Global markets have shifted into a cautious pause after the relief rally that began on Wall Street yesterday and carried through the Asian session. The initial wave of panic selling earlier in the week has subsided, but investors are not yet ready to push risk assets decisively higher. Instead, trading activity has slowed as markets wait for clarity on two major uncertainties.

The first unknown remains the Middle East conflict. The key debate is whether the current military campaign will remain a short, concentrated operation or evolve into a prolonged confrontation. The outcome carries significant implications not just for geopolitics but also for the global inflation outlook.

Supporters of the “short war” scenario argue that the strategy of leadership decapitation and infrastructure degradation has severely damaged Iran’s ability to coordinate sustained military operations. In this view, the weakening of centralized command structures could eventually force either a rapid collapse in resistance or a relatively quick regime transition.

Others, however, warn that such optimism may underestimate Iran’s military doctrine. The country’s “Mosaic Defense” system deliberately decentralizes authority across multiple regional commands designed to operate independently. Even without direct coordination from Tehran, these autonomous cells could continue to wage asymmetric warfare.

For financial markets, the distinction between these scenarios is crucial. If the conflict remains contained to a few weeks, the current spike in oil prices may be treated as a temporary shock. Energy costs would rise briefly before stabilizing, allowing central banks to look through the inflation impact.

However, a prolonged confrontation could generate a much more problematic dynamic. Persistent disruptions to energy flows and shipping routes would likely produce a structural cost-push inflation cycle, complicating the policy outlook for central banks already grappling with fragile disinflation trends.

While geopolitics dominates the headlines, markets are also preparing for another major catalyst: the upcoming US Non-Farm Payrolls report. Following stronger-than-expected ADP private payroll data, expectations for a weak labor report have diminished significantly. This shift has already pushed market pricing for Fed rate cuts further into the future. Investors have scaled back bets on easing in the first half of 2026, reflecting confidence that the US economy remains resilient despite elevated interest rates.

The real risk for markets, however, lies in the wage component of the report. A strong jobs number combined with rising average hourly earnings could signal that inflation pressures remain persistent, particularly if energy prices remain elevated due to the geopolitical situation. In such a scenario, the Fed could face a renewed inflation risk. That environment would likely push policymakers toward an extended policy pause—and potentially even reopen the debate about whether the next move might eventually be another rate hike.

In currency markets, positioning reflects this cautious environment. Loonie is now the strongest performer this week, supported by elevated oil prices, followed by Dollar and Yen. At the other end of the spectrum, the Euro sits at the bottom of the rankings, followed by Swiss Franc and New Kiwi, while Sterling and the Aussie occupy the middle ground.

In Europe, at the time of writing, FTSE is down -0.17%. DAX is down -0.18%. CAC is down -0.26%. UK 10-year yield is up 0.078 at 4.454. Germany 10-year yield is up 0.065 at 2.822. Earlier in Asia, Nikkei rose 1.90%. Hong Kong HSI rose 0.28%. China Shanghai SSE rose 0.64%. Singapore Strait Times rose 0.70%. Japan 10-year JGB yield rose 0.039 at 2.158.

US initial jobless claims unchanged at 213k, vs exp 215k

US initial jobless claims were unchanged at 213k in the week ending February 28, slightly below expectation of 215k. Four-week moving average of initial claims fell -5k to 215k. Continuing claims rose 46k to 1,868k in the week ending February 21. Four-week moving average of continuing claims rose 7k to 1,852k.

ECB officials split between caution and baseline calm on war risks

ECB policymakers signaled caution today as they assessed the potential economic fallout from the escalating conflict involving Iran. While acknowledging the risk that higher energy prices could complicate the inflation outlook, officials indicated that the situation does not yet warrant a shift in monetary policy.

ECB Vice President Luis de Guindos said the bank’s “baseline” scenario assumes the conflict will prove “short-lived”. However, he warned that a longer war could begin to influence inflation expectations, particularly if energy prices remain elevated for an extended period.

Finnish Governing Council member Olli Rehn took a more cautious stance, warning against assuming a quick resolution. He noted that the conflict had already had “quite some escalation”, and could create a difficult macroeconomic combination of higher inflation and weaker growth across the Eurozone

At the same time, French Governing Council member Francois Villeroy de Galhau emphasized that the current situation does not justify a rate hike. Speaking to French radio, the central bank will continue to monitor developments carefully and assess policy decisions on a meeting-by-meeting basis.

Eurozone retail sales slip -0.1% mom in January as non-food spending weakens

Eurozone retail sales slipped -0.1% mom in January, falling short of expectations for a 0.2% increase. Looking at the breakdown, spending on food, drinks and tobacco rose 0.3%, providing the only notable source of support. However, this was more than offset by declines in other categories.

Non-food retail sales (excluding fuel) dropped -0.2% in Eurozone, while automotive fuel sales fell sharply by -1.1%, reflecting both weaker mobility demand and softer energy consumption after the holiday period.

Across the broader EU, retail sales also declined -0.1% mom. The strongest increases were recorded in Estonia (+4.4%), Latvia (+2.8%), and Portugal (+2.0%), while the steepest declines were seen in Slovakia (-3.5%), Slovenia (-1.9%), and Croatia (-1.3%).

