Yen is once again attempting to recover from its recent sharp losses, with momentum this time supported by a more forceful policy backdrop. Japanese authorities have stepped up verbal intervention, and crucially, officials have gone beyond routine warnings and have explicitly flagged the possibility of joint action with the US. Additionally, combined with speculation of earlier BoJ rate-hike , this has strengthened the perception that Japan is increasingly determined to defend the 160 level against Dollar.

That shift matters for positioning. After weeks of one-way yen selling, this week’s developments argue that Tokyo is no longer comfortable letting depreciation run unchecked. With that resolve now more visible, speculators may be reluctant to test the authorities aggressively in the near term, opening scope for a more sustained rebound in USD/JPY.

Japanese Finance Minister Satsuki Katayama reinforced the message on Friday, saying the government is ready to take “decisive action” to stem Yen’s continued fall. “I have repeatedly said that we will take every possible measure,” she told reporters. Katayama pointed specifically to last September’s joint statement with the US, emphasizing that its language on intervention was deliberate. Importantly, she stressed that the statement does not specify whether intervention must be coordinated, adding that “no options are excluded.”

Monetary policy expectations are also in flux. According to a Reuters report, some BoJ policymakers see scope for raising rates earlier than markets expect, with April under discussion if Yen weakness amplifies inflationary pressures. That view contrasts with broader market consensus. Analysts polled by Reuters still expect the BoJ to wait until July before hiking again, with more than 75% forecasting rates to reach 1% or higher by September. Still, the gap between official thinking and market pricing is narrowing.

Sources suggest some policymakers are willing to move sooner if evidence builds that Japan can sustainably meet its 2% inflation goal. The BoJ is also expected to revise up its fiscal 2026 growth and inflation projections at next week’s meeting, adding to the sense of policy optionality. That said, there remains no consensus within the policy board. Governor Kazuo Ueda has consistently signaled caution, stressing the need to assess how previous rate hikes affect a still-fragile economy before committing to faster normalization.

In FX performance terms this week, Kiwi remains the strongest, lifted again by robust domestic manufacturing data released today. Aussie follows, supported by stable risk sentiment, with Loonie third as it digests recent losses. Euro is the weakest, followed by the Swiss franc and then Yen, which has stabilized but not yet decisively turned. Sterling and Dollar are trading in the middle of the pack.

ECB’s Lane: Remarkably stable baseline leaves no near-term rate debate

ECB Chief Economist Philip Lane said the Eurozone is now in a “remarkably stable situation,” arguing there is “no near term interest rate debate” under the central bank’s baseline scenario. Speaking in an interview with La Stampa, Lane said the current policy setting is consistent with inflation staying around target, growth close to potential, and low, declining unemployment.

Lane stressed that the current level of interest rates provides the baseline for “the next several years.” With the economy expected to grow in the neighborhood of its potential rate, he said it would take a significant acceleration in activity to push outcomes meaningfully above the baseline and trigger a policy response.

One alternative scenario he flagged was a major global disruption similar to 2021–2022, involving supply-chain bottlenecks. Lane described this as a “nightmarish” outcome, noting it would also carry recessionary forces rather than a clean inflationary impulse.

NZ BNZ PMI surges to 56.1, a four-year high

New Zealand’s manufacturing sector ended 2025 on a strong footing, with the BusinessNZ Performance of Manufacturing Index jumping sharply from 51.7 to 56.1 in December. The reading marked the highest level of activity since December 2021 and moved decisively above the long-run average of 52.5.

The rebound was broad-based. Production rose from 53.2 to 57.4, while new orders surged from 52.5 to 59.8, pointing to strong demand momentum. Employment also improved, climbing from 52.6 to 53.8, suggesting firms are beginning to respond to higher workloads. Positive commentary from respondents increased to 57.1%, up from 54.4% in November and just 45.9% in October.

BNZ Senior Economist Doug Steel said the PMI is positive for Q4 GDP calculations and points to good momentum heading into the new year, flagging “upside risks” to already constructive near-term growth forecasts.

