Dollar came under broad pressure in early US trade after delayed employment data confirmed a deeper-than-expected loss of momentum in the labor market. The October payrolls collapse was the key shock. A steep contraction marked the third negative print in six months, a development that few had anticipated. To compound the damage, both August and September payroll figures were revised lower, deepening the sense that job growth has been deteriorating for longer than previously believed.

November’s payroll rebound came in slightly above expectations, but the modest gain was far from sufficient to offset the earlier damage. Taken together, the data painted a retrospective picture that strongly validates the Fed’s decision to deliver another rate cut last week.

That said, the release did little to shift expectations for January, where a pause remains the clear base case. Instead, the repricing was concentrated further out the curve. Market-implied odds for a March cut jumped above 55%, reflecting growing conviction that easing will resume sooner rather than later.

With the Fed having penciled in one additional 25bps cut for 2026, debate remains on timing rather than direction. The risk is that markets start pulling that cut forward into early 2026 if labor market weakness persists.

The key uncertainty is whether November’s recovery represents a genuine inflection point. Part of the improvement was attributed to reduced uncertainty following the one-year US–China tariff truce. Whether that relief translates into sustained hiring momentum is an open question.

Besides, speculation around the next Fed Chair intensified. Betting markets have shifted sharply toward former Fed Governor Kevin Warsh, whose odds surged on Kalshi to around 46%, overtaking Kevin Hassett. Just a week ago, Hassett was the clear favorite at 77%. The shift follows reported pushback from senior advisers close to the president, who view Hassett as too closely aligned with Trump.

In FX markets this week, Yen is currently the strongest performer, followed by Sterling and Swiss Franc. Aussie and Dollar lag, with Kiwi also under pressure, while Euro and Loonie trade mid-pack—reflecting a cautious and uneven risk environment rather than a clean risk-on tone. UK 10-year yield is up 0.053 at 4.561.

In Europe, at the time of writing, FTSE is down -0.64%. DAX is down -0.44%. CAC is down -0.05%. Germany 10-year yield is up 0.015 at 2.870. Earlier in Asian, Nikkei fell -1.56%. Hong Kong HSI fell -1.54%. China Shanghai SSE fell -1.11%. Singapore Strait Times fell -0.21%. Japan 10-year JGB yield fell -0.004 to 1.955.

US NFP falls -105k in October, overshadows November bounce

US labor market data for October and November painted a clear picture of weakness. Payrolls plunged by -105k in October, the sharpest monthly decline since late 2020. November delivered a rebound of 64k jobs, beating expectations, but the gain was far too small to offset the prior month’s contraction, leaving overall payroll growth effectively flat since April.

Labor market slack continued to build. The unemployment rate rose to 4.6% in November, above expectations and up from 4.4% previously in September. That increase came alongside a modest rise in the labor force participation rate to 62.5%, suggesting that some of the uptick in unemployment reflects workers re-entering the labor market rather than outright layoffs.

Wage growth offered little offsetting support. Average hourly earnings rose just 0.1% mom, well below expectations of 0.3% mom, reinforcing signs that pay pressures are easing as demand for labor cools. The combination of weak net job creation, rising unemployment, and softer wages strengthens the case that the US labor market is losing momentum.

Also released, retail sales was flat mom in October, below expectation of 0.2% mom. Ex-auto sales rose 0.4% mom, slightly above expectation of 0.3% mom

Eurozone growth loses steam as PMIs slide into year-end

Eurozone PMI data for December pointed to a clear loss of momentum heading into year-end. PMI Manufacturing slipped from 49.6 to 49.2, an eight-month low. PMI Services also eased from 53.6 to 52.6, dragging PMI Composite down from 53.8 to 51.9 and signaling a broader slowdown in activity.

According to Hamburg Commercial Bank, the weakness was driven mainly by Germany, where the industrial downturn intensified. France showed tentative signs of industrial stabilization, but that improvement was offset by stagnation in services. Germany’s service sector, by contrast, continued to expand solid. Overall, the data suggests that “the runway into the new year seems pretty unstable”.

