Australian Dollar advanced in Asian session today, lifted by broad gains across regional equities and improving investor confidence. Japan led the advance, with a technology-driven rally pushing the Nikkei higher. Shares of SoftBank surged over 10% after the company announced plans to acquire the robotics division of Swiss engineering firm ABB, a deal that deepens its ambitions in the AI sector. Founder Masayoshi Son described that as part of the company’s push into “Physical AI.” Son said the deal would merge “Artificial Super Intelligence and robotics” to fuel the next phase of innovation.

Chinese markets also reopened firmly after the holiday break, with AI and gold stocks spearheading gains. The recovery helped offset disappointing consumer data and shifted attention toward the Communist Party’s October 20–23 meeting, where the 15th five-year plan will be unveiled. Investors are watching for signals on technology investment, infrastructure policy, and more importantly, potential stimulus measures to sustain China’s growth narrative into 2026 and beyond.

Meanwhile, Dollar slipped modestly as investors digested the FOMC minutes released overnight. The minutes showed that while policymakers see little scope for rapid easing, they still agree that interest rates are on a downward path, and cuts are in pipeline for the rest of the year. The ongoing government shutdown also weighed on the greenback, with traders hesitant to build new long positions amid fiscal uncertainty and political deadlock.

Among major currencies, Yen remains pinned at the bottom of the performance table, pressured by risk-on flows and expectations that the BoJ will postpone its next rate hike until 2026. Euro is the second weakest, with attention turning to ECB minutes, expected to confirm a continued pause. However, France’s political paralysis continues to overshadow monetary discussions, leaving Euro vulnerable. Swiss Franc also softened as safe-haven demand faded.

On the other side of the ledger,Loonie leads the week, supported by optimism on trade. Prime Minister Mark Carney said bilateral deals with the U.S. were progressing alongside the continental trade framework, noting that discussions with President Donald Trump were “very granular” and showing tangible progress. Aussie ranks second among top performers, just behind the Loonie, while Dollar holds the third place. Kiwi and Sterling are mixed in the middle, with Kiwi staging a mild rebound after its RBNZ-driven selloff.

In Asia, at the time of writing, Nikkei is up 1.53%. Hong Kong HSI is up 0.10%. China Shanghai SSE is up 1.12%. Singapore Strait Times is down -0.17%. Japan 10-year JGB yield is down -0.006 at 1.698. Overnight, DOW closed flat, S&P 500 rose 0.58%. NASDAQ rose 1.12%. 10-year yield rose 0.002 to 4.129.

Fed minutes leans dovish, but no scope for rapid easing

Minutes from the Fed’s September 16–17 meeting, released overnight, show the Committee leaning toward additional rate cuts this year while emphasizing the need for caution in the pace of easing. “Most judged that it likely would be appropriate to ease policy further over the remainder of this year,” the minutes said.

But, officials also acknowledged a “range of views” about how restrictive policy currently is and how fast it should be relaxed. Some members cautioned that “financial conditions suggested monetary policy may not be particularly restrictive,” arguing for patience.

In a key passage, the Committee “stressed the importance of taking a balanced approach” to achieving its dual goals, mindful of “the extent of departures from those goals” and the “different time horizons” for inflation and employment to normalize.

Currently, Core PCE is at 2.9% and unemployment at 4.3%. The Summary of Economic Projections showed inflation to rise to 3.1% by year end, and then only decline gradually to 2.6% in 2026, and 2.1% in 2027. Unemployment is forecast to edge up modestly to 4.5% and then stabilizes.

That combination means the economy is at risk of policy over-restriction: keeping rates too high for too long could cause a sharper, sustained rise in unemployment. But — and this is the key point — the pace of that easing must be gradual as inflation would only slow over the next two years. That means the Fed can’t risk loosening so fast that it reignites price pressures or unanchors expectations.

At the meeting, Fed cut interest rates by 25bps to 4.00-4.25%, with Governor Stephen Miran as the only dissenter voting for a 50bps reduction.

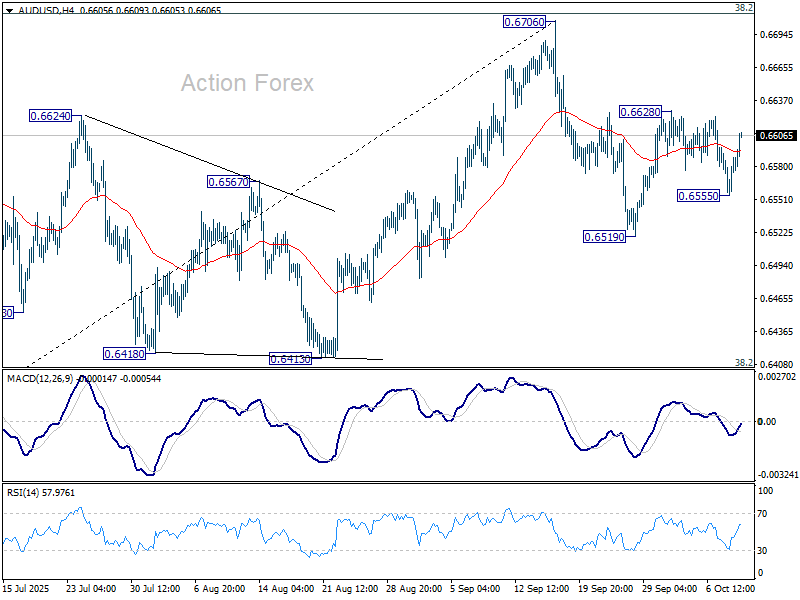

AUD/USD Daily Report

Daily Pivots: (S1) 0.6566; (P) 0.6578; (R1) 0.6598; More...

AUD/USD recovered after dipping to 0.6555 but stays below 0.6628 resistance. Intraday bias stays neutral first. On the upside, break of 0.6628 will resume the rebound from 0.6519 to retest 0.6706 high. However, on the downside, sustained trading below 55 D EMA (0.6558) will confirm rejection by 0.6713 fibonacci resistance, and bring deeper fall to 0.6413 cluster support (38.2% retracement of 0.5913 to 0.6706 at 0.6403).

In the bigger picture, there is no clear sign that down trend from 0.8006 (2021 high) has completed. Rebound from 0.5913 is seen as a corrective move. Outlook will remain bearish as long as 38.2% retracement of 0.8006 to 0.5913 at 0.6713 holds. Nevertheless, considering bullish convergence condition in W MACD, sustained break of 0.6713 will be a strong sign of bullish trend reversal, and pave the way to 0.6941 structural resistance for confirmation.

{kind=link}