Next week’s U.S. data should point to a resilient, but increasingly strained, consumer spending environment. We expect the PCE deflator rose 0.4% in April, weighing on household purchasing power and leaving real income growth soft. The housing market remains constrained, with renewed affordability pressures and supply-side constraints, and we expect new home sales fell back toward a 669K pace in April as higher mortgage rates and a weak labor market weigh on demand. In emerging markets, Brazil’s growth likely held firm in Q1, but momentum is set to slow as inflation risks rise and policy remains restrictive. In Australia, we expect headline CPI to rise 4.7% year over year, driven largely by Easter holiday travel, with trimmed mean at 3.4%, while temporary fuel excise cuts keep energy prices more contained.

United States:

- Personal Income & Spending (Thursday), New Home Sales (Thursday)

G10 Economies:

- Australia CPI (Wednesday)

Emerging Markets:

- Brazil GDP (Friday)

U.S. Week Ahead

Personal Income & Spending • Thursday

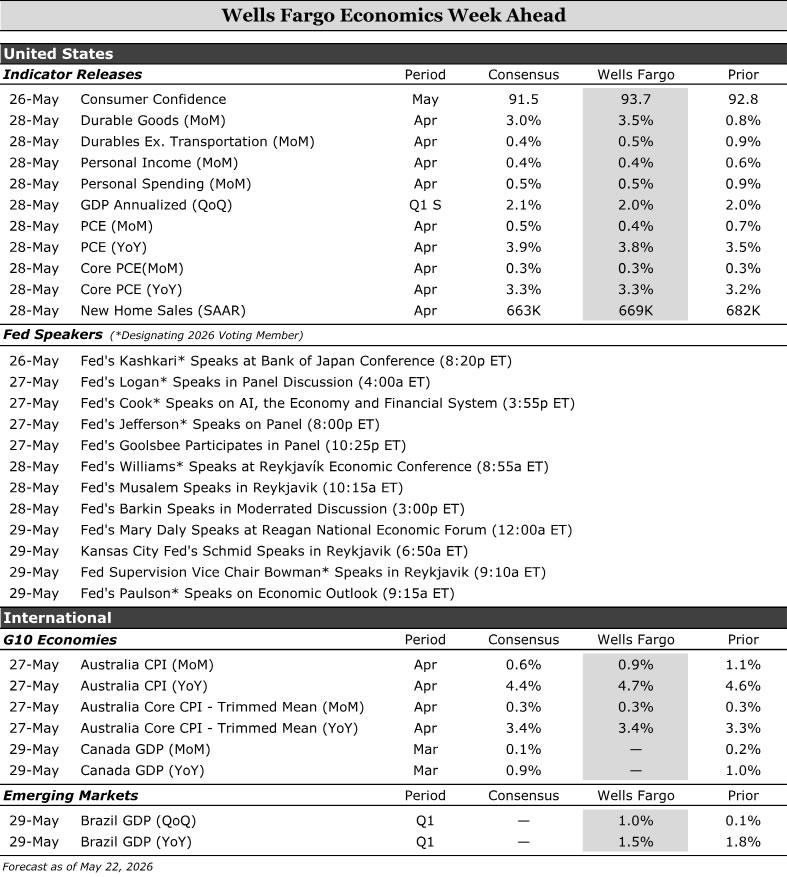

Broad consumer spending carried into April, but the backdrop is becoming more challenging as the conflict in Iran drags on. Control group retail sales (sales excluding gas, autos, building materials, and restaurants) rose 0.5% during the month and growth remained positive even when adjusting for higher prices. That decent growth, along with some modest upward revisions to prior data, suggests goods spending started off on a decent clip in the second quarter. Still, households are operating in a constrained environment, with rising trade-offs in how spending is allocated.

We estimate consumer inflation measured by the PCE deflator rose 0.4% in April, offsetting nearly all the 0.5% gain we expect in nominal spending growth. Renewed price pressure is eroding household purchasing power, while a cooling labor market and lackluster hiring are weighing on wage growth. We look for broad personal income to rise 0.4%, leaving real income growth weak and unlikely to sustain current spending momentum.

