Currency markets have entered deep holiday mode, with trading exceptionally subdued despite sharp swings elsewhere, notably in precious metals. In FX, volume and volatility have both contracted sharply. With liquidity thin and risk appetite selective, traders are choosing patience over positioning, especially with little fresh macro information to work with.

December minutes from the Fed due today may inject temporary noise, but expectations for a lasting impact are muted. The Fed has already signaled a higher bar for further easing, anchoring near-term expectations for a hold in January. Attention remains on March, but clarity is lacking. Whether rate cuts resume then will depend on multiple rounds of jobs and inflation data, leaving markets hesitant to commit either way.

Geopolitics continues to simmer in the background. In East Asia, China escalated military activity around Taiwan, firing rockets into surrounding waters today and deploying new amphibious assault vessels alongside air and naval forces. Elsewhere, diplomatic progress in Europe faced a setback after Russia accused Ukraine of targeting President Vladimir Putin’s residence, a claim rejected by Kyiv and seen by some as an attempt to derail fragile negotiations.

For the week so far, Kiwi underperforms, followed by Aussie and Loonie. Yen leads gains ahead of Sterling and Swiss Franc. Dollar and Euro sit mid-pack. Still, nearly all major pairs remain confined within last week’s ranges, reinforcing the view that markets are consolidating, without directional intent.

Swiss KOF barometer rises to 101.7, manufacturing outlook strengthens

Swiss KOF Economic Barometer rose from 101.7 to 103.4 in December, beating expectations of 101.4 and signaling improving momentum heading into early 2026. According to KOF Swiss Economic Institute, the outlook for the Swiss economy at the turn of the year is now above its long-term average.

The improvement is being driven primarily by the production side of the economy. Indicator bundles linked to output showed broad-based gains, with manufacturing standing out as a particular bright spot.

However, the picture was uneven. On the demand side, indicators tied to private consumption and foreign demand remain under pressure, highlighting lingering caution among households and external headwinds.

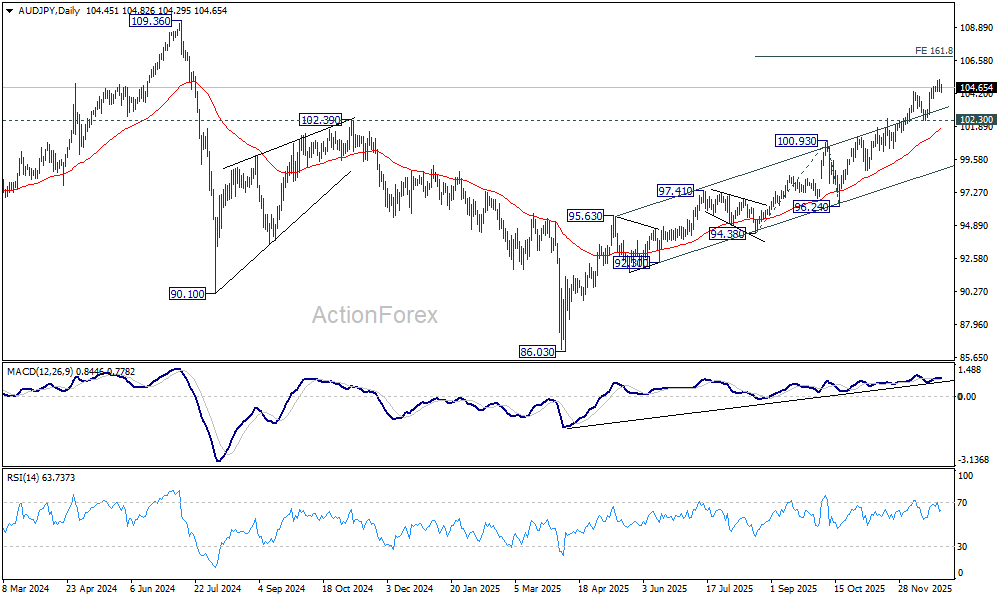

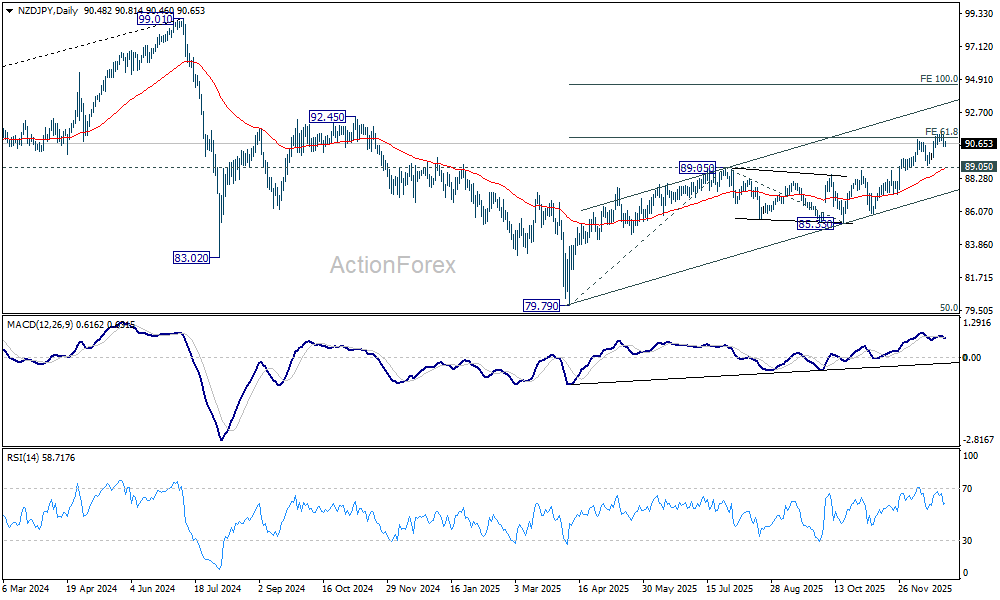

Structural Yen weakness to persist Into 2026, AUD/JPY accelerates, NZD/JPY follows

Yen’s inability to stage a meaningful rebound has become a defining feature of late-year trading. Even the BoJ’s December rate hike failed to generate sustained support, highlighting how entrenched the bearish forces have become.

