Market sentiment staged a sharp U-turn after signs that U.S.–European tensions over Greenland had moved toward resolution. The immediate risk of a transatlantic trade war has been averted for now, allowing investors to unwind defensive positioning built earlier in the week. The pivot lifted global equities, with Japan leading the charge in Asia, while European Indexes jumped at the open. U.S. equity futures also strengthened, building on yesterday’s firm Wall Street close.

Meanwhile, Gold and silver retreated from record highs, signaling a pullback in geopolitical hedging demand. In rates, U.S. 10-year yields slipped back below 4.25%, after briefly breaching 4.30% earlier in the week as term premium surged on political risk.

The catalyst came late Wednesday when US President Donald Trump said he had secured a “framework” deal on Greenland. Trump said the agreement would grant the U.S. and its European allies access to mineral rights and cooperation on the proposed Golden Dome missile defense initiative. Crucially, Trump added that punitive tariffs scheduled for February 1 on several European countries would no longer be imposed, directly removing the market’s most immediate escalation risk.

Speaking minutes after the social media post in an interview with CNBC, Trump described the Greenland arrangement as the “concept of a deal.” He offered few details, saying the proposal was complex and would be explained later, but reiterated that minerals and missile defense cooperation were central.

European reaction was cautiously constructive. Danish Prime Minister Mette Frederiksen welcomed the shift, saying Denmark was prepared to hold talks with Washington on the Golden Dome plan. She also said it was “good and natural” that Arctic security had been discussed between Trump and Mark Rutte at the World Economic Forum, reinforcing the view that the matter is being handled within an alliance framework.

In FX markets, Australian Dollar is leading the performance table for the day, alongside the New Zealand Dollar, both benefiting from the risk-on turn. Aussie is drawing additional support from strong jobs data, which has lifted expectations for an RBA rate hike in February. At the other end, Yen is the weakest performer, followed by Dollar. European majors are mixed in the middle, trading alongside Loonie.

Australia jobs surge 65.2k in December, unemployment drops to 4.1%

Australia’s labor market delivered a major upside surprise in December, reinforcing the picture of persistent tightness. Employment surged 65.2k, more than double expectations of 26.5k, driven primarily by a strong rise in full-time jobs (+54.8k), with part-time employment also increasing (+10.4k).

The strength fed directly into the unemployment rate, which fell from 4.3% to 4.1%, far below expectations of 4.4% and matching the joint-lowest level since December 2024. The participation rate held steady at 66.8%, while monthly hours worked rose 0.4% mom, signaling that labor demand remains robust rather than superficial.

According to Sean Crick, head of labour statistics at Australian Bureau of Statistics, the drop in unemployment was partly driven by more younger people entering the workforce. Even so, the scale of job creation highlights an economy that continues to absorb new entrants with ease.

RBA hike risks jump, AUD/USD heading to 7.2, AUD/JPY to 110

The Australian Dollar surged sharply as markets aggressively repriced interest-rate expectations following much stronger-than-expected jobs data. The rally reflects a swift reassessment of policy risk, with labor market resilience undermining the assumption that unemployment would drift higher and cool inflation pressures on its own.

The key shift is the absence of any rise in unemployment, which raises the risk that inflation could re-accelerate without additional policy restraint. In that context, markets are increasingly open to the idea that another rate hike may be required in the near term to keep price pressures contained.

That said, conviction remains conditional. The decisive input will be next week’s quarterly inflation report, which is likely to determine whether labor strength translates into a renewed inflation problem or simply reflects lagging labor-market adjustment.