Cost inflation in the service sector accelerated to its highest level in nine months, reinforcing the ECB’s concern over wage-driven price pressures. With the central bank meeting on December 18 and closely monitoring services inflation, the PMI data is likely to validate its stated preference to leave interest rates unchanged, despite softer growth signals.

German ZEW sentiment rises to 45.8, but conditions still weak

German investor sentiment improved notably in December, with ZEW Economic Sentiment index rising from 38.5 to 45.8, well above expectations of 40.0. The gain signals growing optimism about the medium-term outlook, even as Current Situation Index fell from -78.7 to -81.0, undershooting forecasts of -76.2.

Across the Eurozone, sentiment strengthened even more decisively. ZEW Economic Sentiment index jumped from 25.0 to 33.7, comfortably beating expectations of 26.3, suggesting confidence is building that the region may be nearing a turning point after a prolonged period of stagnation. However, Current Situation Index edged lower by -1.2 pts to 28.5.

ZEW President Achim Wambach said expectations have become more positive after three years of economic stagnation, with expansive fiscal policy expected to inject fresh momentum into the German economy. Still, he cautioned that the “recovery remains fragile”, with persistent trade conflicts, geopolitical tensions, and weak investment likely to feature prominently on the reform agenda heading into 2026.

UK PMIs points to 0.2% growth in December, post-budget clarity lifts activity

UK PMI surveys delivered a more constructive signal in December, pointing to firmer momentum at year-end. PMI Manufacturing jumped from 50.2 to 51.2, a 15-month high, while PMI Services rose from 51.3 to 52.1. PMI Composite also climbed to 52.1 from 51.2.

S&P Global noted that businesses were buoyed by the “post-Budget lifting of uncertainty”. The survey is consistent with GDP growth accelerating to around 0.2% in December, though momentum for the fourth quarter as a whole remains more modest at roughly 0.1%.

Despite the improvement, growth remains uneven. Output and demand are still described as “lackluster overall”, with expansion heavily reliant on technology and financial services. Many other sectors continue to struggle or remain in outright contraction. Job losses were reported as worryingly widespread, raising doubts over whether stronger orders will translate into renewed hiring, particularly with staff costs still cited as a major pressure.

Taken together, the PMI data supports expectations for a further rate cut at the December MPC meeting, while reinforcing that the path for additional easing in 2026 will remain highly data dependent.

UK payrolls decline deepens even as earnings stay elevated

UK labor market data for November pointed to further cooling in employment conditions. Payrolled employment fell by -38k on the month, a -0.1% mom. Annual drop widened to -171k, or 0.6% yoy. Annual payroll growth has now been negative every month since March.

Wage indicators showed clearer signs of easing at the margin. Median monthly pay growth slowed sharply to 2.7% yoy, down from 3.7% previously and less than half the pace seen in August. At the same time, the claimant count rose by 20.1k.

That said, broader earnings data remains elevated. In the three months to October, unemployment rate edged up from 5.0% to 5.1%. Average earnings growth surprised to the upside, rising 4.7% yoy including bonuses and 4.6% yoy excluding bonuses.

Japan’s PMI composite falls to 51.5, slowing momentum but manufacturing nears expansion

Japan’s December PMI data pointed to a modest cooling in overall momentum, while offering tentative signs of stabilization in manufacturing. PMI Manufacturing rose from 48.7 to 49.7. PMI Services eased from 53.2 to 52.5, while PMI Composite slipped from 52.0 to 51.5, indicating slower but still positive private-sector growth.

According to S&P Global, Japan’s private sector ended the year on a relatively strong footing, with output continuing to expand and new business rising further. Firms responded by stepping up hiring, with employment growth accelerating to its fastest pace in more than a year and a half. Growth remained concentrated in services, though the decline in manufacturing output and sales softened noticeable.

Forward-looking signals were more cautious. Business confidence weakened, particularly among manufacturers, reflecting subdued foreign demand and concerns about the outlook for 2026. At the same time, cost pressures intensified, with input prices rising at the fastest pace since April. Firms responded by raising output charges “at a solid pace”.

