Greenland dominated global headlines today as geopolitical risk surged back into focus. What had previously looked like an unusual diplomatic dispute escalated sharply over the weekend, forcing markets, governments, and corporates to reassess transatlantic relations and the risk of renewed trade war.

The escalation followed a pledge by US President Donald Trump to impose 10% tariffs from February 1 on eight European countries unless the United States is allowed to buy Greenland. Trump warned those tariffs could rise further, turning the dispute into a direct trade and political confrontation rather than a rhetorical standoff.

Greenland’s leadership moved quickly to push back. Prime Minister Jens-Frederik Nielsen said on Monday that the Arctic island would not be pressured by tariff threats. His comments followed weekend protests in Nuuk, where he joined demonstrators opposing U.S. efforts to take control of the self-governing Danish territory.

European capitals responded with unusual unity. Germany and France delivered a coordinated rejection of what they described as economic blackmail. German Finance Minister Lars Klingbeil said Europe would not allow itself to be coerced, while French Finance Minister Roland Lescure called tariff pressure between allies “obviously unacceptable.”

The United Kingdom struck a slightly more cautious tone. Prime Minister Keir Starmer warned that tariffs should not be used against allies, stressing that a tariff war is in nobody’s interest and that his priority was to prevent escalation rather than retaliate immediately.

Markets are now turning to the sectoral fallout. Europe’s automotive industry is widely seen as one of the most exposed, given deeply globalized supply chains and heavy reliance on manufacturing links across North America. Luxury stocks, which were largely insulated during earlier phases of U.S.–EU trade tensions, may not be immune this time. While demand from wealthy consumers tends to be resilient, the risk that tariffs trigger a broader economic slowdown could eventually spill over.

Europe’s pharmaceutical sector faces potentially more direct exposure. Medicines and pharmaceutical products represent the EU’s largest export category to the U.S., leaving the industry vulnerable should tariffs be applied broadly rather than selectively. Oil and gas could also face indirect pressure. Even if not targeted directly, weaker global demand expectations, softer crude prices, and higher supply-chain costs could weigh on the sector as geopolitical uncertainty rises.

On the policy front, EU governments are preparing a range of retaliatory options. These include tariffs on up to EUR 93 billion of U.S. goods and possible use of the Anti-Coercion Instrument (ACI), a framework approved in 2023 that allows far-reaching countermeasures beyond simple tariffs. The ACI is widely viewed as a “nuclear option.” It allows the EU to impose investment restrictions and limit the export of services, including those provided by U.S. digital giants, significantly broadening Europe’s leverage should confrontation deepen.

Elsewhere, political uncertainty is not limited to Europe. In Japan, Prime Minister Sanae Takaichi finally announced she will call a snap election on February 8, dissolving parliament this week. She framed the vote as a referendum on her leadership, saying she is staking her political future on securing a fresh mandate.

The election is centered on an aggressive fiscal and security agenda. Takaichi pledged a two-year suspension of the 8% consumption tax on food, alongside increased public spending aimed at boosting household demand and job creation. At the same time, her administration plans to unveil a new national security strategy later this year, accelerating Japan’s military build-up and lifting defense spending to 2% of GDP, a decisive break from decades of restraint near 1%.

In currency markets, risk-sensitive positioning reflected the uneasy backdrop. The Swiss Franc led gains on the day, followed by Kiwi and Aussie. Dollar lagged at the bottom, followed by Yen and Loonie. Euro and Sterling held mid-table.

Canada CPI rises to 2.4% in December tax effects

Canada’s inflation picture turned mixed in December, with headline pressure firming but core measures easing. CPI accelerated to 2.4% yoy, up from 2.2% and above expectations of 2.2%. According to Statistics Canada, the pickup in headline inflation was largely technical rather than demand-driven.

The acceleration was driven by base effects linked to the temporary GST/HST tax break that began in mid-December 2024. As exempt goods and services dropped out of the year-over-year comparison, this mechanically pushed headline CPI higher. That effect was partly offset by a year-over-year decline in gasoline prices. Excluding gasoline, CPI rose 3.0% yoy, up from 2.6% yoy in November.

Nevertheless, core measures offered reassurance. CPI median slowed from 2.8% to 2.5%, CPI trimmed eased from 2.9% to 2.7%, both below expectations. CPI common held steady at 2.8%. matched expectations.

Eurozone CPI finalized at 1.9% in December, regional gaps persist

Final inflation data confirmed that price pressures in the Eurozone continued to ease into year-end. Eurostat reported headline CPI at 1.9% yoy in December, down from 2.1% in November. Core inflation slowed modestly to 2.3% yoy from 2.4%.

