Sterling leads the currency markets today, buoyed by stronger-than-expected UK PMI and retail sales data that reinforced the narrative of economic resilience. The rebound in business activity helped offset lingering concerns generated earlier in the week by softer labor and inflation figures.

For the BoE this means policy easing can proceed cautiously. A March rate cut remains likely. Yet, a measured pace of one 25bps cut per quarter still appears plausible. There is little evidence that the economy is deteriorating sharply enough to warrant aggressive action. Instead, the BoE may continue to recalibrate policy cautiously as disinflation progresses.

In the US, Dollar remains generally firm, though upward momentum is beginning to lose steam. Earlier gains were fueled by hawkish FOMC minutes and strong jobless claims data, reinforcing expectations that rate cuts are not imminent. The Q4 GDP slowdown to 1.4% was disappointing, but much of the weakness stemmed from the temporary government shutdown and a drop in exports. Underlying domestic demand remained more resilient than the headline suggests.

Personal spending continued to expand steadily, and inflation readings—both headline and core PCE—picked up in December. That combination limits any urgency for the Fed to bring forward rate cuts. As a result, market pricing remains anchored around a likely mid-year easing move rather than an imminent shift. There is little additional pressure on the Fed to accelerate its timeline.

For the week so far, Dollar remains the strongest performer, followed by Aussie and Loonie. Yen sits at the bottom of the table, trailed by Kiwi and Sterling, despite today’s rebound. Euro and Swiss Franc are positioned in the middle.

In Europe, at the time of writing, FTSE is up 0.43%. DAX is up 0.21%. CAC is up 0.71%. UK 10-year yield is down -0.008 at 4.362. Germany 10-year yield is down -0.009 at 2.738. Earlier in Asia, Nikkei fell -1.12%. Hong Kong HSI fell -1.1%. China was still on holiday. Singapore Strait Times rose 0.32%. Japan 10-year JGB yield fell -0.032 to 2.109.

US income and spending rise in December, PCE inflation picks up

US personal income rose by USD 86.2B, or 0.3% mom in December, supported mainly by gains in compensation and higher government social benefits. Personal spending increased by USD 91.0B, or 0.4% mom. The rise was driven by a solid rebound in services outlays (+USD 98.5B), which more than offset a decline in goods spending (-USD 7.5B).

Inflation pressures, however, picked up at the margin. PCE price index rose 0.4% mom, with core PCE also up 0.4% mom. On an annual basis, headline PCE accelerated to 2.9% yoy from 2.8%, well above expectations, while core PCE ticked up from 2.8% yoy to 3.0%. Both matched expectations.

US Q4 GDP growth slows sharply to 1.4% annualized, shutdown and exports weigh

US economic growth decelerated markedly in the Q4 2025, with real GDP expanding at an annualized pace of 1.4%, well below expectations of 2.9%. The slowdown is significant compared with the 4.4% surge recorded in Q3.

Growth was supported by resilient consumer spending, particularly in services such as healthcare, alongside continued business investment. However, these gains were largely offset by sharp declines in federal government spending following the 43-day shutdown, as well as weaker exports.

On inflation, the PCE price index rose 2.9% in Q4, while core PCE increased 2.7%.

Canada retail sales slip -0.4% mom in December, January rebound expected

Canada’s retail sales declined -0.4% mom in December to CAD 70.0B, slightly better than the -0.5% drop expected. The pullback marks a modest softening in year-end consumer activity, though the headline miss was not as severe as feared.

Core retail sales, which exclude gasoline and motor vehicles, fell -0.3% mom, weighed heavily by a sharp -4.0% contraction in building materials and garden equipment. However, excluding motor vehicle and parts dealers alone, sales edged up 0.1%, suggesting underlying consumer demand was not uniformly weak.

Nevertheless, Statistics Canada’s advance estimate for January points to a strong rebound, with sales projected to rise 1.5% mom.

Eurozone manufacturing returns to growth, PMI hits 44-month high

Eurozone PMI Manufacturing rose from 49.5 to 50.8 in February, moving back into expansion territory and reaching its highest level in 44 months. PMI Services edged up from 51.6 to 51.8. PMI Composite climbed from 51.3 to 51.9.

According to Hamburg Commercial Bank’s Cyrus de la Rubia, this could mark a potential “turning point” for the manufacturing sector. Manufacturing has been a persistent drag since mid-2022, and although the index briefly crossed 50 last August, this time the foundation appears stronger. New business improved across both manufacturing and services, pointing to continued expansion in coming months.

Germany is playing a central role in the improved outlook. Higher public spending on infrastructure and defence, along with firmer external demand, are supporting industrial activity. However, de la Rubia cautioned that overall growth momentum has softened slightly compared with the fourth quarter, suggesting expansion remains moderate rather than accelerating.

Price pressures in services — closely watched by ECB — “relaxed a bit”. Nevertheless, service inflation remains elevated enough to discourage a shift in policy stance. With activity stable and inflation not yet fully subdued, ECB appears inclined to keep rates steady for now.