Carry trade dynamics remain central. Nikkei has enjoyed a powerful uptrend this year, helped by optimism surrounding Prime Minister Sanae Takaichi’s new administration and ongoing enthusiasm for AI- and tech-linked stocks, despite persistent valuation concerns.

The scale of the rally has been striking. From levels around 30,000 in April, Nikkei surged to fresh record highs above 50,000 by early November, marking one of its strongest advances in decades. While some jitters have emerged since November, the index has so far held comfortably in a broad range around 50,000. That consolidation suggests underlying momentum remains intact, leaving scope for another leg higher early next year.

At the same time, fiscal concerns are quietly intensifying. Japan’s expansive budget stance has pushed long-dated yields higher. Thirty-year JGB yields remain close to record highs near 3.4%, while 10-year yields hover above the 2% mark, levels not seen in decades. Even so, yields remain artificially suppressed. The crucial context is that the BoJ is still a massive buyer of government bonds in gross terms, effectively capping long-term yields.

As a result, risks that would normally push yields much higher—such as fiscal sustainability concerns—are instead being priced into Yen. That dynamic leaves the currency vulnerable to further downside in the months ahead. Even direct government intervention, should it move beyond verbal warnings, is unlikely to offer lasting relief

Among Yen crosses, AUD/JPY and NZD/JPY are particularly constructive, supported by emerging speculation that RBA and RBNZ could return to rate hikes in early 2027, or even in late 2026.

Technically, AUD/JPY’s up trend from 86.03 is still in progress. The strong bounce from prior medium term channel ceiling is a clear bullish signal, which solidifies that it’s in upside acceleration. Outlook will continue to stay bullish as long as 102.30 support holds. Next target is 161.8% projection of 94.38 to 100.93 from 96.24 at 106.83. There is prospect of retesting 109.36 (2024 high) next year if momentum continues.

NZD/JPY is underperforming AUD/JPY primarily because RBNZ out-eased RBA much this year. Still, the up trend from 79.79 remains intact and healthy. Near term outlook in NZD/JPY will stay bullish as long as 89.05 resistance turned support holds. Sustained trading above 61.8% projection of 79.79 to 89.05 from 85.33 at 91.05 would likely prompt upside acceleration towards 100% projection at 94.59 next.

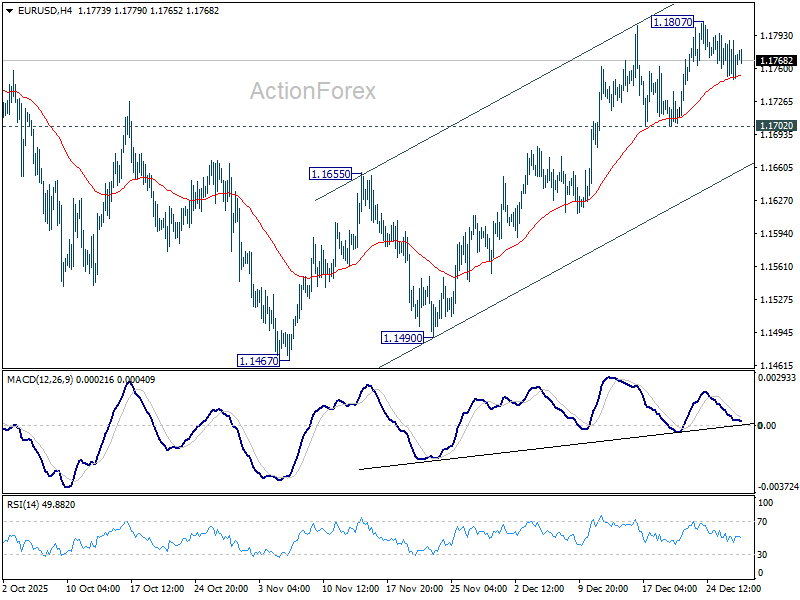

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1752; (P) 1.1771; (R1) 1.1791; More….

EURUSD is extending consolidations below 1.1807 and intraday bias stays neutral. Further rally is in favor as long as 1.1702 support holds. Break of 1.1807 will resume the rise from 1.1467 to retest 1.1917 high. However, firm break of 1.1702 will turn bias back to the downside for 1.1467 support, to extend the corrective pattern form 1.19717 with another falling leg.

In the bigger picture, as long as 55 W EMA (now at 1.1386) holds, up trend from 0.9534 (2022 low) is still in favor to continue. Decisive break of 1.2 key psychological level will carry larger bullish implication. However, sustained trading below 55 W EMA will argue that rise from 0.9534 has completed as a three wave corrective bounce, and keep long term outlook bearish.

{kind=link}