Global financial markets remain trapped in a tense but directionless pattern as investors struggle to price a US-Iran conflict that is neither escalating into full confrontation nor moving convincingly toward resolution. Brent crude continues hovering near USD 105 after another volatile week, while US 10-year Treasury yields remain comfortably above 4.5%. Equities are largely drifting sideways, with US futures flat and European indexes posting only marginal gains. Dollar also remains broadly firm as persistent geopolitical uncertainty keeps risk appetite restrained.

At the center of the paralysis is a negotiation process increasingly resembling a war of attrition rather than a genuine march toward peace. US Secretary of State Marco Rubio acknowledged there had been “slight progress” and “a little bit of movement” in talks ahead of the NATO summit in Sweden, but he simultaneously warned against excessive optimism, emphasizing that a comprehensive breakthrough remains highly unlikely.

Both Washington and Tehran appear convinced that time and economic endurance favor their own position. The US continues applying heavy economic pressure by disrupting Iranian oil exports and maritime trade, while Iran is leveraging its grip over the Strait of Hormuz as its ultimate bargaining tool.

Two major issues continue blocking meaningful progress. First, Iran’s insistence on retaining its highly enriched uranium stockpile remains fundamentally incompatible with US demands that the material be removed entirely from the country. Second, Tehran’s proposed Hormuz transit system — including ship vetting procedures and “security fees” for passage — has emerged as another major sticking point. Rubio called the tolling proposal “completely unacceptable,” warning it would make any diplomatic solution unworkable.

The result is an unstable quiet where the greatest fear may no longer be outright diplomatic collapse itself, but rather a single maritime miscalculation capable of destroying the fragile ceasefire.

Markets are therefore entering the weekend bracing for another intense burst of headline volatility. A highly technical, bare-minimum agreement aimed merely at lowering economic tensions remains possible. But equally plausible is a rapid return to more aggressive rhetoric if negotiators fail to produce a signed framework over the next 48 hours.

Until one side is ultimately forced to blink — or until a fresh escalation reshapes the balance entirely — markets may remain trapped inside volatile geopolitical limbo.

Canada Retail Sales Jump on Higher Fuel Prices, Underlying Demand Still Soft

Canada’s retail sales jumped in March as higher oil prices boosted gasoline spending, but weaker core sales and falling volumes pointed to softer underlying demand. Read More.

EUR/CAD Struggles for Direction as Oil Volatility and ECB Divisions Offset Each Other

EUR/CAD remained trapped in consolidation as fading oil sensitivity in CAD and divisions inside the ECB offset each other and capped directional momentum. Read More.

Germany Ifo Business Climate Improves Further, but Recovery Still Fragile

Germany’s business sentiment improved modestly in May as services returned to positive territory, though trade and construction sectors continued struggling. Read More.

Germany GfK Consumer Climate Improves to -29.8 as Income Outlook Recovers

Germany’s consumer confidence showed tentative signs of stabilization as income expectations improved sharply, though Middle East tensions continued weighing on households. Read More.

UK Retail Sales Fall -1.3% mom in April as Consumer Demand Weakens

UK retail sales fell far more than expected in April, reinforcing signs that consumer demand is weakening as households turned cautious on discretionary spending. Read More.

Silver’s $90 Breakout Dream Fades, but Structural Deficit Keeps $70 Floor Alive

The silver market may be shifting from speculative breakout mania toward violent range trading as geopolitical panic remerges but industrial demand remains structurally strong. Read More.

Japan Core Inflation Slows to Four-Year Low as Weak Price Momentum Challenges BoJ Hawks

Weakening service inflation and fading food-price spikes reinforced concerns that Japan’s underlying inflation trend may still be too fragile for aggressive BoJ tightening. Read More.

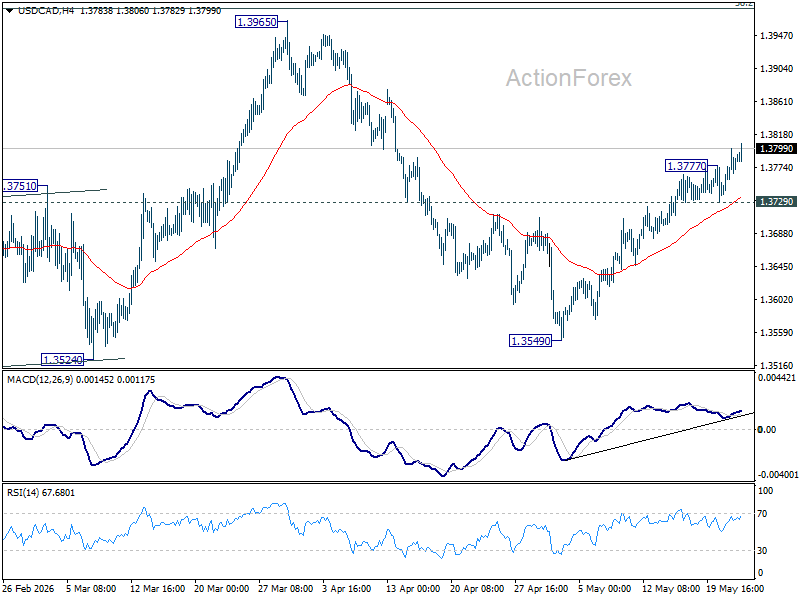

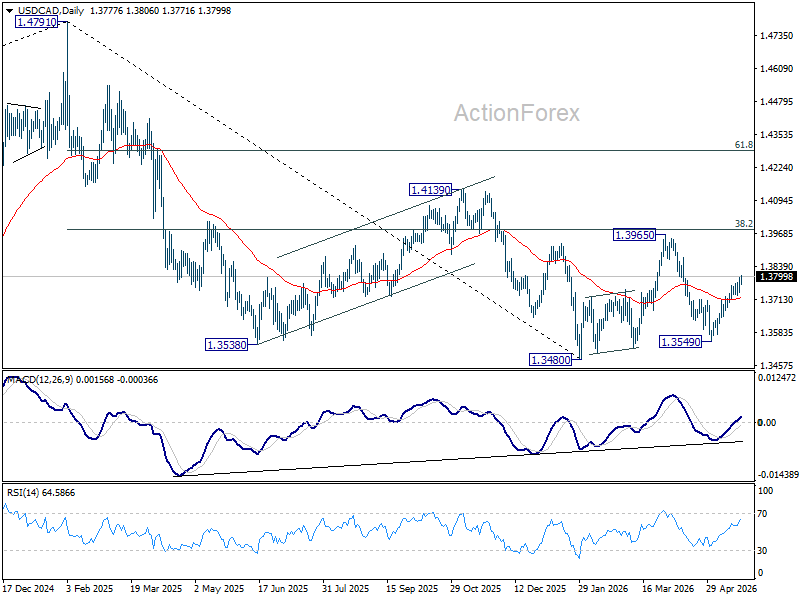

USD/CAD Daily Outlook

USD/CAD’s rise from 1.3549 resumed after brief retreat ad intraday bias is back on the upside. The rally is seen as seen as the third leg of the corrective pattern from 1.3480, and should target 1.3965 resistance next. On the downside, below 1.3729 minor support will turn intraday bias neutral again.

In the bigger picture, price actions from 1.4791 are seen as a corrective pattern to the whole up trend from 1.2005 (2021 low). Deeper fall could be seen, as the pattern extends, to 61.8% retracement of 1.2005 to 1.4791 at 1.3069. However, decisive break of 38.2% retracement of 1.4791 to 1.3480 at 1.3981 will argue that the correction has completed with three waves down to 1.3480 already.

{kind=link}