UK PMI composite rises to 53.9, consistent with over 0.3% Q1 GDP growth

UK business activity continued to expand in February, with PMI Manufacturing rising from 51.8 to 52.0, marking an 18-month high. PMI Services edged slightly lower from 54.0 to 53.9. PMI Composite improved from 53.7 to 53.9, reaching its strongest level in 22 months.

According to S&P Global’s Chris Williamson, the data point to an “encouraging start” to the year. Output growth across both manufacturing and services has accelerated in January and February. Current readings are consistent with GDP rising just over 0.3% in the first quarter if momentum carries through March.

For the BoE, while firmer activity will be welcomed, relatively modest price pressures and ongoing labor market weakness may keep pressure on BoE to consider further easing.

UK retail sales surge 1.8% in January, strongest since May 2024

UK retail sales volumes jumped 1.8% mom in January, far exceeding expectations of 0.2% and marking the largest monthly increase since May 2024. The rebound suggests consumers began the year on firmer footing despite broader concerns over slowing growth.

On an annual basis, sales volumes rose 4.5% yoy, pointing to solid underlying demand. Over the three months to January, volumes edged up 0.1% compared with the prior three-month period and were 2.6% higher than a year earlier, indicating steady momentum rather than a one-off spike.

The data offer a counterbalance to recent signs of labor market softening and cooling inflation. While markets continue to price a March rate cut from BoE, resilient consumer spending may temper expectations for an aggressive easing cycle, particularly if inflation remains sticky in services.

Japan’s CPI slows to 1.5% in January, core measures ease further

Japan’s headline CPI slowed to 1.5% yoy in January from 2.1%, falling below the BoJ’s 2% target for the first time in 45 months. Core CPI (excluding fresh food) declined to 2.0% from 2.4%, while core-core inflation eased to 2.6% from 2.9%, signaling broader moderation in underlying price pressures.

The slowdown was largely driven by energy, where costs dropped -5.2% yoy after a -3.1% fall in December. Goods inflation cooled sharply from 2.7% to 1.6%. In contrast, services inflation remained steady at 1.4%, suggesting domestic wage-driven price gains have yet to accelerate meaningfully.

Food inflation remains elevated but is gradually cooling. Prices excluding fresh items rose 6.2% yoy, down from 6.7%. Rice inflation slowed for an eighth consecutive month to 27.9%.

Japan PMI composite jumps to 53.8, export demand surges

Japan’s private sector gathered further momentum in February, with PMI Manufacturing rising from 51.5 to 52.8 and PMI Services edging up to 53.8. PMI Composite climbed from 53.1 to 53.8, marking the strongest expansion since May 2023 and signaling a more broad-based recovery.

According to S&P Global’s Annabel Fiddes, the upturn was supported by firmer demand both domestically and overseas. Total new orders expanded at the quickest pace since May 2023, while manufacturers recorded the strongest increase in export work in eight years.

Stronger sales pushed capacity utilization higher, with backlogs rising at a record pace. Firms responded by increasing hiring, while improved demand allowed businesses to regain some pricing power despite persistent cost pressures. Business confidence also strengthened, supported by new product launches, technology demand and optimism following Prime Minister Sanae Takaichi’s landslide election victory.

Australia PMI composite dives to 52.0 in February, cost pressures reaccelerate

Australia’s February flash PMIs signaled a slowdown in private sector momentum. PMI Manufacturing slipped from 52.3 to 51.5, while PMI Services dropped sharply from 56.3 to 52.2. As a result, PMI Composite fell from 55.7 to 52.0, indicating growth continued but at a much more modest pace.

According to S&P Global’s Eleanor Dennison, the private sector was unable to sustain the strong start to the year. Both manufacturing and services recorded softer expansions in output and new orders, with the services sector experiencing the more pronounced pullback.

However, inflationary pressures remain evident. Firms reported elevated wage burdens and higher supplier costs, pushing both input and output price inflation to five-month highs. Despite softer new business growth, job creation accelerated to an 11-month high, underscoring labor market tightness.

RBNZ’s Breman confident inflation will return to target, policy not on preset path

RBNZ Governor Anna Breman said in speech that the central bank remains confident inflation will return to target despite its current 3.1% reading. She expects inflation to move back inside the 1–3% band in the first quarter and ease toward the 2% midpoint over the 12 months. That formed a key basis for the decision to keep the OCR unchanged at 2.25% this week.

Breman stressed that policymakers needed to determine whether the recent uptick in inflation signaled broader price pressures or merely a “temporary bump”. She pointed to global factors lifting tradables prices, while non-tradables inflation continues to decline, albeit slowly.

The economy expanded in the September quarter and indicators suggest recovery is continuing into early 2026. With unemployment still elevated and wage growth subdued, the RBNZ sees room for recovery without reigniting inflation.

At the same time, she reiterated that monetary policy is “not on a preset course”.