New Home Sales • Thursday

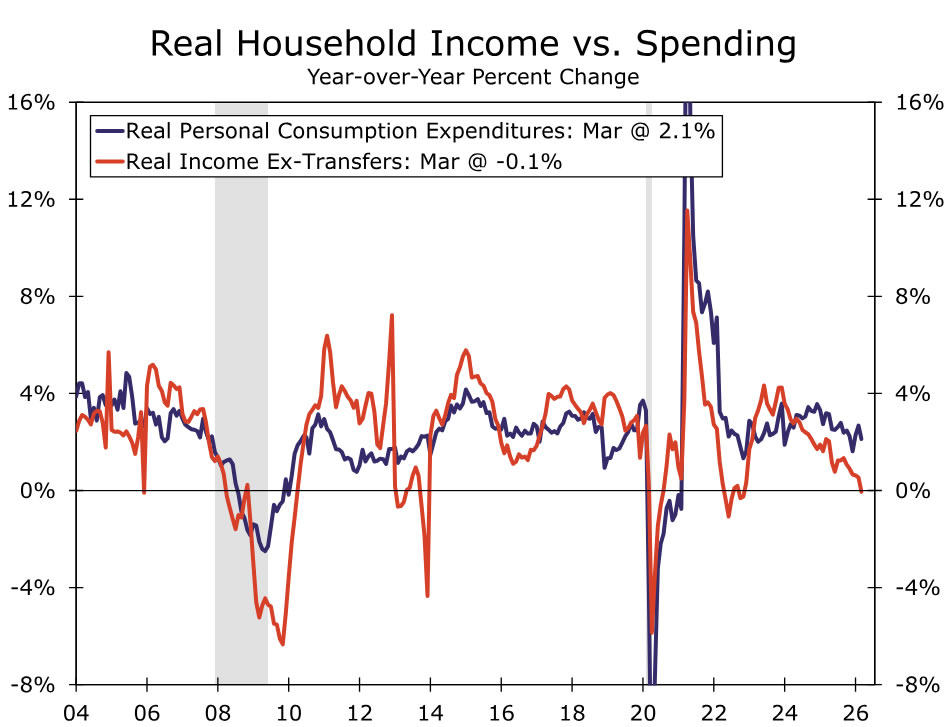

The trend in sales has firmed over the past several months. During March, the pace of sales rose to 682K, a 3.3% year-over-year gain. That said, the new home market remains generally soft. Builders continue to lean on incentives such as mortgage rate buy-downs and price cuts to support demand, and in March, the median new home price was down 6.2% on a yearly basis. Meanwhile, inventory remained high with the count of new homes available for sale at 481K in March.

Looking forward, we expect new home sales fell back to a 669K unit pace in April. Mortgage rates have legged higher in recent months and are currently hovering around 6.5%, largely reflecting the war in the Middle East and the potential for an end to the Fed’s easing cycle on account of higher inflation. In addition to renewed affordability challenges, weak labor market fundamentals represent another headwind for demand. What’s more, builders are contending with several supply-side constraints, including elevated inventory levels, higher land prices and increased building material and labor costs.

