The global markets are holding in limbo today as the initial surge in geopolitical risk faded and attention shifted back toward the upcoming Fed decision tomorrow. While tensions in the Middle East remain elevated, price action across assets suggests that much of the shock has already been absorbed, leaving traders reluctant to take strong directional bets.

Oil prices briefly spiked earlier after renewed Iranian attacks on UAE energy infrastructure, pushing Brent toward the 104 level, but the move quickly reversed. The key shift in narrative is that the Strait of Hormuz, while heavily disrupted, is not fully blocked. Reports of selective tanker transits, including vessels linked to Pakistan and Turkey, suggest that the situation resembles a bottleneck rather than a complete shutdown. This distinction has been crucial in preventing a more aggressive repricing in energy markets.

At the same time, oil prices above 100 already reflect a significant geopolitical premium. Without a direct and sustained hit to major producers such as Saudi Arabia or Iraq, markets appear reluctant to push prices materially higher. As a result, the energy shock is now seen as elevated but contained, at least in the near term.

This stabilization in oil has removed a key pillar of support for Dollar. While the greenback initially attempted to rally on renewed risk aversion, gains quickly faded as energy markets failed to extend higher. The result is a sluggish Dollar, unable to capitalize on geopolitical tensions in the way it did earlier in the conflict.

Compounding this dynamic is the Fed’s blackout period, which has left markets without guidance on how policymakers are interpreting the recent oil-driven inflation shock. Since the surge in energy prices began in late February, there has been no official commentary, creating what can best be described as a valuation vacuum.

This uncertainty has become a central driver of current market behavior. With a rate hold fully priced for the upcoming FOMC meeting tomorrow, the real question is how hawkish that hold will be. Without clarity, traders are unwilling to commit, leading to muted price action across currencies and rates.

Against this backdrop, Australian Dollar has emerged as the standout performer. Initial volatility following the RBA’s split decision quickly gave way to renewed strength after Governor Michele Bullock clarified that the board remains united on the need for further tightening, with disagreement centered only on timing.

Market expectations have since stabilized, with April seen as a likely pause ahead of key inflation data, but another rate hike broadly anticipated in May. This clarity has allowed Aussie to outperform in an otherwise directionless FX landscape.

Overall, currency markets reflect a broader theme of consolidation. With oil risks capped for now and Fed policy uncertainty unresolved, major pairs remain trapped within last week’s ranges. Until either energy markets break higher again or the Fed provides clearer guidance, markets are likely to remain stuck in ranges.

In Europe, at the time of writing, FTSE is up 0.82%. DAX is up 0.47%. CAC is up 0.73%. UK 10-year yield is down -0.059 at 4.653. Germany 10-year yield is down -0.029 at 2.920. Earlier in Asia, Nikkei fell -0.09%. Hong Kong HSI rose 0.13%. China Shanghai SSE fell -0.85%. Singapore Strait Times rose 1.38%. Japan 10-year JGB yield fell -0.017 to 2.263.

German ZEW collapses to -0.5 on rising stagflation risks

German ZEW Economic Sentiment plunged into negative territory in March, with Eurozone sentiment also dropping sharply as rising energy prices dent confidence. The collapse reflects growing concern that Middle East tensions and inflation risks could derail Europe’s fragile recovery. Read more.

RBA rate hike to 4.10% lacks conviction as board splits 5–4

RBA raised the cash rate to 4.10%, but the narrow 5–4 vote revealed a divided board and limited conviction behind the move. While policymakers cited rising fuel costs and inflation risks, the split highlights growing uncertainty over the outlook as energy shocks threaten both inflation and growth. Read more.

RBA united on further tightening despite split vote, Bullock says

RBA Governor Michele Bullock said the board remains united on further tightening despite the 5–4 split, with disagreement centered on timing rather than direction. She emphasized that inflation remains too high and driven by excess demand, while warning that policy may need to stay restrictive to prevent more persistent price pressures. Read more.

