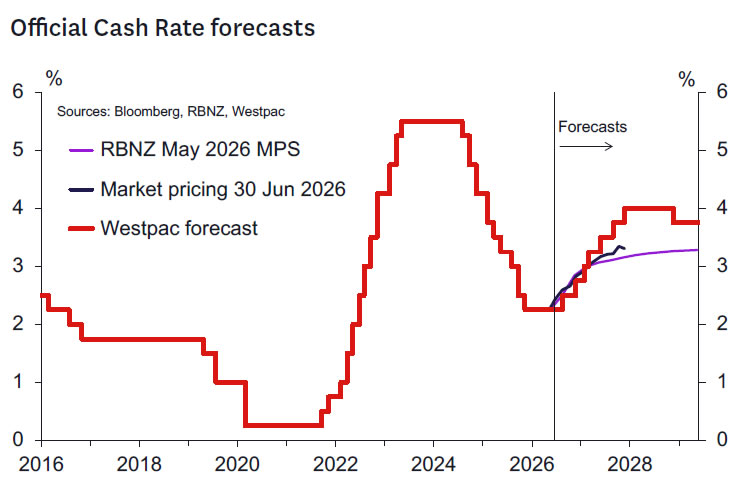

- We expect the RBNZ to leave the OCR at 2.25% at the 8 July Review.

- Much has changed over the past six weeks. Therefore, while three MPC members had voted for a rate hike in May, we think the “on hold” decision may well be reached by consensus.

- Forward guidance should remain consistent with a lift in the OCR this year. However, the message is expected to be more data dependent than came across at the May Statement.

- The press release will likely reaffirm that the timing of OCR increases will depend on what data and other developments suggest about the outlook for medium-term inflation pressures.

“What we’re saying is it’s likely we’ll see OCR hikes at coming meetings, but we’re not being, you know, exact… how much and at what meeting because we will consider, you know, the incoming data and how the inflation outlook evolves. So, if we see oil prices falling really much more than expected, if we see much much weaker growth, then we may not hike.”

– Governor Anna Breman, Heather du Plessis-Allan Drive interview, 27 May 2026

RBNZ Decision and Communication

We expect the OCR to remain at 2.25% at next week’s 8 July policy meeting. A tightening bias will remain in place that will be explicitly data dependent. In determining when that bias might be acted upon, key factors cited will be the extent of second round pricing pressures, wages pressures and evidence of increasing medium to long term inflation expectations. Evidence that the economic recovery is resuming and the output gap narrowing would also prompt policy tightening at some stage, as was the RBNZ’s forecast in the February Statement. The language pointing to OCR increases as likely in coming meetings could be kept but with a more explicit rider that these are conditional on evidence warranting those increases.

While three MPC members voted for a rate hike in May, the significant developments over the past six weeks make it quite possible that a vote is not required on this occasion. It would be perfectly reasonable for those previously hawkish members to change their view given the relatively quick resolution of the Iran tensions have caught most if not all commentators by surprise. Data dependence is a virtue not a failing in a well-functioning MPC.

Should a vote be needed, then we expect only a small minority of external members to support an OCR increase in July. We don’t think any of the doves from the May meeting will want to join the hawkish group. There is also a strong prospect that the hawks from last time will be happy to review the key data that will be released in the weeks that follow the July meeting and raise the case for an OCR rise at the September meeting, should that data support that stance.

The discussion will aim to redirect market attention on upcoming data to justify future OCR hikes. Markets became unduly fixated on a July hike after the May meeting and saw it as relatively independent of incoming data and developments in the Middle East, which was unfortunate. We expect the MPC to take the opportunity to correct that impression.

Prospects for a normalisation of the OCR will remain a feature of the RBNZ’s communication. But we expect the Bank to shift the frame of reference towards the view the MPC held pre-war. This envisaged a single OCR hike no sooner than the end of this year. As inflation is still higher than anticipated back in February, we think they will signal bringing forward of the date of lift off in the OCR to September but suggest a gradual trajectory from there if second-round inflation pressures from the Middle East supply shock remain in check. The option of consecutive increases in the OCR from September might still be a possibility but would not be presented as base case and would be dependent on data warranting a less gradual cadence of OCR increases. We don’t expect the MPC to present a September OCR increase as a given. A slow bounce back of economic activity and evidence of weak underlying inflation pressures in the June quarter CPI could justify delaying to December and thus moving the RBNZ’s stance all the way back to that communicated in the February 2026 Statement. Reintroducing data dependence into the MPC’s future decision-making framework will aim to preserve the option to push the tightening cycle back to December should data suggest that appropriate.