G10 Week Ahead

Australia CPI • Wednesday

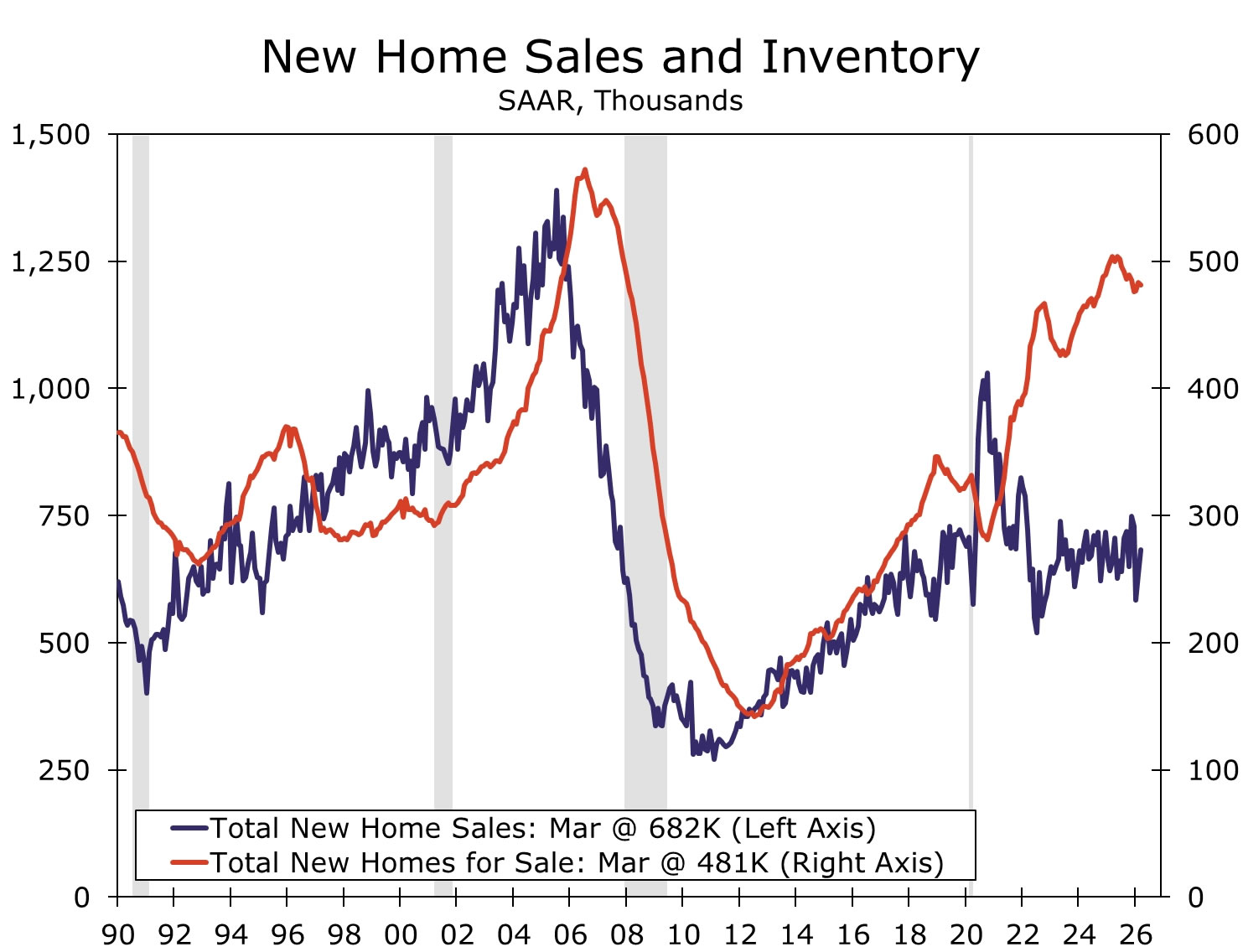

Next week brings Australia’s April inflation release. We expect headline CPI to rise 4.7% year over year, with trimmed mean inflation at 3.4%. In March, CPI rose 4.6%, driven largely by a 33% month-over-month surge in fuel prices. The government announced temporary measures to reduce fuel excise by half from April 1, which lowered average petrol pump prices. At its May monetary policy meeting, the Reserve Bank of Australia (RBA) said it expected the measure to subtract around 0.5 percentage points from year-over-year inflation in April.

Still, the cost shock appears broader than fuel. April PMIs and business surveys pointed to stronger price pressures, with firms also raising output prices at one of the fastest rates in the survey’s decade-long history. Pass-through may be visible across food, recreation, and housing-related categories. Restaurants have enacted temporary fuel surcharges, while reports also point to sharp increases in building material costs, including pipes, timber, and plastic. Seasonal Easter travel could also lift recreation and culture inflation.

