We are looking for cautious optimism in Canada’s manufacturing and wholesale reports for September in the coming week.

Manufacturing has borne the brunt of the negative fallout from U.S. tariffs since spring. Production contracted an annualized 9% in Q2. That was the largest one quarter decline outside of the 2020 pandemic since the 2008/09 recession.

But, the sector has shown signs of stabilizing. Average production over July and August is little changed from Q2, and the advance estimate of manufacturing sales in September jumped 2.8%. Part of that increase likely reflects higher prices. Canadian industrial output prices rose1.3%, seasonally adjusted, by our count in September led by higher petroleum prices. That still leaves volume up 1 ½ % from August.

Most Canadian exports have remained duty free under exemptions for CUSMA compliant trade. Details in manufacturing sales next Friday will be closely watched to gauge the impact of U.S. tariffs on targeted subsectors. Early evidence is starting to suggest that tariff impact on these sectors may have been smaller than feared with U.S. buyers appearing to struggle to find alternative cheaper sources.

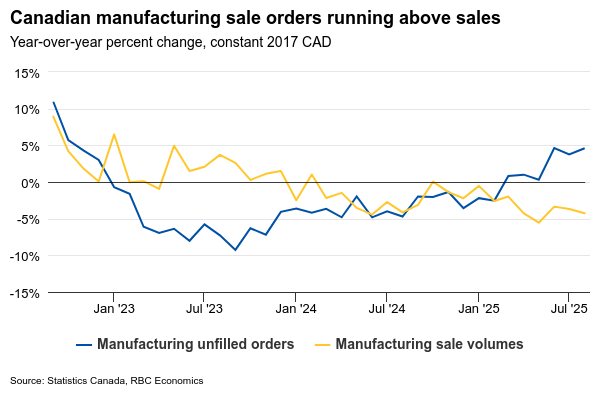

Unfilled Canadian manufacturing orders were still up 4.6% from a year ago, and 2.7% since March as of August. Exports of steel products have fallen sharply, but aluminum production and prices are both up from a year ago (1.8% in August and 15% in September, respectively). Employment in the aluminum sector (from SEPH data) was up 8% since March as of August.

Concerns remain about the outlook for motor vehicles, but the number of vehicles produced in Canada in September was slightly above year ago levels.

Jobs in manufacturing and wholesale are up

The advance estimate of September wholesale sales (ex-petroleum) from Statistics Canada was little changed after declining 1.2% in August, but rising 1.7% in July. That would leave sales up an annualized 5% in Q3. Seasonally adjusted, September saw the largest monthly increase in both manufacturing and wholesale employment since January.

Overall, stabilizing industry data are in line with steadying trade flows in Q3. It suggests CUSMA exemptions are still working effectively to backstop the bulk of Canada-U.S. trade even as the details after July can’t be directly reported from U.S. Census Bureau’s trade data that’s critically delayed by the ongoing U.S. government shutdown.

U.S. data including October’s consumer price index and retail sales will not be released on schedule in the coming week. Not only is reading the U.S. economy becoming increasingly foggy, the shutdown— now at a record—is having a larger direct economic impact, especially if crucial SNAP benefits are curtailed.

{kind=link}