The war in Middle East is rapidly spiraling, showcasing how wars are easy to start, almost impossible to control and difficult to end. Even if it is not our main scenario, readers should prepare for a long war, and one where the broader MENA region and perhaps parts of Europe are to some extent affected as well.

We should expect supply bottlenecks and price increases for not just crude oil and natural gas, but also for fertilizers. The longer the problems last, the higher the risk of a more persistent inflation shock. But for Europe particularly, the negative growth impact would also be significant in that case.

Despite the recent rise in short-term market inflation expectations, we do not think major central banks will react by hiking rates. And they should not. This is a classic negative supply shock beyond central banks’ control, and longer inflation expectations remain anchored.

As the conflict escalates, beware of propaganda

The non-apology: On Saturday, Iran’s President Masoud Pezeshkian apologized the country’s Gulf neighbours and promised they would not be targeted anymore for as long as the Gulf states themselves would not attack Iran. Whenever you hear something like this, a de-escalatory tone, regardless of which side presents it, take it with caution at this point.

This is warfare, and propaganda is a key part of it. 1) Pezeshkian, while a member of the provisional council, has never been the most influential decision-maker in Iran. 2) The comment was most likely posturing towards neighbours and the international community (= “we are not the bad guys”) more than anything else. 3) In fact, they broke the promise immediately and this morning Pezeshkian said the “enemy drew naïve conclusions from our remarks”.

So, attacks continue. The US / Israeli air raid has been very intense, reportedly the most intense US operation in recent decades. Iran, in turn, based on media reports has reduced the intensity of launching missiles. We do not know if this is to preserve stockpiles or the first signals that their stockpiles are being depleted. Remember, the side that is first starting to run out of stockpiles (Iran missiles vs. US interceptors), will be forced to change tactics. For Iran, it would mean greater reliance on drones (and they are very good at that). For the US (and allies), running out of interceptors would force them to a) prioritize which targets to protect and which to ignore or b) consider a boots-on-the-ground operation, or c) both.

Regarding “boots-on-the-ground”, Axios reported this morning that the US and Israel are considering sending a “special operation” group on the ground in Iran, but at a later stage in the conflict when Iran’s military would no longer pose a danger to the troops. Remember, without boots on the ground, it will be close to impossible to destroy Iran’s nuclear and missile programs completely. According to the same article, the US administration is also mulling seizure of Iran’s main oil exports terminal (responsible for 90% of exports), Kharg Island. (Resembles the Venezuela playbook.)

In a dangerous escalation, both sides now seem to be targeting water desalination plants. First, Iran claimed the US had attacked a desalination plant on Qeshm island on Saturday. Both the US and Israel denied it, and instead, the Israeli media reported that the UAE was behind it. The UAE officials also deny it. Today, Bahrain said an Iranian drone attack had caused material damage to one of their desalination plants.

These attacks mark a very serious escalation. Attacking critical civilian infrastructure could constitute a war crime. In the desert, desalination plants are vital for human life. We can take the example of Jubail plant that supplies Riyadh with more than 90% of its drinking water. As a Bloomberg analyst reported earlier in the week, the city would have to evacuate within a week if the plant was seriously damaged.