With the RBA focused on inflation risks and inflation expectations as its “north star,” the April data will be important for gauging how quickly higher input costs are moving through the broader inflation basket. A stronger-than-expected print would raise upside risks to the Cash Rate, especially after the 2026–27 Federal Budget leaned more stimulative. At the same time, recent labor market data have shown some signs of easing, which supports a data-dependent approach. We continue to expect a June hold and an August hike, bringing the Cash Rate to a terminal rate of 4.60%, with the RBA’s next move contingent on developments in the Middle East conflict, inflation’s response to this year’s three rate hikes, growth, and labor market conditions.

EM Week Ahead

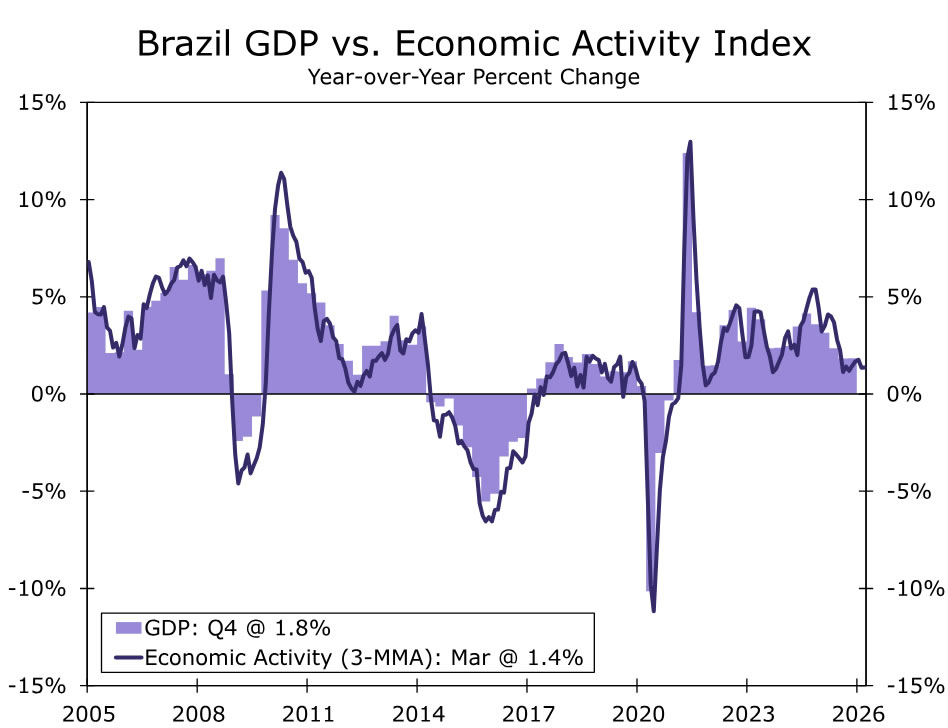

Brazil GDP • Friday

Brazil’s Q1-2026 GDP data are due next week and are likely to show that the economy expanded by 1.0% quarter over quarter and 1.5% year over year. Strong real wage gains and supportive fiscal policy have continued to underpin consumption, helping activity start the year on solid footing. However, growth is likely to soften beyond Q1 as restrictive policy weighs more heavily on activity. The inflation backdrop has also become more complicated, as disinflation from last year’s aggressive tightening faces renewed external price pressures from the war in the Middle East and persistent domestic fiscal risks. Election-year dynamics are also likely to add pressure for more stimulative fiscal policy, while longer-term inflation expectations have moved higher across survey-based and market-based measures. These factors should constrain the scope for monetary easing.

Against this backdrop, we still expect the Brazilian Central Bank (BCB) to proceed with monetary easing, but at a more cautious pace than anticipated at the start of the year. We now see fewer cuts over the remainder of 2026. While easing is still likely to extend into 2027, we expect a higher terminal rate as policy decisions become increasingly driven by the evolving inflation outlook, rather than growth conditions alone.

{kind=link}