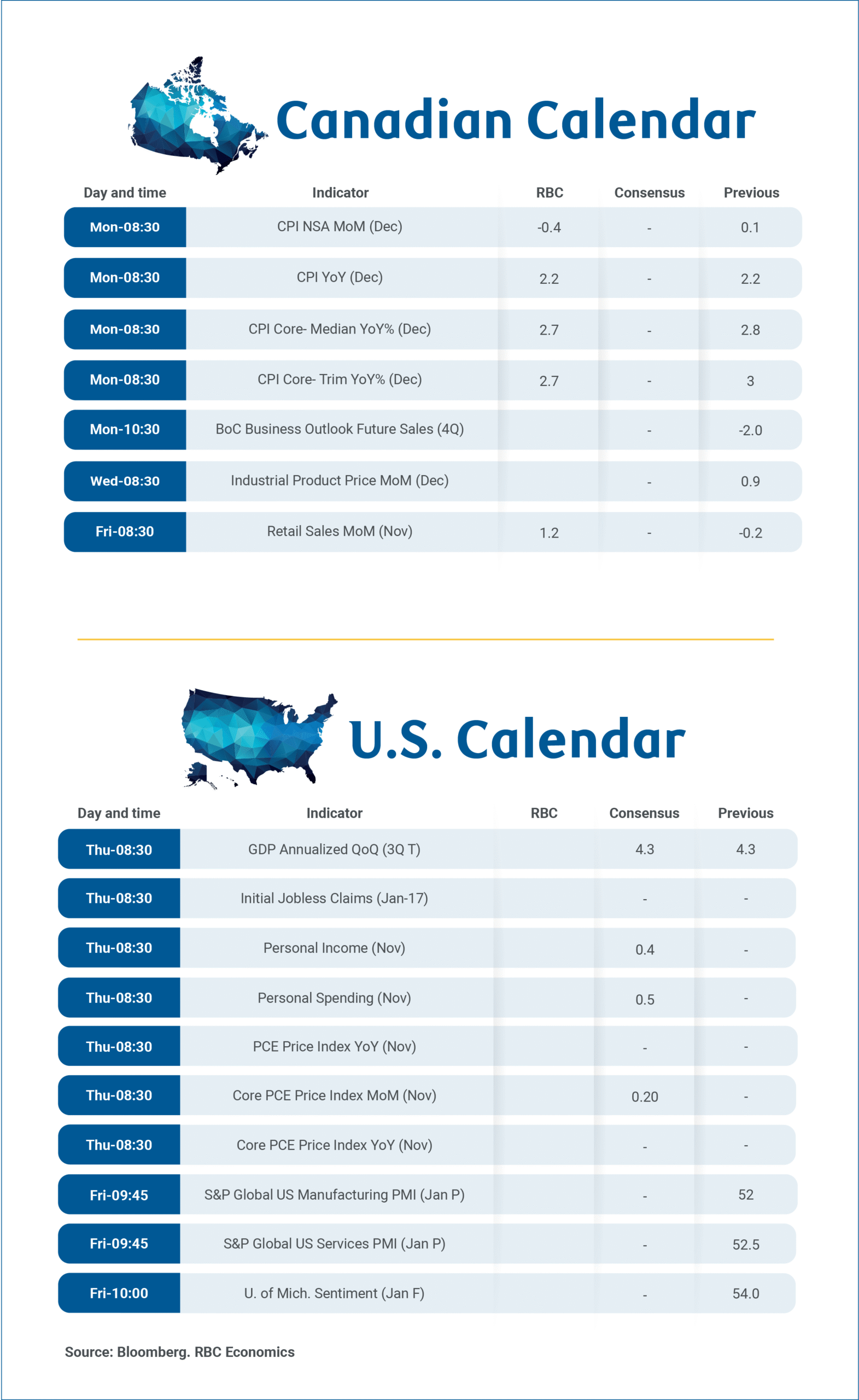

There’s a full slate of Canadian data releases in the coming week kicking off with the final monthly inflation report for 2025 and the Bank of Canada’s closely watched Business Outlook Survey for Q4 on Monday, along with November’s retail sales on Friday.

We expect headline inflation trended broadly sideways in December, matching the 2.2% year-over-year in November. We anticipate little-changed core price growth trends that leave inflation still running moderately above the Bank of Canada’s inflation target.

An 8% drop in December gasoline prices should push energy prices further below a year ago. However, food inflation remained elevated for much of 2025 following short-lived easing late in 2024. We look for food price growth to rise above 5% in December—in part due to low after-tax restaurant prices a year earlier during the GST/HST tax holiday. But, grocery price inflation also remains elevated (4.7% as of November).

Inflation, excluding food and energy products, is expected to edge lower to 2.3% from 2.4% in November. If realized, this would mark a second consecutive month of improvement. The BoC’s median and trim CPI measures were similar year-over-year from the 2.8% increases in November (still above the BoC’s 2% inflation target).

