- Investors reduce Fed cut bets ahead of NFP and ISM PMI data.

- Eurozone CPI and ECB minutes in focus amid strong euro concerns.

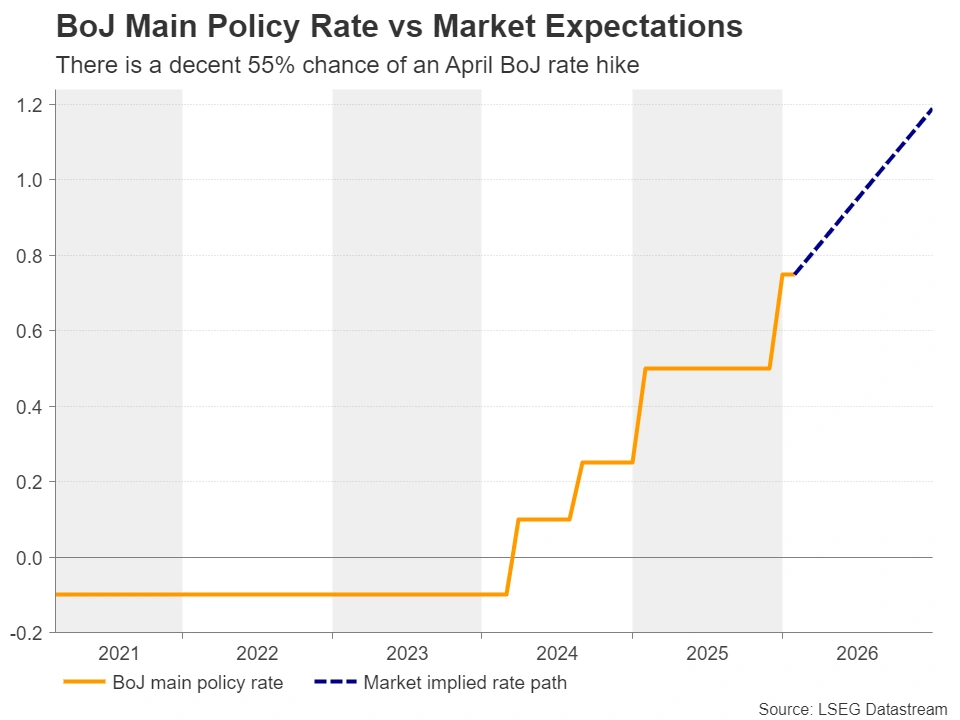

- Will Japan’s employment numbers allow the BoJ to hike rates in April?

- Australian GDP and Switzerland’s inflation numbers also in focus.

