Employment: +14.9k (from –11.9k). Unemployment Rate: 4.5% (from 4.3%). Participation Rate: 67.0% (from 66.9%).

- Unemployment rate jumps to a new cycle high of 4.5%, driven by stronger-than-expected labour force participation.

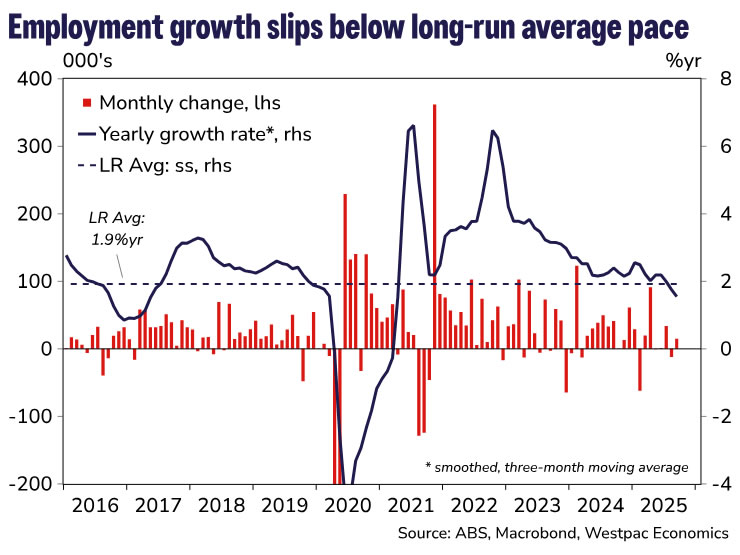

- Employment growth slips to a below-average pace of 1.5%yr amid an underlying slowdown in ‘care economy’ jobs growth.

- Today’s data lends weight to our view that there is still a good chance the RBA will cut rates in November; Q3 CPI data (due October 29) will be the decider.

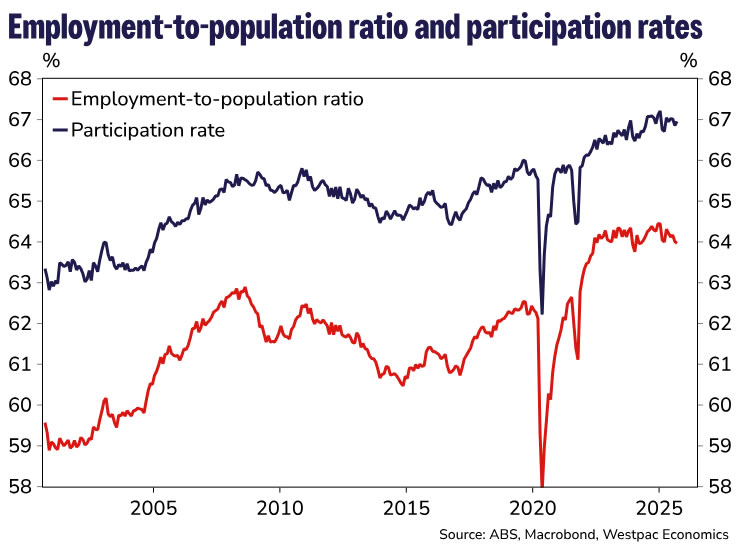

Employment rose by +14.9k (+0.1%) in September, virtually spot on Westpac’s forecast (+15k) but below the market consensus (+20k). On a three-month average basis, employment growth has now slowed to 1.5%yr, down from 2.2%yr six months ago and now well below the long-run average pace of 1.9%yr. This is currently weaker than population growth, seeing the employment-to-population continue to track a downtrend, currently at 64.0% in September.

Underlying this slowdown in employment growth is a rebalancing across industries, with the contribution from the job-intensive ‘care economy’ falling while the market sector stages a gradual and ‘patchy’ recovery. We will not have the complete detail on how the industry mix fared for the September quarter until the next instalment of the Labour Account (due 5 December), but we suspect a continuation of these broad trends.