Headline inflation compared to a year ago will continue to be distorted by tax changes. The removal of the consumer carbon tax in most provinces in April 2025 continues to lower annual energy price growth. The temporary GST/HST tax break introduced mid-December 2024 (stretching through mid-February 2025) will artificially raise annual price growth in December. Although, an offsetting rise in pre-tax prices a year ago will limit the impact.

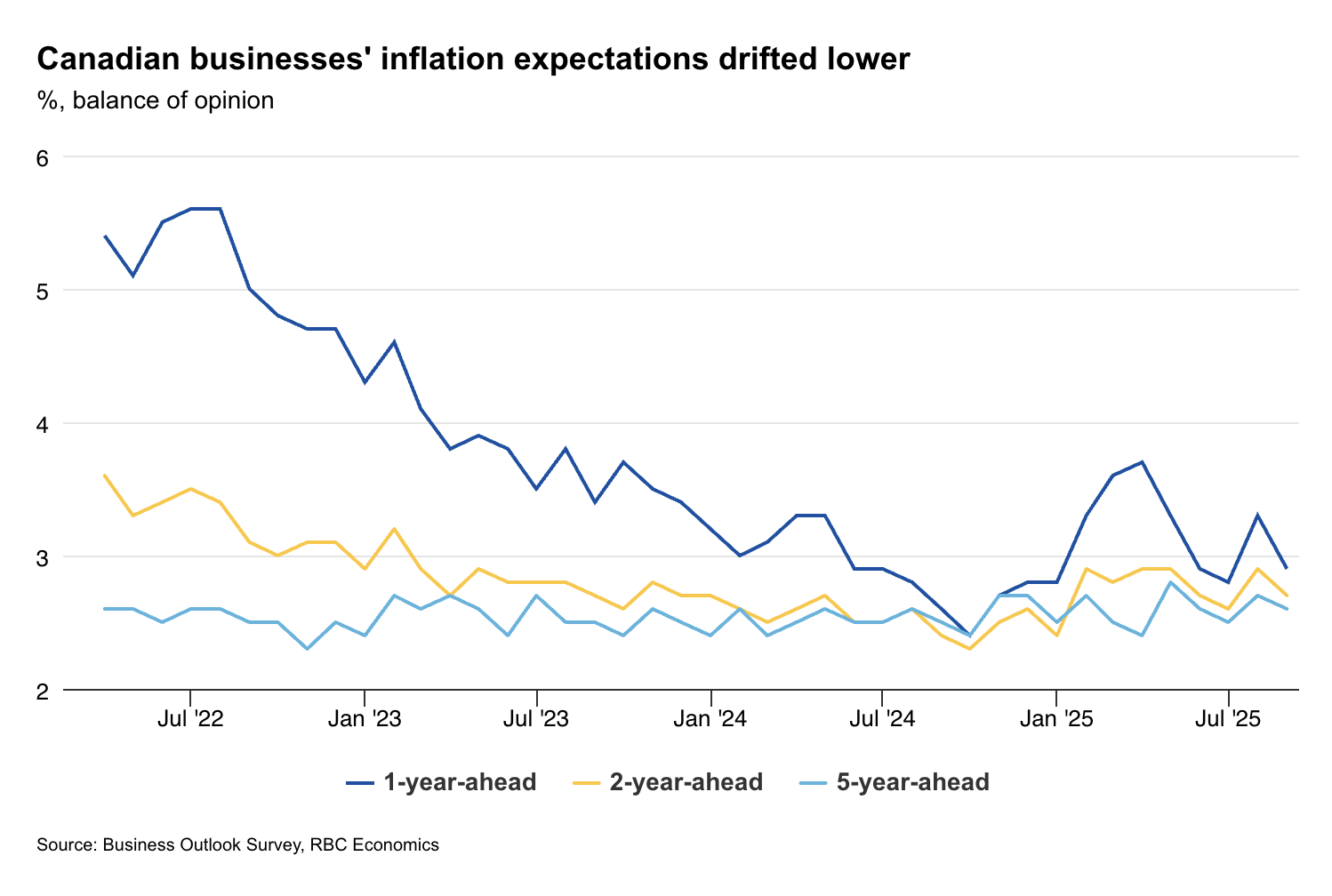

Muted demand, cautious pricing and restrained hiring

The Q4 Business Outlook Survey comes ahead of the next interest rate decision later this month. In Q3, the survey reinforced the picture of an economy stabilizing, albeit at a subdued level. We expect to see more of the same in Q4 with muted demand, cautious pricing behaviour, and restrained hiring plans.

Still, significant downside international trade scenarios feared earlier this year have yet to emerge, and the BoC likely remains cautiously optimistic about the economy. Heavily trade-exposed sectors have continued to underperform, but November’s retail sales should reinforce consumer demand remains relatively resilient (in line with Statistics Canada’s advance estimate for a 1.2% monthly increase). Our cardholder spending tracker showed domestic purchases firming through the holiday shopping season.

We continue to expect the BoC will leave the overnight rate unchanged in 2026 with the next move more likely to be a hike, but we don’t expect until 2027.

{kind=link}