Key risks to supply chains – it’s not just oil and gas

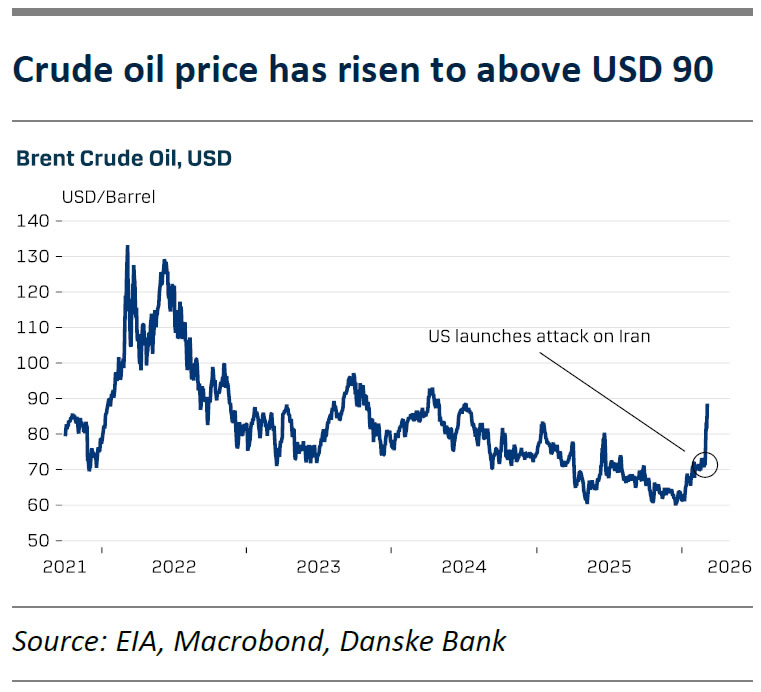

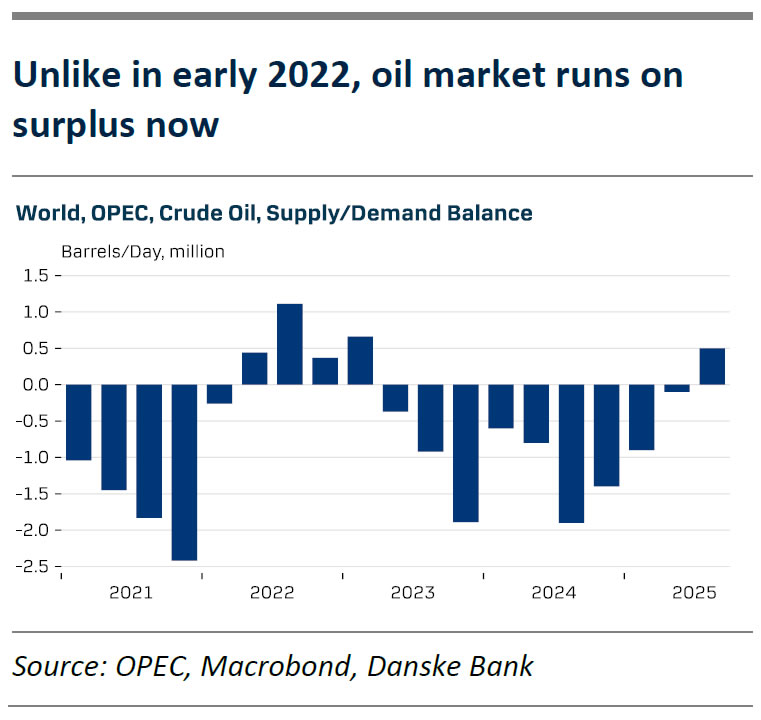

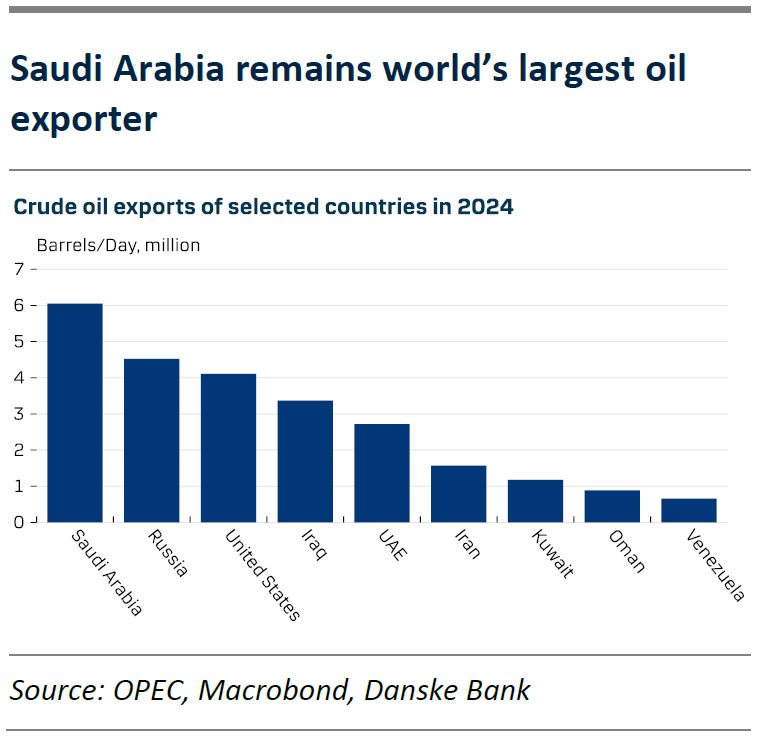

Crude oil: According to the IEA, 20 mb/d, around 25% of world seaborne oil trade, transits the Strait of Hormuz – 80% destined for Asia. The pipeline capacity (alternative to SOH) is 3.5 to 5.5 mb/d. At least Kuwait, the UAE and Iraq have already started reducing oil production as the SOH is effectively closed. On Saudi Arabia’s largest refinery, Ras Tanura, operations have been suspended since Monday due to a drone hit. On Saturday, Saudi Arabia said they intercepted drones that were heading toward Shaybah oil field. Brent oil price topped USD 90 on Friday and will most likely continue higher on Monday when markets open.

