Sterling’s rally has been about more than better sentiment toward the UK. It has been driven by the disappearance of one of the market’s biggest bearish trades. As political uncertainty faded following the resolution of Labour’s leadership transition, investors who had built sizeable short Sterling positions found themselves on the wrong side of the market. That process is still unfolding, helping explain why Sterling has outperformed most clearly in the crosses rather than against the Dollar alone.

Before UK Prime Minister Keir Starmer’s resignation, political uncertainty encouraged investors to build substantial bearish positions against Sterling. The decisive outcome of the Makerfield by-election on June 18 removed much of that uncertainty far more quickly than markets had anticipated. For traders who had sold Sterling on expectations of a prolonged political transition, the rationale for the trade weakened almost overnight.

What followed was not necessarily a wave of fresh optimism toward the UK economy but a mechanical process of buying Sterling back. Société Générale estimates speculative accounts were still holding short positions equivalent to 35.5% of open interest as of late June. Although some of those positions have already been unwound, the bank argues the remaining short base is still large enough to support further gains as investors continue to close bearish trades.

At the same time, the fundamental backdrop has quietly become more supportive. Bank of England Governor Andrew Bailey has pushed back against expectations for early policy easing, suggesting interest rates may need to stay restrictive to ensure the inflationary effects of this year’s oil shock fully dissipate. With Bank Rate still at 3.75%, Sterling retains a sizeable yield advantage over the Swiss Franc (0.00%), Euro (2.25%) and Japanese Yen (1.00%), providing an additional incentive for investors to hold the currency.

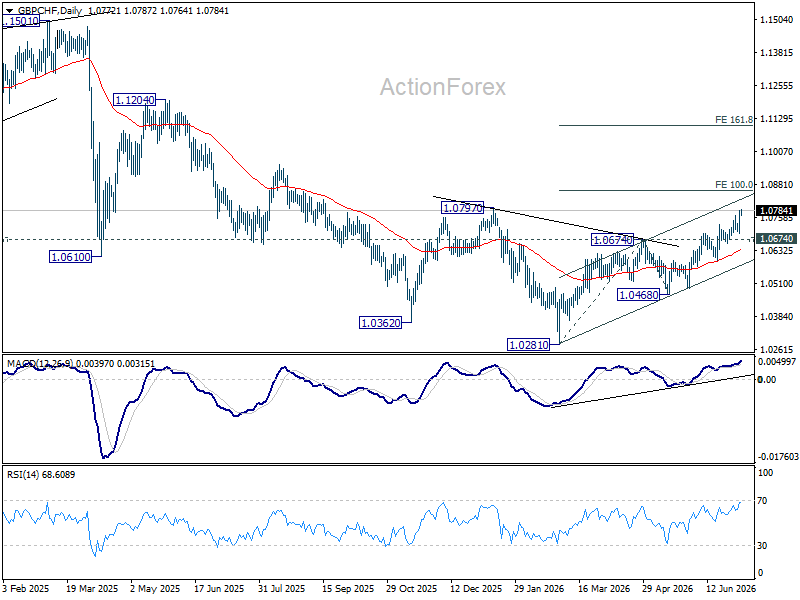

Those macro and positioning forces are now converging at a technically significant moment. GBP/CHF has resumed its advance from the March low at 1.0281 and is approaching the important resistance zone around 1.08. Provided support at 1.0674 holds, the path of least resistance continues to point higher.

The importance of this zone extends well beyond a simple breakout. A decisive move above 1.0797 would break the medium-term downtrend that has been in place since the 2024 peak at 1.1675. A subsequent break above 100% projection of 1.0821 to 1.0674 from 1.0468 at 1.0861 would reinforce the view that the recovery has transitioned from a corrective rebound into a new impulsive advance, increasing the likelihood of an acceleration toward 161.8% projection at 1.1104.

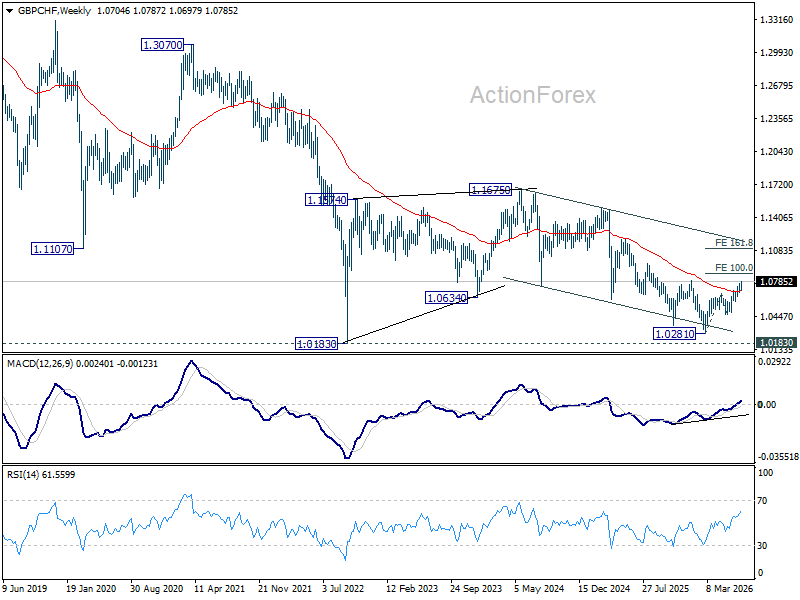

The longer-term technical backdrop is also improving. GBP/CHF has reclaimed its 55 W EMA (now at 1.0689) and successfully defended the major low at 1.0183 established in 2022. Combined with the ongoing unwinding of Sterling shorts and the Bank of England’s relatively restrictive policy stance, the technical picture suggests Sterling’s recent strength could mark the beginning of a broader medium-term reversal rather than simply another short-lived rebound.

{kind=link}