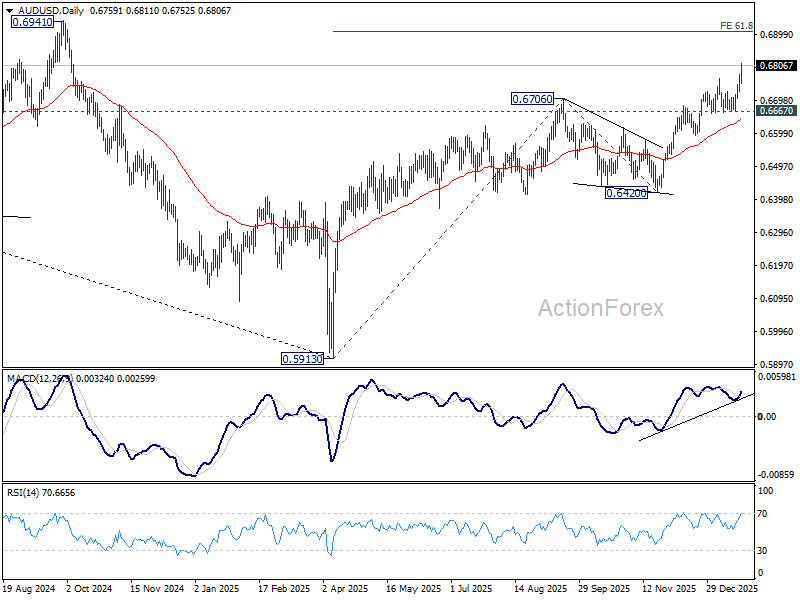

Technically, AUD/USD broke above 0.68 handle, with D MACD suggesting the move is accelerating. The next immediate target sits at 61.8% projection of 0.5913 to 0.6706 from 0.6420 at 0.6910. As long as 0.6667 support holds, near-term outlook remains bullish, even if consolidation emerges along the way.

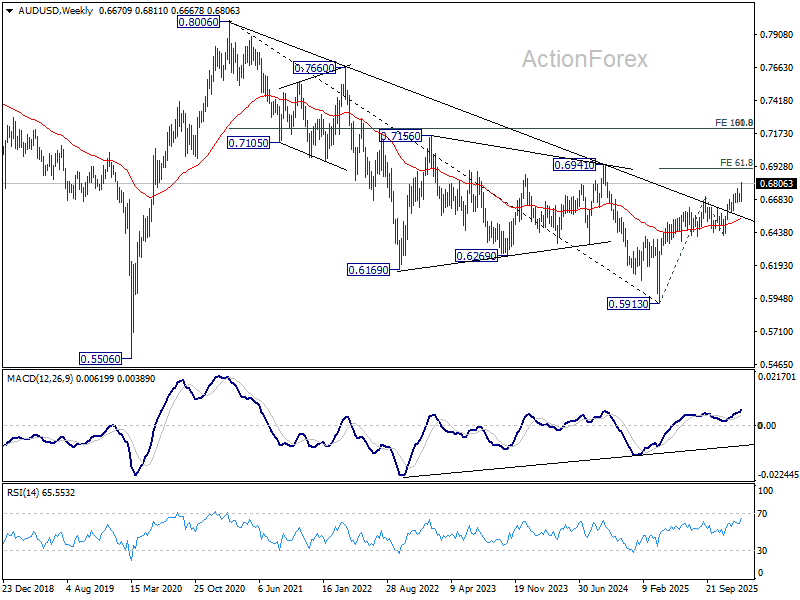

More importantly, the current advance strengthens the case that the rally from 0.5913 is reversing the entire downtrend from 2021 high at 0.8006. Firm break above 0.6941 would be a solid confirmation. Next target will be at around 0.72, which is 100% projection at 0.7213, which is close to 61.8% retracement of 0.8006 to 0.5913 at 0.7206.

