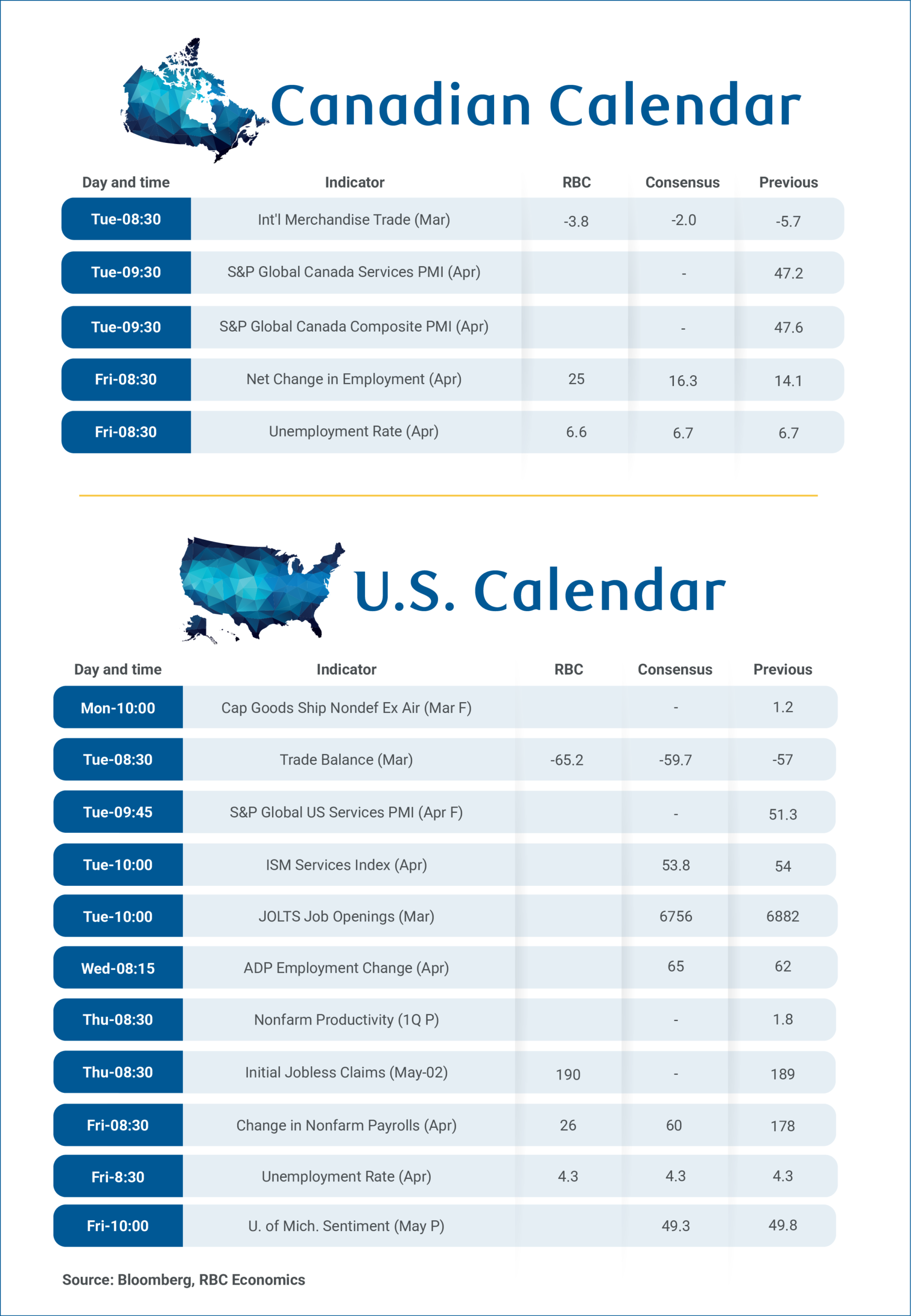

Canadian labour market data for April next Friday will be in focus, and we expect employment to remain broadly consistent with a gradual improvement in per-worker conditions after controlling for an unprecedented pullback in labour force growth.

We expect about 25,000 jobs were added in April following losses in January and February that only partially recovered in March.

That would still leave employment down 70,000 in the first four months of 2026, but would also likely still be enough to push the unemployment rate down to 6.6% from 6.7%—further below the recent 7.1% peak in August and September 2025.

We have discussed before how aggressive federal immigration caps and an aging population have sharply lowered the amount of employment growth needed to push the unemployment rate (the better indicator of per-worker labour conditions) lower.

Details of recent labour market reports have also not been as soft as headline employment growth numbers imply. Specifically:

- Weakness has been largely contained to trade-exposed sectors with little evidence of spreading. Employment in sectors heavily exposed to U.S. trade (with 35% or more jobs due to demand from the U.S.) have declined 3% since February 2024, while other sectors grew by 1%.

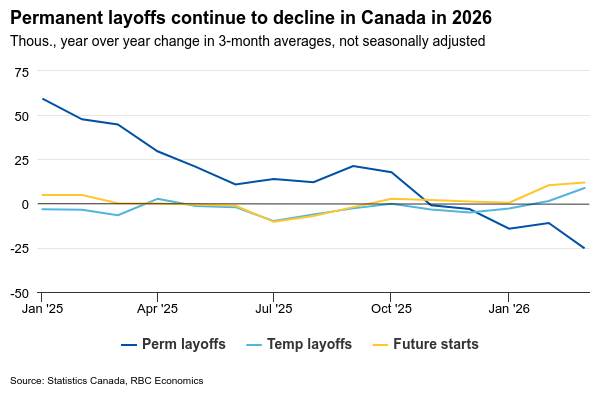

- Permanent layoffs have declined. Early 2026 job losses were not driven by permanent layoffs, which have fallen since October 2025. Instead, temporary layoffs and future starts (workers with a future job start date, but still technically unemployed) account for recent increases.

- No signs of “hidden” unemployment. The unemployment rate provides a “clean” read of per-worker conditions only if discouraged workers are not giving up their jobs or being pushed into part-time work when they would rather have full time jobs.

- Still, broader unemployment measures like R-8, which include such workers (discouraged and involuntary part-time workers) remain aligned with the official rate. Both measures have been relatively unchanged from a year ago, indicating weakness is not masked beneath the surface.

- Business sentiment is brightening. The Bank of Canada’s Business Outlook Survey, conducted in February, revealed strengthening hiring and investment intentions. Businesses reported plans focused on productivity gains and capacity expansion, reflecting a healthy rebound in household spending in 2025, and substantial improvement in trade uncertainties.

The labour market is not yet strong: Unemployment rate declines have still been modest to date, and we don’t expect a spike in wages in March will be repeated in April.

But, our base case projections assume further gradual improvements this year with the unemployment rate edging down to 6.3% by year end even with job growth softer than historically normal.

Canadian international trade data has been exceptionally volatile, but the merchandise trade deficit should narrow in March with a 40% surge in oil prices due to the Middle East conflict pushing the energy surplus higher. We look for exports to rise almost 5%, and imports to post a smaller 1.5% increase, pushing the trade deficit down to -$3.8 billion from -$5.7 billion in February.

We expect U.S. nonfarm payrolls added just 26,000 jobs in March—a number that, given current conditions, represents breakeven growth and has become routine. With shrinking labor supply, the U.S. does not need substantial job additions to maintain a steady unemployment rate. A meaningful decline in continuing claims between the March and April reference weeks supports our expectation that the unemployment rate will hold steady at 4.3% in March.

{kind=link}