Yen came under renewed pressure today after comments over the weekend from Japanese Prime Minister Sanae Takaichi suggested a softer stance on currency weakness. The shift in tone has been interpreted as reducing the near-term threat of official intervention, reopening the door for Yen sellers.

In a campaign speech on Saturday, Takaichi highlighted the benefits of a weaker Yen for Japan’s export sector. “People say the weak Yen is bad right now, but for export industries, it’s a major opportunity,” Takaichi said, adding that the currency has helped cushion the impact of U.S. tariffs on sectors ranging from food to automobiles. Her remarks were seen as implicitly tolerant of Yen depreciation.

However, the rhetoric was partly walked back on Sunday. In a post on X, Takaichi said she did not favor any specific Yen direction and stressed that her intention had been misinterpreted. She added that, as prime minister, she would refrain from commenting directly on currency levels. “I did not say which is better or worse — a strong Yen or a weak Yen,” she wrote. She also emphasized the need to build an economic structure resilient to exchange-rate fluctuations by boosting domestic investment.

Despite the clarification, markets have focused on the reduced immediacy of intervention risk. Still, traders remain wary that official warnings could quickly return to headlines, especially if volatility accelerates.

Besides, with a snap lower house election scheduled for February 8, traders are likely to remain cautious. According to a survey by the Asahi newspaper, Takaichi’s party is on track for a landslide victory. A decisive LDP majority could embolden expectations of expansionary fiscal policy, potentially pushing stocks higher and lifting USD/JPY back toward the 160 area. In contrast, a coalition outcome could cap the pair closer to 155.00, depending on the makeup of partners.

Beyond Japan, Asian markets are also digesting the nomination of former Fed Governor Kevin Warsh by Donald Trump as the next Fed chair. Stocks have generally softened on expectations of a less dovish Fed under Warsh. Risk sentiment elsewhere remains fragile, with Gold, Silver, and Bitcoin all trading heavy. Given Warsh’s strong data focus, this week’s ISM surveys and U.S. non-farm payrolls are likely to carry extra weight.

In FX, Euro is leading gains on the day so far, followed by Swiss Franc and Dollar. Aussie is the weakest, trailed by Loonie and Kiwi. Sterling and Yen are trading mid-pack.

In Asia, at the time of writing, Nikkei is down -0.69%. Hong Kong HSI is down -2.40%. China Shanghai SSE is down -1.32%. Singapore Strait Times is down -0.34%. Japan 10-year JGB yield is down -0.001 at 2.250.

Japan PMI manufacturing finalized at 51.5, growth returns, inflation a risk

Japan’s manufacturing sector returned to expansion in January, with PMI Manufacturing finalized at 51.5. This marks the first improvement in operating conditions since mid-2025 and represents the strongest rate of growth since August 2022, offering early evidence of a cyclical recovery taking hold.

The details were encouraging. S&P Global Market Intelligence noted that output and new orders recorded their sharpest increases in almost four years, while export demand rose for the first time since 2022. Employment growth also accelerated to its fastest pace since September 2022, suggesting the sector is “gearing up for further increases in output in the months ahead.”

That said, cost pressures are resurfacing as a potential constraint. Input price inflation climbed to a near one-year high, driven in part by the weaker yen, and firms passed some of those costs on to customers. Whether these price pressures intensify will be key in assessing how durable the recovery proves to be.