Dollar fragile even as investors scale back Fed cut bets

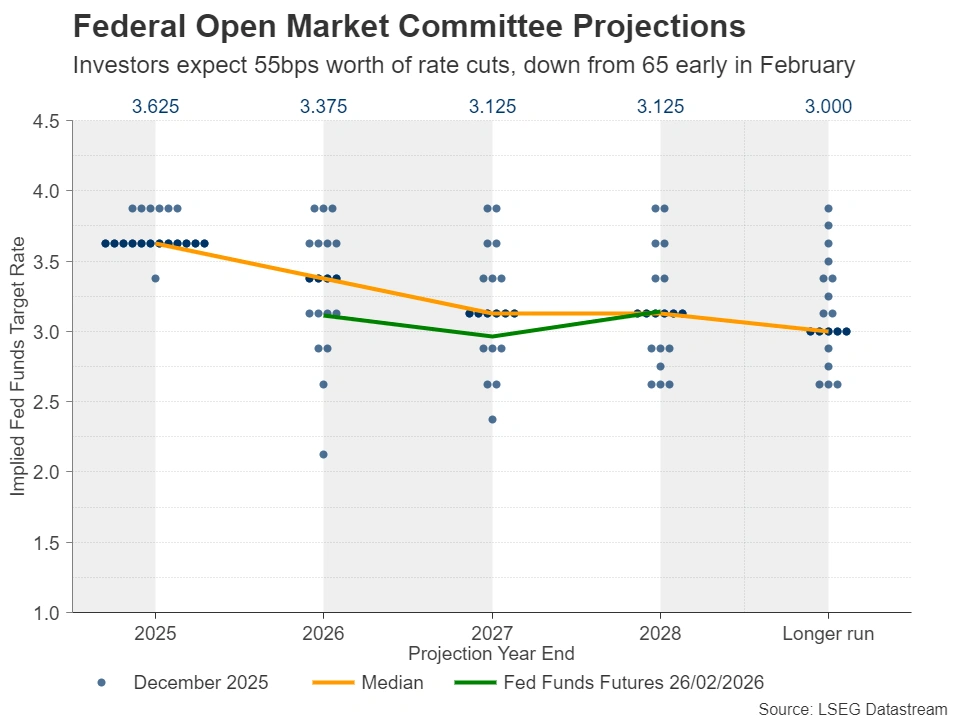

The US dollar remained on the back foot against most of its major counterparts this week, gaining notable ground only against the Japanese yen. Strangely, this has been the case even after investors scaled back their rate cut bets to price in 55bps worth of rate cuts.

In early February, they were expecting around 65bps, which translates into two quarter-point reductions and a more-than-50% chance of a third. However, following the blockbuster NFP report for January, some Fed officials showed little willingness to further loosen monetary policy immediately. Even the minutes of the latest FOMC decision, which took place before the jobs data revealed a divided Committee, with several members open to rate hikes if inflation remains elevated and others leaning towards more rate cuts should inflation further cool down.

Maybe the dollar stayed on the back foot as, even with 55bps worth of expected rate cuts, the Fed remains the most dovish major central bank, keeping the divergence with some others, like the RBA, very wide. The greenback may have also been sold following the latest saga between US President Trump and the Supreme Court. After the court ruled some of Trump’s tariffs as illegal, the US President announced a 15% duty on global goods, using a law that does not fall under the court’s decision.

NFP and ISM PMI data take center stage

With all that in mind, next week, dollar traders are likely to lock their gaze on the US employment report for February, but before the NFP release, the ISM manufacturing and services PMIs on Monday and Wednesday may also attract special attention. The Atlanta Fed GDPNow model is pointing to a rebound in economic growth from 1.4% in Q4 to 3.1% in Q1, and should this be confirmed by the ISM numbers, the dollar is likely to strengthen as investors become more convinced that the Fed does not need to rush into further lowering borrowing costs.

However, given the Fed’s dual mandate of full employment and stable inflation at 2%, investors may put some emphasis on the employment and prices subindices of the ISM surveys. The ADP private employment report on Wednesday could also be monitored ahead of Friday’s non-farm payrolls.