We expect market pricing to take a bit more out of the amount of tightening expected for 2026 and move to a situation where markets price between one and two 25bp increases by year end. From there the data will determine how market pricing evolves.

Arguments in Favour of a Hike

The most prominent argument we have heard among market participants expecting a July hike is that this was more-or-less promised in the May Statement. It’s certainly the case that the RBNZs Q3 2026 assumption of an average OCR of 2.51% is most consistent with a July hike and for some members a July hike may have been the presumption in the absence of a marked change in the inflation outlook. But we certainly don’t agree that a hike was in any way promised.

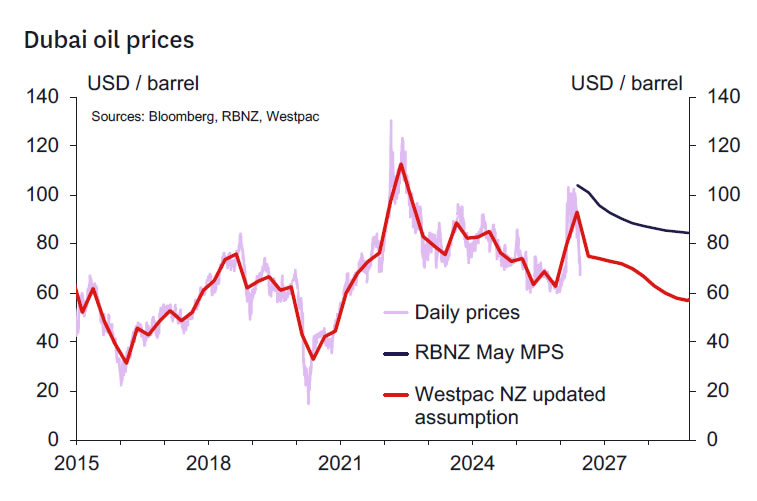

The Governor described OCR increases “in coming meetings”, which was deliberately and appropriately vague given the uncertain nature of the environment. The quote we included on the front page of this note illustrates the conditionality of the policy outlook. The Governor explicitly noted in a radio interview after the May meeting that “… if we see oil prices falling really much more than expected, if we see much much weaker growth, then we may not hike”. And in various speaking engagements the Governor has referred to a desire to see evidence of second-round pricing dynamics, rising wage pressures and increasing inflation expectations to confirm that any earlier hike in the OCR was necessary. No such evidence has accumulated since May. Similarly, in her public appearances, Assistant Governor Silk has noted that all options were on the table for the July meeting, including a “hold”. We think that the near $30/bbl decline in oil prices since the May meeting was probably beyond even the most optimistic scenario that Silk might have envisaged when she made that comment.