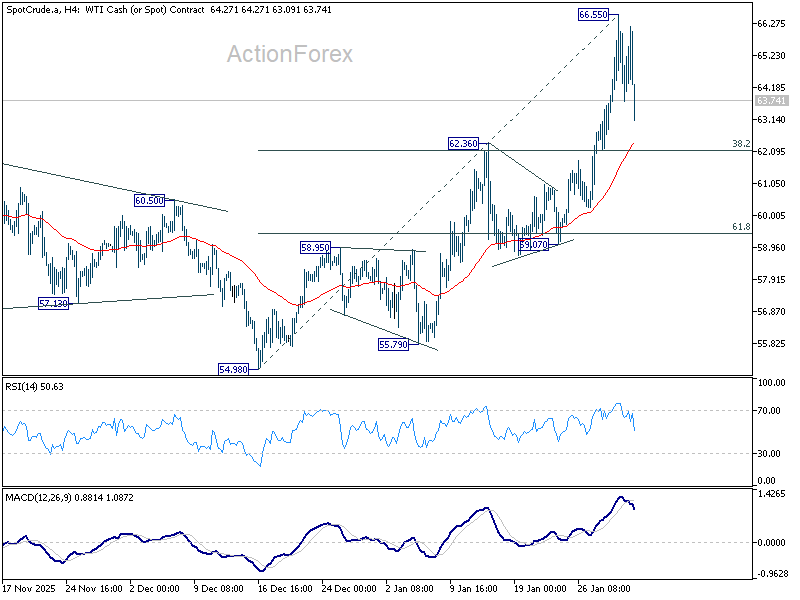

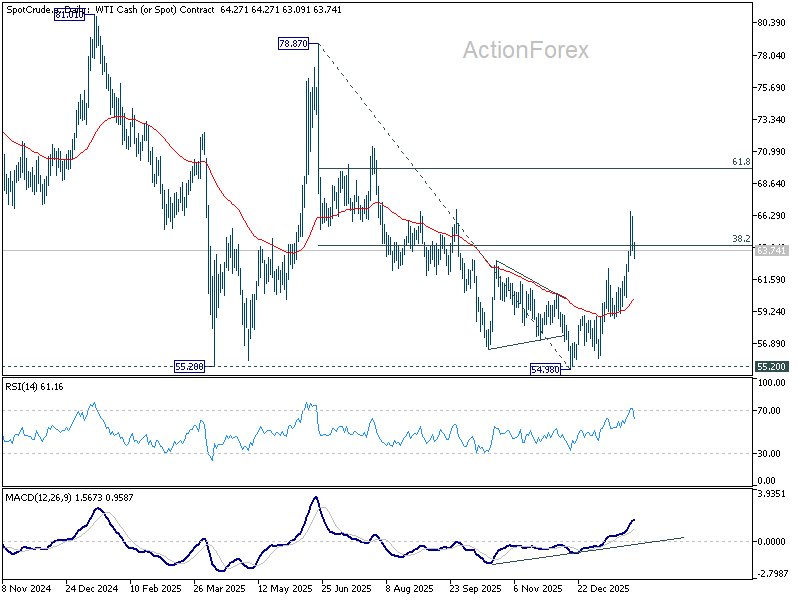

WTI oil rally pauses on OPEC+ hold, bullish trend reversal still intact for 70 later

Oil prices edged lower today after OPEC+ agreed to keep output unchanged for March. Sunday’s brief meeting reaffirmed earlier decisions to freeze planned output increases through the first quarter of 2026.

Those increases—amounting to roughly 2.9 million barrels per day—were scheduled to be phased in from April through December 2025 by eight producers, including Saudi Arabia and Russia, representing about 3% of global demand. With seasonal consumption typically weaker early in the year, the group has opted to stay patient.

What stood out was not what OPEC+ said, but what it avoided saying. The statement offered no clues on production plans beyond March, effectively keeping all options open. With U.S.–Iran tensions rising and crude prices having pushed to six-month highs last week on fears of potential military escalation, that strategic ambiguity is likely intentional.

Against that backdrop, today’s pullback in WTI looks more corrective than trend-changing. Technically, the dip helps confirm a short-term top at 66.55. WTI now appears to be consolidating the five-wave rally from the 54.98 low. While deeper retracement cannot be ruled out in the near term, downside should be limited. Strong support is expected near the 38.2% retracement of 54.98 to 66.55 at 62.13, where buying interest is likely to re-emerge.

Beyond the short-term noise, the broader technical picture has improved materially. The earlier break above 38.2% retracement of 78.87 to 54.98 at 64.10 argues that the entire sell-off from last year’s highs has likely been completed. In that context, the rise from 54.98 is tentatively viewed as the third leg of the larger pattern that began at 55.20. As long as the 55 D EMA (now at 60.14) holds, the medium-term bias remains to the upside for 61.8% retracement at 69.74 and potentially beyond at a later stage.

Unless geopolitical risks—particularly around Iran—ease decisively, any near-term dips may continue to attract buyers rather than signal a reversal.