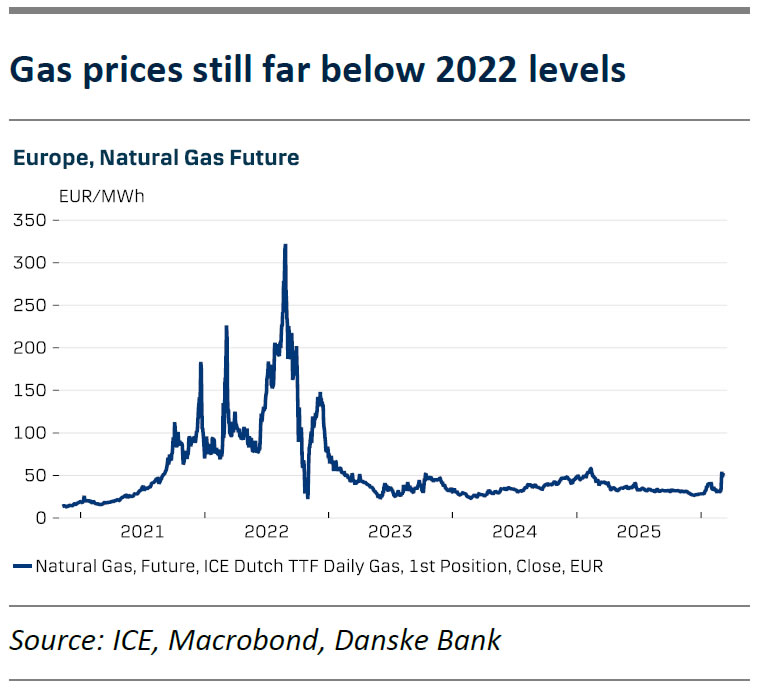

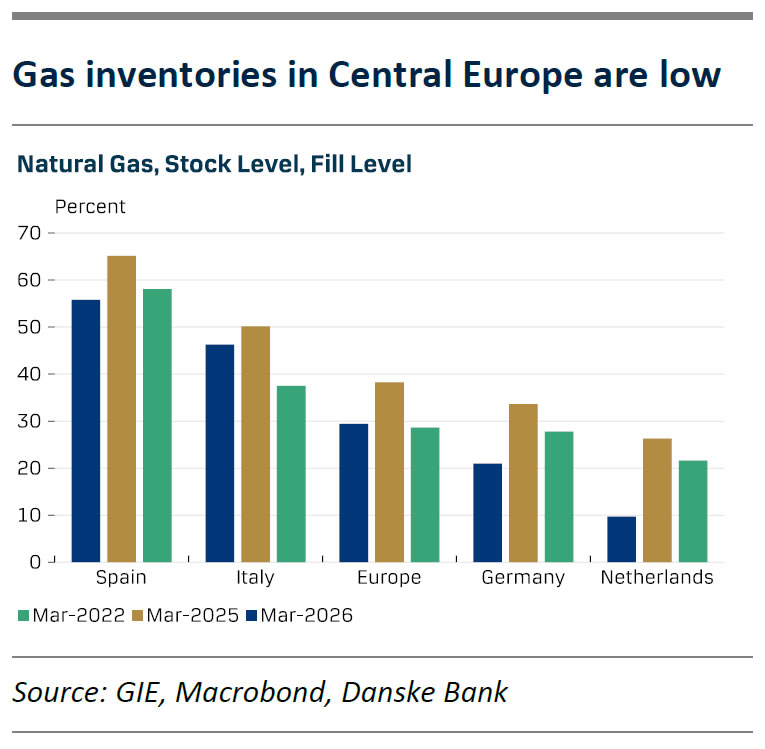

Natural gas: About 93% of Qatar’s and 96% of the UAE’s LNG exports transit through the Strait, representing 19% of global LNG trade. For LNG, there is no alternative route to the SOH. Qatari LNG production has been halted for days due to repeated attacks on key sites. In Europe, gas inventories are already low and during the coming months, inventories will have to be refilled for the coming winter. As it is likely that inventories will now be filled at a higher price, the impact will still be felt next winter, even if we soon witness a de-escalation (which is looking increasingly unlikely).

Fertilizers: Thanks to the abundant gas reserves, the Persian Gulf is one of the most strategically important regions in global fertilizer supply. Approximately 25-35% of global nitrogen fertilizer exports origins from the region. Exports depend heavily on maritime routes i.e. the SOH, and only small amounts could be rerouted by land / rail. Farmers in the Northern Hemisphere particularly buy fertilizers in March-May before the planting season. Now, as prices spike, farmers could delay or reduce purchases with a negative impact on crop yields. Outcome in any case: higher food prices.

The Trump administration is saying they will ensure safe navigation in the SOH. But how exactly? The US was unable to stabilize situation in the Red Sea, and that’s when the enemy was the Yemeni Houthis, not Iran. The only way to return to normalcy in the Red Sea was for President Trump to sign a truce deal with the Houthis in May last year. Only then attacks stopped. And that truce has now collapsed, the Houthis are active again, and vessels are forced to take the longer route around the Cape of Good Hope as the Suez Canal route is not safe.

Central banks should not react to a textbook supply shock

As we write in our Reading the Markets EUR: Geopolitical inflation concerns, 6 March 2026, we do not think the ECB (nor other major central banks) should or would react to the war-induced increase in commodity prices. This is a textbook negative supply shock completely beyond central banks’ control. And despite the increase in short-term market inflation expectations, longer inflation expectations remain anchored.

In our new inflation projection, we see euro area inflation at 2.1% y/y in 2026 and 1.8% in 2027. We also assess a severe scenario with a prolonged surge in oil and gas prices, where 2026 inflation reaches 2.9% y/y and GDP growth slows to 0.6%, yet we still expect the ECB to keep the policy rate unchanged at 2.00%. The European fixed income market has come under significant pressure following the start of the war.

However, as we do not expect this to result in hikes from the ECB, we favour fading such pricing once significant volatility subsides. An apparent risk to our view is that the 2021-22 trauma from not reacting fast enough dominates and the ECB rushes to hike rates.