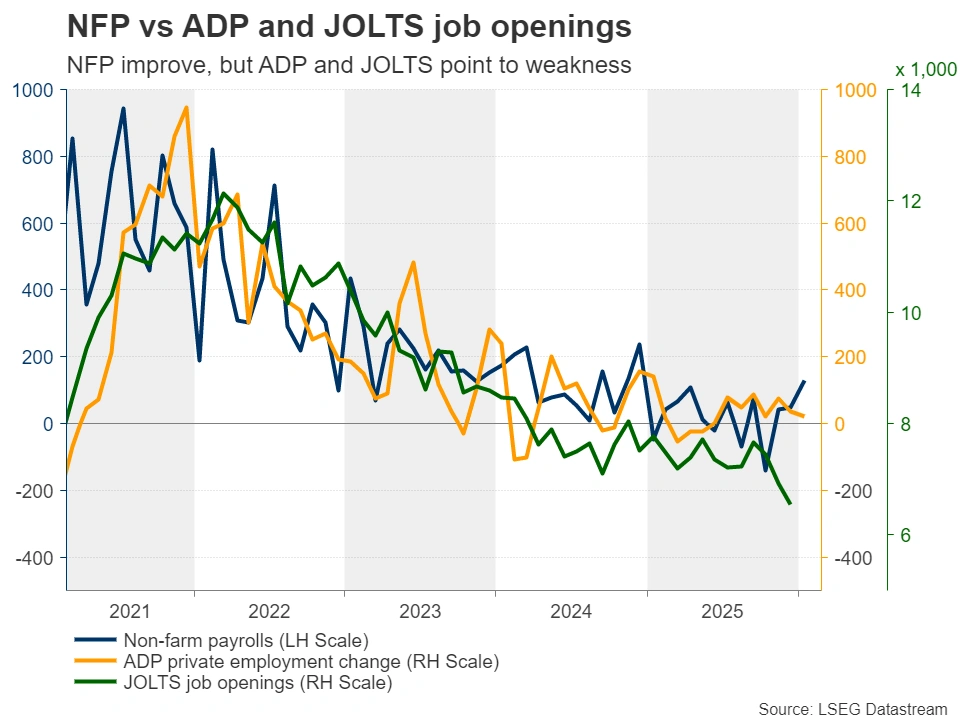

Although the Bureau of Labor Statistics (BLS) announced strong jobs data for January, the ADP reported sluggish growth in private employment during the month, while the JOLTS job openings dropped to their lowest since September 2020 in December. This means that more improvement in labor market data may be needed for investors to further scale back their rate cut bets. That said, for the dollar to stage a meaningful and lasting recovery, rate cut expectations may need to start reflecting less than 50bps worth of rate cuts. In other words, traders may need to start questioning a second quarter-point reduction for 2026.

Will the EZ CPI data raise speculation of lower ECB rates?

The euro held onto its gains, with euro/dollar aided by the divergence in monetary policy expectations between the ECB and the Fed. Although at their prior gathering, ECB officials appeared worried about the latest strength of the euro, they later clarified that they see no need for an imminent policy change, allowing market participants to price in a small 25% chance of a rate cut by December.

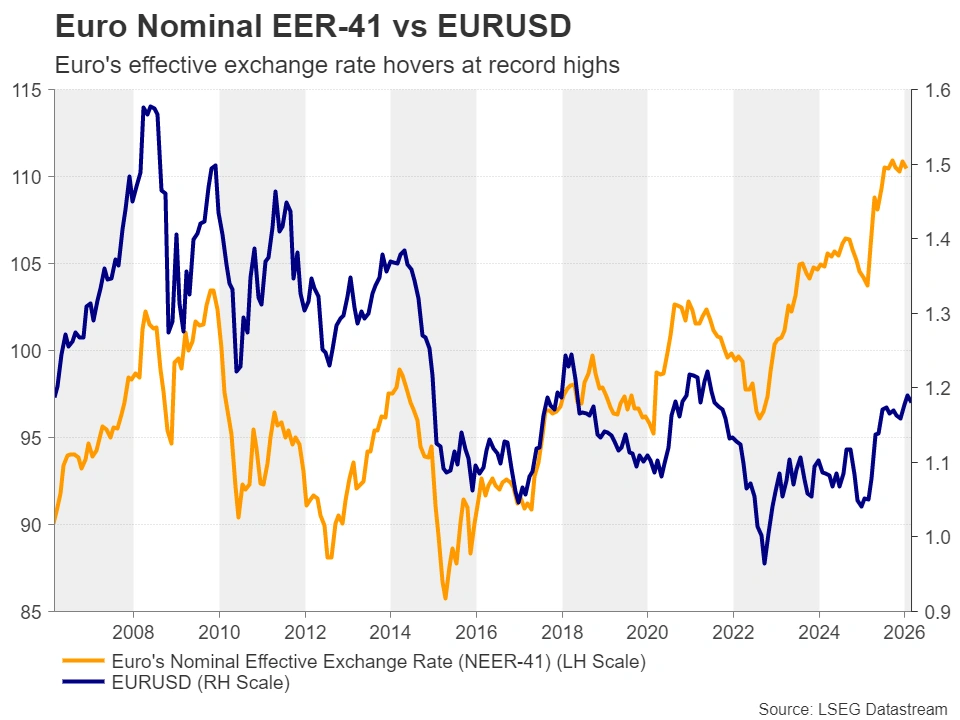

That said, with the nominal effective exchange rate (NEER) of the euro against the currencies of 41 of Eurozone’s biggest trading partners still hovering near record highs, the preliminary CPI data for February on Tuesday could enter the spotlight.