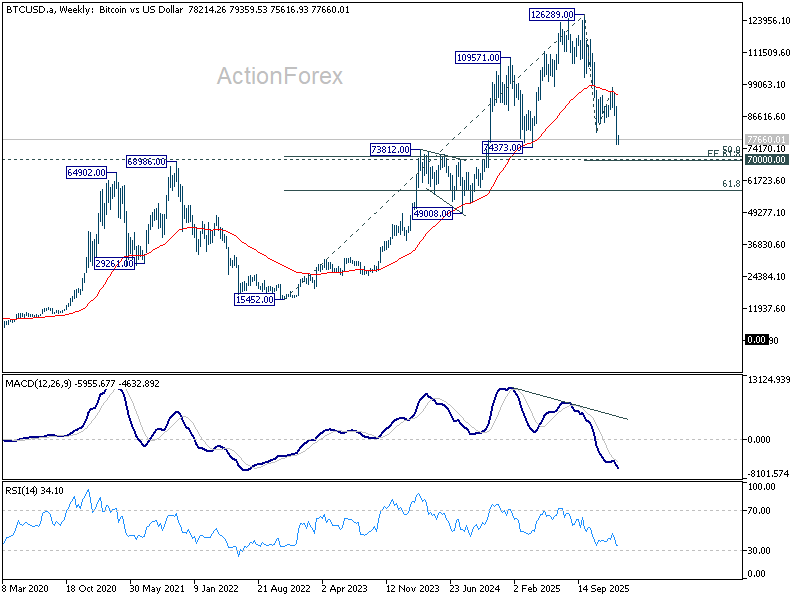

Bitcoin breaks down, 70k becomes critical test for broader market sentiment

Bitcoin remains under heavy pressure after plunging late last week, with prices still struggling to regain 80,000. The selloff closely follows last week’s crash in precious metals, suggesting a shared catalyst of US President Donald Trump’s decision to nominate Kevin Warsh as the next Fed chair.

For now, broader risk assets have so far absorbed the shock. Equity indexes and volatility measures remain relatively calm, indicating that investors are not yet pricing in a wider risk-off regime. That calm, however, may prove misleading. Given Bitcoin’s persistent correlation with tech stocks, sustained weakness in crypto could serve as an early warning signal that underlying sentiment is deteriorating beneath the surface, even as traditional risk gauges remain resilient.

Technically, the damage is already done. The break below 80,492 confirms that Bitcoin’s broader downtrend from 126,289 record high has resumed. As long as 84,380 support turned resistance holds, deeper decline should be seen to 61.8% projection of 126,289 to 80,492 from 97,922 at 69,619, which is slightly below 70k psychological level.

This target sits just beneath the key 70,000 psychological level, making that zone a critical battleground between medium-term bulls and bears. It coincides with 50% retracement of the entire 2022–2025 advance. A strong rebound from that zone would keep the post-peak price action in a medium-term sideway consolidation. However, decisive break would open the door to deeper unwind toward 49,008.

Should that bearish scenario unfolds, close monitoring of NASDAQ will be essential, as confirmation from equities would point to broader liquidation across risk markets rather than a crypto-only reset.

Week ahead: RBA, BoE, ECB and US NFP in focus

A dense macro calendar awaits markets, with three central bank meetings and critical US labor data set to shape near-term policy expectations.

The most immediate event risk comes from the RBA, where a rate hike has become the dominant expectation. The RBA is widely expected to raise the cash rate by 25bps to 3.85%, undoing part of its prior easing. The case for action has strengthened as inflation has crept back above the Bank’s 2–3% target band. Particular attention is on trimmed mean inflation, which rose to 3.3%, a level that will be uncomfortable for policymakers. Combined with unemployment holding at a low 4.1%, the RBA has room to tighten without immediate concern about growth or labor market damage.

That said, a hike this week is unlikely to mark the start of an extended tightening cycle. There is little evidence of consensus within the RBA that rates need to be pushed decisively above 4% at this stage. Instead, a return to a wait-and-see stance is likely after the meeting. The Bank may communicate a willingness to follow up if inflation fails to cool, but without committing to a sequence of further moves.

In the UK, the BoE is expected to hold Bank Rate at 3.75%. While further easing remains the central scenario, the timing is increasingly contentious. A recent Reuters poll showed economists split, with only 55% expecting a cut by end-March, down sharply from December when nearly three-quarters anticipated easing this quarter. Beyond Q1, there is no clear majority view on the rate path.

One cut later this year looks relatively assured, but whether the BoE delivers a second move remains highly uncertain. As ever, the MPC vote split will be scrutinized closely for signals on internal divisions.

The ECB meeting is likely to pass quietly. A hold at 2.00% is fully priced, with policymakers expected to stress comfort with current settings barring material new developments. The ECB is also likely to dismiss market talk of a potential hike as premature.

In the US, focus turns to non-farm payrolls and ISM manufacturing and services, especially in light of Kevin Warsh’s nomination by Donald Trump to chair the Fed. Warsh’s data-driven approach puts added weight on labor market signals. For now, even with lingering tariff risks, the Fed is likely to view price effects as transitory. The key question is whether the “no hiring, no firing” dynamic evolves into a deeper labor market deterioration that would force earlier rate cuts. Absent that, policy is likely to remain on hold, with markets tentatively leaning toward a June cut, but with little conviction.

Canadian and New Zealand jobs data, alongside Eurozone CPI flash, round out a week dense with economic data and events.

Here are some highlights for the week:

- Monday: Swiss retail sales, PMI manufacturing; Eurozone PMI manufacturing final; UK PMI manufacturing final; US ISM manufacturing.