Contagion risk in MENA region – with spillover risks to Europe

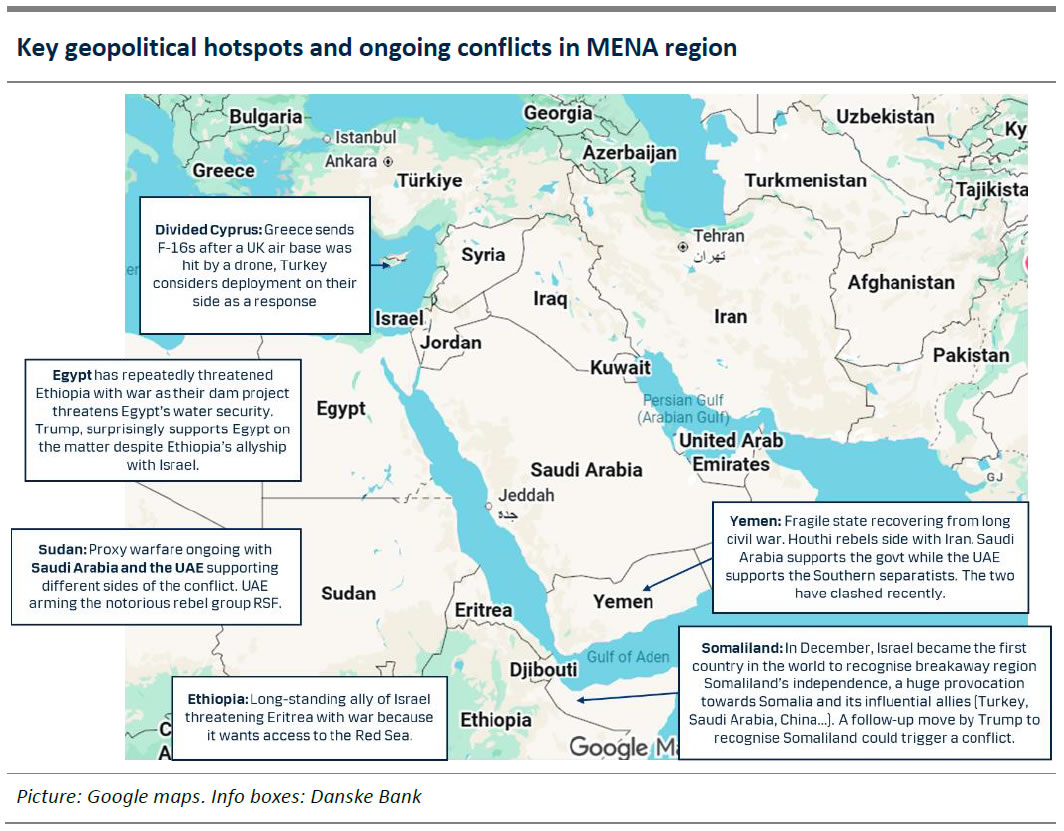

Lastly, note that tensions are very high in the broader MENA region. Just see the map below where the key hotspots or ongoing conflicts are illustrated. Several European countries are already to some extent involved as well. The UK is allowing the US to use their bases. France has promised to join the US alliance in ensuring safe navigation in the SOH. Turkey and Greece are increasingly at odds in Cyprus. And Trump is threatening to cut trade ties to Spain – the only European country whose leadership has strongly criticized the US attack.

For Russia, the current situation is ambiguous. The longer the US remains tied up in Middle East, the less it will have attention and resources to support Ukraine. On the other hand, the US is now using Ukrainian drones to intercept the Iranian ones, so at least the military collaboration is now reciprocal, which should please Trump. In theory, Russia should benefit from the increase in global oil and gas prices. However, at least for now, Urals price gap to Brent remains unchanged. Lastly, Putin, will certainly take note that his list of friends is getting shorter and shorter: first Al-Assad, then Maduro, now Khamenei… It has become risky being close with Putin.

China will also be watching closely. Will the fact that the US is tied up in Middle East change their calculus regarding Taiwan? A huge provocation would be if the US followed Israel and went to recognize Somaliland’s independence on the other side of the Red Sea. Somaliland is a long-standing friend of Taiwan, which is why China aligns with motherland Somalia. For years, experts have feared that the first conflict between superpowers China and the US would be a proxy war in Africa.

{kind=link}