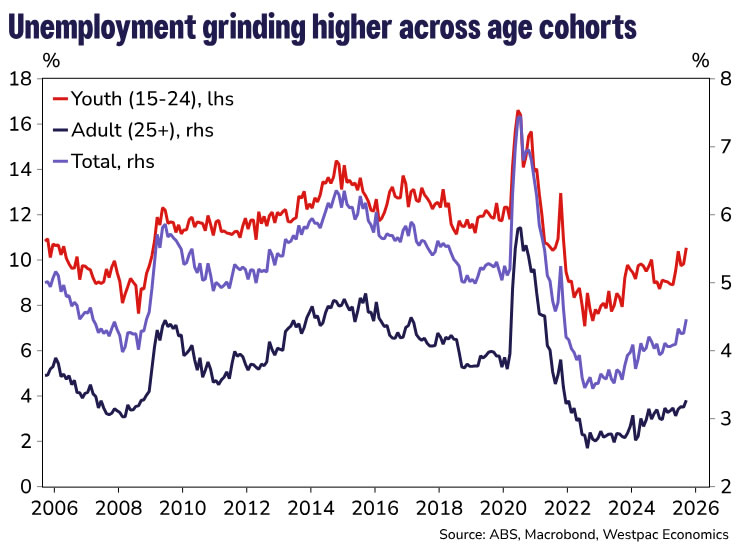

What really caught the market’s attention, though, was the jump up in the unemployment rate from an upwardly revised 4.3% in August to 4.5% in September, the highest recorded so far in this cycle (though at 4.46%, it was close to the rounding barrier). It is also worth noting that youth unemployment also rose +0.8ppts to 10.5%, a new cycle high as well. This echoes the large increase back in June, when we flagged that sharp jumps in cyclically sensitive youth unemployment often precede a grind higher in total unemployment. We are now starting to see this unfold, with ‘adult’ unemployment also moving to a cycle high of 3.3%.

Higher participation, combined with softer hiring, opened up a bit more labour market slack in September. The participation rate lifted to 67.0% from 66.9% (revised up from 66.8%), in line with the year-average to date. There are competing forces underlying the trend for participation – easing cost-of-living pressures and cooling labour demand is driving a cyclical unwind, while demographic factors still look to be driving a structural increase in labour supply. The mix may continue to see ‘bumpy’ moves month-to-month – there is a risk that October could see a partial unwind, which may see the unemployment rate round back down, but we are still confident in our base case that unemployment will continue to trend higher for the rest of the year.

Another part of the data we are closely watching is underemployment, which largely captures part-time individuals who desire more hours in this part of the survey (although there are broader ‘analytical’ measures which expand the scope). The underemployment rate ticked up from 5.7% to 5.9% in September, though it has tracked a gradual downtrend over the past year. We suspect that this can largely be explained by the pull-back in part-time employment growth from its peak of around 6%yr to 2%yr currently, meaning there are relatively fewer part-time workers entering the workforce and seeking extra hours of work. The easing in part-time employment growth has slowed somewhat but there are no clear-cut signs that the downtrend is over just yet.

Conclusion

Today’s data is yet another instalment in a series of readings that clearly indicate the labour market is softening again. Employment growth is already tracking a slightly weaker pace than the RBA had pencilled in for Dec-25 (1.5%yr vs 1.6%yr), and the unemployment rate looks likely to overshoot the RBA’s flat-as-a-pancake projection of 4.3% through to Dec-27. This is a clear challenge to the RBA’s most recent assessments, the Monetary Policy Board describing the labour market as “broadly steady” and “a little tight” at its October meeting.

We are unlikely to see the MPB suddenly embrace a more downbeat view on the labour market – especially given the RBA’s ‘sticky’ NAIRU assumption that is higher than that of most market economists. Today’s data could see the language start to pivot, however. The market reaction has lent weight to our view that a 25bp cut in November is a good chance. Swaps markets now pricing in roughly a 75% chance of a cut versus 40% prior to the data. Still, the Q3 CPI (due 29 October) will be the ultimate deciding factor.

, and the unemployment rate looks likely to overshoot the RBA’s flat-as-a-pancake projection of 4.3% through to Dec-27. This is a clear challenge to the RBA’s most recent assessments, the Monetary Policy Board describing the labour market as “broadly steady” and “a little tight” at its October meeting.){kind=link}