- Tuesday: RBA rate decision.

- Wednesday: New Zealand employment; Eurozone PMI services final, CPI flash, PPI; US ISM services.

- Thursday: Australia trade balance; Germany factory orders; France industrial production; Eurozone retail sales; BoE rate decision; ECB rate decision; US jobless claims.

- Friday: Japan household spending, Germany industrial production, trade balance; Swiss foreign currency reserves, unemployment rate; Canada employment; US non-farm payroll, U of Michigan consumer sentiment.

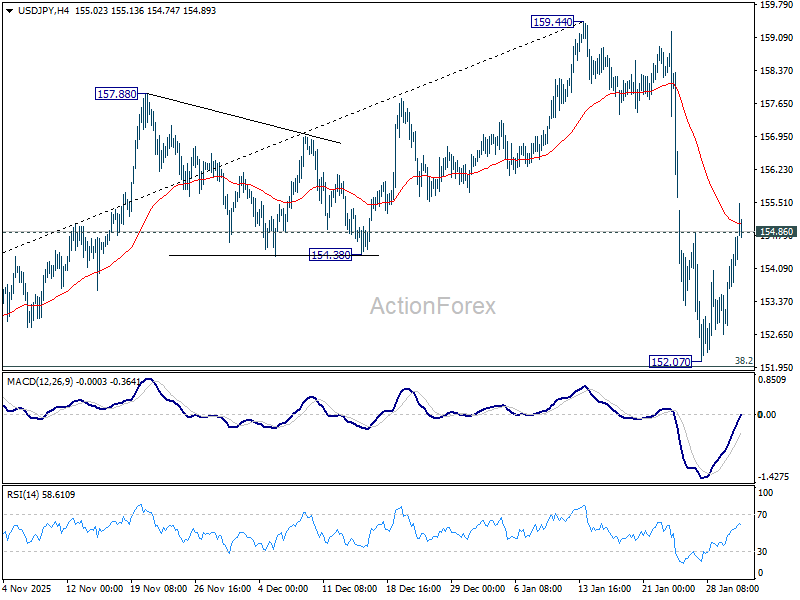

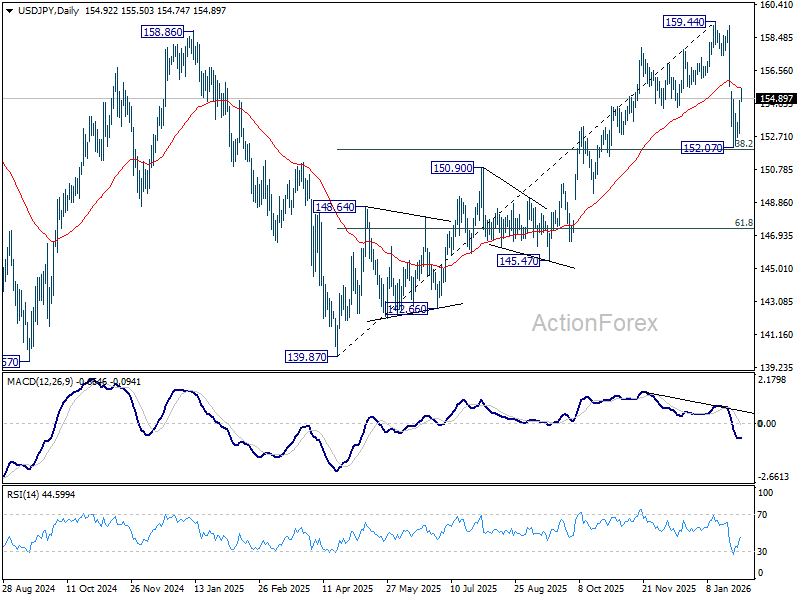

USD/JPY Daily Outlook

Daily Pivots: (S1) 153.49; (P) 154.15; (R1) 155.42; More…

USD/JPY’s break of 154.86 resistance suggests that a short term bottom was formed at 152.07, ahead of 38.2% retracement of 139.87 to 159.44 at 151.96. Corrective pattern from 159.44 should be in the second leg. Intraday bias is back on the upside, and sustained trading above 55 D EMA (now at 155.52) will pave the way back to retest 159.44. However, decisive break of 151.96 will argue that it is reversing whole rise from 139.87. Deeper decline would then be seen to 61.8% retracement at 147.34.

In the bigger picture, outlook is unchanged that corrective pattern from 161.94 (2024 high) should have completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94. This will remain the favored case as long as 55 W EMA (now at 151.59) holds. However, sustained break of 55 W EMA will argue that the pattern from 161.94 is extending with another falling leg.

{kind=link}