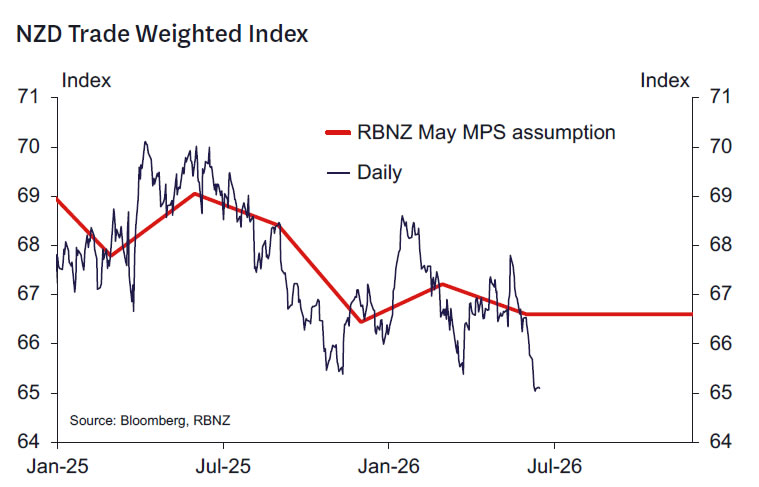

Another argument is the weakening in the exchange rate in the face of wide interest rate differentials. It is the case that the US dollar has been stronger since the FOMC shifted towards a tightening bias at their last meeting. Similarly, the Reserve Bank of Australia Board sent a message in their last meeting that cash rate increases were still possible. The associated weakening in the NZD has added to inflation pressures. But it’s still unclear how persistent these will prove to be in much the same way we don’t know how persistent energy related costs pressures will be. More generally the weaker NZD is a positive economic influence as it is assisting the competitive parts of the economy that are the key drivers of economic recovery. It’s also useful additional pressure on less competitive parts of the economy to adjust (for example import demand, the construction and real estate sectors). The risks of FX depreciation are more likely better managed by retaining the view that the OCR will eventually need to return to developed country norm levels, adjusted for risk premia, as opposed to justify what might be premature OCR increases.

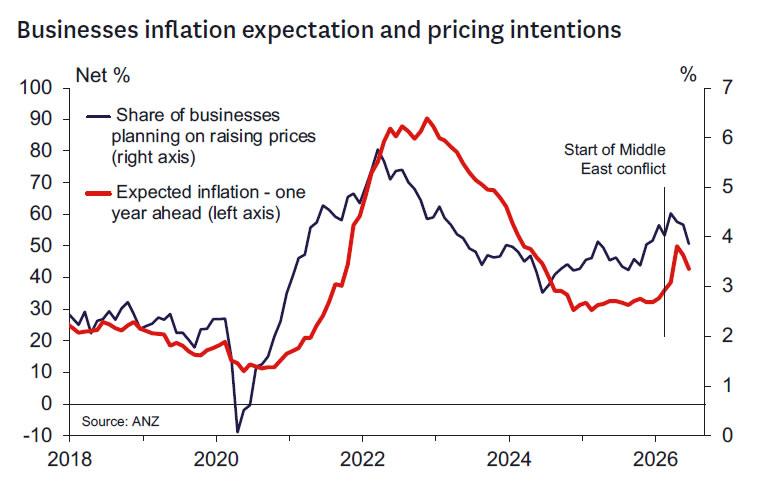

The resolution of at least some of the uncertainty associated with the Iran war will be a fillip to growth in the second half of 2026. The RBNZ has modest expectations for Q3 GDP (0.2% growth) that should be revised higher. Similarly, forecasts for later quarters could be revised higher in line with the stronger anticipated terms of trade now energy prices are lower. Business and consumer confidence, along with housing market prospects, should bounce as the Iran war uncertainty is reduced. Indeed, there is some evidence of this in today’s monthly business confidence survey that shows general business confidence rising in June. We think there is some merit to these arguments. But importantly it seems very unlikely that future upgrades to the growth outlook will be sufficient to restore the RBNZ’s February Statement growth outlook, when recall the RBNZ forecast no more than one 25bp hike in the OCR this year. Today’s business survey also shows that its very much early days in the business sector recovery given that backward looking measures of activity suggest still weakening growth momentum. Also the level of business confidence, while higher than that seen in May, is some distance below the levels seen in early 2026, when the RBNZ saw OCR increases coming at the end of 2026.

Arguments in Favour of No Change

No further evidence on second round inflation impacts, rising wages pressures or increasing inflation expectations has accumulated since the May meeting. Indeed, short term inflation expectations appear to have reduced in business and consumer surveys as energy prices have fallen and will likely continue to decline if current energy price levels are sustained. Westpac’s employment confidence survey shows a still fragile labour market that seems unlikely to support upward pressure on wages.

The Iran war has resolved (at least for now) unexpectedly quickly. A $30/bbl decline in oil prices is big news, sufficient to change the medium-term outlook, just as a $30/bbl increase was on the way up. With oil and refined fuels prices now well below the levels assumed in prior forecasts (including the RBNZ’s May forecasts), forecasts of peak and end year inflation are being revised lower. For example, Westpac now sees CPI inflation peaking a quarter earlier in the June quarter at 4% and ending 2026 at 3.5%. The risks of prolonged inflation dynamics – such as those that had clearly bothered MPC member Prasanna Gai – taking hold must have a much lower probability now compared to that contemplated back in May. Similarly risks to inflation expectations have reduced.