China’s new growth target reflects strategic economic transition

Chinese Premier Li Qiang unveiled Beijing’s economic priorities for the year during the annual government work report at the National People’s Congress, setting the country’s GDP growth target at 4.5% to 5%. The range represents a slight step down from the “around 5%” goal used in the past three years.

The introduction of a target range rather than a single figure signals a more flexible policy approach. By allowing growth to fluctuate between 4.5% and 5%, policymakers are granting themselves greater room to manage domestic challenges without the pressure of hitting a rigid numerical target.

Those challenges remain significant. China’s economy continues to grapple with a prolonged property sector downturn, persistent industrial overcapacity, and uneven domestic demand. Against that backdrop, the leadership appears increasingly focused on stability rather than aggressive expansion.

The new target also highlights Beijing’s strategic shift toward “high-quality” growth. Instead of pursuing rapid expansion through debt-fueled infrastructure or property stimulus, policymakers are emphasizing technology development, advanced manufacturing, and consumption as the core engines of growth.

Other policy targets announced in the report reinforce this balanced approach. Inflation is projected to run around 2%, reflecting authorities’ efforts to guard against deflation risks. The unemployment rate is expected to remain below 5.5%, while the fiscal deficit is set at 4% of GDP, suggesting a somewhat more proactive fiscal stance to support economic activity.

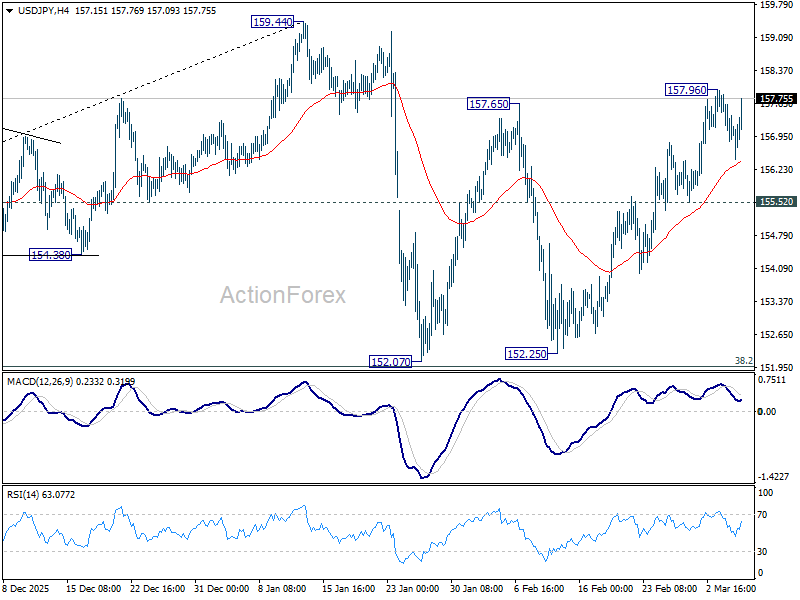

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 156.64; (P) 157.26; (R1) 157.65; More…

USD/JPY recovered ahead of 55 4H EMA, but stays below 157.96 temporary top so far. Intraday bias stays neutral first. On the upside, above 157.96 will extend the rebound from 152.25 to retest 159.44 high. On the downside, though, break of 155.52 will bring deeper fall back to 152.07/152.25 support zone. Overall, price actions from 159.44 are viewed as a near term consolidation pattern. Outlook will remain bullish as long as 38.2% retracement of 139.87 to 159.44 at 151.96 holds.

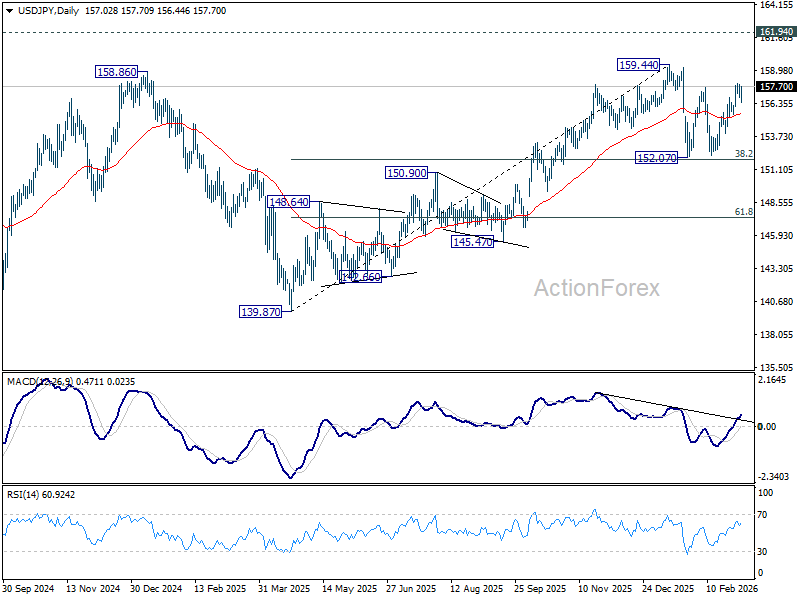

In the bigger picture, outlook is unchanged that corrective pattern from 161.94 (2024 high) should have completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94. This will remain the favored case as long as 55 W EMA (now at 152.16) holds. However, sustained break of 55 W EMA will argue that the pattern from 161.94 is extending with another falling leg.

{kind=link}