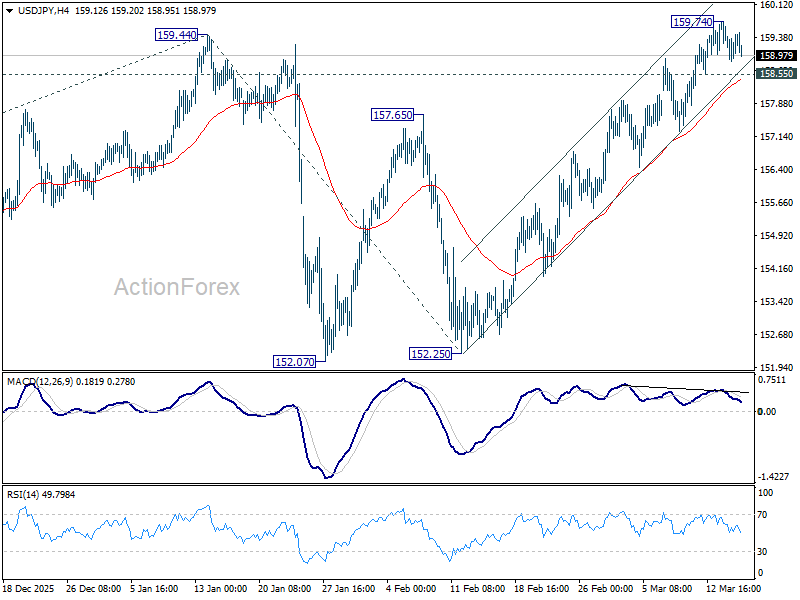

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 158.68; (P) 159.21; (R1) 159.58; More…

USD/JPY is extending consolidations below 159.74 and intraday bias remains neutral. On the upside, above 159.74 will target a retest of 161.94. Firm break there will confirm larger up trend resumption and target 61.8% projection of 139.87 to 159.44 from 152.25 at 164.34. However, considering bearish divergence condition in 4H MACD, break of 158.55 should indicate short term topping, and turn bias back to the downside for deeper pullback.

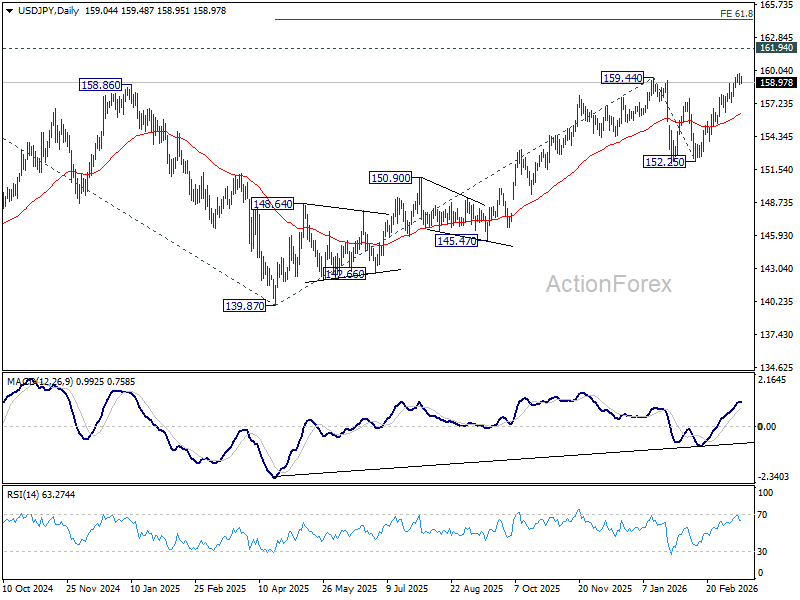

In the bigger picture, outlook is unchanged that corrective pattern from 161.94 (2024 high) should have completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94. This will remain the favored case as long as 55 W EMA (now at 152.70) holds. Firm break of 161.94 will pave the way to 61.8% projection of 102.58 to 161.94 from 139.87 at 176.75.

{kind=link}