Australia PM composite falls to 51.1, growth cooling but persistent price pressures

Australia’s PMI readings for December pointed to moderating growth momentum toward year-end. PMI Manufacturing rose from 51.6 to 52.2, signaling a stronger expansion in factory activity. PMI Services slipped from 52.8 to 51.0. As a result, PMI Composite eased from 52.6 to 51.1, the lowest level in seven months.

The slowdown in overall activity was accompanied by more encouraging details beneath the surface. According to S&P Global, new orders continued to rise at a solid pace, while business confidence improved in December. Employment growth also remained robust, with job creation sustained at faster rates across both manufacturing and services, suggesting firms remain confident enough in demand to continue hiring.

Inflation signals, however, firmed again. Cost pressures intensified for Australian businesses, prompting companies to raise output prices more quickly in an effort to “defend their margins”. As a result, output price inflation returned to its long-run average after two months of subdued increases.

Australia Westpac consumer sentiment falls back to 94.5, bounce proves short-lived

Australian consumer confidence fell sharply in December, reversing November’s brief improvement. The Westpac Consumer Sentiment Index dropped -9.0% mom to 94.5, slipping back toward levels seen prior to last month’s surprise bounce. The pullback leaves sentiment only in “cautiously pessimistic” territory as the year comes to a close.

Westpac noted that while confidence has improved meaningfully from the deep and prolonged pessimism that dominated much of 2024, households remain reluctant to shift into outright optimism. The November rebound marked the first net positive reading since the economy reopened after the pandemic, but the latest data suggests that underlying confidence remains fragile and easily unsettled.

The survey reinforces a cautious backdrop for the RBA ahead of its February 2–3 meeting. While inflation has picked up recently, there are few signs that tight labor markets or strong consumer demand are driving the move. Instead, administered prices outside the reach of monetary policy have been a key factor. As those pressures fade, inflation is expected to resume its path toward the midpoint of the target range, though policymakers have warned that if normalization proves slow, rates may need to stay on hold for longer, with hikes still a live contingency.

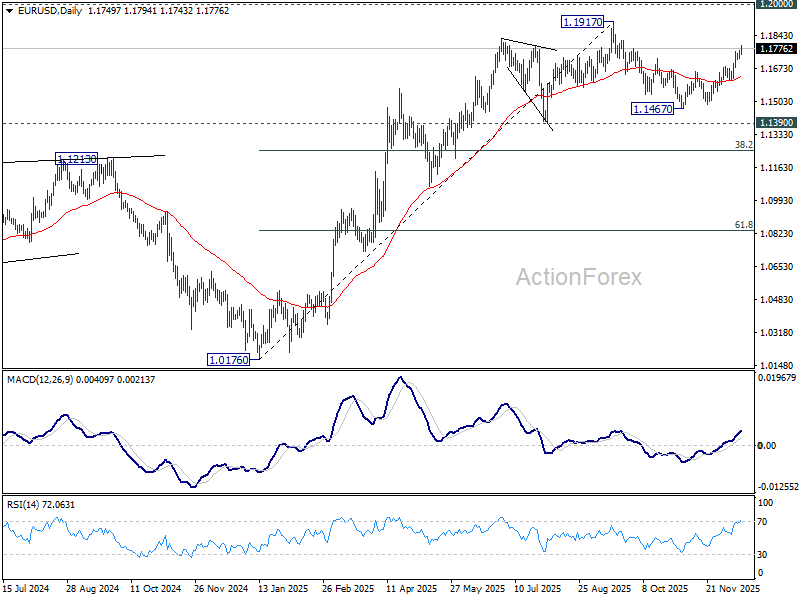

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1723; (P) 1.1737; (R1) 1.1753; More….

EUR/USD’s rise from 1.1467 resumed after brief consolidations and intraday bias is back on the upside, retest of 1.1917 high should be seen next, and decisive break there will resume larger up trend. On the downside, below 1.1718 minor support will turn intraday bias neutral again and bring more consolidations.

In the bigger picture, as long as 55 W EMA (now at 1.1373) holds, up trend from 0.9534 (2022 low) is still in favor to continue. Decisive break of 1.2 key psychological level will carry larger bullish implication. However, sustained trading below 55 W EMA will argue that rise from 0.9534 has completed as a three wave corrective bounce, and keep long term outlook bearish.

{kind=link}