Risk rally is pausing as anticipation gives way to verification. Equity gains are stalling near record levels as markets move from pricing a US-Iran deal to waiting for actual delivery, with renewed talks likely in the coming days. Oil’s pullback on diplomatic optimism has taken pressure off inflation expectations, while Dollar consolidates losses, signaling a market that has run ahead of events and is now in wait-and-see mode.

A key driver behind the earlier rally was the steady unwind of the war premium. As prospects for renewed negotiations emerged, the “fear bid” in oil faded quickly, removing a major support for Dollar and easing pressure on global risk assets. However, with that repricing largely complete, markets now lack a fresh catalyst to extend gains further.

Comments from US President Donald Trump have reinforced the perception that the conflict is nearing its endgame. In a Fox Business interview, he said the war is “very close to over” and added that “they want to make a deal very badly.” Still, markets are no longer reacting to rhetoric alone. The next phase hinges on whether the anticipated second round of talks—expected within the next two days—can deliver tangible progress.

Focus is firmly on whether there will be a ceasefire extension or, even better, a “bridge deal” that provides a pathway toward a more durable settlement. Markets appears to be cautiously leaning toward the latter, but confirmation is still lacking yet.

On the monetary policy front, attention is also turning to the Federal Reserve outlook. Trump expressed optimism that his nominee, Kevin Warsh, could be confirmed as the next Fed Chair as soon as next week. He also indicated that interest rates would likely decline once Warsh takes office.

Warsh’s confirmation process will be closely watched, particularly given its implications for Fed independence and the future path of rates. Chair Tim Scott noted that the Senate Banking Committee will focus on inflation, economic conditions, and institutional independence during the hearings.

In the currency markets, Dollar remains the worst performer for the week so far despite today’s recovery. Yen is the second worst, followed by Loonie. Aussie is now the strongest, followed by Kiwi, and the Swiss Franc. Euro and Sterling are positioning in the middle of the ladder.

In Europe, at the time of writing, FTSE is up 0.12%. DAX is up 0.09%. CAC is down -0.53%. UK 10-year yield is up 0.02 at 4.745. Germany 10-year yield is up 0.019 at 3.042. Earlier in Asia, Nikkei rose 0.44%. Hong Kong HSI rose 0.29%. China Shanghai SSE rose 0.01%. Singapore Strait Times rose 0.27%. Japan 10-year JGB yield fell -0.016 at 2.403.

Bitcoin Rallies Without Conviction, Clarity Act Uncertainty to Cap Break Above $80K

Bitcoin is rising—but without conviction. Despite improving risk sentiment, uncertainty around the Clarity Act and Senate delays cap upside momentum. With a narrow window for progress before the US election cycle takes over, regulatory clarity may remain out of reach—leaving $80K as both a technical and policy ceiling. Read more.

WTI Drops Below $90, $80 Next If US-Iran Talks Deliver ‘Bridge Deal’

WTI has slipped below $90 as markets bet a second round of US-Iran talks could deliver a ceasefire extension or even a “bridge deal,” paving the way toward $80. With the war premium unwinding, traders are front-running a path to de-escalation rather than waiting for confirmation. Read more.

Eurozone Industrial Production Rises 0.4%, Led by Capital and Consumer Goods

Eurozone industrial production rose more than expected in February, with strength in capital goods and non-durable output offsetting declines in energy. The data points to a modest but uneven recovery in the sector. Read more.

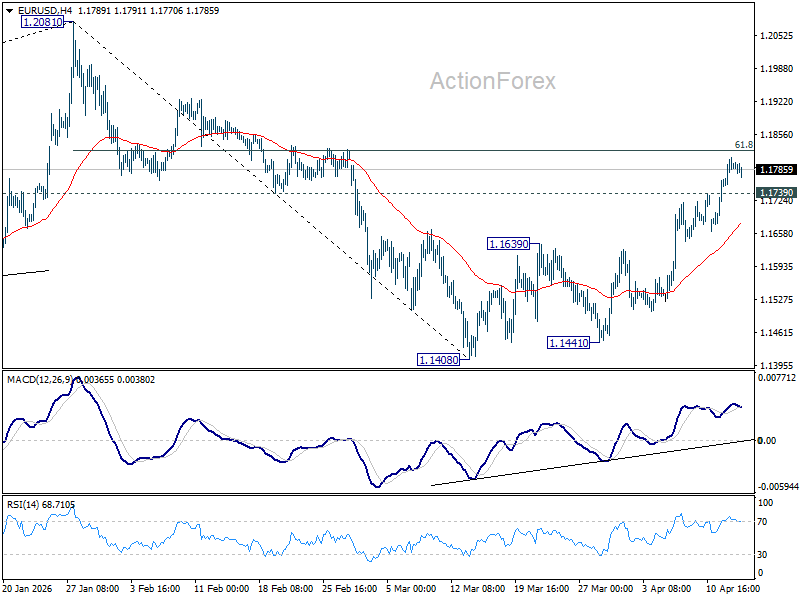

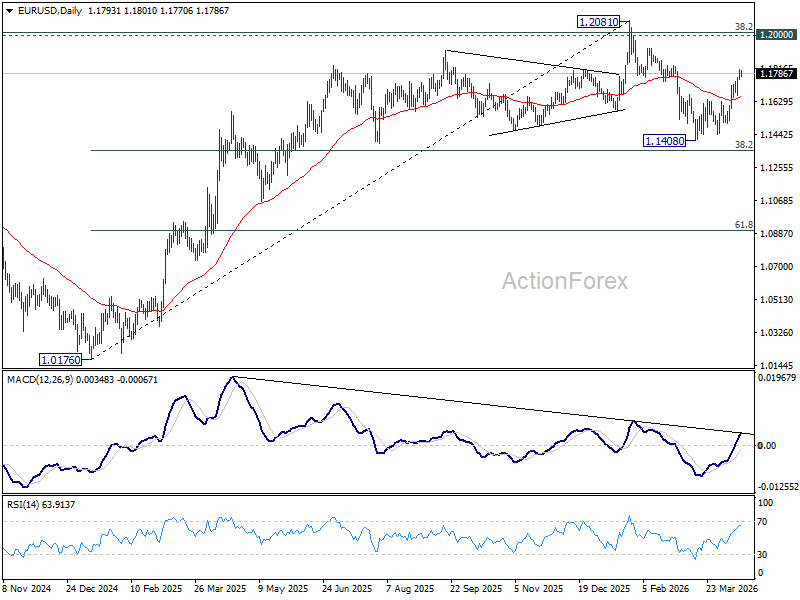

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1763; (P) 1.1788; (R1) 1.1820; More….

Intraday bias in EUR/USD stays mildly on the upside despite some loss of upward momentum. Decisive break of 61.8% retracement of 1.2081 to 1.1408 at 1.1824 will extend the rally from 1.1408 to retest 1.2081 high. On the downside, below 1.1739 minor support will turn intraday bias neutral first.

In the bigger picture, the strong support from 38.2% retracement of 1.0176 to 1.2081 at 1.1353 suggests that the pullback from 1.2081 is more likely a corrective move. Strong support was also found in 55 W EMA (now at 1.1513). Focus is back on 1.2 key cluster resistance level. Decisive break there will carry long term bullish implications. Nevertheless, break of 1.1408 support will revive the case of medium term bearish trend reversal.

{kind=link}