Dollar remains generally weak as markets move into the early US session, even though outright selling pressure has eased slightly. The slowdown, however, looks more like consolidation than recovery, with the greenback still exposed to fresh political and policy risks. That vulnerability follows an already bruising period marked by renewed transatlantic trade tensions and the latest tariff spat involving Canada. Markets are increasingly uneasy that US trade policy is becoming more erratic rather than more predictable.

A new source of concern has now emerged in Washington, where the risk of another US government shutdown is rising rapidly. Over the weekend, Senate Democrats vowed to oppose a funding package that includes financing for the Department of Homeland Security, following the fatal shooting of Alex Pretti by U.S. Immigration and Customs Enforcement agents in Minnesota. Democrats warned they would not support the USD 1.2 trillion funding bill for federal government operations, citing concerns over how immigration enforcement is being carried out. The stance sharply raises the stakes ahead of a looming funding deadline.

Until recently, markets viewed another shutdown as a manageable risk. Probabilities had hovered around 30% for much of January. That situation has shifted abruptly. On Polymarket, traders now price near 80% probability of a federal government shutdown by January 31, this coming Saturday. The threat is not new, but its immediacy has increased. Funding for a wide range of federal agencies is set to expire at the end of January, and failure to agree on a new package would trigger another partial shutdown, following a similar standoff late last year.

Against this backdrop, markets are struggling to find reasons to buy Dollar. Political dysfunction adds to an already fragile confidence backdrop shaped by trade frictions and capital flow concerns.

Elsewhere on the trade front, developments in other regions offered a contrasting signal. Reports suggest India is preparing to slash tariffs on EU car imports to 40% from as high as 110%, as New Delhi and Brussels close in on a free trade agreement that could be announced as early as Tuesday. Under the plan, Prime Minister Narendra Modi’s government would immediately lower duties on a limited number of high-end vehicles priced above EUR 15,000, with rates eventually falling to 10%. The move would ease access for European automakers.

In currency markets, Yen remains the strongest performer, underpinned by direct and blunt intervention warnings from Prime Minister Sanae Takaichi over the weekend. Aussie and Kiwi follow as the next strongest. Dollar sits at the bottom alongside its neighbor Loonie, with Sterling also lagging. Euro and Swiss Franc are holding middle ground.

In Europe, at the time of writing, FTSE is up 0.30%. DAX is up 0.25%. CAC is up 0.16%. UK 10-year yield is down -0.031 at 4.498. Germany 10-year yield is down -0.037 at 2.872. Earlier in Asia, Nikkei fell -1.79%. Hong Kong HSI rose 0.06%. China Shanghai SSE fell -0.09%. Singapore Strait Times fell -0.62%. Japan 10-year JGB yield fell -0.016 to 2.248.

US durable goods orders surge 5.3% mom in November, led by transport strength

US durable goods orders posted a strong upside surprise in November, rising 5.3% mom to USD 323.8B, well above expectations for a 3.1% increase.

Excluding transportation, orders rose a solid 0.5% mom to USD 204.4B, also beating forecasts of a 0.3% increase. Ex-defense orders jumped an even stronger 6.6% mom to USD 286.9B.

Transportation equipment was the clear driver, surging 17.9% mom to USD 119.3B. While volatility in this category is common, the underlying gains in core orders suggest business investment remained resilient.

German Ifo stalls at 87.6, as weak momentum carries into new year

Germany’s Ifo Institute Business Climate Index was unchanged at 87.6 in January, undershooting expectations for a modest improvement to 88.3. The stagnant headline reading reinforces the view that Germany’s economy is entering the new year without meaningful traction.

Beneath the surface, the details were mixed. Current Assessment Index edged slightly higher from 85.6 to 85.7, suggesting conditions have stabilized but remain weak. In contrast, Expectations Index slipped from 89.7 to 89.5, indicating that confidence about the months ahead has softened rather than improved.

Sector performance highlighted the uneven picture. Manufacturing showed a notable improvement, rising from -14.6 to -12.2, while trade and construction also edged higher to -21.1 and -14.2 respectively. Services, however, deteriorated from -2.1 to -2.6. Ifo summed up the survey bluntly, saying the German economy is “starting the new year with little momentum”.

Yuan hits 32-month high against Dollar, but dives against Euro

Chinese Yuan edged higher against Dollar today, pushing to a fresh 32-month high and drawing renewed attention to Beijing’s currency stance. The move comes amid growing speculation that Chinese authorities may be quietly signaling greater tolerance for a firmer Yuan.

However, a broader look at currency markets suggests Yuan’s gains are far more a function of broad-based Dollar weakness than a deliberate shift in Chinese policy. The greenback has been under sustained pressure globally, and USD/CNH has largely followed that trend rather than leading it. Indeed, when compared with other major currencies, Yuan’s appreciation has been notably measured and controlled. This relative restraint argues against the idea that Beijing is prepared to allow a free or rapid strengthening.