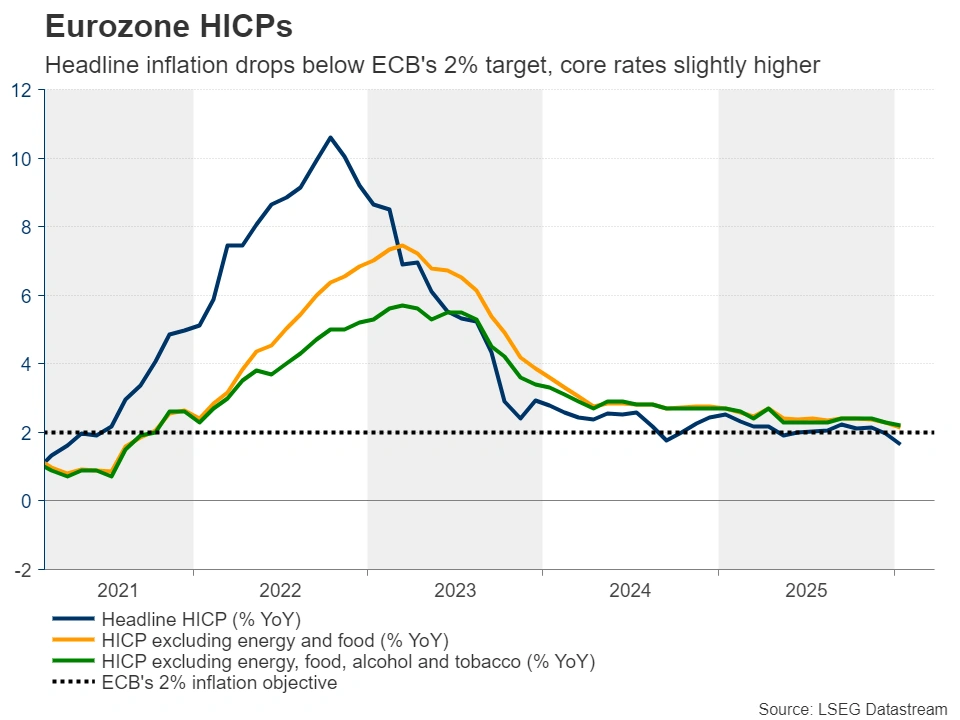

In January, the headline CPI slowed to 1.7% y/y from 1.9%, and the core rate, which excludes the volatile items of food, energy, alcohol and tobacco, ticked down to 2.2% from 2.3%. Further slowdown in the Eurozone’s consumer prices may spark some concerns about whether a strong euro could eventually harm the broader economy, thereby prompting participants to add to the likelihood of a contingency rate cut by the ECB at some point in the foreseeable future.

This could weigh on the euro, especially if the minutes of the latest ECB gathering, due out on Thursday, reveal that there were members discussing the option of additional reductions in interest rates due to a stubbornly strong euro. Eurozone’s retail sales for January, will also be released on Thursday.

Japan’s jobs data on tap amid BoJ hike confusion

The yen saw its wounds deepening this week as focus on PM Takaichi’s plans of aggressive fiscal spending returned, with headlines hitting the wires that she expressed concerns about additional BoJ rate hikes during a meeting with Governor Ueda on February 17. She went a step further earlier this week and appointed two dovish-leaning policymakers to join the Bank’s Board.

