UK inflation data offered some relief ahead of this week’s Bank of England meeting, with headline CPI holding steady at 2.8% yoy in May, below expectations for a rise to 3.0% yoy. On a monthly basis, CPI slowed sharply from 0.7% mom to 0.2% mom, also undershooting forecasts of 0.4% mom. Core inflation edged higher from 2.5% yoy to 2.6% yoy, but came in below the expected 2.7% yoy.

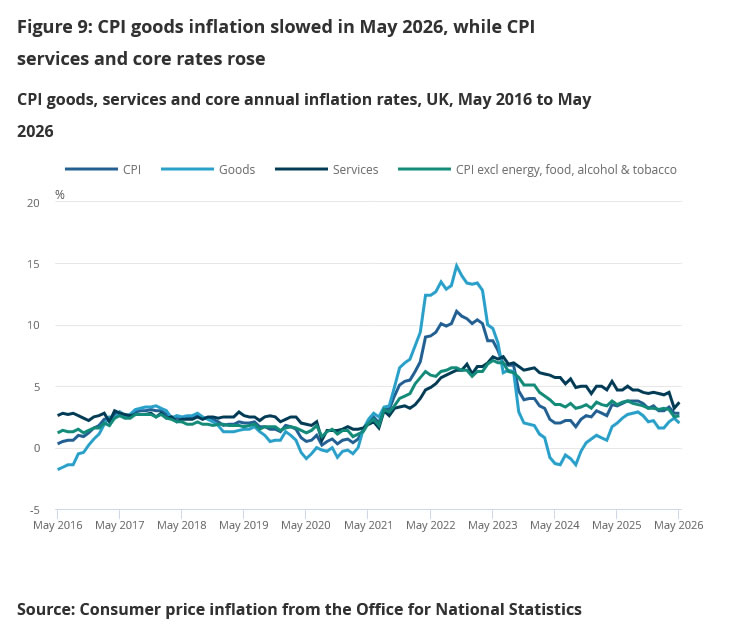

The details suggest inflation pressures are becoming increasingly concentrated in services. The annual rate for CPI goods slowed from 2.4% yoy to 2.0% yoy. In contrast, services inflation accelerated from 3.2% yoy to 3.7% yoy, highlighting the continued influence of domestic wage and labor-cost pressures. For policymakers, that divergence is likely to reinforce the view that imported and goods-related inflation is easing while underlying domestic inflation remains more persistent.

| Indicator | Apr 2026 | May 2026 | Expected |

|---|---|---|---|

| CPI M/M | 0.7% | 0.2% | 0.4% |

| CPI Y/Y | 2.8% | 2.8% | 3.0% |

| Core CPI Y/Y | 2.5% | 2.6% | 2.7% |

| CPI Goods Y/Y | 2.4% | 2.0% | |

| CPI Services Y/Y | 3.2% | 3.7% |

Producer price data painted a similarly mixed picture. Input PPI slowed from 2.6% mom to 2.4% mom and rose from 7.9% yoy to 8.7% yoy, while output PPI eased from 1.5% mom to 1.4% mom and slipped from 4.1% yoy to 4.0% yoy. Meanwhile, core output inflation slowed from 2.6% yoy to 2.3% yoy, suggesting some moderation in pipeline inflation pressures despite elevated input costs.

Overall, the report is unlikely to materially alter expectations for Thursday’s BoE decision, where rates are widely expected to remain unchanged. However, the softer-than-expected headline and core readings reduce the urgency for policymakers to move quickly toward another rate hike. While services inflation remains uncomfortably high, the broader inflation picture does not appear to be accelerating as rapidly as feared, supporting the case for patience while the Monetary Policy Committee assesses incoming data.

{kind=link}