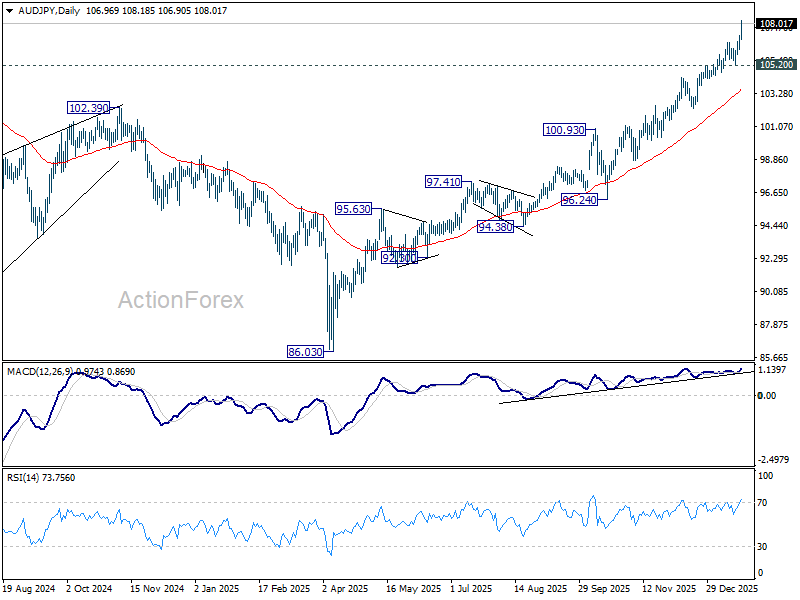

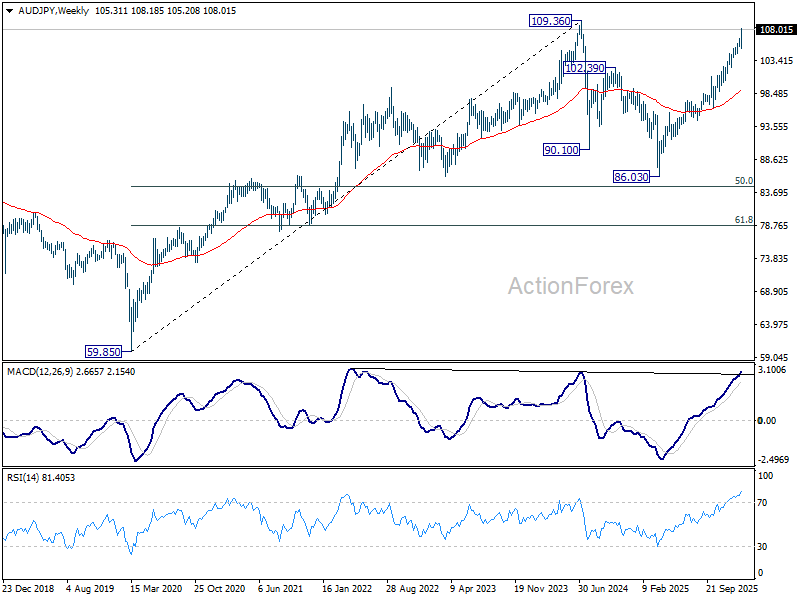

AUD/JPY is also surging, with the uptrend from 86.03 (2025 low) on track to retest 109.36, 2024 high. Given current momentum, a break above that level is likely to resume the long-term uptrend from 59.85 (2020 low). In any case, outlook will stay bullish as long as 105.20 support holds.

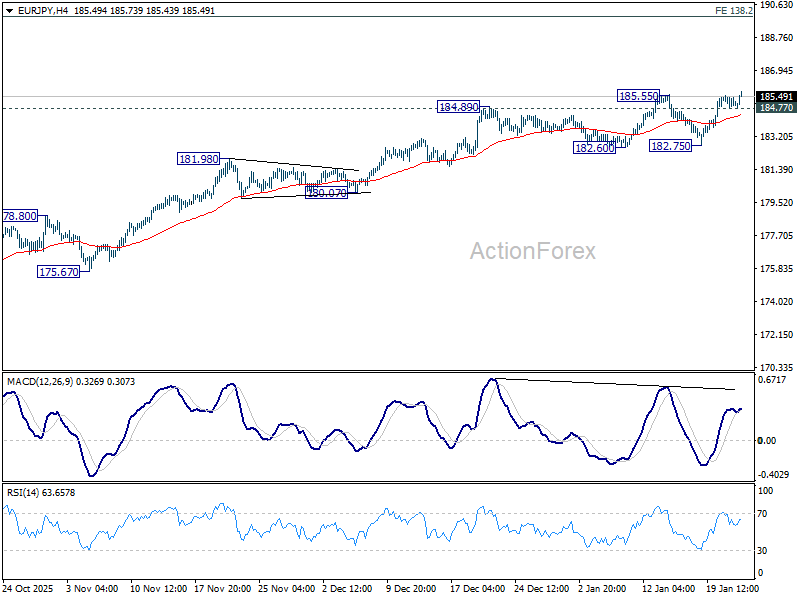

EUR/JPY Daily Outlook

Daily Pivots: (S1) 184.71; (P) 185.13; (R1) 185.43; More…

Intraday bias in EUR/JPY is back on the upside as breach of 185.55 suggests resumption of the long term up trend. Next target is 186.31 projection level. Firm break there will target 138.2% projection of 151.06 to 173.87 from 172.24 at 189.94. On the downside, below 184.77 will delay the bullish case and turn intraday bias neutral again. But further rally is expected as long as 182.75 support holds, in case of retreat.

In the bigger picture, up trend from 114.42 (2020 low) is in progress and should target 61.8% projection of 124.37 to 175.41 from 154.77 at 186.31. Considering bearish divergence condition in D MACD, upside could be capped by 186.31 on first attempt. Still, outlook will stay bullish as long as 55 W EMA (now at 172.58) holds, even in case of deep pullback. Sustained break of 186.31 will pave the way to 78.6% projection at 194.88 next.

{kind=link}