NZ trade deficit at NZD -519m as China flows diverge

New Zealand’s goods exports rose 2.6% yoy in January to NZD 6.2B, up NZD 157m from a year earlier. Goods imports increased 1.9% yoy to NZD 6.7B, up NZD 126m. The result was a monthly trade deficit of NZD -519m.

By destination, export performance was mixed. Shipments to China, New Zealand’s largest trading partner, fell NZD -118m (-7.0%) yoy. In contrast, exports to Australia jumped NZD 134M (+20%), while flows to the EU (+16%) and Japan (+11%) also posted solid gains. Exports to the US were broadly flat.

On the import side, China led the increase, with imports surging NZD 346m (+24%) yoy. South Korea also recorded a strong rise (+36%), while imports from the EU edged higher. Meanwhile, purchases from the US (-17%) and Australia (-8.1%) declined.

The data suggest stable overall trade volumes but highlight shifting bilateral flows, particularly with China, which may have implications for growth in coming months.

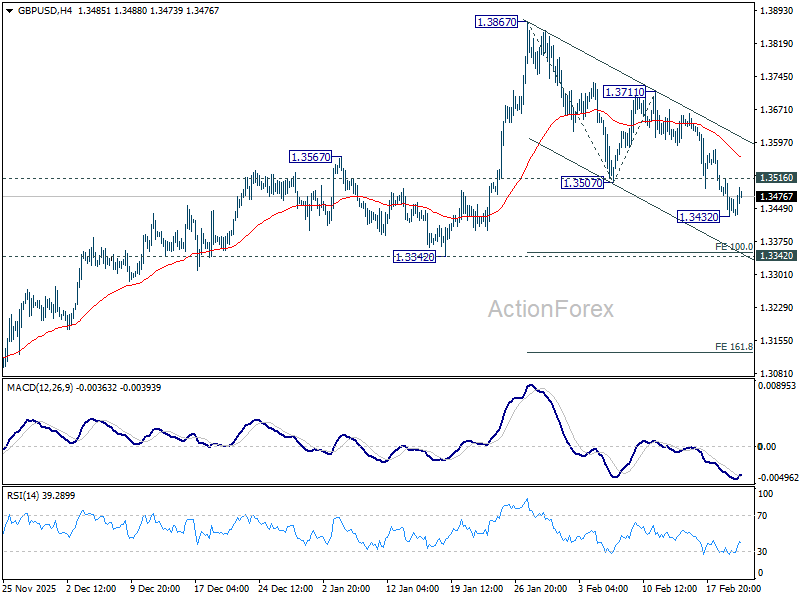

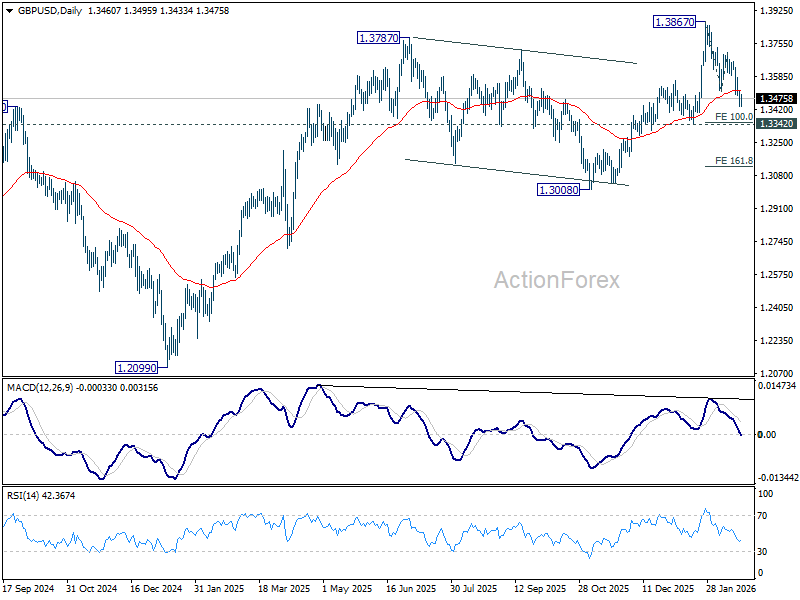

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3428; (P) 1.3473; (R1) 1.3511; More…

A temporary low is in place at 1.3432 in GBP/USD with 4H MACD crossed above signal line. Intraday bias is turned neutral for consolidations. But risk will stay on the downside as long as 1.3711 resistance holds. Below 1.3432 will target 1.3342 support next. Current development suggests that the decline is at least correcting the uptrend from 1.2099. Break of 1.3342 support will solidify this case, and target 161.8% projection of 1.3867 to 1.3507 from 1.3711 at 1.3129.

In the bigger picture, rise from 1.0351 (2022 low) still in progress and should target 1.4284 key resistance (2021 high). Decisive break there will add to the case of long term bullish trend reversal. For now, outlook will stay bullish as long as 1.3008 support holds, even in case of deep pullback.

{kind=link}