That said, after BoJ hawk Takata insisted that more hikes are needed due to “heated” inflation, the probability of a 25bps rate hike in April rose to around 55%. A quarter-point increase is nearly fully priced in for June. Overall, market expectations suggest that the BoJ will wait for the outcome of the spring wage negotiations before deciding to press the hike button again.

On that note, Japan’s employment report for January will be released on Tuesday and signs of further improvement could add to the notion that the BoJ may consider raising rates again in coming months and thereby support somewhat the yen. The opposite may be true in case of weak data, but further declines in the yen could trigger fresh intervention warnings by finance minister Katayama. Thus, the broader picture of dollar/yen may continue pointing to a trendless phase with volatile swings.

Aussie GDP and Swiss inflation data also on the agenda

The aussie continued benefitting from the divergence in monetary policy expectations between the RBA and the Fed, with Australia’s sticky CPI data this week keeping the probability of a back-to-back rate hike on March 17 at a low but decent 20%. Therefore, should Wednesday’s Australian GDP for Q4 and the Chinese PMIs for February come in on the strong side, the commodity-linked currency may extend its uptrend as investors become more convinced about additional RBA rate increases. Australia’s trade data will be released on Thursday.

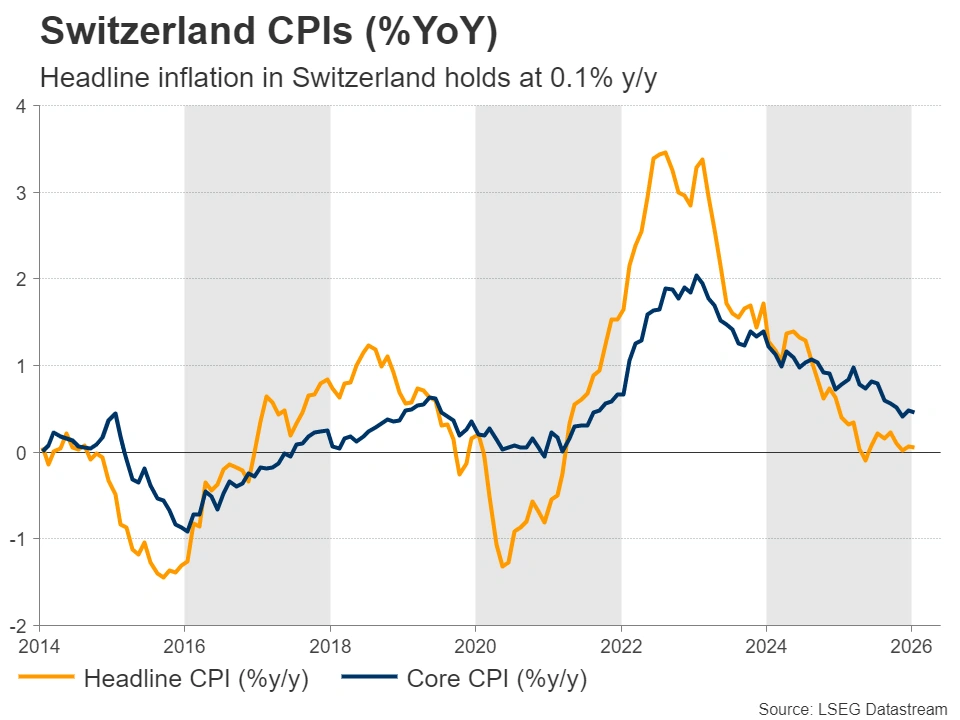

Switzerland’s CPI data will also be released amid increased concerns about how the SNB could stop further advances in the all-mighty franc and thereby prevent the economy from falling into deflation.

The tools available for the central bank are negative interest rates and intervention, but SNB President Schlegel recently noted that the bar for adopting a negative-rate policy again is very high. Intervention may be the more likely choice, although it does not come without risks. So, should the CPI reveal that indeed prices in Switzerland stagnated or even dropped in January, concerns about potential SNB intervention may increase and the Swiss franc may be sold.

{kind=link}