Japan remains the center of attention in an otherwise quiet Asian session, with traders focused on the relentless climb in JGB yields. The 10-year benchmark surged to a fresh 18-year high today and appears poised to challenge the psychological 2% handle soon, an escalation that is increasingly difficult for global markets to ignore.

Much of the pressure stems from Prime Minister Sanae Takaichi’s JPY 18.3 trillion stimulus package, which has put the government on a collision course with investors concerned about fiscal sustainability. The scale of the planned spending, combined with a softening stance on fiscal consolidation, has amplified expectations for higher long-term borrowing costs.

Earlier this week, Japan’s Fiscal System Council retreated from its previous call for a rapid return to surplus, instead advising only an annual review of the primary balance. Markets interpreted the shift as clearing the runway for Takaichi to pursue more aggressive stimulus—reinforcing fears that Japan’s debt could steepen further.

Finance Minister Satsuki Katayama pushed back today, stressing that the supplementary budget was crafted with sustainability in mind and that fiscal responsibility will guide the FY2026 budget. But these assurances have done little to ease investor unease.

In parallel, markets have intensified bets on a December 19 BoJ rate hike to 0.75%, fuelled by recent comments from Governor Kazuo Ueda and signs of improved communication between the new cabinet and the central bank. Katayama noted positive engagement with Ueda since taking office, while emphasizing the BoJ’s operational independence—remarks seen as a subtle green light for further tightening.

The key question for traders now is whether soaring JGB yields and rising BoJ expectations will translate into a durable rebound in Yen. A meaningful JPY rally raises the risk of triggering the kind of carry-trade unwind seen last year, an unwind that briefly shook global risk assets and exposed vulnerabilities in leveraged positioning.

In the currency markets, Dollar remains pinned at the bottom of the weekly performance chart, with today’s US personal income, spending, PCE inflation, and consumer sentiment data unlikely to spark a sustained recovery. Swiss Franc and Loonie follow as the next weakest performers.

At the strong end, Aussie continues to lead as markets doubt whether the RBA has room to cut rates again next year. Yen follows in second place, while Sterling also benefits from improved domestic sentiment. Kiwi and Euro sit in the middle of the pack.

In Asia, Nikkei fell -1.22%. Hong Kong HSI is up 0.31% at the time of writing. China Shanghai SSE is up 0.71%. Singapore Strait Times is down -0.24%. Japan 10-year JGB yield rose 0.01 to 1.951. Overnight, DOW fell -0.07%. S&P 500 rose 0.11%. NASDAQ rose 0.22%. 10-year yield rose 0.051 to 4.108.

Japan household spending slumps -3.0% yoy in October, casting doubt over strength of recovery

Japan’s household spending fell sharply by -3.0% yoy in October, far below expectations for 1.1% yoy increase, and marking the steepest decline since January 2024. It was also the first annual drop in six months.

On a monthly, seasonally adjusted basis, spending plunged -3.5% mom, defying forecasts of a 0.7% mom growth. Lower outlays on food, leisure and automobile-related expenses drove the weakness, though officials said it remains unclear whether the decline represents a one-off setback, noting consumption is still perceived to be in a recovery phase.

The data arrive at a delicate moment for the BoJ. Markets have ramped up bets on a rate hike this month following recent comments from Governor Kazuo Ueda that the Bank would weigh the “pros and cons” of further tightening. The slump in spending, however, introduces fresh uncertainty around the durability of domestic demand—one of the BoJ’s key criteria for normalizing policy continuously.

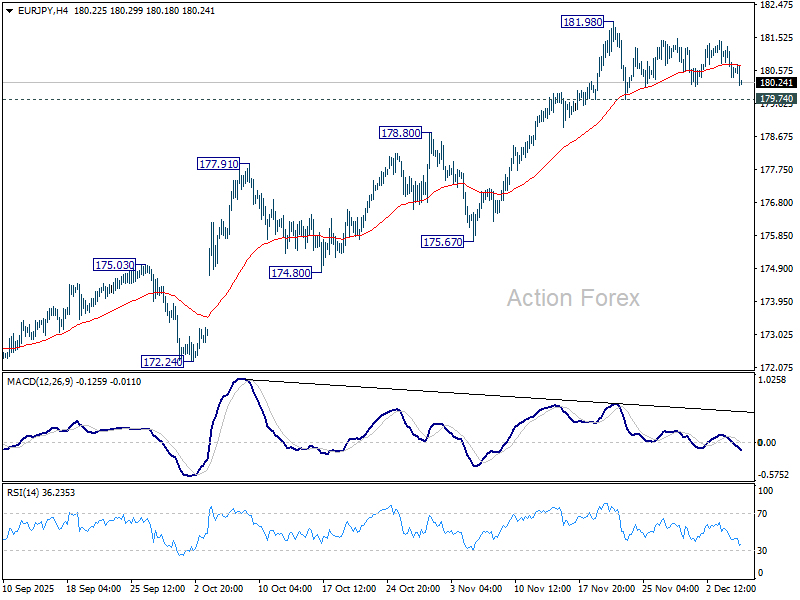

EUR/JPY Daily Outlook

Daily Pivots: (S1) 180.24; (P) 180.77; (R1) 181.14; More…

EUR/JPY dips again today but stays above 179.74 support. Intraday bias remains neutral and another rally is still in favor. On the upside, break of 181.98 will target 100% projection of 161.06 to 173.87 from 171.09 at 183.90 next. However, firm break of 178.80 will argue that deeper correction is already underway towards 55 D EMA (now at 177.81).

In the bigger picture, up trend from 114.42 (2020 low) is in progress and should target 61.8% projection of 124.37 to 175.41 from 154.77 at 186.31. However, considering bearish divergence condition in D MACD, upside should be capped by 186.31 on first attempt. Outlook will continue to stay bullish as long as 55 W EMA (now at 169.87) holds, even in case of deep pullback.

{kind=link}