Importantly, further key information will be available soon. The June quarter CPI (released 21 July) will show how widespread inflation pressures are. The monthly indicators provide little insight but to the extent they do, they have shown less inflation than previously feared. The June quarter QSBO will be available in a week and will similarly provide indicators on businesses’ pricing and margins as well as activity indicators. The June quarter labour market reports due early August will shed light on the strength of the labour market and wage pressures. The best measures of inflation expectations are also available in August. This avalanche of relevant data scheduled between the July and September meetings always made a July hike a courageous move. With the sharp decline in energy prices significantly reducing the merit of pre-emptive action we suspect even the hawkish MPC members will now be content to see what this data reveals.

Activity data seemingly confirm a stagnant economy in the June quarter. Most indicators suggest little growth occurred in the June quarter, hence the output gap should have widened. Q1 GDP data was pretty much in line with RBNZ views once revisions are considered (the economy was just 0.1% larger than assumed in the May MPS).

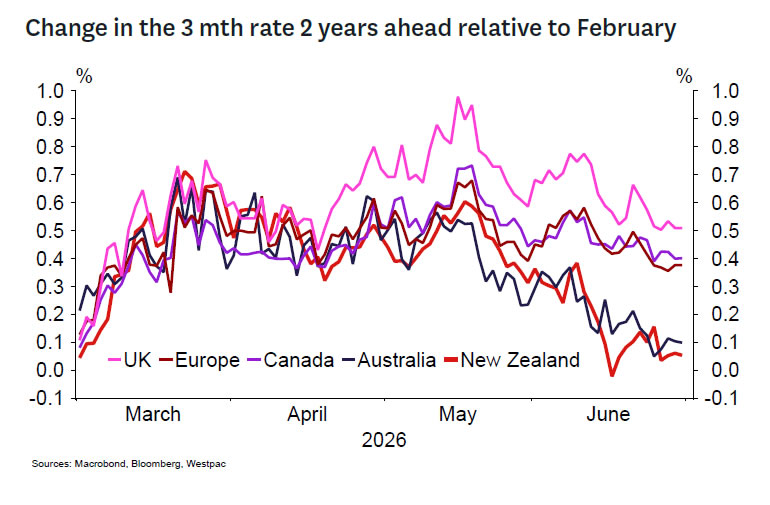

It’s also useful to remember that global views on the need for interest rate increases have generally pulled back noticeably (with the key exception of the United States). Market pricing of the expected change in 90-day rates in the coming 2 years has pulled back across most peer economies with the adjustment to Australasian interest rate expectations being greater than for most. We note that the Bank of Canada remains cool on the potential for interest rate increases this year. This is interesting as Canada seems to be the closest comparator to New Zealand in that both countries are operating with a negative output gap and have similar monetary policy frameworks.

Scenarios

More hawkish and dovish possibilities exist including:

- A hawkish scenario where the OCR is increased and language suggesting the RBNZs views haven’t shifted much. Markets would rationally assume at least 3, possibly 4 hikes in aggregate for 2026. We see this as implausible and assign a 10% probability to it.

- A dovish scenario that seriously questions a hike before December. The forward guidance could be omitted noting that inflation risks seem much less prominent relative to the still large level of excess capacity. Evidence of strong core inflation and broadening second-round inflation pressures would need to be seen to justify a lift in the OCR, and the statement could note that such evidence is lacking at this stage. The February MPS forecasts could be explicitly referred to as being nearer to the MPC’s current frame of reference. This is more plausible and we attach a 30% probability to this scenario.

Kelly’s Take

This is an easy decision. While I advocated for an increase in May, there seems much to be gained from waiting to see the outcome of the June quarter CPI. Certainly, the risks of prolonged second-round price impacts are lower than thought earlier given the Iran conflict seems to have resolved much sooner than expected and energy prices have declined far sooner than expected.

Higher interest rates are in prospect in time. But the urgency to begin the process now when such critical evidence is available just around the corner is gone. I suspect a gradual approach of 25bp increases in September and December should prove sufficient for now. The economy will continue to recover through the second half of the year, calling for a return of the OCR to hopefully not much higher than neutral levels (in the high 3s in my view) next year.

I see the risk that the exchange rate will depreciate further over the balance of the year given steep negative interest rate differentials. But if this occurs, this will aid the needed rebalancing of the economy. The market needs to be reminded of the importance of data dependence in determining future OCR adjustments.

{kind=link}