggest that the CPI will sit close to the top of the RBNZ’s 1-3% target range in the September quarter, as the RBNZ forecast in the August MPS.

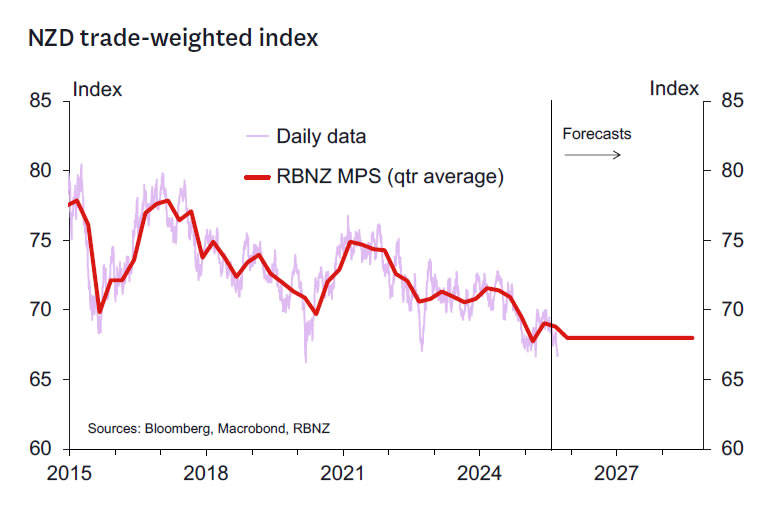

- The trade-weighted exchange rate has fallen around 2% below the RBNZ’s August MPS assumption, reflecting the market’s reaction to the weak June quarter GDP data and the pricing of a 2.25% terminal rate for the OCR.

- The RBNZ will also be watching the upcoming QSBO survey (out 7 October) closely. This survey has tended to be one of the more reliable gauges of economic activity and inflation pressures in New Zealand, and will provide a timely update on how the economy has been tracking following the weaker than expected June quarter GDP result.

Kelly’s take.

A 50bps cut at this meeting is appropriate. In the past few meetings, I’ve been counselling a more cautious approach consistent with the end of the easing cycle potentially getting nearer. But events have overtaken that view as it was predicated on growth broadening and strengthening in the second half of 2025 in the context of an inflation rate that’s too high and unlikely to fall into the lower half of the 1-3% target range.

Where we stand now is a situation where the level of excess capacity has grown instead of shrunk in the last 3-6 months. And while the primary sector and rural economies look strong enough, the flow through to the urban economies and critically the services sector seems sufficiently weak to imply its far from assured that at OCR around 3% will deliver above trend growth quickly.

It’s reasonable to assume that inflation will moderate from the 3%-plus level we expect to print in the September and December quarters. The level of excess capacity seems sufficient to achieve an inflation rate closer to 2% in time – although I don’t expect inflation to move significantly below 2%, especially since the exchange rate seems likely to remain weak given low growth and widening interest rate differentials.

The biggest medium-term concern is the risks of monetary policy overshooting. Given where underlying growth momentum appears to be, my sense is that the OCR would need to fall below 2% before those risks become material. And it’s easy enough to take back some stimulus at some stage in 2026 should growth quickly accelerate and bring the OCR back closer to the 3.75% level I continue to see as broadly neutral. Indeed, that scenario would likely be a quality problem I suspect.

A sub-2% OCR would be an entirely different story and not one that’s in the thinking right now. We would need to see some kind of problem – domestic or global – to emerge to justify an OCR below 2%. And questions should be asked of fiscal policy in those circumstances also.

Right now, the concern should be to get the OCR set by Christmas at a level where the MPC can be confident of seeing trend to above trend growth outcomes in the New Year. Doing less now and then having to promise more in February, as was the case at the end of 2024, risks extending unduly the timeframe where growth resumes and the labour market strengthens.

the RBNZ indicated that it expected to reduce the OCR to 2.5% by year end. On balance, the data flow since August – notably the very disappointing June quarter GDP report – has supported the RBNZ’s forecast. Indeed, commentators seem united in the belief that the OCR needs to go to 2.5%, with downside risk beyond. The market has similar views regarding the policy outlook, having quickly moved to price a terminal OCR of 2.25% in the wake of the GDP report.){kind=link}