Despite the overall cooling, inflation remained heavily services-led. Services accounted for +1.54pp of headline inflation, far outweighing contributions from food, alcohol and tobacco (+0.49pp) and non-energy industrial goods (+0.09pp). Energy prices continued to offset inflation pressures, subtracting -0.18pp.

At the EU level, CPI was finalized at 2.3% yoy, also easing from 2.4% previously. Disinflation was broad-based, with inflation falling in 18 countries, though dispersion remains notable. Inflation was lowest in Cyprus (0.1%), France (0.7%) and Italy (1.2%). Romania (8.6%), Slovakia (4.1%) and Estonia (4.0%) posted elevated readings.

China GDP growth slows to 4.5% in Q4, pressure builds for fresh stimulus

China’s economy slowed at the end of 2025, reinforcing concerns that headline growth masks deepening domestic weakness. GDP expanded 4.5% yoy in Q4, down from 4.8% in Q3, in line with expectations. For the full year, growth reached 5.0%, matching the government’s target, but momentum clearly faded as the year closed.

Officials were quick to acknowledge the strain. Kang Yi, head of the National Bureau of Statistics, described 2025’s performance as “hard-won,” citing persistent challenges from strong supply and weak demand—a combination that continues to weigh on private confidence.

Full-year investment data underscored the depth of the slowdown. Fixed asset investment fell -3.8% ytd yoy, marking the first full-year contraction since the 1990s. The property sector remained the biggest drag, with property investment plunging -17.2% and new construction starts down -20.4%, extending a downturn now in its fourth year. Private investment dropped -6.4%, reflecting weak profit incentives amid overcapacity and cautious households.

December activity data showed mixed signals. Industrial production rose 5.2% yoy, improving from November and beating expectations of 5.0%. But retail sales slowed to 0.9% yoy, missing 1.2% forecasts and reinforcing the message that consumption remains the economy’s main weak spot.

The Q4 slowdown increases pressure on Beijing to step up stimulus in 2026 to meet a growth target of 4.5–5.0%. Without a more decisive pivot toward households and consumption, growth is likely to settle in the low- to mid-4% range, forcing policymakers to confront one of the most persistent domestic demand slumps in decades.

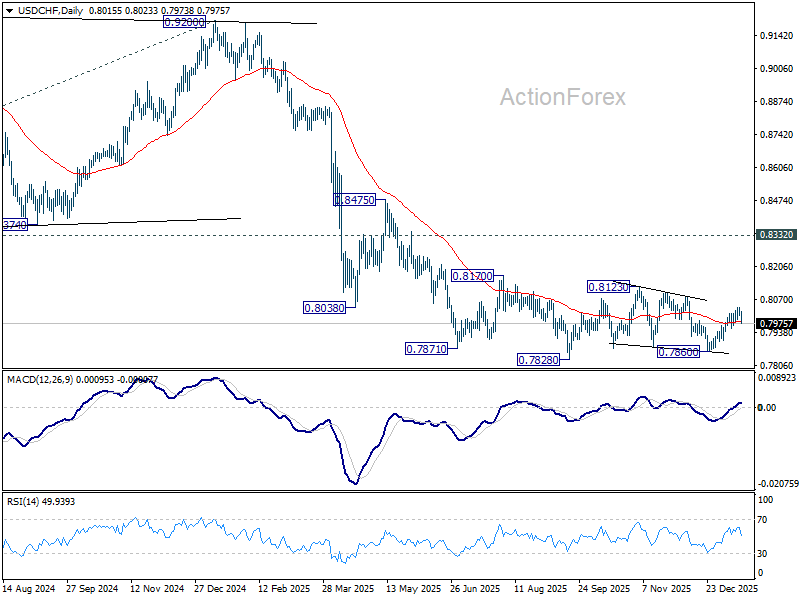

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8011; (P) 0.8026; (R1) 0.8045; More….

USD/CHF gyrates lower today but stays above 0.7954 support. Intraday bias remains neutral and another rise is in favor. On the upside, break of 0.8039 will resume the rally from 0.7860 for 0.8123 resistance However, break of 0.7954 support will argue that the rebound has completed, and turn bias back to the downside for 0.7860. Overall, corrective pattern from 0.7828 is extending.

In the bigger picture, price actions from 0.7828 are seen as a correction. Larger down trend from 1.0342 (2017 high) is still in progress. Break of 0.7828 will target 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8332 support turned resistance holds (2023 low).

{kind=link}