Still, markets have taken note of subtle policy signals. Late last week, the People’s Bank of China set Yuan’s daily fixing at 6.9929 per Dollar, the first time the midpoint has been set stronger than the closely watched 7.00 level since May 2023. It also marked the largest one-day strengthening since August. China went a step further today. Before markets opened, the PBOC fixed the midpoint at 6.9843 per dollar, the strongest level since May 17, 2023. The move reinforced the perception that authorities are comfortable with some near-term Yuan strength, particularly against a weakening dollar.

That said, analysts remain wary of extrapolating too much. Expectations are building that authorities could push back if appreciation pressures intensify, using policy tools to smooth gains and preserve competitiveness. The prevailing view remains that any Yuan strength will be tightly managed rather than left to market forces.

Technically, cross-rates echo that narrative. In EUR/CNH, the strong rally over the past two days and a clear break above the 55 Day EMA at 8.2025 suggest the corrective pullback from 8.4638 has completed at 8.0654, 38.2% retracement of 7.4886 (2025 low) to 8.4638 (2025 high) at 8.0913. Near-term focus is now on 8.3004, with a firm break there opening the door for a retest of 8.4638 high.

Meanwhile, USD/CNH continues to drift lower, but downside momentum is clearly waning. Daily MACD shows fading bearish pressure, while the pair has struggled to extend beyond the falling channel floor and 100% projection of 7.4287 to 7.1608 from 7.2224 at 6.9545.. A rebound from current levels, followed by break above 6.9956, would confirm short-term bottoming and reinforce the view that Yuan strength remains controlled rather than open-ended.

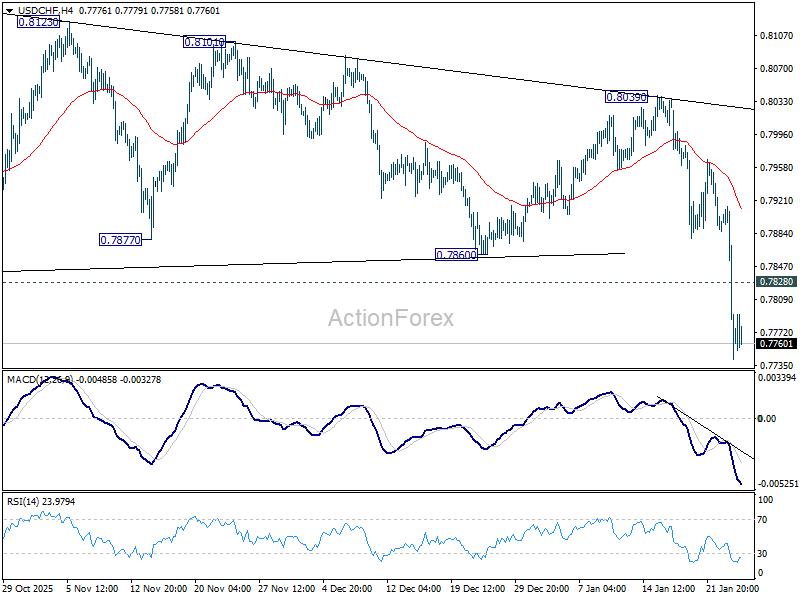

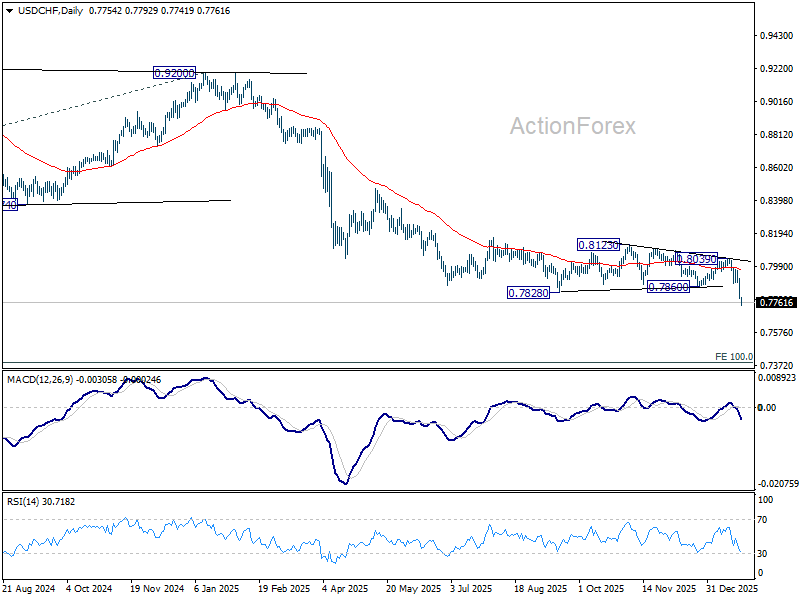

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.7754; (P) 0.7836; (R1) 0.7884; More….

Intraday bias in USD/CHF remains on the downside for the moment. Current fall is part of the larger down trend and should target 0.7382 projection level. On the upside, above 0.7828 minor resistance will turn intraday bias neutral first. But recovery should be limited well below 0.8039 resistance to bring another fall.

In the bigger picture, larger down trend from 1.0342 (2017 high) is still in progress and resuming. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.8184) holds.

{kind=link}