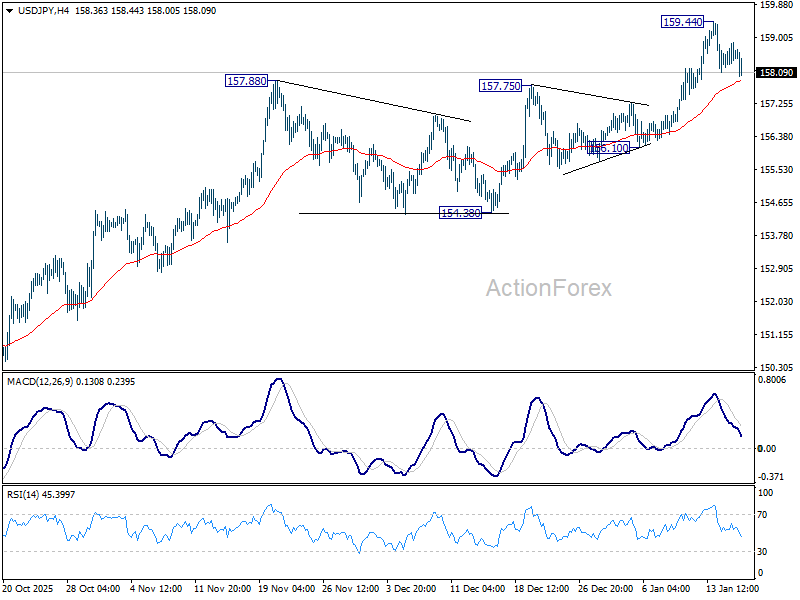

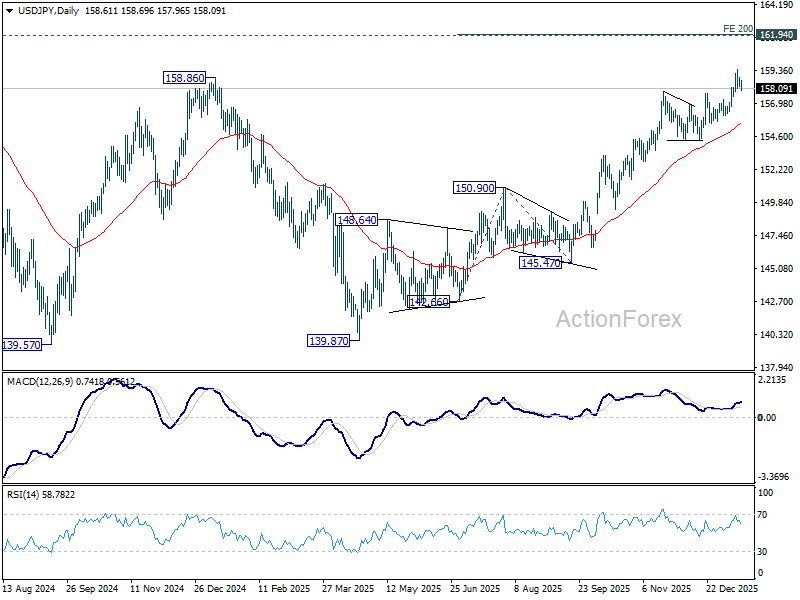

USD/JPY Daily Outlook

Daily Pivots: (S1) 158.26; (P) 158.57; (R1) 158.94; More…

USD/JPY’s retreat from 159.44 extends lower today. Intraday bias remains neutral for the moment, and deeper fall could be seen. But downside should be contained above 156.10 support to bring another rally. On the upside, above 159.44 will resume larger rise from 139.87. Next target is 200% projection of 142.66 to 150.90 from 145.47 at 161.95, which is close to 161.94 high.

In the bigger picture, corrective pattern from 161.94 (2024 high) could have completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94. Decisive break of 158.85 structural resistance will solidify this bullish case and target 161.94 for confirmation. On the downside, break of 154.38 support will dampen this bullish view and extend the corrective range pattern with another falling leg.

{kind=link}